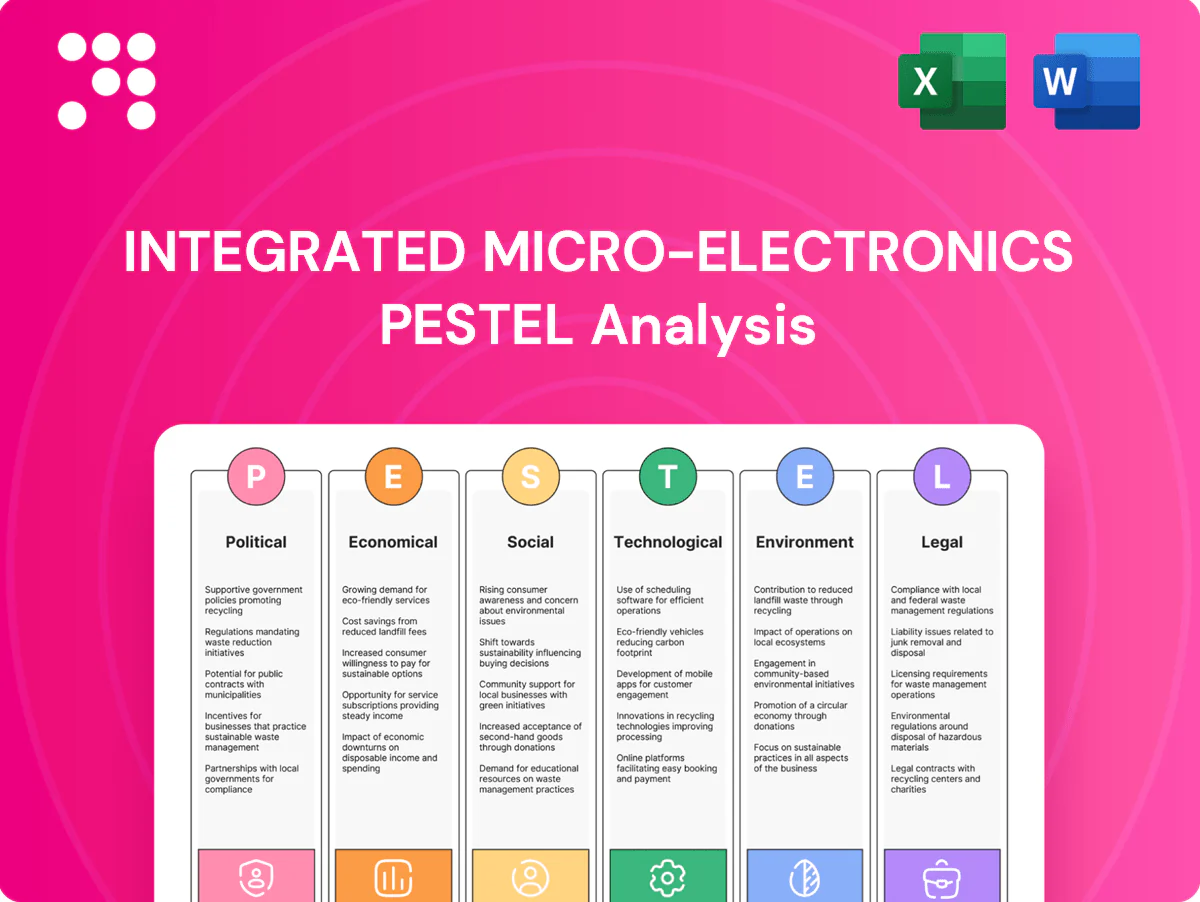

Integrated Micro-Electronics PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, social trends, technological advances, regulatory changes, and environmental pressures are shaping Integrated Micro‑Electronics's strategic outlook in our concise PESTLE briefing. This focused snapshot highlights risks and growth levers to inform investor and management decisions. Purchase the full PESTLE for a complete, actionable breakdown ready for immediate use.

Political factors

Trade policy and tariffs exposure

As a cross-border EMS/SATS provider, IMI is sensitive to tariff regimes on electronics, PCBs and semiconductors, notably US Section 301 rates ranging from 7.5% to 25% on covered goods. Shifts in US‑China, EU‑China and ASEAN trade rules (ASEAN = 10 members) can alter landed costs and sourcing routes, while RCEP (covering ~30% of global GDP) and other FTAs can enhance competitiveness. Active footprint optimization and bonded‑zone strategies mitigate volatility.

Geopolitical supply chain risk

Regional tensions in the Taiwan Strait, where Taiwan accounts for roughly 63% of global semiconductor foundry capacity, and in the South China Sea, which handles about one-third of global shipping, threaten component flows and logistics. Automotive and aerospace defense customers mandate resilience and dual sourcing under standards such as IATF 16949. IMI must hold contingency inventories and enable multi-site routing across ASEAN and beyond. Political risk insurance and formal scenario planning are critical risk mitigants.

Industrial policy and incentives

US CHIPS and Science Act backs roughly $52 billion for semiconductor manufacturing, while ASEAN moves like the Philippines CREATE cut headline corporate tax to 25% and Thailand BOI offers tax holidays up to 8 years and Malaysia Pioneer Status up to 5 years, all shaping plant siting. Government EV and power-electronics programs—with EV adoption scaling rapidly—raise SATS demand. Competing locations now offer grants and training subsidies for automation and upskilling. IMI can capture incentives to cut effective capex and speed capacity adds.

Defense and export controls

A&D programs face US ITAR and EAR, the EU Dual-Use Regulation (Reg. 2021/821) and national defense offset rules; these regimes determine which IMI sites may host sensitive assemblies and export-controlled test flows. Policy tightening or new end-use controls can force production re-routing or additional export licenses, and licensing or classification actions commonly introduce delays measured in weeks to months. Early engagement with export authorities and in-house compliance reduces delivery risk and helps preserve revenue timelines.

- ITAR/EAR: controls on defense articles and tech

- EU Dual-Use Reg. 2021/821: applies to sensitive components

- Local offsets: shape sourcing and site eligibility

- Impact: potential weeks–months of licensing delays

Public health and stability

Policy responses to pandemics and natural disasters directly affect factory uptime and cross-border labor mobility; clear protocols and government coordination sustain essential manufacturing status and limit stoppages. Political stability in host countries underpins long-term contracts and capital deployment. IMI benefits from diversified operations across six countries, lowering single-country disruption risk.

- Factory uptime sensitivity: dependent on host-country health protocols

- Essential status reduces shutdown risk

- Stability supports multi-year contracts

- Diversification: operations in Philippines, Thailand, China, Indonesia, Mexico, US

Tariffs, foundry concentration and shipping chokepoints vs $52B CHIPS and six-country buffer

IMI faces tariff exposure (US Sec.301 7.5–25%) and shifting US/EU/ASEAN trade rules that affect landed costs; RCEP and FTAs can lower duties. Taiwan holds ~63% of global foundry capacity and the South China Sea handles ~30% of shipping, creating concentration risk. US CHIPS provides ~$52B in semiconductor support; IMI's six-country footprint (PH, TH, CN, ID, MX, US) aids resilience.

| Risk | Metric | Impact |

|---|---|---|

| Tariffs | 7.5–25% | Higher COGS |

| Foundry concentration | ~63% | Single-point supply risk |

| Shipping | ~30% | Logistics disruption |

| Subsidies | $52B CHIPS | Onshoring incentives |

| Footprint | 6 countries | Mitigates country risk |

What is included in the product

Explores how macro-environmental forces uniquely affect Integrated Micro‑Electronics across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region/industry context to identify threats and opportunities for executives, investors and strategists; includes forward-looking insights for scenario planning and funding readiness.

A concise, visually segmented PESTLE summary for Integrated Micro‑Electronics that streamlines stakeholder briefings and risk discussions, easily dropped into presentations, annotated for local context, and shared across teams for fast alignment.

Economic factors

Automotive and industrial demand cycles

EMS volumes track global manufacturing PMI (around 50 in 2024), light-vehicle builds (~82m units in 2024) and capex cycles, so slowdowns push mix toward aftermarket and value engineering while upcycles favor NPI ramps. IMI’s exposure to EVs (new-car EV share ~14% in 2024), ADAS and factory automation helps cushion cycles. Flexible staffing and modular lines preserve utilization and margin resilience.

Component pricing and inventory

Silicon, substrate and passive component markets continued to show periodic shortages and price swings into 2024–25, driving expedited freight premiums and occasional supplier-induced lead-time spikes. Bullwhip effects have produced inventory write-downs or expedited-costs for EMS players. Robust S&OP and VMI programs materially cut working capital strain for contract manufacturers. Customer pass-through clauses have been used to protect margins.

FX fluctuations

Integrated Micro-Electronics faces translation and transaction risk from multi-currency revenues and costs (USD, EUR, CNY, PHP, MXN); with the US dollar index around 104 in mid-2025, realized volatility has compressed margins when unhedged. Hedging programs and natural offsets (local sourcing, USD invoicing) are essential to limit EBT swings. Pricing in customer currency with indexed adjustments has stabilized gross margin in recent quarters. Location mix decisions increasingly weigh FX competitiveness and local cost dynamics.

Interest rates and capital intensity

- Higher rates increase capex cost

- Customer program delays lengthen paybacks

- Prioritize ROI lines and co‑investment

- Leasing/supplier finance cushions cash flow

Customer consolidation and pricing power

Large OEM and Tier-1 customers force tight pricing and annual productivity givebacks, pushing IMI to exchange price for volume, contract length, or higher engineering content to preserve margins. Advancing into design, test and system integration has raised gross margins for EMS peers and reduces IMI's reliance on commodity assembly. Diversifying end-markets cuts concentration risk and stabilizes revenue.

- Customer concentration: forces pricing trade-offs

- Higher-value services: improves margins

- Volume/tenure: used to secure contracts

- Vertical diversification: lowers risk

Tariffs, foundry concentration and shipping chokepoints vs $52B CHIPS and six-country buffer

EMS volumes track PMI ~50 and light‑vehicle builds ~82M (2024); slowdowns shift mix to aftermarket while upcycles boost NPI. EV share ~14% (2024), ADAS and factory automation cushion cycles. USD index ~104 (mid‑2025) and multi‑currency exposure raise FX risk; hedging and local sourcing mitigate. Fed funds 5.25–5.50% (mid‑2024/25) lifts capex costs; IME uses co‑investment, leasing and supplier finance.

| Metric | Value |

|---|---|

| Global PMI | ~50 (2024) |

| Light‑vehicle builds | ~82M (2024) |

| EV new‑car share | ~14% (2024) |

| USD Index | ~104 (mid‑2025) |

| Fed funds | 5.25–5.50% (mid‑2024/25) |

Same Document Delivered

Integrated Micro-Electronics PESTLE Analysis

The preview shown here is the exact Integrated Micro-Electronics PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It includes political, economic, social, technological, legal, and environmental factors with actionable insights and data sources. No placeholders or teasers—this is the final, professionally structured file available for immediate download.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, social trends, technological advances, regulatory changes, and environmental pressures are shaping Integrated Micro‑Electronics's strategic outlook in our concise PESTLE briefing. This focused snapshot highlights risks and growth levers to inform investor and management decisions. Purchase the full PESTLE for a complete, actionable breakdown ready for immediate use.

Political factors

Trade policy and tariffs exposure

As a cross-border EMS/SATS provider, IMI is sensitive to tariff regimes on electronics, PCBs and semiconductors, notably US Section 301 rates ranging from 7.5% to 25% on covered goods. Shifts in US‑China, EU‑China and ASEAN trade rules (ASEAN = 10 members) can alter landed costs and sourcing routes, while RCEP (covering ~30% of global GDP) and other FTAs can enhance competitiveness. Active footprint optimization and bonded‑zone strategies mitigate volatility.

Geopolitical supply chain risk

Regional tensions in the Taiwan Strait, where Taiwan accounts for roughly 63% of global semiconductor foundry capacity, and in the South China Sea, which handles about one-third of global shipping, threaten component flows and logistics. Automotive and aerospace defense customers mandate resilience and dual sourcing under standards such as IATF 16949. IMI must hold contingency inventories and enable multi-site routing across ASEAN and beyond. Political risk insurance and formal scenario planning are critical risk mitigants.

Industrial policy and incentives

US CHIPS and Science Act backs roughly $52 billion for semiconductor manufacturing, while ASEAN moves like the Philippines CREATE cut headline corporate tax to 25% and Thailand BOI offers tax holidays up to 8 years and Malaysia Pioneer Status up to 5 years, all shaping plant siting. Government EV and power-electronics programs—with EV adoption scaling rapidly—raise SATS demand. Competing locations now offer grants and training subsidies for automation and upskilling. IMI can capture incentives to cut effective capex and speed capacity adds.

Defense and export controls

A&D programs face US ITAR and EAR, the EU Dual-Use Regulation (Reg. 2021/821) and national defense offset rules; these regimes determine which IMI sites may host sensitive assemblies and export-controlled test flows. Policy tightening or new end-use controls can force production re-routing or additional export licenses, and licensing or classification actions commonly introduce delays measured in weeks to months. Early engagement with export authorities and in-house compliance reduces delivery risk and helps preserve revenue timelines.

- ITAR/EAR: controls on defense articles and tech

- EU Dual-Use Reg. 2021/821: applies to sensitive components

- Local offsets: shape sourcing and site eligibility

- Impact: potential weeks–months of licensing delays

Public health and stability

Policy responses to pandemics and natural disasters directly affect factory uptime and cross-border labor mobility; clear protocols and government coordination sustain essential manufacturing status and limit stoppages. Political stability in host countries underpins long-term contracts and capital deployment. IMI benefits from diversified operations across six countries, lowering single-country disruption risk.

- Factory uptime sensitivity: dependent on host-country health protocols

- Essential status reduces shutdown risk

- Stability supports multi-year contracts

- Diversification: operations in Philippines, Thailand, China, Indonesia, Mexico, US

Tariffs, foundry concentration and shipping chokepoints vs $52B CHIPS and six-country buffer

IMI faces tariff exposure (US Sec.301 7.5–25%) and shifting US/EU/ASEAN trade rules that affect landed costs; RCEP and FTAs can lower duties. Taiwan holds ~63% of global foundry capacity and the South China Sea handles ~30% of shipping, creating concentration risk. US CHIPS provides ~$52B in semiconductor support; IMI's six-country footprint (PH, TH, CN, ID, MX, US) aids resilience.

| Risk | Metric | Impact |

|---|---|---|

| Tariffs | 7.5–25% | Higher COGS |

| Foundry concentration | ~63% | Single-point supply risk |

| Shipping | ~30% | Logistics disruption |

| Subsidies | $52B CHIPS | Onshoring incentives |

| Footprint | 6 countries | Mitigates country risk |

What is included in the product

Explores how macro-environmental forces uniquely affect Integrated Micro‑Electronics across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region/industry context to identify threats and opportunities for executives, investors and strategists; includes forward-looking insights for scenario planning and funding readiness.

A concise, visually segmented PESTLE summary for Integrated Micro‑Electronics that streamlines stakeholder briefings and risk discussions, easily dropped into presentations, annotated for local context, and shared across teams for fast alignment.

Economic factors

Automotive and industrial demand cycles

EMS volumes track global manufacturing PMI (around 50 in 2024), light-vehicle builds (~82m units in 2024) and capex cycles, so slowdowns push mix toward aftermarket and value engineering while upcycles favor NPI ramps. IMI’s exposure to EVs (new-car EV share ~14% in 2024), ADAS and factory automation helps cushion cycles. Flexible staffing and modular lines preserve utilization and margin resilience.

Component pricing and inventory

Silicon, substrate and passive component markets continued to show periodic shortages and price swings into 2024–25, driving expedited freight premiums and occasional supplier-induced lead-time spikes. Bullwhip effects have produced inventory write-downs or expedited-costs for EMS players. Robust S&OP and VMI programs materially cut working capital strain for contract manufacturers. Customer pass-through clauses have been used to protect margins.

FX fluctuations

Integrated Micro-Electronics faces translation and transaction risk from multi-currency revenues and costs (USD, EUR, CNY, PHP, MXN); with the US dollar index around 104 in mid-2025, realized volatility has compressed margins when unhedged. Hedging programs and natural offsets (local sourcing, USD invoicing) are essential to limit EBT swings. Pricing in customer currency with indexed adjustments has stabilized gross margin in recent quarters. Location mix decisions increasingly weigh FX competitiveness and local cost dynamics.

Interest rates and capital intensity

- Higher rates increase capex cost

- Customer program delays lengthen paybacks

- Prioritize ROI lines and co‑investment

- Leasing/supplier finance cushions cash flow

Customer consolidation and pricing power

Large OEM and Tier-1 customers force tight pricing and annual productivity givebacks, pushing IMI to exchange price for volume, contract length, or higher engineering content to preserve margins. Advancing into design, test and system integration has raised gross margins for EMS peers and reduces IMI's reliance on commodity assembly. Diversifying end-markets cuts concentration risk and stabilizes revenue.

- Customer concentration: forces pricing trade-offs

- Higher-value services: improves margins

- Volume/tenure: used to secure contracts

- Vertical diversification: lowers risk

Tariffs, foundry concentration and shipping chokepoints vs $52B CHIPS and six-country buffer

EMS volumes track PMI ~50 and light‑vehicle builds ~82M (2024); slowdowns shift mix to aftermarket while upcycles boost NPI. EV share ~14% (2024), ADAS and factory automation cushion cycles. USD index ~104 (mid‑2025) and multi‑currency exposure raise FX risk; hedging and local sourcing mitigate. Fed funds 5.25–5.50% (mid‑2024/25) lifts capex costs; IME uses co‑investment, leasing and supplier finance.

| Metric | Value |

|---|---|

| Global PMI | ~50 (2024) |

| Light‑vehicle builds | ~82M (2024) |

| EV new‑car share | ~14% (2024) |

| USD Index | ~104 (mid‑2025) |

| Fed funds | 5.25–5.50% (mid‑2024/25) |

Same Document Delivered

Integrated Micro-Electronics PESTLE Analysis

The preview shown here is the exact Integrated Micro-Electronics PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It includes political, economic, social, technological, legal, and environmental factors with actionable insights and data sources. No placeholders or teasers—this is the final, professionally structured file available for immediate download.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, social trends, technological advances, regulatory changes, and environmental pressures are shaping Integrated Micro‑Electronics's strategic outlook in our concise PESTLE briefing. This focused snapshot highlights risks and growth levers to inform investor and management decisions. Purchase the full PESTLE for a complete, actionable breakdown ready for immediate use.

Political factors

Trade policy and tariffs exposure

As a cross-border EMS/SATS provider, IMI is sensitive to tariff regimes on electronics, PCBs and semiconductors, notably US Section 301 rates ranging from 7.5% to 25% on covered goods. Shifts in US‑China, EU‑China and ASEAN trade rules (ASEAN = 10 members) can alter landed costs and sourcing routes, while RCEP (covering ~30% of global GDP) and other FTAs can enhance competitiveness. Active footprint optimization and bonded‑zone strategies mitigate volatility.

Geopolitical supply chain risk

Regional tensions in the Taiwan Strait, where Taiwan accounts for roughly 63% of global semiconductor foundry capacity, and in the South China Sea, which handles about one-third of global shipping, threaten component flows and logistics. Automotive and aerospace defense customers mandate resilience and dual sourcing under standards such as IATF 16949. IMI must hold contingency inventories and enable multi-site routing across ASEAN and beyond. Political risk insurance and formal scenario planning are critical risk mitigants.

Industrial policy and incentives

US CHIPS and Science Act backs roughly $52 billion for semiconductor manufacturing, while ASEAN moves like the Philippines CREATE cut headline corporate tax to 25% and Thailand BOI offers tax holidays up to 8 years and Malaysia Pioneer Status up to 5 years, all shaping plant siting. Government EV and power-electronics programs—with EV adoption scaling rapidly—raise SATS demand. Competing locations now offer grants and training subsidies for automation and upskilling. IMI can capture incentives to cut effective capex and speed capacity adds.

Defense and export controls

A&D programs face US ITAR and EAR, the EU Dual-Use Regulation (Reg. 2021/821) and national defense offset rules; these regimes determine which IMI sites may host sensitive assemblies and export-controlled test flows. Policy tightening or new end-use controls can force production re-routing or additional export licenses, and licensing or classification actions commonly introduce delays measured in weeks to months. Early engagement with export authorities and in-house compliance reduces delivery risk and helps preserve revenue timelines.

- ITAR/EAR: controls on defense articles and tech

- EU Dual-Use Reg. 2021/821: applies to sensitive components

- Local offsets: shape sourcing and site eligibility

- Impact: potential weeks–months of licensing delays

Public health and stability

Policy responses to pandemics and natural disasters directly affect factory uptime and cross-border labor mobility; clear protocols and government coordination sustain essential manufacturing status and limit stoppages. Political stability in host countries underpins long-term contracts and capital deployment. IMI benefits from diversified operations across six countries, lowering single-country disruption risk.

- Factory uptime sensitivity: dependent on host-country health protocols

- Essential status reduces shutdown risk

- Stability supports multi-year contracts

- Diversification: operations in Philippines, Thailand, China, Indonesia, Mexico, US

Tariffs, foundry concentration and shipping chokepoints vs $52B CHIPS and six-country buffer

IMI faces tariff exposure (US Sec.301 7.5–25%) and shifting US/EU/ASEAN trade rules that affect landed costs; RCEP and FTAs can lower duties. Taiwan holds ~63% of global foundry capacity and the South China Sea handles ~30% of shipping, creating concentration risk. US CHIPS provides ~$52B in semiconductor support; IMI's six-country footprint (PH, TH, CN, ID, MX, US) aids resilience.

| Risk | Metric | Impact |

|---|---|---|

| Tariffs | 7.5–25% | Higher COGS |

| Foundry concentration | ~63% | Single-point supply risk |

| Shipping | ~30% | Logistics disruption |

| Subsidies | $52B CHIPS | Onshoring incentives |

| Footprint | 6 countries | Mitigates country risk |

What is included in the product

Explores how macro-environmental forces uniquely affect Integrated Micro‑Electronics across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region/industry context to identify threats and opportunities for executives, investors and strategists; includes forward-looking insights for scenario planning and funding readiness.

A concise, visually segmented PESTLE summary for Integrated Micro‑Electronics that streamlines stakeholder briefings and risk discussions, easily dropped into presentations, annotated for local context, and shared across teams for fast alignment.

Economic factors

Automotive and industrial demand cycles

EMS volumes track global manufacturing PMI (around 50 in 2024), light-vehicle builds (~82m units in 2024) and capex cycles, so slowdowns push mix toward aftermarket and value engineering while upcycles favor NPI ramps. IMI’s exposure to EVs (new-car EV share ~14% in 2024), ADAS and factory automation helps cushion cycles. Flexible staffing and modular lines preserve utilization and margin resilience.

Component pricing and inventory

Silicon, substrate and passive component markets continued to show periodic shortages and price swings into 2024–25, driving expedited freight premiums and occasional supplier-induced lead-time spikes. Bullwhip effects have produced inventory write-downs or expedited-costs for EMS players. Robust S&OP and VMI programs materially cut working capital strain for contract manufacturers. Customer pass-through clauses have been used to protect margins.

FX fluctuations

Integrated Micro-Electronics faces translation and transaction risk from multi-currency revenues and costs (USD, EUR, CNY, PHP, MXN); with the US dollar index around 104 in mid-2025, realized volatility has compressed margins when unhedged. Hedging programs and natural offsets (local sourcing, USD invoicing) are essential to limit EBT swings. Pricing in customer currency with indexed adjustments has stabilized gross margin in recent quarters. Location mix decisions increasingly weigh FX competitiveness and local cost dynamics.

Interest rates and capital intensity

- Higher rates increase capex cost

- Customer program delays lengthen paybacks

- Prioritize ROI lines and co‑investment

- Leasing/supplier finance cushions cash flow

Customer consolidation and pricing power

Large OEM and Tier-1 customers force tight pricing and annual productivity givebacks, pushing IMI to exchange price for volume, contract length, or higher engineering content to preserve margins. Advancing into design, test and system integration has raised gross margins for EMS peers and reduces IMI's reliance on commodity assembly. Diversifying end-markets cuts concentration risk and stabilizes revenue.

- Customer concentration: forces pricing trade-offs

- Higher-value services: improves margins

- Volume/tenure: used to secure contracts

- Vertical diversification: lowers risk

Tariffs, foundry concentration and shipping chokepoints vs $52B CHIPS and six-country buffer

EMS volumes track PMI ~50 and light‑vehicle builds ~82M (2024); slowdowns shift mix to aftermarket while upcycles boost NPI. EV share ~14% (2024), ADAS and factory automation cushion cycles. USD index ~104 (mid‑2025) and multi‑currency exposure raise FX risk; hedging and local sourcing mitigate. Fed funds 5.25–5.50% (mid‑2024/25) lifts capex costs; IME uses co‑investment, leasing and supplier finance.

| Metric | Value |

|---|---|

| Global PMI | ~50 (2024) |

| Light‑vehicle builds | ~82M (2024) |

| EV new‑car share | ~14% (2024) |

| USD Index | ~104 (mid‑2025) |

| Fed funds | 5.25–5.50% (mid‑2024/25) |

Same Document Delivered

Integrated Micro-Electronics PESTLE Analysis

The preview shown here is the exact Integrated Micro-Electronics PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It includes political, economic, social, technological, legal, and environmental factors with actionable insights and data sources. No placeholders or teasers—this is the final, professionally structured file available for immediate download.