Globe Life Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

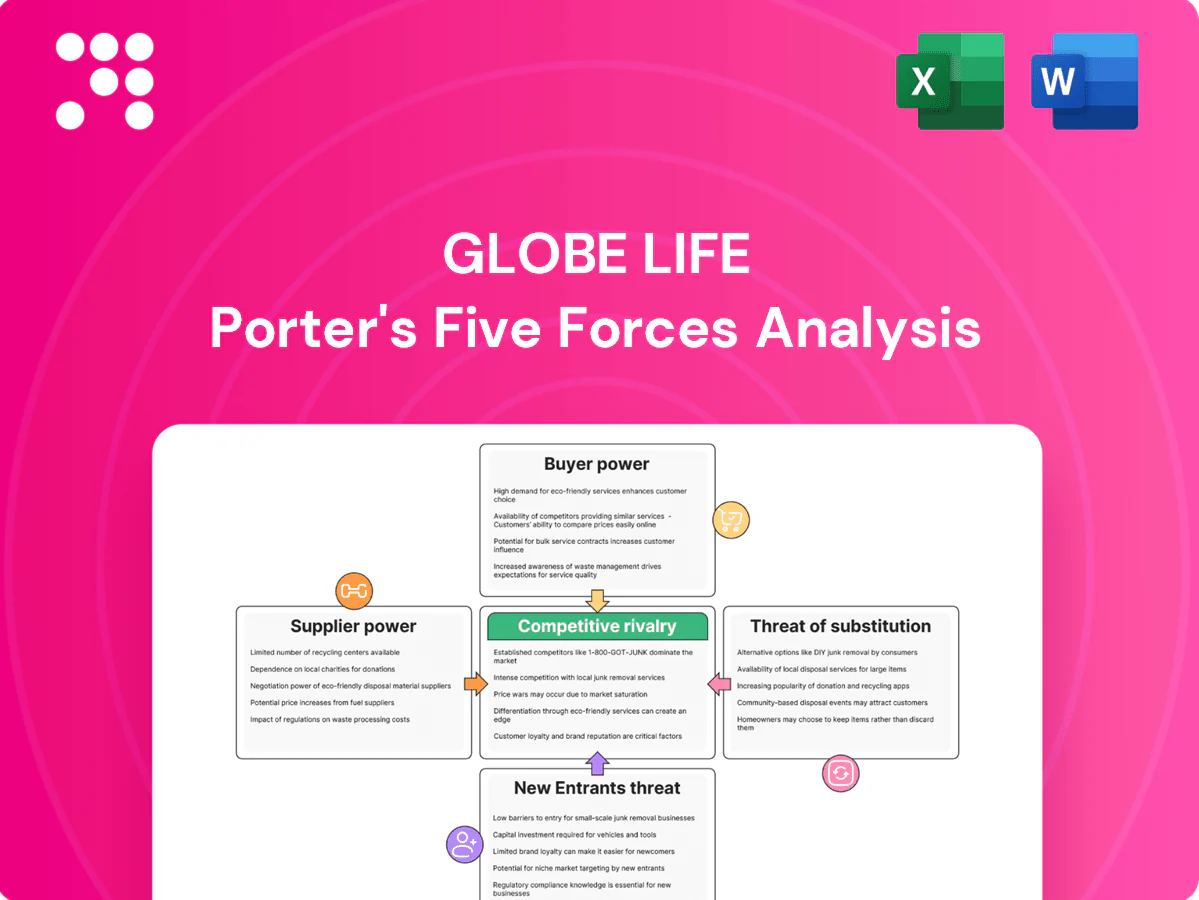

Globe Life’s Porter's Five Forces snapshot highlights concentrated buyer dynamics, moderate supplier leverage, low threat of substitutes for core life products, and regulatory-driven entry barriers. Competitive rivalry centers on price and distribution efficiency. This brief teases strategic implications and risk hotspots. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated reinsurers

Globe Life relies on a limited pool of highly rated reinsurers for risk transfer, and concentrated reinsurer markets can tighten terms, raise ceding costs, or restrict capacity during stressed markets. This concentration elevates supplier leverage over pricing and product design, though Globe Life reported a statutory surplus of about $3.9 billion at YE 2024, which and diversified treaties mitigate but do not eliminate that power.

Distribution partners as suppliers

Independent brokers and captive agencies supply most of Globe Life’s policy flow, with the company reporting roughly $6.0 billion in 2024 revenues that are heavily distribution-driven. High-performing agencies can and do secure higher commissions, enhanced marketing support, or exclusive products to protect share. Channel conflict risks force concessions to retain volume. Multi-channel distribution reduces any single partner’s leverage.

Data, tech, and underwriting tools

Third-party data vendors, the three major credit bureaus, and specialized underwriting platforms provide indispensable, highly specialized inputs for Globe Life, creating moderate supplier power. Vendor switching entails costly integrations, regulatory compliance updates, and model recalibration, producing price stickiness and partial lock-in. Growing vendor competition and expanding in-house analytics capabilities are reducing dependency over time.

Medical networks and TPA services

Supplemental health admin for Globe Life relies heavily on TPAs, networks, and claims processors; their quality and turnaround times (SLAs often target under 30 days) materially affect loss ratios and retention, giving specialized suppliers measurable bargaining leverage.

- TPA reliance: concentration risk

- SLAs: sub-30 day target

- Dual-sourcing reduces supplier power

Capital and rating agencies’ influence

- Rating influence: agencies set covenant/coverage benchmarks

- Market signal: 10y UST ~4.2% (2024)

- Credit squeeze: raises cost of new debt

- Mitigation: conservative capital and liquidity buffers

Insurer faces reinsurer power despite $3.9B surplus

Globe Life faces elevated supplier power from concentrated reinsurers despite a $3.9B statutory surplus (YE 2024), and distribution partners (2024 revenue ~$6.0B) can extract concessions to protect share. Data vendors, TPAs and rating agencies exert moderate leverage; SLA targets <30 days and 10y UST ~4.2% (2024) shape costs and capacity.

| Metric | 2024 |

|---|---|

| Statutory surplus | $3.9B |

| Revenue | $6.0B |

| 10y UST | ~4.2% |

| SLA target | <30 days |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Globe Life, with detailed assessment of supplier/buyer power, substitutes, new entrants, and industry rivalry to highlight disruptive threats, pricing pressure, and protective dynamics for strategy and investor use.

A clear, one-sheet summary of Globe Life's five forces for quick strategic decisions, ready to copy into pitch decks or boardroom slides. Includes an editable spider chart and no-complex-code layout so teams can customize pressure levels by market changes without needing finance experts.

Customers Bargaining Power

Price-sensitive target segment

Middle and lower-middle-income customers are highly price conscious, making small premium differences a common reason for policy selection and lapses in commoditized offerings like term life and final expense. This dynamic increases buyer power and compresses margins for Globe Life unless differentiated value is clearly communicated. Emphasizing guaranteed benefits, simplified underwriting, and agent-led explanations helps sustain retention and pricing power.

Low switching costs

Policies—especially simple life coverage—are easy to replace, and over 70% of US shoppers researched insurance online in 2024, increasing transparency via digital comparison tools. State replacement rules require disclosure but rarely block switches. Persistency programs and loyalty benefits help Globe Life curb churn and sustain renewal rates above industry averages.

Product simplicity and comparability

Simplified-issue life products are highly comparable across carriers, making price and rate tables easy for buyers to benchmark. Limited riders and similar benefit structures amplify price competition and enable purchasers to press for discounts, bundling, or upgraded underwriting classes. Where Globe Life differentiates through fast issue processes, distribution reach, and brand recognition, customer bargaining power is softened by perceived service value.

Direct response channel effects

Globe Life’s direct-response channel cuts intermediary commission drag and reduces broker comparison, lowering buyer power, but digital buyers in 2024 expect frictionless UX and fast underwriting decisions; poor UX raises abandonment and price sensitivity, impacting conversion and lifetime value.

Claims experience and trust

Claims experience and trust drive customer bargaining power for Globe Life: policyholders prioritize rapid, fair claims over product features, and negative reviews or delays sharply amplify skepticism and leverage; Globe Life reported roughly $5.0 billion revenue in 2024, where transparent claims handling supports modest premium differentials and strong reputation lowers pushback.

- Claims speed: key demand driver

- Negative reviews increase churn risk

- Transparency allows premium premiumization

- Reputation cuts buyer leverage

70%+ research insurance online; D2C sales and fast claims erode buyer bargaining power

Customers are price sensitive—small premium gaps drive selection and lapses in commoditized products, increasing buyer power. Over 70% of US shoppers researched insurance online in 2024, raising transparency and comparison pressure. Globe Life reported roughly $5.0 billion revenue in 2024; direct-to-consumer distribution and fast claims handling soften bargaining power.

| Metric | 2024 |

|---|---|

| Online research rate | Over 70% |

| Revenue | $5.0 billion |

Same Document Delivered

Globe Life Porter's Five Forces Analysis

This preview shows the complete Globe Life Porter's Five Forces Analysis and is the exact document you will receive immediately after purchase. It is fully formatted, professionally written, and ready for download and use—no samples, placeholders, or extra setup required. Instant access follows payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Globe Life’s Porter's Five Forces snapshot highlights concentrated buyer dynamics, moderate supplier leverage, low threat of substitutes for core life products, and regulatory-driven entry barriers. Competitive rivalry centers on price and distribution efficiency. This brief teases strategic implications and risk hotspots. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated reinsurers

Globe Life relies on a limited pool of highly rated reinsurers for risk transfer, and concentrated reinsurer markets can tighten terms, raise ceding costs, or restrict capacity during stressed markets. This concentration elevates supplier leverage over pricing and product design, though Globe Life reported a statutory surplus of about $3.9 billion at YE 2024, which and diversified treaties mitigate but do not eliminate that power.

Distribution partners as suppliers

Independent brokers and captive agencies supply most of Globe Life’s policy flow, with the company reporting roughly $6.0 billion in 2024 revenues that are heavily distribution-driven. High-performing agencies can and do secure higher commissions, enhanced marketing support, or exclusive products to protect share. Channel conflict risks force concessions to retain volume. Multi-channel distribution reduces any single partner’s leverage.

Data, tech, and underwriting tools

Third-party data vendors, the three major credit bureaus, and specialized underwriting platforms provide indispensable, highly specialized inputs for Globe Life, creating moderate supplier power. Vendor switching entails costly integrations, regulatory compliance updates, and model recalibration, producing price stickiness and partial lock-in. Growing vendor competition and expanding in-house analytics capabilities are reducing dependency over time.

Medical networks and TPA services

Supplemental health admin for Globe Life relies heavily on TPAs, networks, and claims processors; their quality and turnaround times (SLAs often target under 30 days) materially affect loss ratios and retention, giving specialized suppliers measurable bargaining leverage.

- TPA reliance: concentration risk

- SLAs: sub-30 day target

- Dual-sourcing reduces supplier power

Capital and rating agencies’ influence

- Rating influence: agencies set covenant/coverage benchmarks

- Market signal: 10y UST ~4.2% (2024)

- Credit squeeze: raises cost of new debt

- Mitigation: conservative capital and liquidity buffers

Insurer faces reinsurer power despite $3.9B surplus

Globe Life faces elevated supplier power from concentrated reinsurers despite a $3.9B statutory surplus (YE 2024), and distribution partners (2024 revenue ~$6.0B) can extract concessions to protect share. Data vendors, TPAs and rating agencies exert moderate leverage; SLA targets <30 days and 10y UST ~4.2% (2024) shape costs and capacity.

| Metric | 2024 |

|---|---|

| Statutory surplus | $3.9B |

| Revenue | $6.0B |

| 10y UST | ~4.2% |

| SLA target | <30 days |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Globe Life, with detailed assessment of supplier/buyer power, substitutes, new entrants, and industry rivalry to highlight disruptive threats, pricing pressure, and protective dynamics for strategy and investor use.

A clear, one-sheet summary of Globe Life's five forces for quick strategic decisions, ready to copy into pitch decks or boardroom slides. Includes an editable spider chart and no-complex-code layout so teams can customize pressure levels by market changes without needing finance experts.

Customers Bargaining Power

Price-sensitive target segment

Middle and lower-middle-income customers are highly price conscious, making small premium differences a common reason for policy selection and lapses in commoditized offerings like term life and final expense. This dynamic increases buyer power and compresses margins for Globe Life unless differentiated value is clearly communicated. Emphasizing guaranteed benefits, simplified underwriting, and agent-led explanations helps sustain retention and pricing power.

Low switching costs

Policies—especially simple life coverage—are easy to replace, and over 70% of US shoppers researched insurance online in 2024, increasing transparency via digital comparison tools. State replacement rules require disclosure but rarely block switches. Persistency programs and loyalty benefits help Globe Life curb churn and sustain renewal rates above industry averages.

Product simplicity and comparability

Simplified-issue life products are highly comparable across carriers, making price and rate tables easy for buyers to benchmark. Limited riders and similar benefit structures amplify price competition and enable purchasers to press for discounts, bundling, or upgraded underwriting classes. Where Globe Life differentiates through fast issue processes, distribution reach, and brand recognition, customer bargaining power is softened by perceived service value.

Direct response channel effects

Globe Life’s direct-response channel cuts intermediary commission drag and reduces broker comparison, lowering buyer power, but digital buyers in 2024 expect frictionless UX and fast underwriting decisions; poor UX raises abandonment and price sensitivity, impacting conversion and lifetime value.

Claims experience and trust

Claims experience and trust drive customer bargaining power for Globe Life: policyholders prioritize rapid, fair claims over product features, and negative reviews or delays sharply amplify skepticism and leverage; Globe Life reported roughly $5.0 billion revenue in 2024, where transparent claims handling supports modest premium differentials and strong reputation lowers pushback.

- Claims speed: key demand driver

- Negative reviews increase churn risk

- Transparency allows premium premiumization

- Reputation cuts buyer leverage

70%+ research insurance online; D2C sales and fast claims erode buyer bargaining power

Customers are price sensitive—small premium gaps drive selection and lapses in commoditized products, increasing buyer power. Over 70% of US shoppers researched insurance online in 2024, raising transparency and comparison pressure. Globe Life reported roughly $5.0 billion revenue in 2024; direct-to-consumer distribution and fast claims handling soften bargaining power.

| Metric | 2024 |

|---|---|

| Online research rate | Over 70% |

| Revenue | $5.0 billion |

Same Document Delivered

Globe Life Porter's Five Forces Analysis

This preview shows the complete Globe Life Porter's Five Forces Analysis and is the exact document you will receive immediately after purchase. It is fully formatted, professionally written, and ready for download and use—no samples, placeholders, or extra setup required. Instant access follows payment.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Globe Life’s Porter's Five Forces snapshot highlights concentrated buyer dynamics, moderate supplier leverage, low threat of substitutes for core life products, and regulatory-driven entry barriers. Competitive rivalry centers on price and distribution efficiency. This brief teases strategic implications and risk hotspots. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated reinsurers

Globe Life relies on a limited pool of highly rated reinsurers for risk transfer, and concentrated reinsurer markets can tighten terms, raise ceding costs, or restrict capacity during stressed markets. This concentration elevates supplier leverage over pricing and product design, though Globe Life reported a statutory surplus of about $3.9 billion at YE 2024, which and diversified treaties mitigate but do not eliminate that power.

Distribution partners as suppliers

Independent brokers and captive agencies supply most of Globe Life’s policy flow, with the company reporting roughly $6.0 billion in 2024 revenues that are heavily distribution-driven. High-performing agencies can and do secure higher commissions, enhanced marketing support, or exclusive products to protect share. Channel conflict risks force concessions to retain volume. Multi-channel distribution reduces any single partner’s leverage.

Data, tech, and underwriting tools

Third-party data vendors, the three major credit bureaus, and specialized underwriting platforms provide indispensable, highly specialized inputs for Globe Life, creating moderate supplier power. Vendor switching entails costly integrations, regulatory compliance updates, and model recalibration, producing price stickiness and partial lock-in. Growing vendor competition and expanding in-house analytics capabilities are reducing dependency over time.

Medical networks and TPA services

Supplemental health admin for Globe Life relies heavily on TPAs, networks, and claims processors; their quality and turnaround times (SLAs often target under 30 days) materially affect loss ratios and retention, giving specialized suppliers measurable bargaining leverage.

- TPA reliance: concentration risk

- SLAs: sub-30 day target

- Dual-sourcing reduces supplier power

Capital and rating agencies’ influence

- Rating influence: agencies set covenant/coverage benchmarks

- Market signal: 10y UST ~4.2% (2024)

- Credit squeeze: raises cost of new debt

- Mitigation: conservative capital and liquidity buffers

Insurer faces reinsurer power despite $3.9B surplus

Globe Life faces elevated supplier power from concentrated reinsurers despite a $3.9B statutory surplus (YE 2024), and distribution partners (2024 revenue ~$6.0B) can extract concessions to protect share. Data vendors, TPAs and rating agencies exert moderate leverage; SLA targets <30 days and 10y UST ~4.2% (2024) shape costs and capacity.

| Metric | 2024 |

|---|---|

| Statutory surplus | $3.9B |

| Revenue | $6.0B |

| 10y UST | ~4.2% |

| SLA target | <30 days |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Globe Life, with detailed assessment of supplier/buyer power, substitutes, new entrants, and industry rivalry to highlight disruptive threats, pricing pressure, and protective dynamics for strategy and investor use.

A clear, one-sheet summary of Globe Life's five forces for quick strategic decisions, ready to copy into pitch decks or boardroom slides. Includes an editable spider chart and no-complex-code layout so teams can customize pressure levels by market changes without needing finance experts.

Customers Bargaining Power

Price-sensitive target segment

Middle and lower-middle-income customers are highly price conscious, making small premium differences a common reason for policy selection and lapses in commoditized offerings like term life and final expense. This dynamic increases buyer power and compresses margins for Globe Life unless differentiated value is clearly communicated. Emphasizing guaranteed benefits, simplified underwriting, and agent-led explanations helps sustain retention and pricing power.

Low switching costs

Policies—especially simple life coverage—are easy to replace, and over 70% of US shoppers researched insurance online in 2024, increasing transparency via digital comparison tools. State replacement rules require disclosure but rarely block switches. Persistency programs and loyalty benefits help Globe Life curb churn and sustain renewal rates above industry averages.

Product simplicity and comparability

Simplified-issue life products are highly comparable across carriers, making price and rate tables easy for buyers to benchmark. Limited riders and similar benefit structures amplify price competition and enable purchasers to press for discounts, bundling, or upgraded underwriting classes. Where Globe Life differentiates through fast issue processes, distribution reach, and brand recognition, customer bargaining power is softened by perceived service value.

Direct response channel effects

Globe Life’s direct-response channel cuts intermediary commission drag and reduces broker comparison, lowering buyer power, but digital buyers in 2024 expect frictionless UX and fast underwriting decisions; poor UX raises abandonment and price sensitivity, impacting conversion and lifetime value.

Claims experience and trust

Claims experience and trust drive customer bargaining power for Globe Life: policyholders prioritize rapid, fair claims over product features, and negative reviews or delays sharply amplify skepticism and leverage; Globe Life reported roughly $5.0 billion revenue in 2024, where transparent claims handling supports modest premium differentials and strong reputation lowers pushback.

- Claims speed: key demand driver

- Negative reviews increase churn risk

- Transparency allows premium premiumization

- Reputation cuts buyer leverage

70%+ research insurance online; D2C sales and fast claims erode buyer bargaining power

Customers are price sensitive—small premium gaps drive selection and lapses in commoditized products, increasing buyer power. Over 70% of US shoppers researched insurance online in 2024, raising transparency and comparison pressure. Globe Life reported roughly $5.0 billion revenue in 2024; direct-to-consumer distribution and fast claims handling soften bargaining power.

| Metric | 2024 |

|---|---|

| Online research rate | Over 70% |

| Revenue | $5.0 billion |

Same Document Delivered

Globe Life Porter's Five Forces Analysis

This preview shows the complete Globe Life Porter's Five Forces Analysis and is the exact document you will receive immediately after purchase. It is fully formatted, professionally written, and ready for download and use—no samples, placeholders, or extra setup required. Instant access follows payment.