Ezaki Glico Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

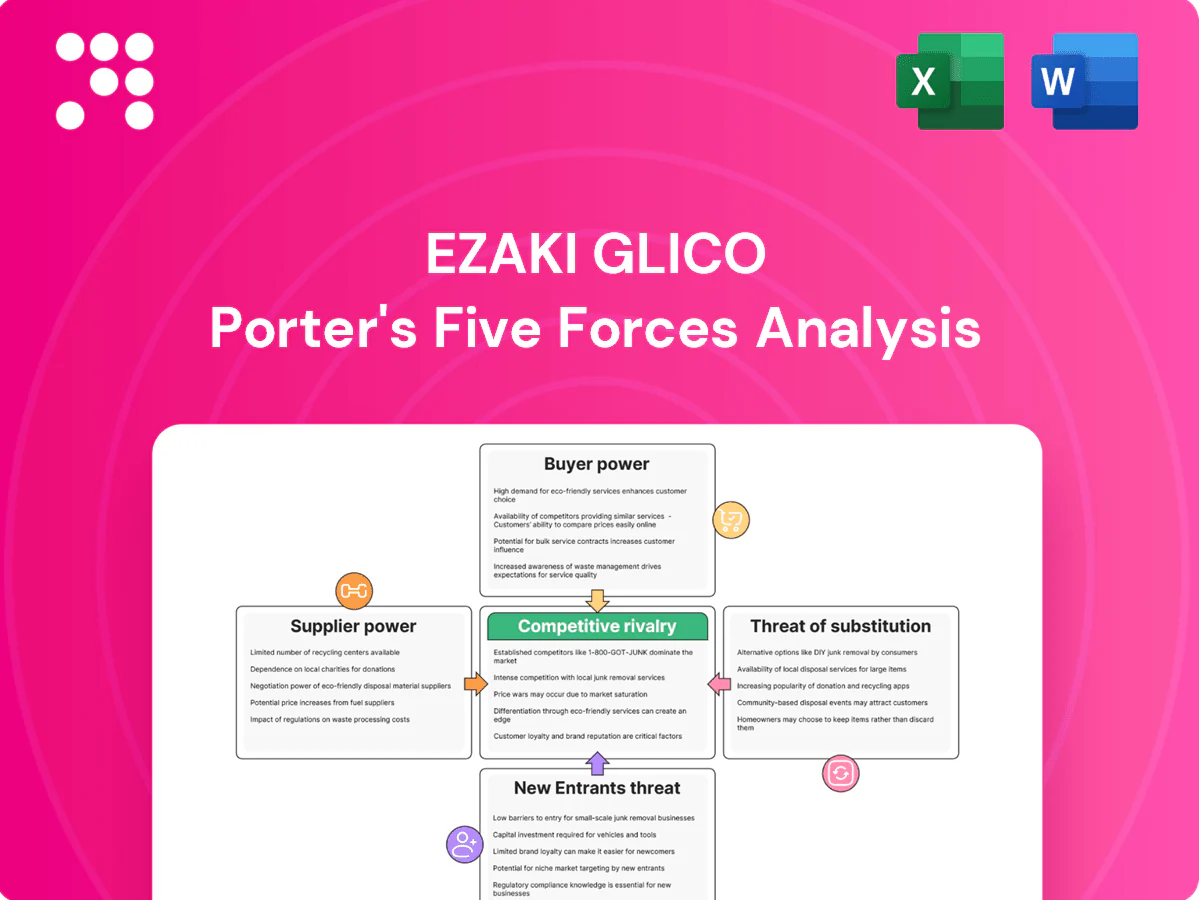

Ezaki Glico operates in a fiercely competitive confectionery and processed foods market where strong brands, scale advantages, and distribution breadth lower buyer power but intensify rivalry; supplier power is moderate while substitutes and changing consumer trends raise strategic risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ezaki Glico’s competitive dynamics in detail.

Suppliers Bargaining Power

Dependence on dairy and cocoa

Core ingredients such as milk powder, cocoa and sugar face global price swings and supply concentration: Côte d'Ivoire and Ghana together supply roughly 60% of cocoa, while New Zealand supplies about 30% of global milk-powder exports. Weather, geopolitics and diseases (eg cocoa pod disease) periodically tighten availability, elevating supplier leverage in cost talks. Ezaki Glico mitigates via long-term contracts and hedging to partially offset input volatility.

Specialized packaging vendors

Specialized packaging vendors hold moderate bargaining power for Ezaki Glico because high-speed lines commonly exceed 10,000 packs/hour and require custom films and laminates, limiting interchangeable suppliers. Switching suppliers risks line downtime and quality deviations that can halt production. Qualified suppliers thus command leverage, but scale-based contracts and dual sourcing are used to balance terms and secure supply continuity in 2024 market conditions.

Scale leverage and vendor fragmentation

As of 2024 Glico’s consolidated scale across confectionery and dairy provides significant bargaining clout with suppliers, enabling volume discounts and preferred terms.

Many agricultural inputs remain highly fragmented among smallholders in Japan and Asia, which limits the negotiating power of individual growers versus a large buyer like Glico.

Consolidating spend across categories and applying vendor scorecards enforces performance and price discipline, strengthening procurement leverage and risk management.

Quality, safety, and compliance requirements

Strict Japanese and export safety standards narrow Ezaki Glico’s approved supplier pool, increasing leverage for compliant vendors and elevating input costs and switching barriers.

Targeted auditing and supplier-development programs (used industry-wide in 2024) can expand qualified suppliers over time, reducing concentration risk.

Co-investments in capacity and joint quality programs secure priority allocation and long-term supply at negotiated terms.

Logistics and geopolitical exposure

Import routes for cocoa, dairy and palm oil expose Ezaki Glico to freight and FX swings—container spot rates in 2024 were roughly 70% below 2021 peaks, yet shipping cost volatility and JPY moves still drive input-cost risk. Supply disruptions shift bargaining power to suppliers with secure upstream access, while nearshoring and inventory buffers dampen short-term leverage spikes. Active FX hedging and flexible incoterms (CIF/FOB) spread logistics risk across partners.

- Import concentration: high reliance on global suppliers

- 2024 freight normalization: ~70% down from 2021 highs

- Mitigants: nearshoring, inventory buffers, FX hedges, flexible incoterms

Cocoa and NZ milk concentration create periodic supplier leverage; firms hedge, dual-source

Core inputs (cocoa 60% from Côte d'Ivoire+Ghana; NZ ~30% of milk‑powder exports) create periodic supplier leverage via weather, disease and geopolitics. Packaging vendors exert moderate power due to high‑speed line specificity, while strict safety standards narrow approved suppliers. Glico offsets with scale, long‑term contracts, hedging, dual sourcing, supplier development and co‑investments in 2024.

| Metric | 2024 figure | Impact |

|---|---|---|

| Cocoa supply concentration | ~60% CI+GH | Higher supplier leverage |

| NZ milk‑powder exports | ~30% | Input price sensitivity |

| Container spot rates vs 2021 | ≈-70% | Lower freight but volatile |

What is included in the product

Tailored Porter's Five Forces for Ezaki Glico uncover competitive drivers, supplier/buyer power, substitute threats, and entry barriers, highlighting strategic risks and opportunities in its snack and confectionery markets.

A concise one-sheet Porter's Five Forces for Ezaki Glico—instantly highlight supplier/buyer leverage, entrant and substitute risks, and competitive rivalry to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Concentrated retail channels

Japanese convenience chains and large supermarkets exert strong shelf control over suppliers; 7-Eleven (~21,000 stores), FamilyMart (~17,000) and Lawson (~14,000) in 2024 leverage scale to extract slotting fees and push pricing concessions. Their bargaining power is reinforced by centralized purchasing and category resets, while growing private‑label penetration in packaged foods (≈15% in 2024) increases supplier pressure. Ezaki Glico partially offsets this through multi‑channel distribution (retail, e‑commerce, exports) and strong branded SKUs with proven sell‑through rates.

End-consumer price sensitivity

Snacks are discretionary and heavily promoted; Ezaki Glico faces high end-consumer price sensitivity as 2024 Japanese inflation around 2.7% increases elasticity in mass segments, driving shoppers toward promotions and private labels.

Consumers readily switch brands for small price gaps (often a few yen on single-serve items), compressing margins on core SKUs.

Premium and novelty SKUs (higher ASP) show lower price elasticity, supporting mix-driven margin recovery for Glico, whose FY2023 consolidated sales were about 456 billion JPY.

Brand loyalty to iconic SKUs

Products like Pocky—launched in 1966 and sold in over 50 countries—create strong repeat purchase stickiness, shrinking buyer leverage. Ezaki Glico reported consolidated net sales around ¥495 billion in FY2023/24, reflecting the premium pull of iconic SKUs. Limited editions and brand collaborations drive periodic spikes in demand, while loyalty programs and D2C channels deepen customer bonds and reduce price sensitivity.

Information transparency

Information transparency raises customer bargaining power for Ezaki Glico: online price comparison and reviews reduce switching costs, e-commerce share in Japan reached about 12% in 2024, and social media accelerates trend shifts that shorten product life cycles. Retailers leverage POS and loyalty data to demand sharper trade terms, while rich product content and influencer marketing partially counterbalance by strengthening brand equity.

- Price comparison: lowers switching costs

- Social media: faster trend cycles

- Retailer data: tougher trade terms

- Content/influencers: mitigate churn

Export market diversity

Export market diversity reduces single-market dependence and helped Ezaki Glico achieve overseas sales of about 20% of net sales in FY2024, lowering buyer concentration risk; buyer power varies significantly by country structure and channel, with modern trade and e‑commerce buyers exerting different pressures. Distributors in some markets demand hefty entry margins, while localized packs and a broad portfolio strengthen Glico’s negotiating stance.

- Diversified revenue: ~20% overseas (FY2024)

- Buyer power: country/channel-dependent

- Distributor margins can be high

- Localized packs boost bargaining leverage

Retailer scale, private-label and e-commerce squeeze suppliers; branded SKUs and D2C sustain power

Retail giants (7‑Eleven ~21,000; FamilyMart ~17,000; Lawson ~14,000 in 2024) exert strong shelf/price leverage; private‑label ≈15% and e‑commerce ≈12% raise supplier pressure. Ezaki Glico (net sales ¥495bn FY2023/24; overseas ~20%) offsets via branded SKUs, D2C and novelty/premium mix that reduce price elasticity. Information transparency and retailer data increase bargaining power, though iconic SKUs (Pocky) sustain stickiness.

| Metric | 2024 |

|---|---|

| Net sales | ¥495bn |

| Overseas | ≈20% |

| Private label | ≈15% |

| E‑commerce | ≈12% |

Preview the Actual Deliverable

Ezaki Glico Porter's Five Forces Analysis

This preview shows the exact Ezaki Glico Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted and ready for download and use the moment you buy. You're looking at the actual file; once you complete your purchase, you’ll get instant access to this identical deliverable. No mockups, no samples.

A Must-Have Tool for Decision-Makers

Ezaki Glico operates in a fiercely competitive confectionery and processed foods market where strong brands, scale advantages, and distribution breadth lower buyer power but intensify rivalry; supplier power is moderate while substitutes and changing consumer trends raise strategic risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ezaki Glico’s competitive dynamics in detail.

Suppliers Bargaining Power

Dependence on dairy and cocoa

Core ingredients such as milk powder, cocoa and sugar face global price swings and supply concentration: Côte d'Ivoire and Ghana together supply roughly 60% of cocoa, while New Zealand supplies about 30% of global milk-powder exports. Weather, geopolitics and diseases (eg cocoa pod disease) periodically tighten availability, elevating supplier leverage in cost talks. Ezaki Glico mitigates via long-term contracts and hedging to partially offset input volatility.

Specialized packaging vendors

Specialized packaging vendors hold moderate bargaining power for Ezaki Glico because high-speed lines commonly exceed 10,000 packs/hour and require custom films and laminates, limiting interchangeable suppliers. Switching suppliers risks line downtime and quality deviations that can halt production. Qualified suppliers thus command leverage, but scale-based contracts and dual sourcing are used to balance terms and secure supply continuity in 2024 market conditions.

Scale leverage and vendor fragmentation

As of 2024 Glico’s consolidated scale across confectionery and dairy provides significant bargaining clout with suppliers, enabling volume discounts and preferred terms.

Many agricultural inputs remain highly fragmented among smallholders in Japan and Asia, which limits the negotiating power of individual growers versus a large buyer like Glico.

Consolidating spend across categories and applying vendor scorecards enforces performance and price discipline, strengthening procurement leverage and risk management.

Quality, safety, and compliance requirements

Strict Japanese and export safety standards narrow Ezaki Glico’s approved supplier pool, increasing leverage for compliant vendors and elevating input costs and switching barriers.

Targeted auditing and supplier-development programs (used industry-wide in 2024) can expand qualified suppliers over time, reducing concentration risk.

Co-investments in capacity and joint quality programs secure priority allocation and long-term supply at negotiated terms.

Logistics and geopolitical exposure

Import routes for cocoa, dairy and palm oil expose Ezaki Glico to freight and FX swings—container spot rates in 2024 were roughly 70% below 2021 peaks, yet shipping cost volatility and JPY moves still drive input-cost risk. Supply disruptions shift bargaining power to suppliers with secure upstream access, while nearshoring and inventory buffers dampen short-term leverage spikes. Active FX hedging and flexible incoterms (CIF/FOB) spread logistics risk across partners.

- Import concentration: high reliance on global suppliers

- 2024 freight normalization: ~70% down from 2021 highs

- Mitigants: nearshoring, inventory buffers, FX hedges, flexible incoterms

Cocoa and NZ milk concentration create periodic supplier leverage; firms hedge, dual-source

Core inputs (cocoa 60% from Côte d'Ivoire+Ghana; NZ ~30% of milk‑powder exports) create periodic supplier leverage via weather, disease and geopolitics. Packaging vendors exert moderate power due to high‑speed line specificity, while strict safety standards narrow approved suppliers. Glico offsets with scale, long‑term contracts, hedging, dual sourcing, supplier development and co‑investments in 2024.

| Metric | 2024 figure | Impact |

|---|---|---|

| Cocoa supply concentration | ~60% CI+GH | Higher supplier leverage |

| NZ milk‑powder exports | ~30% | Input price sensitivity |

| Container spot rates vs 2021 | ≈-70% | Lower freight but volatile |

What is included in the product

Tailored Porter's Five Forces for Ezaki Glico uncover competitive drivers, supplier/buyer power, substitute threats, and entry barriers, highlighting strategic risks and opportunities in its snack and confectionery markets.

A concise one-sheet Porter's Five Forces for Ezaki Glico—instantly highlight supplier/buyer leverage, entrant and substitute risks, and competitive rivalry to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Concentrated retail channels

Japanese convenience chains and large supermarkets exert strong shelf control over suppliers; 7-Eleven (~21,000 stores), FamilyMart (~17,000) and Lawson (~14,000) in 2024 leverage scale to extract slotting fees and push pricing concessions. Their bargaining power is reinforced by centralized purchasing and category resets, while growing private‑label penetration in packaged foods (≈15% in 2024) increases supplier pressure. Ezaki Glico partially offsets this through multi‑channel distribution (retail, e‑commerce, exports) and strong branded SKUs with proven sell‑through rates.

End-consumer price sensitivity

Snacks are discretionary and heavily promoted; Ezaki Glico faces high end-consumer price sensitivity as 2024 Japanese inflation around 2.7% increases elasticity in mass segments, driving shoppers toward promotions and private labels.

Consumers readily switch brands for small price gaps (often a few yen on single-serve items), compressing margins on core SKUs.

Premium and novelty SKUs (higher ASP) show lower price elasticity, supporting mix-driven margin recovery for Glico, whose FY2023 consolidated sales were about 456 billion JPY.

Brand loyalty to iconic SKUs

Products like Pocky—launched in 1966 and sold in over 50 countries—create strong repeat purchase stickiness, shrinking buyer leverage. Ezaki Glico reported consolidated net sales around ¥495 billion in FY2023/24, reflecting the premium pull of iconic SKUs. Limited editions and brand collaborations drive periodic spikes in demand, while loyalty programs and D2C channels deepen customer bonds and reduce price sensitivity.

Information transparency

Information transparency raises customer bargaining power for Ezaki Glico: online price comparison and reviews reduce switching costs, e-commerce share in Japan reached about 12% in 2024, and social media accelerates trend shifts that shorten product life cycles. Retailers leverage POS and loyalty data to demand sharper trade terms, while rich product content and influencer marketing partially counterbalance by strengthening brand equity.

- Price comparison: lowers switching costs

- Social media: faster trend cycles

- Retailer data: tougher trade terms

- Content/influencers: mitigate churn

Export market diversity

Export market diversity reduces single-market dependence and helped Ezaki Glico achieve overseas sales of about 20% of net sales in FY2024, lowering buyer concentration risk; buyer power varies significantly by country structure and channel, with modern trade and e‑commerce buyers exerting different pressures. Distributors in some markets demand hefty entry margins, while localized packs and a broad portfolio strengthen Glico’s negotiating stance.

- Diversified revenue: ~20% overseas (FY2024)

- Buyer power: country/channel-dependent

- Distributor margins can be high

- Localized packs boost bargaining leverage

Retailer scale, private-label and e-commerce squeeze suppliers; branded SKUs and D2C sustain power

Retail giants (7‑Eleven ~21,000; FamilyMart ~17,000; Lawson ~14,000 in 2024) exert strong shelf/price leverage; private‑label ≈15% and e‑commerce ≈12% raise supplier pressure. Ezaki Glico (net sales ¥495bn FY2023/24; overseas ~20%) offsets via branded SKUs, D2C and novelty/premium mix that reduce price elasticity. Information transparency and retailer data increase bargaining power, though iconic SKUs (Pocky) sustain stickiness.

| Metric | 2024 |

|---|---|

| Net sales | ¥495bn |

| Overseas | ≈20% |

| Private label | ≈15% |

| E‑commerce | ≈12% |

Preview the Actual Deliverable

Ezaki Glico Porter's Five Forces Analysis

This preview shows the exact Ezaki Glico Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted and ready for download and use the moment you buy. You're looking at the actual file; once you complete your purchase, you’ll get instant access to this identical deliverable. No mockups, no samples.

Description

A Must-Have Tool for Decision-Makers

Ezaki Glico operates in a fiercely competitive confectionery and processed foods market where strong brands, scale advantages, and distribution breadth lower buyer power but intensify rivalry; supplier power is moderate while substitutes and changing consumer trends raise strategic risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ezaki Glico’s competitive dynamics in detail.

Suppliers Bargaining Power

Dependence on dairy and cocoa

Core ingredients such as milk powder, cocoa and sugar face global price swings and supply concentration: Côte d'Ivoire and Ghana together supply roughly 60% of cocoa, while New Zealand supplies about 30% of global milk-powder exports. Weather, geopolitics and diseases (eg cocoa pod disease) periodically tighten availability, elevating supplier leverage in cost talks. Ezaki Glico mitigates via long-term contracts and hedging to partially offset input volatility.

Specialized packaging vendors

Specialized packaging vendors hold moderate bargaining power for Ezaki Glico because high-speed lines commonly exceed 10,000 packs/hour and require custom films and laminates, limiting interchangeable suppliers. Switching suppliers risks line downtime and quality deviations that can halt production. Qualified suppliers thus command leverage, but scale-based contracts and dual sourcing are used to balance terms and secure supply continuity in 2024 market conditions.

Scale leverage and vendor fragmentation

As of 2024 Glico’s consolidated scale across confectionery and dairy provides significant bargaining clout with suppliers, enabling volume discounts and preferred terms.

Many agricultural inputs remain highly fragmented among smallholders in Japan and Asia, which limits the negotiating power of individual growers versus a large buyer like Glico.

Consolidating spend across categories and applying vendor scorecards enforces performance and price discipline, strengthening procurement leverage and risk management.

Quality, safety, and compliance requirements

Strict Japanese and export safety standards narrow Ezaki Glico’s approved supplier pool, increasing leverage for compliant vendors and elevating input costs and switching barriers.

Targeted auditing and supplier-development programs (used industry-wide in 2024) can expand qualified suppliers over time, reducing concentration risk.

Co-investments in capacity and joint quality programs secure priority allocation and long-term supply at negotiated terms.

Logistics and geopolitical exposure

Import routes for cocoa, dairy and palm oil expose Ezaki Glico to freight and FX swings—container spot rates in 2024 were roughly 70% below 2021 peaks, yet shipping cost volatility and JPY moves still drive input-cost risk. Supply disruptions shift bargaining power to suppliers with secure upstream access, while nearshoring and inventory buffers dampen short-term leverage spikes. Active FX hedging and flexible incoterms (CIF/FOB) spread logistics risk across partners.

- Import concentration: high reliance on global suppliers

- 2024 freight normalization: ~70% down from 2021 highs

- Mitigants: nearshoring, inventory buffers, FX hedges, flexible incoterms

Cocoa and NZ milk concentration create periodic supplier leverage; firms hedge, dual-source

Core inputs (cocoa 60% from Côte d'Ivoire+Ghana; NZ ~30% of milk‑powder exports) create periodic supplier leverage via weather, disease and geopolitics. Packaging vendors exert moderate power due to high‑speed line specificity, while strict safety standards narrow approved suppliers. Glico offsets with scale, long‑term contracts, hedging, dual sourcing, supplier development and co‑investments in 2024.

| Metric | 2024 figure | Impact |

|---|---|---|

| Cocoa supply concentration | ~60% CI+GH | Higher supplier leverage |

| NZ milk‑powder exports | ~30% | Input price sensitivity |

| Container spot rates vs 2021 | ≈-70% | Lower freight but volatile |

What is included in the product

Tailored Porter's Five Forces for Ezaki Glico uncover competitive drivers, supplier/buyer power, substitute threats, and entry barriers, highlighting strategic risks and opportunities in its snack and confectionery markets.

A concise one-sheet Porter's Five Forces for Ezaki Glico—instantly highlight supplier/buyer leverage, entrant and substitute risks, and competitive rivalry to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Concentrated retail channels

Japanese convenience chains and large supermarkets exert strong shelf control over suppliers; 7-Eleven (~21,000 stores), FamilyMart (~17,000) and Lawson (~14,000) in 2024 leverage scale to extract slotting fees and push pricing concessions. Their bargaining power is reinforced by centralized purchasing and category resets, while growing private‑label penetration in packaged foods (≈15% in 2024) increases supplier pressure. Ezaki Glico partially offsets this through multi‑channel distribution (retail, e‑commerce, exports) and strong branded SKUs with proven sell‑through rates.

End-consumer price sensitivity

Snacks are discretionary and heavily promoted; Ezaki Glico faces high end-consumer price sensitivity as 2024 Japanese inflation around 2.7% increases elasticity in mass segments, driving shoppers toward promotions and private labels.

Consumers readily switch brands for small price gaps (often a few yen on single-serve items), compressing margins on core SKUs.

Premium and novelty SKUs (higher ASP) show lower price elasticity, supporting mix-driven margin recovery for Glico, whose FY2023 consolidated sales were about 456 billion JPY.

Brand loyalty to iconic SKUs

Products like Pocky—launched in 1966 and sold in over 50 countries—create strong repeat purchase stickiness, shrinking buyer leverage. Ezaki Glico reported consolidated net sales around ¥495 billion in FY2023/24, reflecting the premium pull of iconic SKUs. Limited editions and brand collaborations drive periodic spikes in demand, while loyalty programs and D2C channels deepen customer bonds and reduce price sensitivity.

Information transparency

Information transparency raises customer bargaining power for Ezaki Glico: online price comparison and reviews reduce switching costs, e-commerce share in Japan reached about 12% in 2024, and social media accelerates trend shifts that shorten product life cycles. Retailers leverage POS and loyalty data to demand sharper trade terms, while rich product content and influencer marketing partially counterbalance by strengthening brand equity.

- Price comparison: lowers switching costs

- Social media: faster trend cycles

- Retailer data: tougher trade terms

- Content/influencers: mitigate churn

Export market diversity

Export market diversity reduces single-market dependence and helped Ezaki Glico achieve overseas sales of about 20% of net sales in FY2024, lowering buyer concentration risk; buyer power varies significantly by country structure and channel, with modern trade and e‑commerce buyers exerting different pressures. Distributors in some markets demand hefty entry margins, while localized packs and a broad portfolio strengthen Glico’s negotiating stance.

- Diversified revenue: ~20% overseas (FY2024)

- Buyer power: country/channel-dependent

- Distributor margins can be high

- Localized packs boost bargaining leverage

Retailer scale, private-label and e-commerce squeeze suppliers; branded SKUs and D2C sustain power

Retail giants (7‑Eleven ~21,000; FamilyMart ~17,000; Lawson ~14,000 in 2024) exert strong shelf/price leverage; private‑label ≈15% and e‑commerce ≈12% raise supplier pressure. Ezaki Glico (net sales ¥495bn FY2023/24; overseas ~20%) offsets via branded SKUs, D2C and novelty/premium mix that reduce price elasticity. Information transparency and retailer data increase bargaining power, though iconic SKUs (Pocky) sustain stickiness.

| Metric | 2024 |

|---|---|

| Net sales | ¥495bn |

| Overseas | ≈20% |

| Private label | ≈15% |

| E‑commerce | ≈12% |

Preview the Actual Deliverable

Ezaki Glico Porter's Five Forces Analysis

This preview shows the exact Ezaki Glico Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted and ready for download and use the moment you buy. You're looking at the actual file; once you complete your purchase, you’ll get instant access to this identical deliverable. No mockups, no samples.