Givaudan PESTLE Analysis

Your Competitive Advantage Starts with This Report

Understand how regulatory, economic and technological shifts are shaping Givaudan’s future and competitive position. This concise PESTLE highlights key risks and growth opportunities for investors, consultants, and strategists. Purchase the full, editable analysis to unlock detailed, actionable insights now.

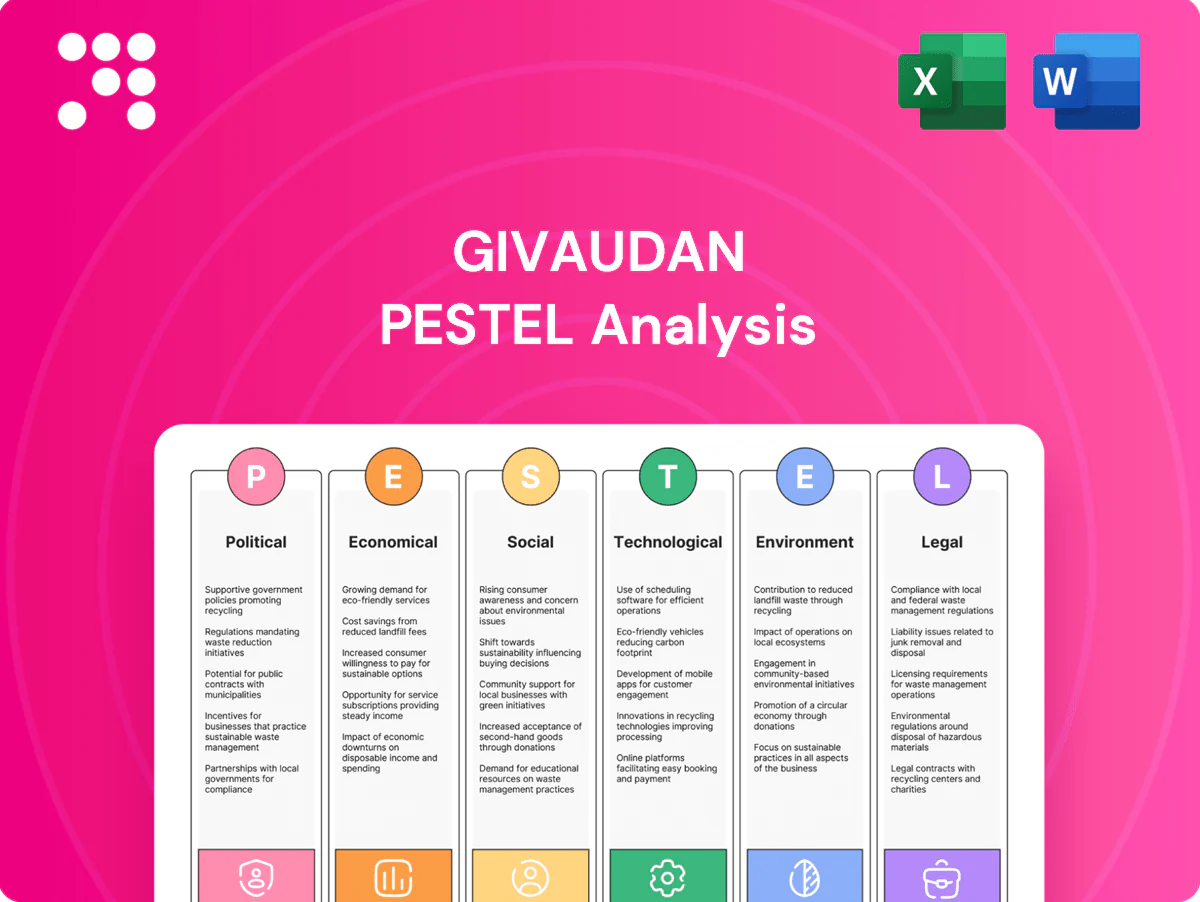

Political factors

Geopolitics and trade policy

Sanctions, tariffs and export controls can disrupt ingredient flows and raise costs for fragrances and flavors; US tariffs on Chinese goods introduced since 2018 still cover roughly 60% of imports by value, affecting aroma-chemical sourcing. EU trade defenses and shifting 2024 tariff schedules increased supplier costs. Givaudan, with 2024 sales exceeding CHF 7bn, must hedge exposure, diversify suppliers and routes, and use proactive customs planning and dual-sourcing to reduce political risk.

Instability in key sourcing regions

Vanilla from Madagascar, which supplies roughly 80% of the global market, and citrus sourced from major Latin American producers like Brazil face political and social volatility that can trigger supply shocks and sharp price spikes. Elections, strikes or governance issues have repeatedly disrupted flows, so Givaudan leans on local engagement and community projects to stabilize supplier relationships. Inventory buffers and long-term contracts are used to mitigate disruption risk.

EU Green Deal and policy steering

EU Green Deal policy pushes decarbonization, Farm to Fork targets 50% pesticide reduction by 2030 and the 2023 Chemical Strategy tightens hazardous substance use; CBAM began phasing in 2023. Funding and rules shape R&D and plant retrofits via instruments like Horizon Europe (€95.5bn 2021–27) and the EU’s stated ~€1tn green investment target. Compliance raises capex but rewards early movers; Givaudan can reorient pipelines to capture policy-linked incentives.

Swiss political context and market access

As a Swiss company, bilateral accords with the EU and regulatory equivalence are key for frictionless trade; changes to mutual recognition can force extra testing and conformity costs. Stable Swiss governance supports long-term planning. Givaudan reported CHF 8.6bn sales in 2024 and, given the EU accounts for roughly 50% of Swiss exports, its strategic EU footprint helps safeguard market access.

- Bilateral accords affect tariffs and regulatory checks

- Mutual recognition changes increase testing/conformity costs

- Stable Swiss governance aids long-term investment

- EU footprint mitigates market-access risk

Food security and agricultural policy

Subsidies, quotas and sustainability mandates reshape availability and prices for botanicals, increasing input-cost volatility for Givaudan. The EU Deforestation Regulation, adopted 2023, and similar rules worldwide are tightening traceability for cocoa, coffee, palm, soy, rubber, wood, cattle and maize. Givaudan leverages its Sourcing4Good program and farmer partnerships to meet policy-driven standards and de-risk supply.

- Policy-driven price/availability shocks

- EUDR 2023 intensifies traceability

- Tighter global import requirements

- Farmer partnerships via Sourcing4Good

Tariffs, EU green rules raise aroma-chemical costs; Madagascar supplies ~80% of vanilla

Political risks—tariffs, sanctions and trade controls (US tariffs cover ~60% of Chinese imports) and EU trade defenses—raise aroma-chemical costs and force supplier diversification; Givaudan reported CHF 8.6bn sales in 2024 and sources ~80% of global vanilla from Madagascar. EU Green Deal, EUDR 2023 and CBAM raise compliance capex; Swiss-EU relations and Sourcing4Good mitigate supply shocks.

| Metric | Value |

|---|---|

| 2024 sales | CHF 8.6bn |

| Vanilla global supply from Madagascar | ~80% |

| US tariffs on China (imports by value) | ~60% |

| EU share of Swiss exports | ~50% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely shape Givaudan’s flavor & fragrance business, linking current market and regulatory trends to risks and opportunities; data-backed, forward-looking insights support executives, investors and strategists in scenario planning and investor-ready reporting.

Provides a concise, visually segmented PESTLE summary of Givaudan that can be dropped into presentations or shared across teams to quickly align on external risks, market positioning, and strategic implications.

Economic factors

FMCG demand cycles and pricing

FMCG demand for flavors and fragrances tracks staples volumes and premiumization: Givaudan reported FY2024 net sales of CHF 9.1bn, reflecting resilience in staples-led categories. In downturns volumes hold but mix can downshift; in upturns innovation boosts margins. Pricing power typically offsets input inflation with a lag, and customer contract terms dictate pass-through speed.

Raw material volatility

Raw material costs for Givaudan—citrus oils, vanillin, petrochemical derivatives and solvents—move with harvest cycles and energy; Brent crude averaged about 86 USD/barrel in 2024, fueling solvent and feedstock swings. Supply shocks can compress margins ahead of contract repricing, while diversification into biotech and captive formulations lowers exposure. Strategic inventories and supplier alliances further stabilize input costs.

Currency exposure (CHF, USD, EUR)

Givaudan reports in Swiss francs while generating over 95% of revenue outside Switzerland, creating material CHF, USD and EUR translation exposure. FX moves alter competitiveness as costs and reporting remain Swiss-franc-centric, so natural hedges from local production and currency-matched sales are important. The company uses derivatives and active treasury management to limit volatility. A balanced regional footprint further reduces single-currency risk.

M&A and scale advantages

Consolidation lets Givaudan expand portfolio, leverage R&D and cross-sell to multinationals; as the world’s largest fragrance and flavor company (2023 sales CHF 7.9bn, ~25% market share) scale drives margin and innovation leverage. Integration execution determines synergy capture and timelines; antitrust scrutiny in EU/US may pace deal flow. Bolt-on biotech and naturals acquisitions accelerate growth and specialty capabilities.

- Portfolio breadth and cross-selling

- R&D leverage and margin scale

- Integration execution = synergy capture

- Antitrust scrutiny may slow pacing

- Bolt-ons in biotech/naturals boost growth

Emerging market growth

Rising middle classes in emerging markets drive higher demand for personal care, beverages and packaged foods as IMF data show emerging-market growth at about 4.1% in 2024, necessitating localized taste profiles and faster innovation cycles to capture share. Macro volatility forces agile pricing and tighter credit control, while regional labs and application centers speed product wins and market adaptation.

- Emerging growth 4.1% (IMF 2024)

- Localized flavors accelerate NPD

- Agile pricing & credit management

- Regional labs shorten time-to-market

Tariffs, EU green rules raise aroma-chemical costs; Madagascar supplies ~80% of vanilla

Demand mirrors staples volumes with premiumization lifting mix; pricing power offsets input inflation with lag. Raw-materials remain volatile (Brent ~86 USD/bbl in 2024); biotech and inventories lower exposure. FX translation is material (>95% sales outside Switzerland) while scale (FY2024 sales CHF 9.1bn, ~25% market share) and consolidation drive margin leverage.

| Metric | Value |

|---|---|

| FY2024 sales | CHF 9.1bn |

| Market share | ~25% (2023) |

| Revenue outside CH | >95% |

| Brent (2024) | ~86 USD/bbl |

| Emerging growth (IMF 2024) | 4.1% |

Preview Before You Purchase

Givaudan PESTLE Analysis

The preview of the Givaudan PESTLE Analysis shown here is the exact document you’ll receive after purchase — fully formatted, professionally structured, and ready to use. This is the final file with no placeholders or teasers. After checkout you’ll instantly download this same complete report. What you see is what you’ll own.

Your Competitive Advantage Starts with This Report

Understand how regulatory, economic and technological shifts are shaping Givaudan’s future and competitive position. This concise PESTLE highlights key risks and growth opportunities for investors, consultants, and strategists. Purchase the full, editable analysis to unlock detailed, actionable insights now.

Political factors

Geopolitics and trade policy

Sanctions, tariffs and export controls can disrupt ingredient flows and raise costs for fragrances and flavors; US tariffs on Chinese goods introduced since 2018 still cover roughly 60% of imports by value, affecting aroma-chemical sourcing. EU trade defenses and shifting 2024 tariff schedules increased supplier costs. Givaudan, with 2024 sales exceeding CHF 7bn, must hedge exposure, diversify suppliers and routes, and use proactive customs planning and dual-sourcing to reduce political risk.

Instability in key sourcing regions

Vanilla from Madagascar, which supplies roughly 80% of the global market, and citrus sourced from major Latin American producers like Brazil face political and social volatility that can trigger supply shocks and sharp price spikes. Elections, strikes or governance issues have repeatedly disrupted flows, so Givaudan leans on local engagement and community projects to stabilize supplier relationships. Inventory buffers and long-term contracts are used to mitigate disruption risk.

EU Green Deal and policy steering

EU Green Deal policy pushes decarbonization, Farm to Fork targets 50% pesticide reduction by 2030 and the 2023 Chemical Strategy tightens hazardous substance use; CBAM began phasing in 2023. Funding and rules shape R&D and plant retrofits via instruments like Horizon Europe (€95.5bn 2021–27) and the EU’s stated ~€1tn green investment target. Compliance raises capex but rewards early movers; Givaudan can reorient pipelines to capture policy-linked incentives.

Swiss political context and market access

As a Swiss company, bilateral accords with the EU and regulatory equivalence are key for frictionless trade; changes to mutual recognition can force extra testing and conformity costs. Stable Swiss governance supports long-term planning. Givaudan reported CHF 8.6bn sales in 2024 and, given the EU accounts for roughly 50% of Swiss exports, its strategic EU footprint helps safeguard market access.

- Bilateral accords affect tariffs and regulatory checks

- Mutual recognition changes increase testing/conformity costs

- Stable Swiss governance aids long-term investment

- EU footprint mitigates market-access risk

Food security and agricultural policy

Subsidies, quotas and sustainability mandates reshape availability and prices for botanicals, increasing input-cost volatility for Givaudan. The EU Deforestation Regulation, adopted 2023, and similar rules worldwide are tightening traceability for cocoa, coffee, palm, soy, rubber, wood, cattle and maize. Givaudan leverages its Sourcing4Good program and farmer partnerships to meet policy-driven standards and de-risk supply.

- Policy-driven price/availability shocks

- EUDR 2023 intensifies traceability

- Tighter global import requirements

- Farmer partnerships via Sourcing4Good

Tariffs, EU green rules raise aroma-chemical costs; Madagascar supplies ~80% of vanilla

Political risks—tariffs, sanctions and trade controls (US tariffs cover ~60% of Chinese imports) and EU trade defenses—raise aroma-chemical costs and force supplier diversification; Givaudan reported CHF 8.6bn sales in 2024 and sources ~80% of global vanilla from Madagascar. EU Green Deal, EUDR 2023 and CBAM raise compliance capex; Swiss-EU relations and Sourcing4Good mitigate supply shocks.

| Metric | Value |

|---|---|

| 2024 sales | CHF 8.6bn |

| Vanilla global supply from Madagascar | ~80% |

| US tariffs on China (imports by value) | ~60% |

| EU share of Swiss exports | ~50% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely shape Givaudan’s flavor & fragrance business, linking current market and regulatory trends to risks and opportunities; data-backed, forward-looking insights support executives, investors and strategists in scenario planning and investor-ready reporting.

Provides a concise, visually segmented PESTLE summary of Givaudan that can be dropped into presentations or shared across teams to quickly align on external risks, market positioning, and strategic implications.

Economic factors

FMCG demand cycles and pricing

FMCG demand for flavors and fragrances tracks staples volumes and premiumization: Givaudan reported FY2024 net sales of CHF 9.1bn, reflecting resilience in staples-led categories. In downturns volumes hold but mix can downshift; in upturns innovation boosts margins. Pricing power typically offsets input inflation with a lag, and customer contract terms dictate pass-through speed.

Raw material volatility

Raw material costs for Givaudan—citrus oils, vanillin, petrochemical derivatives and solvents—move with harvest cycles and energy; Brent crude averaged about 86 USD/barrel in 2024, fueling solvent and feedstock swings. Supply shocks can compress margins ahead of contract repricing, while diversification into biotech and captive formulations lowers exposure. Strategic inventories and supplier alliances further stabilize input costs.

Currency exposure (CHF, USD, EUR)

Givaudan reports in Swiss francs while generating over 95% of revenue outside Switzerland, creating material CHF, USD and EUR translation exposure. FX moves alter competitiveness as costs and reporting remain Swiss-franc-centric, so natural hedges from local production and currency-matched sales are important. The company uses derivatives and active treasury management to limit volatility. A balanced regional footprint further reduces single-currency risk.

M&A and scale advantages

Consolidation lets Givaudan expand portfolio, leverage R&D and cross-sell to multinationals; as the world’s largest fragrance and flavor company (2023 sales CHF 7.9bn, ~25% market share) scale drives margin and innovation leverage. Integration execution determines synergy capture and timelines; antitrust scrutiny in EU/US may pace deal flow. Bolt-on biotech and naturals acquisitions accelerate growth and specialty capabilities.

- Portfolio breadth and cross-selling

- R&D leverage and margin scale

- Integration execution = synergy capture

- Antitrust scrutiny may slow pacing

- Bolt-ons in biotech/naturals boost growth

Emerging market growth

Rising middle classes in emerging markets drive higher demand for personal care, beverages and packaged foods as IMF data show emerging-market growth at about 4.1% in 2024, necessitating localized taste profiles and faster innovation cycles to capture share. Macro volatility forces agile pricing and tighter credit control, while regional labs and application centers speed product wins and market adaptation.

- Emerging growth 4.1% (IMF 2024)

- Localized flavors accelerate NPD

- Agile pricing & credit management

- Regional labs shorten time-to-market

Tariffs, EU green rules raise aroma-chemical costs; Madagascar supplies ~80% of vanilla

Demand mirrors staples volumes with premiumization lifting mix; pricing power offsets input inflation with lag. Raw-materials remain volatile (Brent ~86 USD/bbl in 2024); biotech and inventories lower exposure. FX translation is material (>95% sales outside Switzerland) while scale (FY2024 sales CHF 9.1bn, ~25% market share) and consolidation drive margin leverage.

| Metric | Value |

|---|---|

| FY2024 sales | CHF 9.1bn |

| Market share | ~25% (2023) |

| Revenue outside CH | >95% |

| Brent (2024) | ~86 USD/bbl |

| Emerging growth (IMF 2024) | 4.1% |

Preview Before You Purchase

Givaudan PESTLE Analysis

The preview of the Givaudan PESTLE Analysis shown here is the exact document you’ll receive after purchase — fully formatted, professionally structured, and ready to use. This is the final file with no placeholders or teasers. After checkout you’ll instantly download this same complete report. What you see is what you’ll own.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Understand how regulatory, economic and technological shifts are shaping Givaudan’s future and competitive position. This concise PESTLE highlights key risks and growth opportunities for investors, consultants, and strategists. Purchase the full, editable analysis to unlock detailed, actionable insights now.

Political factors

Geopolitics and trade policy

Sanctions, tariffs and export controls can disrupt ingredient flows and raise costs for fragrances and flavors; US tariffs on Chinese goods introduced since 2018 still cover roughly 60% of imports by value, affecting aroma-chemical sourcing. EU trade defenses and shifting 2024 tariff schedules increased supplier costs. Givaudan, with 2024 sales exceeding CHF 7bn, must hedge exposure, diversify suppliers and routes, and use proactive customs planning and dual-sourcing to reduce political risk.

Instability in key sourcing regions

Vanilla from Madagascar, which supplies roughly 80% of the global market, and citrus sourced from major Latin American producers like Brazil face political and social volatility that can trigger supply shocks and sharp price spikes. Elections, strikes or governance issues have repeatedly disrupted flows, so Givaudan leans on local engagement and community projects to stabilize supplier relationships. Inventory buffers and long-term contracts are used to mitigate disruption risk.

EU Green Deal and policy steering

EU Green Deal policy pushes decarbonization, Farm to Fork targets 50% pesticide reduction by 2030 and the 2023 Chemical Strategy tightens hazardous substance use; CBAM began phasing in 2023. Funding and rules shape R&D and plant retrofits via instruments like Horizon Europe (€95.5bn 2021–27) and the EU’s stated ~€1tn green investment target. Compliance raises capex but rewards early movers; Givaudan can reorient pipelines to capture policy-linked incentives.

Swiss political context and market access

As a Swiss company, bilateral accords with the EU and regulatory equivalence are key for frictionless trade; changes to mutual recognition can force extra testing and conformity costs. Stable Swiss governance supports long-term planning. Givaudan reported CHF 8.6bn sales in 2024 and, given the EU accounts for roughly 50% of Swiss exports, its strategic EU footprint helps safeguard market access.

- Bilateral accords affect tariffs and regulatory checks

- Mutual recognition changes increase testing/conformity costs

- Stable Swiss governance aids long-term investment

- EU footprint mitigates market-access risk

Food security and agricultural policy

Subsidies, quotas and sustainability mandates reshape availability and prices for botanicals, increasing input-cost volatility for Givaudan. The EU Deforestation Regulation, adopted 2023, and similar rules worldwide are tightening traceability for cocoa, coffee, palm, soy, rubber, wood, cattle and maize. Givaudan leverages its Sourcing4Good program and farmer partnerships to meet policy-driven standards and de-risk supply.

- Policy-driven price/availability shocks

- EUDR 2023 intensifies traceability

- Tighter global import requirements

- Farmer partnerships via Sourcing4Good

Tariffs, EU green rules raise aroma-chemical costs; Madagascar supplies ~80% of vanilla

Political risks—tariffs, sanctions and trade controls (US tariffs cover ~60% of Chinese imports) and EU trade defenses—raise aroma-chemical costs and force supplier diversification; Givaudan reported CHF 8.6bn sales in 2024 and sources ~80% of global vanilla from Madagascar. EU Green Deal, EUDR 2023 and CBAM raise compliance capex; Swiss-EU relations and Sourcing4Good mitigate supply shocks.

| Metric | Value |

|---|---|

| 2024 sales | CHF 8.6bn |

| Vanilla global supply from Madagascar | ~80% |

| US tariffs on China (imports by value) | ~60% |

| EU share of Swiss exports | ~50% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely shape Givaudan’s flavor & fragrance business, linking current market and regulatory trends to risks and opportunities; data-backed, forward-looking insights support executives, investors and strategists in scenario planning and investor-ready reporting.

Provides a concise, visually segmented PESTLE summary of Givaudan that can be dropped into presentations or shared across teams to quickly align on external risks, market positioning, and strategic implications.

Economic factors

FMCG demand cycles and pricing

FMCG demand for flavors and fragrances tracks staples volumes and premiumization: Givaudan reported FY2024 net sales of CHF 9.1bn, reflecting resilience in staples-led categories. In downturns volumes hold but mix can downshift; in upturns innovation boosts margins. Pricing power typically offsets input inflation with a lag, and customer contract terms dictate pass-through speed.

Raw material volatility

Raw material costs for Givaudan—citrus oils, vanillin, petrochemical derivatives and solvents—move with harvest cycles and energy; Brent crude averaged about 86 USD/barrel in 2024, fueling solvent and feedstock swings. Supply shocks can compress margins ahead of contract repricing, while diversification into biotech and captive formulations lowers exposure. Strategic inventories and supplier alliances further stabilize input costs.

Currency exposure (CHF, USD, EUR)

Givaudan reports in Swiss francs while generating over 95% of revenue outside Switzerland, creating material CHF, USD and EUR translation exposure. FX moves alter competitiveness as costs and reporting remain Swiss-franc-centric, so natural hedges from local production and currency-matched sales are important. The company uses derivatives and active treasury management to limit volatility. A balanced regional footprint further reduces single-currency risk.

M&A and scale advantages

Consolidation lets Givaudan expand portfolio, leverage R&D and cross-sell to multinationals; as the world’s largest fragrance and flavor company (2023 sales CHF 7.9bn, ~25% market share) scale drives margin and innovation leverage. Integration execution determines synergy capture and timelines; antitrust scrutiny in EU/US may pace deal flow. Bolt-on biotech and naturals acquisitions accelerate growth and specialty capabilities.

- Portfolio breadth and cross-selling

- R&D leverage and margin scale

- Integration execution = synergy capture

- Antitrust scrutiny may slow pacing

- Bolt-ons in biotech/naturals boost growth

Emerging market growth

Rising middle classes in emerging markets drive higher demand for personal care, beverages and packaged foods as IMF data show emerging-market growth at about 4.1% in 2024, necessitating localized taste profiles and faster innovation cycles to capture share. Macro volatility forces agile pricing and tighter credit control, while regional labs and application centers speed product wins and market adaptation.

- Emerging growth 4.1% (IMF 2024)

- Localized flavors accelerate NPD

- Agile pricing & credit management

- Regional labs shorten time-to-market

Tariffs, EU green rules raise aroma-chemical costs; Madagascar supplies ~80% of vanilla

Demand mirrors staples volumes with premiumization lifting mix; pricing power offsets input inflation with lag. Raw-materials remain volatile (Brent ~86 USD/bbl in 2024); biotech and inventories lower exposure. FX translation is material (>95% sales outside Switzerland) while scale (FY2024 sales CHF 9.1bn, ~25% market share) and consolidation drive margin leverage.

| Metric | Value |

|---|---|

| FY2024 sales | CHF 9.1bn |

| Market share | ~25% (2023) |

| Revenue outside CH | >95% |

| Brent (2024) | ~86 USD/bbl |

| Emerging growth (IMF 2024) | 4.1% |

Preview Before You Purchase

Givaudan PESTLE Analysis

The preview of the Givaudan PESTLE Analysis shown here is the exact document you’ll receive after purchase — fully formatted, professionally structured, and ready to use. This is the final file with no placeholders or teasers. After checkout you’ll instantly download this same complete report. What you see is what you’ll own.