Glanbia PESTLE Analysis

Skip the Research. Get the Strategy.

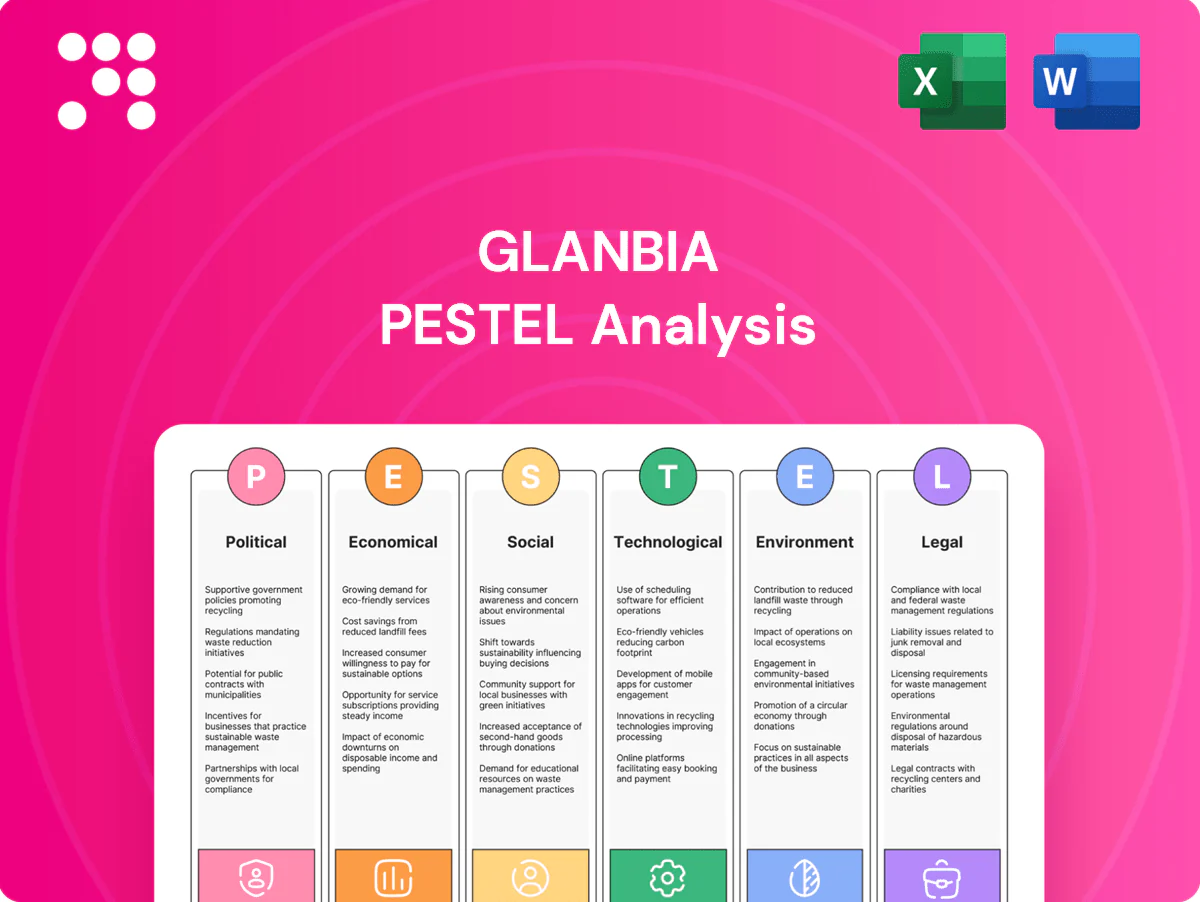

Our Glanbia PESTLE Analysis reveals how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures shape the company’s prospects. Built for investors and strategists, it converts external risk into actionable insight. Purchase the full, editable report to access detailed findings and tactical recommendations instantly.

Political factors

Trade policies and tariffs

Shifts in trade agreements and tariff regimes directly affect cross-border flows of dairy and nutrition ingredients, impacting Glanbia’s sourcing costs and market access; Glanbia reported group revenue of €4.7bn in 2024, so margin swings from tariffs are material. Tariff escalations on whey, lactose or specialty proteins can compress margins or force price rises, while preferential trade agreements unlock cost-effective sourcing and new markets. Glanbia must actively manage customs strategies and diversify logistics routes to protect margins and supply continuity.

Agricultural subsidies and farm policy

Subsidy frameworks in the EU, US and other dairy regions shape milk supply and input costs; the EU CAP 2023–27 package totals about €386.6bn, affecting producer incentives and price signals. Changes to quotas, carbon-linked supports or feed incentives directly alter whey availability for sports nutrition as global milk output (~925 million tonnes in 2023) shifts. Active engagement with producer networks and close monitoring of CAP and US Farm Bill updates is critical for stabilizing raw material pipelines.

Geopolitical risk and sanctions

Conflicts and sanctions, notably post-2022 Russia-Ukraine measures, can disrupt Glanbia ingredient sourcing and shipping lanes, raising logistics risk; European gas TTF spiked to ~€345/MWh in Aug 2022, driving processing costs. Sanctions limit market entry and counterparties. Contingency sourcing and insurance coverage preserve supply continuity.

Public health agendas and nutrition policy

Brexit and EU regulatory divergence

Brexit-driven divergence in UK and EU food standards complicates labeling, approvals and cross-border logistics for Glanbia, increasing documentation and parallel compliance tracks. Added border checks lengthen lead times and raise working capital tied to in-transit inventory. Gaps in mutual recognition can slow product rollouts; detailed compliance mappings and dual-market registrations reduce disruption.

Tariffs, CAP and milk supply squeeze margins for large dairy group; high-protein pivot

Trade/tariff shifts and Brexit raise cross-border costs for Glanbia; group revenue €4.7bn (2024) makes margin exposure material. CAP 2023–27 (€386.6bn) and global milk ~925Mt (2023) affect whey supply and input prices. Health taxes and procurement (school meals ~30M/day) push reformulation toward high-protein SKUs.

| Metric | Value |

|---|---|

| 2024 revenue | €4.7bn |

| CAP 2023–27 | €386.6bn |

| Global milk 2023 | ~925Mt |

What is included in the product

Examines how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Glanbia, with data-backed trends and region/industry-specific examples to identify risks and opportunities; written for executives and investors and including forward-looking insights to support scenario planning and strategic decisions.

Concise, visually segmented Glanbia PESTLE summary that distills external risks and opportunities for quick reference in meetings or presentations, easily editable for region- or business-line specifics and shareable across teams to align strategy and support planning discussions.

Economic factors

Commodity and input price volatility

Milk, whey, sweetener and packaging costs swing with seasonal cycles and weather—milk supply shocks and whey price moves drove input volatility in 2024, impacting Glanbia alongside its ~€4.1bn FY2024 revenue base. Energy and freight spikes (notably 2022–24 route congestion) have pressured gross margins and delivery reliability. Active hedging and long-term supplier contracts stabilize cost bases. Flexible pricing and SKU mix preserve profitability.

Consumer spending and macro cycles

Discretionary demand for premium sports nutrition closely follows real incomes and employment; the global sports nutrition market was estimated at about US$44.8bn in 2023 with mid-single-digit growth, making premium SKUs sensitive to downturns. During recessions consumers shift to value formats and private label, pressuring margin mix. Recovery phases support innovation-led premiumization, and Glanbia’s diversified channels across retail, direct-to-consumer and B2B help balance cyclical exposure.

Foreign exchange movements

Revenues and costs across USD, EUR and emerging-market currencies create both translation and transaction risk for Glanbia. FX swings affect competitiveness and reported earnings, with EUR/USD averaging about 1.09 in 2024. Natural hedging from local sourcing and local-currency pricing helps offset volatility. Treasury policies and use of forwards and options manage residual exposure.

Emerging market growth

Emerging market growth (IMF 2024: ~4.1% EM growth) is expanding middle classes, boosting demand for protein, performance and functional foods and increasing addressable markets for Glanbia. Infrastructure gaps and route-to-market complexity raise costs to serve and slow margin expansion. Local partnerships and tailored pack sizes/price points accelerate regulatory navigation, distribution scale and penetration.

- Demand: rising middle classes, stronger protein uptake

- Costs: higher logistics and route-to-market complexity

- Strategy: local partnerships for regulation and scale

- Execution: small packs and price tiers unlock volume

M&A and capital allocation

Consolidation in nutrition ingredients and brands lets Glanbia scale manufacturing and R&D, targeting bolt-on deals to deepen capabilities; in 2024 the group executed ~€150m of strategic acquisitions to expand specialty ingredients.

Valuation cycles drove selective timing of purchases and divestments in 2024, with management pausing larger bids as multiples compressed; disciplined ROIC hurdles (target >12%) guide portfolio shaping.

Integration excellence remains vital to capture projected cost and cross-sell revenue synergies and protect transaction economics.

- Consolidation: scale R&D and manufacturing

- 2024 spend: ~€150m in bolt-ons

- Valuation-led timing: selective deal cadence

- ROIC target: >12%

- Focus: integration to secure synergies

Tariffs, CAP and milk supply squeeze margins for large dairy group; high-protein pivot

Input-cost volatility (milk/whey/energy) hit margins despite Glanbia’s ~€4.1bn FY2024 revenue; hedges and contracts reduce tail risk. Premium sports-nutrition demand tracks incomes (global market ~US$44.8bn in 2023) and is cyclical; EM expansion (IMF 2024: ~4.1%) supports volume. FX (EUR/USD ~1.09 in 2024), €150m bolt-ons in 2024 and ROIC target >12% shape capital allocation.

| Metric | Value |

|---|---|

| FY2024 Revenue | ~€4.1bn |

| Global sports nutrition (2023) | US$44.8bn |

| EUR/USD (2024 avg) | ~1.09 |

| EM GDP (2024 IMF) | ~4.1% |

| 2024 M&A spend | ~€150m |

| ROIC target | >12% |

Preview the Actual Deliverable

Glanbia PESTLE Analysis

The Glanbia PESTLE Analysis provides a clear evaluation of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It’s concise, sourced and ready for immediate application.

Skip the Research. Get the Strategy.

Our Glanbia PESTLE Analysis reveals how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures shape the company’s prospects. Built for investors and strategists, it converts external risk into actionable insight. Purchase the full, editable report to access detailed findings and tactical recommendations instantly.

Political factors

Trade policies and tariffs

Shifts in trade agreements and tariff regimes directly affect cross-border flows of dairy and nutrition ingredients, impacting Glanbia’s sourcing costs and market access; Glanbia reported group revenue of €4.7bn in 2024, so margin swings from tariffs are material. Tariff escalations on whey, lactose or specialty proteins can compress margins or force price rises, while preferential trade agreements unlock cost-effective sourcing and new markets. Glanbia must actively manage customs strategies and diversify logistics routes to protect margins and supply continuity.

Agricultural subsidies and farm policy

Subsidy frameworks in the EU, US and other dairy regions shape milk supply and input costs; the EU CAP 2023–27 package totals about €386.6bn, affecting producer incentives and price signals. Changes to quotas, carbon-linked supports or feed incentives directly alter whey availability for sports nutrition as global milk output (~925 million tonnes in 2023) shifts. Active engagement with producer networks and close monitoring of CAP and US Farm Bill updates is critical for stabilizing raw material pipelines.

Geopolitical risk and sanctions

Conflicts and sanctions, notably post-2022 Russia-Ukraine measures, can disrupt Glanbia ingredient sourcing and shipping lanes, raising logistics risk; European gas TTF spiked to ~€345/MWh in Aug 2022, driving processing costs. Sanctions limit market entry and counterparties. Contingency sourcing and insurance coverage preserve supply continuity.

Public health agendas and nutrition policy

Brexit and EU regulatory divergence

Brexit-driven divergence in UK and EU food standards complicates labeling, approvals and cross-border logistics for Glanbia, increasing documentation and parallel compliance tracks. Added border checks lengthen lead times and raise working capital tied to in-transit inventory. Gaps in mutual recognition can slow product rollouts; detailed compliance mappings and dual-market registrations reduce disruption.

Tariffs, CAP and milk supply squeeze margins for large dairy group; high-protein pivot

Trade/tariff shifts and Brexit raise cross-border costs for Glanbia; group revenue €4.7bn (2024) makes margin exposure material. CAP 2023–27 (€386.6bn) and global milk ~925Mt (2023) affect whey supply and input prices. Health taxes and procurement (school meals ~30M/day) push reformulation toward high-protein SKUs.

| Metric | Value |

|---|---|

| 2024 revenue | €4.7bn |

| CAP 2023–27 | €386.6bn |

| Global milk 2023 | ~925Mt |

What is included in the product

Examines how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Glanbia, with data-backed trends and region/industry-specific examples to identify risks and opportunities; written for executives and investors and including forward-looking insights to support scenario planning and strategic decisions.

Concise, visually segmented Glanbia PESTLE summary that distills external risks and opportunities for quick reference in meetings or presentations, easily editable for region- or business-line specifics and shareable across teams to align strategy and support planning discussions.

Economic factors

Commodity and input price volatility

Milk, whey, sweetener and packaging costs swing with seasonal cycles and weather—milk supply shocks and whey price moves drove input volatility in 2024, impacting Glanbia alongside its ~€4.1bn FY2024 revenue base. Energy and freight spikes (notably 2022–24 route congestion) have pressured gross margins and delivery reliability. Active hedging and long-term supplier contracts stabilize cost bases. Flexible pricing and SKU mix preserve profitability.

Consumer spending and macro cycles

Discretionary demand for premium sports nutrition closely follows real incomes and employment; the global sports nutrition market was estimated at about US$44.8bn in 2023 with mid-single-digit growth, making premium SKUs sensitive to downturns. During recessions consumers shift to value formats and private label, pressuring margin mix. Recovery phases support innovation-led premiumization, and Glanbia’s diversified channels across retail, direct-to-consumer and B2B help balance cyclical exposure.

Foreign exchange movements

Revenues and costs across USD, EUR and emerging-market currencies create both translation and transaction risk for Glanbia. FX swings affect competitiveness and reported earnings, with EUR/USD averaging about 1.09 in 2024. Natural hedging from local sourcing and local-currency pricing helps offset volatility. Treasury policies and use of forwards and options manage residual exposure.

Emerging market growth

Emerging market growth (IMF 2024: ~4.1% EM growth) is expanding middle classes, boosting demand for protein, performance and functional foods and increasing addressable markets for Glanbia. Infrastructure gaps and route-to-market complexity raise costs to serve and slow margin expansion. Local partnerships and tailored pack sizes/price points accelerate regulatory navigation, distribution scale and penetration.

- Demand: rising middle classes, stronger protein uptake

- Costs: higher logistics and route-to-market complexity

- Strategy: local partnerships for regulation and scale

- Execution: small packs and price tiers unlock volume

M&A and capital allocation

Consolidation in nutrition ingredients and brands lets Glanbia scale manufacturing and R&D, targeting bolt-on deals to deepen capabilities; in 2024 the group executed ~€150m of strategic acquisitions to expand specialty ingredients.

Valuation cycles drove selective timing of purchases and divestments in 2024, with management pausing larger bids as multiples compressed; disciplined ROIC hurdles (target >12%) guide portfolio shaping.

Integration excellence remains vital to capture projected cost and cross-sell revenue synergies and protect transaction economics.

- Consolidation: scale R&D and manufacturing

- 2024 spend: ~€150m in bolt-ons

- Valuation-led timing: selective deal cadence

- ROIC target: >12%

- Focus: integration to secure synergies

Tariffs, CAP and milk supply squeeze margins for large dairy group; high-protein pivot

Input-cost volatility (milk/whey/energy) hit margins despite Glanbia’s ~€4.1bn FY2024 revenue; hedges and contracts reduce tail risk. Premium sports-nutrition demand tracks incomes (global market ~US$44.8bn in 2023) and is cyclical; EM expansion (IMF 2024: ~4.1%) supports volume. FX (EUR/USD ~1.09 in 2024), €150m bolt-ons in 2024 and ROIC target >12% shape capital allocation.

| Metric | Value |

|---|---|

| FY2024 Revenue | ~€4.1bn |

| Global sports nutrition (2023) | US$44.8bn |

| EUR/USD (2024 avg) | ~1.09 |

| EM GDP (2024 IMF) | ~4.1% |

| 2024 M&A spend | ~€150m |

| ROIC target | >12% |

Preview the Actual Deliverable

Glanbia PESTLE Analysis

The Glanbia PESTLE Analysis provides a clear evaluation of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It’s concise, sourced and ready for immediate application.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Our Glanbia PESTLE Analysis reveals how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures shape the company’s prospects. Built for investors and strategists, it converts external risk into actionable insight. Purchase the full, editable report to access detailed findings and tactical recommendations instantly.

Political factors

Trade policies and tariffs

Shifts in trade agreements and tariff regimes directly affect cross-border flows of dairy and nutrition ingredients, impacting Glanbia’s sourcing costs and market access; Glanbia reported group revenue of €4.7bn in 2024, so margin swings from tariffs are material. Tariff escalations on whey, lactose or specialty proteins can compress margins or force price rises, while preferential trade agreements unlock cost-effective sourcing and new markets. Glanbia must actively manage customs strategies and diversify logistics routes to protect margins and supply continuity.

Agricultural subsidies and farm policy

Subsidy frameworks in the EU, US and other dairy regions shape milk supply and input costs; the EU CAP 2023–27 package totals about €386.6bn, affecting producer incentives and price signals. Changes to quotas, carbon-linked supports or feed incentives directly alter whey availability for sports nutrition as global milk output (~925 million tonnes in 2023) shifts. Active engagement with producer networks and close monitoring of CAP and US Farm Bill updates is critical for stabilizing raw material pipelines.

Geopolitical risk and sanctions

Conflicts and sanctions, notably post-2022 Russia-Ukraine measures, can disrupt Glanbia ingredient sourcing and shipping lanes, raising logistics risk; European gas TTF spiked to ~€345/MWh in Aug 2022, driving processing costs. Sanctions limit market entry and counterparties. Contingency sourcing and insurance coverage preserve supply continuity.

Public health agendas and nutrition policy

Brexit and EU regulatory divergence

Brexit-driven divergence in UK and EU food standards complicates labeling, approvals and cross-border logistics for Glanbia, increasing documentation and parallel compliance tracks. Added border checks lengthen lead times and raise working capital tied to in-transit inventory. Gaps in mutual recognition can slow product rollouts; detailed compliance mappings and dual-market registrations reduce disruption.

Tariffs, CAP and milk supply squeeze margins for large dairy group; high-protein pivot

Trade/tariff shifts and Brexit raise cross-border costs for Glanbia; group revenue €4.7bn (2024) makes margin exposure material. CAP 2023–27 (€386.6bn) and global milk ~925Mt (2023) affect whey supply and input prices. Health taxes and procurement (school meals ~30M/day) push reformulation toward high-protein SKUs.

| Metric | Value |

|---|---|

| 2024 revenue | €4.7bn |

| CAP 2023–27 | €386.6bn |

| Global milk 2023 | ~925Mt |

What is included in the product

Examines how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Glanbia, with data-backed trends and region/industry-specific examples to identify risks and opportunities; written for executives and investors and including forward-looking insights to support scenario planning and strategic decisions.

Concise, visually segmented Glanbia PESTLE summary that distills external risks and opportunities for quick reference in meetings or presentations, easily editable for region- or business-line specifics and shareable across teams to align strategy and support planning discussions.

Economic factors

Commodity and input price volatility

Milk, whey, sweetener and packaging costs swing with seasonal cycles and weather—milk supply shocks and whey price moves drove input volatility in 2024, impacting Glanbia alongside its ~€4.1bn FY2024 revenue base. Energy and freight spikes (notably 2022–24 route congestion) have pressured gross margins and delivery reliability. Active hedging and long-term supplier contracts stabilize cost bases. Flexible pricing and SKU mix preserve profitability.

Consumer spending and macro cycles

Discretionary demand for premium sports nutrition closely follows real incomes and employment; the global sports nutrition market was estimated at about US$44.8bn in 2023 with mid-single-digit growth, making premium SKUs sensitive to downturns. During recessions consumers shift to value formats and private label, pressuring margin mix. Recovery phases support innovation-led premiumization, and Glanbia’s diversified channels across retail, direct-to-consumer and B2B help balance cyclical exposure.

Foreign exchange movements

Revenues and costs across USD, EUR and emerging-market currencies create both translation and transaction risk for Glanbia. FX swings affect competitiveness and reported earnings, with EUR/USD averaging about 1.09 in 2024. Natural hedging from local sourcing and local-currency pricing helps offset volatility. Treasury policies and use of forwards and options manage residual exposure.

Emerging market growth

Emerging market growth (IMF 2024: ~4.1% EM growth) is expanding middle classes, boosting demand for protein, performance and functional foods and increasing addressable markets for Glanbia. Infrastructure gaps and route-to-market complexity raise costs to serve and slow margin expansion. Local partnerships and tailored pack sizes/price points accelerate regulatory navigation, distribution scale and penetration.

- Demand: rising middle classes, stronger protein uptake

- Costs: higher logistics and route-to-market complexity

- Strategy: local partnerships for regulation and scale

- Execution: small packs and price tiers unlock volume

M&A and capital allocation

Consolidation in nutrition ingredients and brands lets Glanbia scale manufacturing and R&D, targeting bolt-on deals to deepen capabilities; in 2024 the group executed ~€150m of strategic acquisitions to expand specialty ingredients.

Valuation cycles drove selective timing of purchases and divestments in 2024, with management pausing larger bids as multiples compressed; disciplined ROIC hurdles (target >12%) guide portfolio shaping.

Integration excellence remains vital to capture projected cost and cross-sell revenue synergies and protect transaction economics.

- Consolidation: scale R&D and manufacturing

- 2024 spend: ~€150m in bolt-ons

- Valuation-led timing: selective deal cadence

- ROIC target: >12%

- Focus: integration to secure synergies

Tariffs, CAP and milk supply squeeze margins for large dairy group; high-protein pivot

Input-cost volatility (milk/whey/energy) hit margins despite Glanbia’s ~€4.1bn FY2024 revenue; hedges and contracts reduce tail risk. Premium sports-nutrition demand tracks incomes (global market ~US$44.8bn in 2023) and is cyclical; EM expansion (IMF 2024: ~4.1%) supports volume. FX (EUR/USD ~1.09 in 2024), €150m bolt-ons in 2024 and ROIC target >12% shape capital allocation.

| Metric | Value |

|---|---|

| FY2024 Revenue | ~€4.1bn |

| Global sports nutrition (2023) | US$44.8bn |

| EUR/USD (2024 avg) | ~1.09 |

| EM GDP (2024 IMF) | ~4.1% |

| 2024 M&A spend | ~€150m |

| ROIC target | >12% |

Preview the Actual Deliverable

Glanbia PESTLE Analysis

The Glanbia PESTLE Analysis provides a clear evaluation of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It’s concise, sourced and ready for immediate application.