Gina Tricot Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

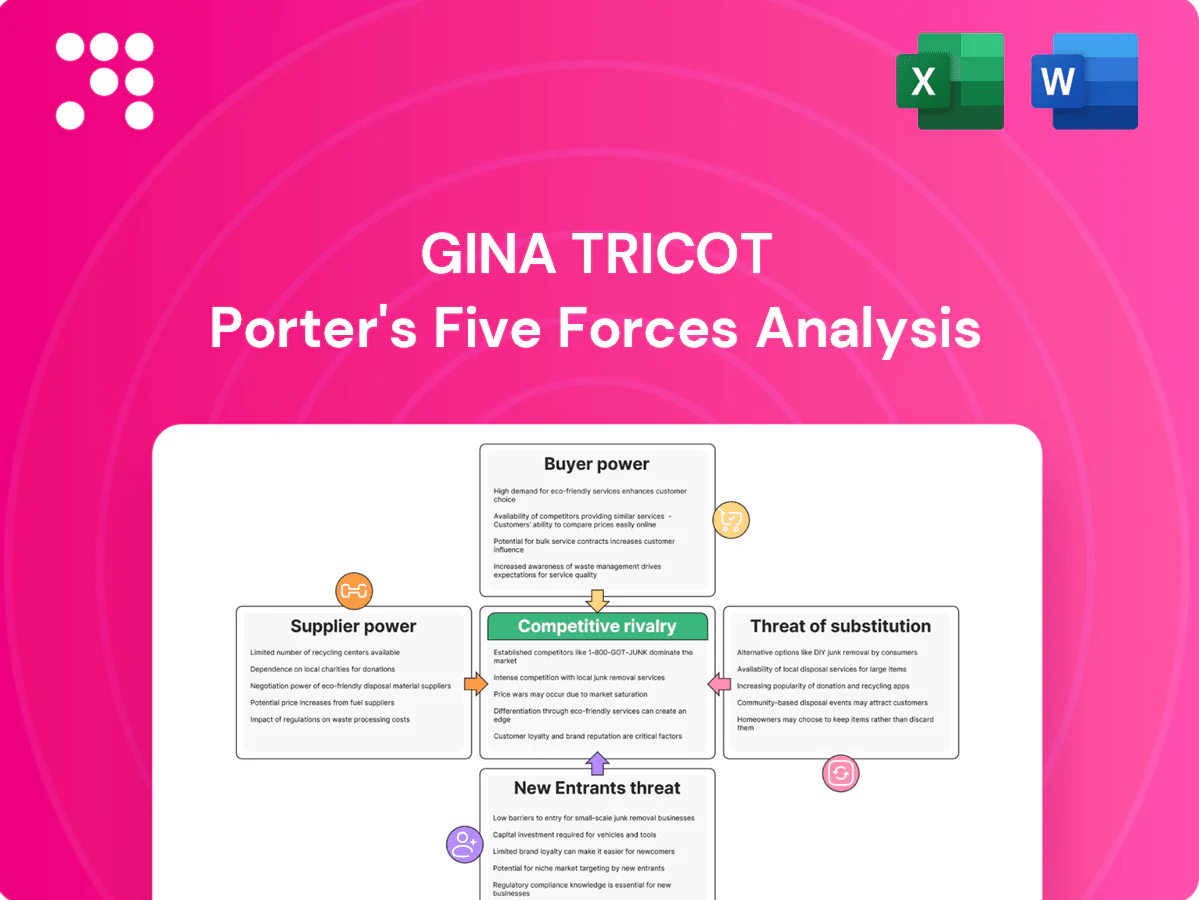

Gina Tricot's Porter's Five Forces highlights intense retail rivalry, moderate buyer power, constrained supplier leverage, and evolving threats from fast-fashion substitutes and new entrants. This snapshot teases key competitive dynamics and strategic pressure points. Ready for actionable depth? Unlock the full Porter's Five Forces Analysis to explore Gina Tricot’s market risks and opportunities in detail.

Suppliers Bargaining Power

Fragmented apparel sourcing

Global garment supply is highly fragmented—ILO estimates about 60 million garment workers worldwide—so a mid-sized chain like Gina Tricot can keep switching options open and dual-source to reduce factory dependence. This fragmentation generally suppresses supplier pricing power and bargaining leverage. However, demand for specialized materials or small-batch trend drops can create localized capacity tightness and temporarily raise supplier leverage.

Input cost volatility

Fluctuations in cotton and synthetics—cotton futures moved roughly 8% higher in 2024 versus 2023—together with freight volatility (SCFI levels down about 60% from 2021 peaks but still prone to spikes) strengthen suppliers’ bargaining stance during tight cycles, as vendors can rapidly pass through costs on short lead-time orders.

Gina Tricot therefore needs financial hedging and flexible supplier contracts to dampen price shocks, while long-term relationships and volume commitments can secure better terms and mitigate input-cost risk.

Lead-time sensitivity

Fast trend refresh (Inditex launches new styles twice weekly) shrinks tolerance for delays, giving timely suppliers leverage as retailers push styles on 12–16 week Asian lead-time backdrops. Priority production slots command premiums, especially in Q3/Q4 peak windows. Expanding nearshore capacity (cutting lead times toward 2–6 weeks) and strict calendar discipline with improved forecasting reduce rush-order dependence and supplier power.

Compliance and sustainability

Rising ESG standards—driven by EU rules like the CSRD extending to ~50,000 firms in 2024—increase the pool of certified factories, boosting bargaining power for compliant suppliers; audits and traceability systems raise unit costs that suppliers may seek to pass on. Collaborating on multi-year compliance roadmaps lets Gina Tricot trade slightly higher prices for supply stability and lower interruption risk. Clear codes of conduct enable measured vendor diversification without brand damage.

- Suppliers certified: higher leverage

- Audit/traceability add recoverable costs

- Partnerships trade price for stability

- Code-of-conducts preserve brand, enable diversification

Technology and MOQs

Low minimum order quantities for fast-turn capsules often push unit prices higher; 2024 industry surveys report small-run premiums up to 20% which increases supplier leverage. Digital product creation and shared PLM data have cut sampling cycles by ~30% in 2024, improving purchasing visibility and negotiation leverage. Consolidating SKUs into core fabrics lowers composite MOQs over time, while strategic capacity reservations trade 1–3% higher holding cost for 48–72 hour replenishment agility.

- MOQ premium: up to 20% (2024)

- PLM/sample cycle reduction: ~30% (2024)

- SKU consolidation: reduces aggregate MOQs

- Capacity reservations: +1–3% cost for 48–72h agility

Nearshore agility boosts vendor leverage: cotton +8%, small-run premiums up to 20%

Global garment fragmentation (ILO ~60m workers) limits supplier power, but cotton +8% in 2024, SCFI volatility (down ~60% from 2021) and small-run premiums up to 20% raise leverage for timely or certified vendors. PLM/sample cycles -30% (2024) and nearshore 2–6wk vs Asian 12–16wk shift negotiation dynamics; capacity reservations cost +1–3% for 48–72h agility.

| Metric | Value |

|---|---|

| Garment workers (ILO) | 60m |

| Cotton 2024 vs 2023 | +8% |

| SCFI vs 2021 peak | -60% |

| Small-run premium | up to 20% |

| PLM/sample cycle | -30% |

| Nearshore lead-time | 2–6 weeks |

| Asian lead-time | 12–16 weeks |

| Capacity reservation cost | +1–3% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Gina Tricot; evaluates supplier and buyer power, substitutes, and disruptive threats to its market share. Detailed strategic commentary—fully editable Word format for use in investor materials, strategy decks, or academic projects.

Clear, one-sheet Porter’s Five Forces for Gina Tricot—instantly clarifies competitive pressure and supplier/buyer dynamics to speed board decisions; customizable scores and a radar chart make scenario planning and slide-ready summaries effortless.

Customers Bargaining Power

Price-sensitive fashion shoppers

Accessible pricing at Gina Tricot attracts value-driven, deal-seeking shoppers, pressuring ASPs as the brand—operating c.160 Nordic stores in 2024—competes on affordability.

Easy online comparison across rivals increases buyer leverage, forcing disciplined promotions; excess discounting risks eroding already-thin fast-fashion gross margins.

Targeted loyalty mechanics and a clear value-for-money messaging can temper discount expectations and protect margin resilience.

Omnichannel transparency

Omnichannel transparency gives Gina Tricot customers strong leverage: visible online and in‑store prices and reviews mean poor experiences prompt switching, while 2024 fashion e‑commerce return rates near 30% and omnichannel shoppers spending roughly 3x amplify this power; harmonized pricing and free, easy returns cut churn, and data‑driven personalization in 2024 shows measurable lift in perceived value, lowering price elasticity.

Low switching costs

Fast-fashion buyers switch brands effortlessly to chase trends and fit, a dynamic underscored by industry scale—H&M Group reported SEK 199.5 billion in net sales for 2023—which intensifies competition and limits differentiation in basics, elevating buyer power. Exclusive collaborations and curated edits, used by Gina Tricot, increase switching frictions. Consistent sizing and reliable quality build repeat-purchase stickiness.

Trend immediacy expectations

Customers now demand near-instant availability of current looks, and stock-outs or slow refresh cycles trigger immediate defection to competitors; tight buy-plans and responsive replenishment are essential to curb churn. Capsule drops and deliberate scarcity reframe urgency while limiting inventory risk, shifting power back toward the retailer when executed with rapid omnichannel fulfillment.

- Trend immediacy: drives fast defection

- Tight buy-plans: reduce overstock & dissatisfaction

- Responsive replenishment: essential for retention

- Capsule drops: create urgency, control inventory

Return and service norms

Industry-standard free returns raise buyer leverage and add costs: online fashion return rates averaged 20–30% in 2024, with returns eating into as much as 5–10% of revenue and costing roughly €10 per return; seamless customer service is baseline, not a differentiator, while clear fit guidance and rich product content materially lower return rates, and proactive post-purchase communication sustains loyalty.

- Free returns increase leverage and costs

- Seamless service = table stakes

- Fit guidance + rich content reduce returns

- Proactive post-purchase comms sustain loyalty

c.160 Nordic stores, ~30% returns; omnichannel buyers spend ~3x

Accessible pricing and c.160 Nordic stores (2024) heighten price sensitivity and comparison shopping. Omnichannel visibility and ~30% return rates (2024) boost switching; omnichannel shoppers spend ~3x. Free returns (~€10; 5–10% revenue hit) increase buyer leverage; loyalty and personalization reduce churn.

| Metric | Value | Impact |

|---|---|---|

| Stores | c.160 (2024) | Broader reach, price competition |

| Return rate | ~30% (2024) | Higher costs, easier switching |

| Omnichannel spend | ~3x | Concentrated revenue |

| Return cost | ~€10 | 5–10% revenue drag |

Preview the Actual Deliverable

Gina Tricot Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Gina Tricot you'll receive immediately after purchase—no surprises, no placeholders. It covers threat of new entrants, bargaining power of buyers and suppliers, threat of substitutes, and competitive rivalry with data-driven insights and strategic implications. The file is professionally formatted and ready for download and use the moment you buy.

Go Beyond the Preview—Access the Full Strategic Report

Gina Tricot's Porter's Five Forces highlights intense retail rivalry, moderate buyer power, constrained supplier leverage, and evolving threats from fast-fashion substitutes and new entrants. This snapshot teases key competitive dynamics and strategic pressure points. Ready for actionable depth? Unlock the full Porter's Five Forces Analysis to explore Gina Tricot’s market risks and opportunities in detail.

Suppliers Bargaining Power

Fragmented apparel sourcing

Global garment supply is highly fragmented—ILO estimates about 60 million garment workers worldwide—so a mid-sized chain like Gina Tricot can keep switching options open and dual-source to reduce factory dependence. This fragmentation generally suppresses supplier pricing power and bargaining leverage. However, demand for specialized materials or small-batch trend drops can create localized capacity tightness and temporarily raise supplier leverage.

Input cost volatility

Fluctuations in cotton and synthetics—cotton futures moved roughly 8% higher in 2024 versus 2023—together with freight volatility (SCFI levels down about 60% from 2021 peaks but still prone to spikes) strengthen suppliers’ bargaining stance during tight cycles, as vendors can rapidly pass through costs on short lead-time orders.

Gina Tricot therefore needs financial hedging and flexible supplier contracts to dampen price shocks, while long-term relationships and volume commitments can secure better terms and mitigate input-cost risk.

Lead-time sensitivity

Fast trend refresh (Inditex launches new styles twice weekly) shrinks tolerance for delays, giving timely suppliers leverage as retailers push styles on 12–16 week Asian lead-time backdrops. Priority production slots command premiums, especially in Q3/Q4 peak windows. Expanding nearshore capacity (cutting lead times toward 2–6 weeks) and strict calendar discipline with improved forecasting reduce rush-order dependence and supplier power.

Compliance and sustainability

Rising ESG standards—driven by EU rules like the CSRD extending to ~50,000 firms in 2024—increase the pool of certified factories, boosting bargaining power for compliant suppliers; audits and traceability systems raise unit costs that suppliers may seek to pass on. Collaborating on multi-year compliance roadmaps lets Gina Tricot trade slightly higher prices for supply stability and lower interruption risk. Clear codes of conduct enable measured vendor diversification without brand damage.

- Suppliers certified: higher leverage

- Audit/traceability add recoverable costs

- Partnerships trade price for stability

- Code-of-conducts preserve brand, enable diversification

Technology and MOQs

Low minimum order quantities for fast-turn capsules often push unit prices higher; 2024 industry surveys report small-run premiums up to 20% which increases supplier leverage. Digital product creation and shared PLM data have cut sampling cycles by ~30% in 2024, improving purchasing visibility and negotiation leverage. Consolidating SKUs into core fabrics lowers composite MOQs over time, while strategic capacity reservations trade 1–3% higher holding cost for 48–72 hour replenishment agility.

- MOQ premium: up to 20% (2024)

- PLM/sample cycle reduction: ~30% (2024)

- SKU consolidation: reduces aggregate MOQs

- Capacity reservations: +1–3% cost for 48–72h agility

Nearshore agility boosts vendor leverage: cotton +8%, small-run premiums up to 20%

Global garment fragmentation (ILO ~60m workers) limits supplier power, but cotton +8% in 2024, SCFI volatility (down ~60% from 2021) and small-run premiums up to 20% raise leverage for timely or certified vendors. PLM/sample cycles -30% (2024) and nearshore 2–6wk vs Asian 12–16wk shift negotiation dynamics; capacity reservations cost +1–3% for 48–72h agility.

| Metric | Value |

|---|---|

| Garment workers (ILO) | 60m |

| Cotton 2024 vs 2023 | +8% |

| SCFI vs 2021 peak | -60% |

| Small-run premium | up to 20% |

| PLM/sample cycle | -30% |

| Nearshore lead-time | 2–6 weeks |

| Asian lead-time | 12–16 weeks |

| Capacity reservation cost | +1–3% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Gina Tricot; evaluates supplier and buyer power, substitutes, and disruptive threats to its market share. Detailed strategic commentary—fully editable Word format for use in investor materials, strategy decks, or academic projects.

Clear, one-sheet Porter’s Five Forces for Gina Tricot—instantly clarifies competitive pressure and supplier/buyer dynamics to speed board decisions; customizable scores and a radar chart make scenario planning and slide-ready summaries effortless.

Customers Bargaining Power

Price-sensitive fashion shoppers

Accessible pricing at Gina Tricot attracts value-driven, deal-seeking shoppers, pressuring ASPs as the brand—operating c.160 Nordic stores in 2024—competes on affordability.

Easy online comparison across rivals increases buyer leverage, forcing disciplined promotions; excess discounting risks eroding already-thin fast-fashion gross margins.

Targeted loyalty mechanics and a clear value-for-money messaging can temper discount expectations and protect margin resilience.

Omnichannel transparency

Omnichannel transparency gives Gina Tricot customers strong leverage: visible online and in‑store prices and reviews mean poor experiences prompt switching, while 2024 fashion e‑commerce return rates near 30% and omnichannel shoppers spending roughly 3x amplify this power; harmonized pricing and free, easy returns cut churn, and data‑driven personalization in 2024 shows measurable lift in perceived value, lowering price elasticity.

Low switching costs

Fast-fashion buyers switch brands effortlessly to chase trends and fit, a dynamic underscored by industry scale—H&M Group reported SEK 199.5 billion in net sales for 2023—which intensifies competition and limits differentiation in basics, elevating buyer power. Exclusive collaborations and curated edits, used by Gina Tricot, increase switching frictions. Consistent sizing and reliable quality build repeat-purchase stickiness.

Trend immediacy expectations

Customers now demand near-instant availability of current looks, and stock-outs or slow refresh cycles trigger immediate defection to competitors; tight buy-plans and responsive replenishment are essential to curb churn. Capsule drops and deliberate scarcity reframe urgency while limiting inventory risk, shifting power back toward the retailer when executed with rapid omnichannel fulfillment.

- Trend immediacy: drives fast defection

- Tight buy-plans: reduce overstock & dissatisfaction

- Responsive replenishment: essential for retention

- Capsule drops: create urgency, control inventory

Return and service norms

Industry-standard free returns raise buyer leverage and add costs: online fashion return rates averaged 20–30% in 2024, with returns eating into as much as 5–10% of revenue and costing roughly €10 per return; seamless customer service is baseline, not a differentiator, while clear fit guidance and rich product content materially lower return rates, and proactive post-purchase communication sustains loyalty.

- Free returns increase leverage and costs

- Seamless service = table stakes

- Fit guidance + rich content reduce returns

- Proactive post-purchase comms sustain loyalty

c.160 Nordic stores, ~30% returns; omnichannel buyers spend ~3x

Accessible pricing and c.160 Nordic stores (2024) heighten price sensitivity and comparison shopping. Omnichannel visibility and ~30% return rates (2024) boost switching; omnichannel shoppers spend ~3x. Free returns (~€10; 5–10% revenue hit) increase buyer leverage; loyalty and personalization reduce churn.

| Metric | Value | Impact |

|---|---|---|

| Stores | c.160 (2024) | Broader reach, price competition |

| Return rate | ~30% (2024) | Higher costs, easier switching |

| Omnichannel spend | ~3x | Concentrated revenue |

| Return cost | ~€10 | 5–10% revenue drag |

Preview the Actual Deliverable

Gina Tricot Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Gina Tricot you'll receive immediately after purchase—no surprises, no placeholders. It covers threat of new entrants, bargaining power of buyers and suppliers, threat of substitutes, and competitive rivalry with data-driven insights and strategic implications. The file is professionally formatted and ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Gina Tricot's Porter's Five Forces highlights intense retail rivalry, moderate buyer power, constrained supplier leverage, and evolving threats from fast-fashion substitutes and new entrants. This snapshot teases key competitive dynamics and strategic pressure points. Ready for actionable depth? Unlock the full Porter's Five Forces Analysis to explore Gina Tricot’s market risks and opportunities in detail.

Suppliers Bargaining Power

Fragmented apparel sourcing

Global garment supply is highly fragmented—ILO estimates about 60 million garment workers worldwide—so a mid-sized chain like Gina Tricot can keep switching options open and dual-source to reduce factory dependence. This fragmentation generally suppresses supplier pricing power and bargaining leverage. However, demand for specialized materials or small-batch trend drops can create localized capacity tightness and temporarily raise supplier leverage.

Input cost volatility

Fluctuations in cotton and synthetics—cotton futures moved roughly 8% higher in 2024 versus 2023—together with freight volatility (SCFI levels down about 60% from 2021 peaks but still prone to spikes) strengthen suppliers’ bargaining stance during tight cycles, as vendors can rapidly pass through costs on short lead-time orders.

Gina Tricot therefore needs financial hedging and flexible supplier contracts to dampen price shocks, while long-term relationships and volume commitments can secure better terms and mitigate input-cost risk.

Lead-time sensitivity

Fast trend refresh (Inditex launches new styles twice weekly) shrinks tolerance for delays, giving timely suppliers leverage as retailers push styles on 12–16 week Asian lead-time backdrops. Priority production slots command premiums, especially in Q3/Q4 peak windows. Expanding nearshore capacity (cutting lead times toward 2–6 weeks) and strict calendar discipline with improved forecasting reduce rush-order dependence and supplier power.

Compliance and sustainability

Rising ESG standards—driven by EU rules like the CSRD extending to ~50,000 firms in 2024—increase the pool of certified factories, boosting bargaining power for compliant suppliers; audits and traceability systems raise unit costs that suppliers may seek to pass on. Collaborating on multi-year compliance roadmaps lets Gina Tricot trade slightly higher prices for supply stability and lower interruption risk. Clear codes of conduct enable measured vendor diversification without brand damage.

- Suppliers certified: higher leverage

- Audit/traceability add recoverable costs

- Partnerships trade price for stability

- Code-of-conducts preserve brand, enable diversification

Technology and MOQs

Low minimum order quantities for fast-turn capsules often push unit prices higher; 2024 industry surveys report small-run premiums up to 20% which increases supplier leverage. Digital product creation and shared PLM data have cut sampling cycles by ~30% in 2024, improving purchasing visibility and negotiation leverage. Consolidating SKUs into core fabrics lowers composite MOQs over time, while strategic capacity reservations trade 1–3% higher holding cost for 48–72 hour replenishment agility.

- MOQ premium: up to 20% (2024)

- PLM/sample cycle reduction: ~30% (2024)

- SKU consolidation: reduces aggregate MOQs

- Capacity reservations: +1–3% cost for 48–72h agility

Nearshore agility boosts vendor leverage: cotton +8%, small-run premiums up to 20%

Global garment fragmentation (ILO ~60m workers) limits supplier power, but cotton +8% in 2024, SCFI volatility (down ~60% from 2021) and small-run premiums up to 20% raise leverage for timely or certified vendors. PLM/sample cycles -30% (2024) and nearshore 2–6wk vs Asian 12–16wk shift negotiation dynamics; capacity reservations cost +1–3% for 48–72h agility.

| Metric | Value |

|---|---|

| Garment workers (ILO) | 60m |

| Cotton 2024 vs 2023 | +8% |

| SCFI vs 2021 peak | -60% |

| Small-run premium | up to 20% |

| PLM/sample cycle | -30% |

| Nearshore lead-time | 2–6 weeks |

| Asian lead-time | 12–16 weeks |

| Capacity reservation cost | +1–3% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Gina Tricot; evaluates supplier and buyer power, substitutes, and disruptive threats to its market share. Detailed strategic commentary—fully editable Word format for use in investor materials, strategy decks, or academic projects.

Clear, one-sheet Porter’s Five Forces for Gina Tricot—instantly clarifies competitive pressure and supplier/buyer dynamics to speed board decisions; customizable scores and a radar chart make scenario planning and slide-ready summaries effortless.

Customers Bargaining Power

Price-sensitive fashion shoppers

Accessible pricing at Gina Tricot attracts value-driven, deal-seeking shoppers, pressuring ASPs as the brand—operating c.160 Nordic stores in 2024—competes on affordability.

Easy online comparison across rivals increases buyer leverage, forcing disciplined promotions; excess discounting risks eroding already-thin fast-fashion gross margins.

Targeted loyalty mechanics and a clear value-for-money messaging can temper discount expectations and protect margin resilience.

Omnichannel transparency

Omnichannel transparency gives Gina Tricot customers strong leverage: visible online and in‑store prices and reviews mean poor experiences prompt switching, while 2024 fashion e‑commerce return rates near 30% and omnichannel shoppers spending roughly 3x amplify this power; harmonized pricing and free, easy returns cut churn, and data‑driven personalization in 2024 shows measurable lift in perceived value, lowering price elasticity.

Low switching costs

Fast-fashion buyers switch brands effortlessly to chase trends and fit, a dynamic underscored by industry scale—H&M Group reported SEK 199.5 billion in net sales for 2023—which intensifies competition and limits differentiation in basics, elevating buyer power. Exclusive collaborations and curated edits, used by Gina Tricot, increase switching frictions. Consistent sizing and reliable quality build repeat-purchase stickiness.

Trend immediacy expectations

Customers now demand near-instant availability of current looks, and stock-outs or slow refresh cycles trigger immediate defection to competitors; tight buy-plans and responsive replenishment are essential to curb churn. Capsule drops and deliberate scarcity reframe urgency while limiting inventory risk, shifting power back toward the retailer when executed with rapid omnichannel fulfillment.

- Trend immediacy: drives fast defection

- Tight buy-plans: reduce overstock & dissatisfaction

- Responsive replenishment: essential for retention

- Capsule drops: create urgency, control inventory

Return and service norms

Industry-standard free returns raise buyer leverage and add costs: online fashion return rates averaged 20–30% in 2024, with returns eating into as much as 5–10% of revenue and costing roughly €10 per return; seamless customer service is baseline, not a differentiator, while clear fit guidance and rich product content materially lower return rates, and proactive post-purchase communication sustains loyalty.

- Free returns increase leverage and costs

- Seamless service = table stakes

- Fit guidance + rich content reduce returns

- Proactive post-purchase comms sustain loyalty

c.160 Nordic stores, ~30% returns; omnichannel buyers spend ~3x

Accessible pricing and c.160 Nordic stores (2024) heighten price sensitivity and comparison shopping. Omnichannel visibility and ~30% return rates (2024) boost switching; omnichannel shoppers spend ~3x. Free returns (~€10; 5–10% revenue hit) increase buyer leverage; loyalty and personalization reduce churn.

| Metric | Value | Impact |

|---|---|---|

| Stores | c.160 (2024) | Broader reach, price competition |

| Return rate | ~30% (2024) | Higher costs, easier switching |

| Omnichannel spend | ~3x | Concentrated revenue |

| Return cost | ~€10 | 5–10% revenue drag |

Preview the Actual Deliverable

Gina Tricot Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Gina Tricot you'll receive immediately after purchase—no surprises, no placeholders. It covers threat of new entrants, bargaining power of buyers and suppliers, threat of substitutes, and competitive rivalry with data-driven insights and strategic implications. The file is professionally formatted and ready for download and use the moment you buy.