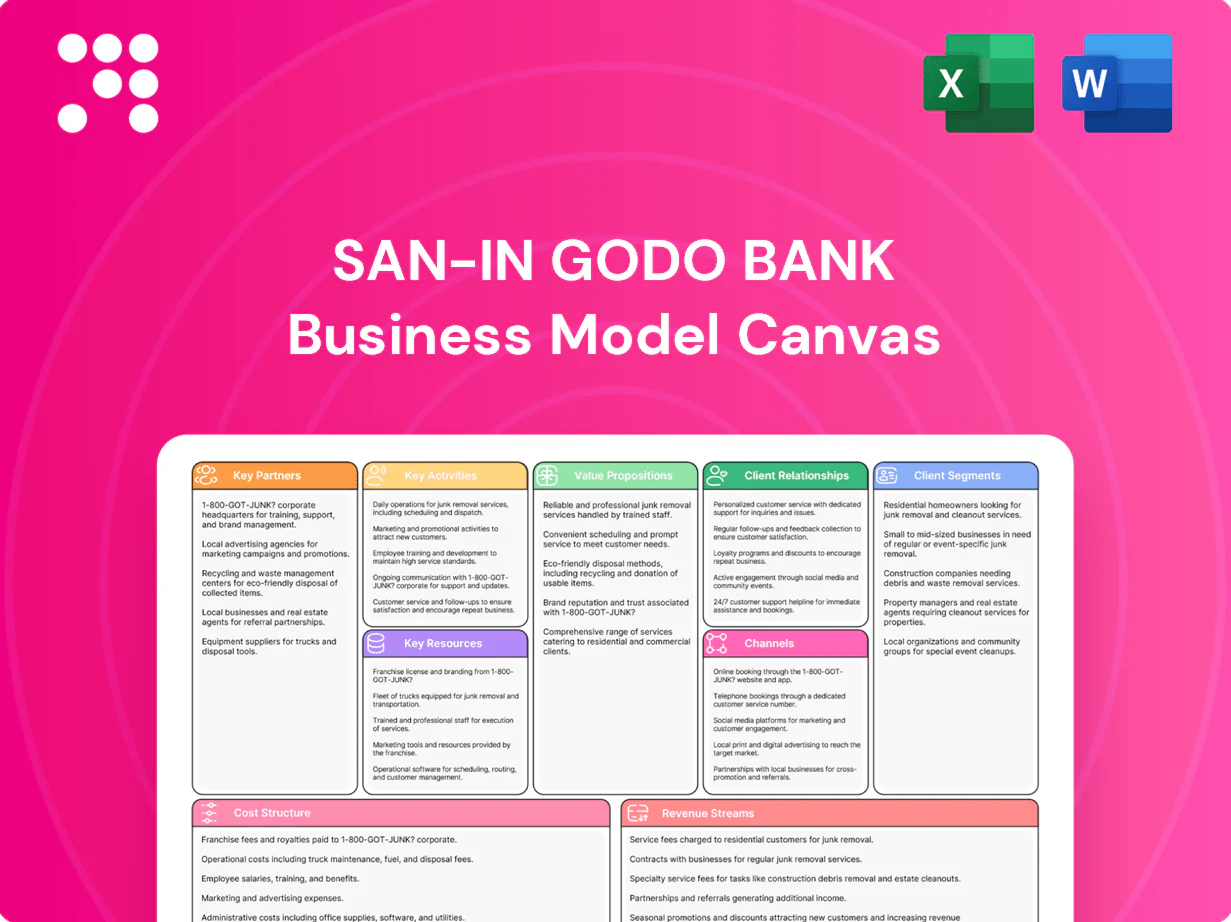

San-In Godo Bank Business Model Canvas

Unlock the strategic blueprint of a regional bank with our Business Model Canvas

Unlock the strategic blueprint behind San-In Godo Bank with our Business Model Canvas — a concise, actionable map of its value propositions, customer segments, revenue streams and key partnerships. Ideal for investors, consultants and strategists seeking practical insights. Download the full editable Canvas in Word and Excel to benchmark, plan or pitch with confidence.

Partnerships

Local businesses & SMEs

Collaborate with regional SMEs—which comprise about 90% of businesses and account for over 50% of employment globally (World Bank)—to deliver tailored lending and cash-management solutions. Co-create financing packages timed to local industry cycles and seasonal cash flows, using loan structures and working-capital lines to stabilize revenues. Leverage chambers of commerce to build reciprocal referral networks and deepen deposit and loan relationships within the community.

International correspondent banks

Partner with international correspondent banks to process remittances (global flows ~USD 650B in 2024) and trade finance, enabling FX, letters of credit and cross-border settlements. This expands reach for clients importing/exporting goods and addresses parts of the ~USD 1.5T trade finance gap (ICC 2024). Provide advisory on international risk, AML/CFT and regulatory compliance.

Asset managers & fund providers

San-In Godo Bank partners with asset managers and fund providers to distribute mutual funds and model portfolios, tapping into a global mutual fund market that exceeded $60 trillion in AUM by 2023 to broaden client access to equities, fixed income, and alternatives. These partnerships supply research and multi-asset solutions that enrich the bank’s retail and HNW offerings. They aim to grow fee-based income while expanding customer choice and maintaining strict product governance and suitability standards aligned with regulatory expectations.

Fintech and technology vendors

Partnering with fintech and technology vendors lets San-In Godo Bank integrate core banking, digital onboarding, and payment platforms, accelerating mobile app, biometrics, and analytics rollout and cutting time-to-market by up to 30% per 2024 industry benchmarks while preserving security and compliance via modern stacks.

- core-banking integration

- digital onboarding & payments

- mobile/biometrics/analytics

- 30% faster launch (2024)

- modern-secure, compliant stacks

Government & development agencies

San-In Godo Bank partners with municipal and national development agencies to drive regional revitalization projects, aligning lending with policy programs that support local growth and Japan’s regional policy priorities in 2024. The bank channels government-backed credit guarantees (commonly covering around 80% of SME loans) and subsidies to stimulate SME investment, support disaster recovery lending after floods and earthquakes, and fund sustainability projects tied to municipal plans.

- Regional revitalization alignment — policy-driven lending

- SME support — government credit guarantees ~80% coverage

- Disaster recovery — prioritized contingent credit lines

- Sustainability — co-finance municipal green projects

Leverage SME partnerships, correspondents, asset managers, fintech and govt guarantees

Leverage SME partnerships (SMEs ≈90% of firms, >50% employment; World Bank) for tailored lending and deposits. Use correspondent banks for remittances (~USD650B 2024) and trade finance (USD1.5T gap, ICC 2024). Distribute funds (global mutual fund AUM >USD60T 2023) and deploy fintech to cut launch time ~30% (2024); use govt guarantees (~80% SME loan coverage) for risk transfer.

| Partnership | KPI | 2024/2023 |

|---|---|---|

| SMEs | Market share/employment | ≈90% firms; >50% jobs |

| Correspondents | Remittances | ≈USD650B (2024) |

| Asset managers | AUM | >USD60T (2023) |

| Fintech | Time-to-market | -30% (2024) |

| Govt agencies | Guarantee coverage | ≈80% SME loans |

What is included in the product

A concise, pre-built Business Model Canvas for San-In Godo Bank outlining customer segments, channels, value propositions, revenue streams and cost structure across the nine BMC blocks; reflects real-world operations, competitive advantages and linked SWOT insights to support presentations, investor discussions and strategic decision-making.

High-level view of San-In Godo Bank’s business model with editable cells to quickly pinpoint customer segments, revenue drivers, and cost pressures, saving hours of structuring and enabling fast, shareable insights for strategy, boardrooms, or comparison across regional banks.

Activities

Deposit gathering

San-In Godo Bank focuses on attracting and retaining retail and corporate deposits by offering competitive rates, strong deposit protection and branch/online convenience; Japan’s household deposits exceeded ¥1,000 trillion in 2024 and average retail deposit rates remained near 0.001% in 2024. The bank optimizes its funding mix to lower cost of capital, prioritizing low-cost current/account deposits and targeted time deposits. Active asset-liability management monitors interest-rate sensitivity and liquidity to meet regulatory liquidity coverage and contingency funding needs.

Lending & credit underwriting

San-In Godo Bank provides housing, business and working-capital loans tailored to regional households and SMEs. Creditworthiness is assessed with prudent risk models and local market insights, updated as of 2024. Lending is priced to cover risk while promoting regional development and financial inclusion. Active portfolio monitoring and early-warning systems reduce defaults and preserve asset quality.

Investment & wealth services

Advise clients on mutual funds and savings plans, conducting suitability assessments and periodic reviews at least annually and upon material change. Educate clients on risk-return tradeoffs and portfolio diversification. Generate fee income through advisory and distribution, with typical retail advisory fees in Japan ranging about 0.5–1.5% annually (industry norm in 2024).

International banking

San-In Godo Bank facilitates FX, trade finance, and overseas remittances, supporting exporters/importers with documentation, letters of credit, and hedging to mitigate cross‑border risk. The bank provides market insights on currencies and key trade corridors and enforces AML and sanctions screening in all flows; ICC estimates a global trade finance gap of about US$1.7tn (2023) and global remittances ~US$702bn (2023).

- Services: FX, trade finance, remittances

- Support: documentation, LC, hedging

- Insight: currency and corridor research

- Compliance: AML, sanctions screening

Digital banking operations

Operate mobile and online platforms for everyday banking with 99.98% uptime and 24/7 availability; continuous UX improvements raised mobile NPS by ~12 points in 2024. Use analytics to personalize offers, lifting cross-sell by ~20% and reducing churn up to 15%. Streamline back-office workflows with RPA and API-led automation to cut processing costs ~30%.

- Uptime: 99.98%

- Mobile NPS +12 pts (2024)

- Cross-sell +20%, churn -15%

- Back-office cost -30% via automation

Attract Japanese deposits: optimize funding, ALM, mortgages, SME lending, digital +20% cross-sell

Focus on attracting/retaining retail and corporate deposits (Japan household deposits >¥1,000tn in 2024; retail deposit rates ~0.001% in 2024), optimizing funding mix and ALM for liquidity and capital cost. Provide regional mortgages, SME and working-capital lending with prudent credit models and portfolio monitoring. Deliver digital banking (99.98% uptime), advisory fees (0.5–1.5% typical), omnichannel sales (cross-sell +20%, mobile NPS +12).

| Metric | 2024 |

|---|---|

| Household deposits | ¥>1,000tn |

| Avg retail deposit rate | ~0.001% |

| Uptime | 99.98% |

| Mobile NPS | +12 pts |

| Cross-sell lift | +20% |

Full Version Awaits

Business Model Canvas

The San-In Godo Bank Business Model Canvas shown here is the actual deliverable, not a sample or mockup. It reflects the full structure, content, and layout you’ll receive after purchase. Upon ordering you’ll get this same document ready to download and edit. No surprises—what you preview is what you’ll own.

Unlock the strategic blueprint of a regional bank with our Business Model Canvas

Unlock the strategic blueprint behind San-In Godo Bank with our Business Model Canvas — a concise, actionable map of its value propositions, customer segments, revenue streams and key partnerships. Ideal for investors, consultants and strategists seeking practical insights. Download the full editable Canvas in Word and Excel to benchmark, plan or pitch with confidence.

Partnerships

Local businesses & SMEs

Collaborate with regional SMEs—which comprise about 90% of businesses and account for over 50% of employment globally (World Bank)—to deliver tailored lending and cash-management solutions. Co-create financing packages timed to local industry cycles and seasonal cash flows, using loan structures and working-capital lines to stabilize revenues. Leverage chambers of commerce to build reciprocal referral networks and deepen deposit and loan relationships within the community.

International correspondent banks

Partner with international correspondent banks to process remittances (global flows ~USD 650B in 2024) and trade finance, enabling FX, letters of credit and cross-border settlements. This expands reach for clients importing/exporting goods and addresses parts of the ~USD 1.5T trade finance gap (ICC 2024). Provide advisory on international risk, AML/CFT and regulatory compliance.

Asset managers & fund providers

San-In Godo Bank partners with asset managers and fund providers to distribute mutual funds and model portfolios, tapping into a global mutual fund market that exceeded $60 trillion in AUM by 2023 to broaden client access to equities, fixed income, and alternatives. These partnerships supply research and multi-asset solutions that enrich the bank’s retail and HNW offerings. They aim to grow fee-based income while expanding customer choice and maintaining strict product governance and suitability standards aligned with regulatory expectations.

Fintech and technology vendors

Partnering with fintech and technology vendors lets San-In Godo Bank integrate core banking, digital onboarding, and payment platforms, accelerating mobile app, biometrics, and analytics rollout and cutting time-to-market by up to 30% per 2024 industry benchmarks while preserving security and compliance via modern stacks.

- core-banking integration

- digital onboarding & payments

- mobile/biometrics/analytics

- 30% faster launch (2024)

- modern-secure, compliant stacks

Government & development agencies

San-In Godo Bank partners with municipal and national development agencies to drive regional revitalization projects, aligning lending with policy programs that support local growth and Japan’s regional policy priorities in 2024. The bank channels government-backed credit guarantees (commonly covering around 80% of SME loans) and subsidies to stimulate SME investment, support disaster recovery lending after floods and earthquakes, and fund sustainability projects tied to municipal plans.

- Regional revitalization alignment — policy-driven lending

- SME support — government credit guarantees ~80% coverage

- Disaster recovery — prioritized contingent credit lines

- Sustainability — co-finance municipal green projects

Leverage SME partnerships, correspondents, asset managers, fintech and govt guarantees

Leverage SME partnerships (SMEs ≈90% of firms, >50% employment; World Bank) for tailored lending and deposits. Use correspondent banks for remittances (~USD650B 2024) and trade finance (USD1.5T gap, ICC 2024). Distribute funds (global mutual fund AUM >USD60T 2023) and deploy fintech to cut launch time ~30% (2024); use govt guarantees (~80% SME loan coverage) for risk transfer.

| Partnership | KPI | 2024/2023 |

|---|---|---|

| SMEs | Market share/employment | ≈90% firms; >50% jobs |

| Correspondents | Remittances | ≈USD650B (2024) |

| Asset managers | AUM | >USD60T (2023) |

| Fintech | Time-to-market | -30% (2024) |

| Govt agencies | Guarantee coverage | ≈80% SME loans |

What is included in the product

A concise, pre-built Business Model Canvas for San-In Godo Bank outlining customer segments, channels, value propositions, revenue streams and cost structure across the nine BMC blocks; reflects real-world operations, competitive advantages and linked SWOT insights to support presentations, investor discussions and strategic decision-making.

High-level view of San-In Godo Bank’s business model with editable cells to quickly pinpoint customer segments, revenue drivers, and cost pressures, saving hours of structuring and enabling fast, shareable insights for strategy, boardrooms, or comparison across regional banks.

Activities

Deposit gathering

San-In Godo Bank focuses on attracting and retaining retail and corporate deposits by offering competitive rates, strong deposit protection and branch/online convenience; Japan’s household deposits exceeded ¥1,000 trillion in 2024 and average retail deposit rates remained near 0.001% in 2024. The bank optimizes its funding mix to lower cost of capital, prioritizing low-cost current/account deposits and targeted time deposits. Active asset-liability management monitors interest-rate sensitivity and liquidity to meet regulatory liquidity coverage and contingency funding needs.

Lending & credit underwriting

San-In Godo Bank provides housing, business and working-capital loans tailored to regional households and SMEs. Creditworthiness is assessed with prudent risk models and local market insights, updated as of 2024. Lending is priced to cover risk while promoting regional development and financial inclusion. Active portfolio monitoring and early-warning systems reduce defaults and preserve asset quality.

Investment & wealth services

Advise clients on mutual funds and savings plans, conducting suitability assessments and periodic reviews at least annually and upon material change. Educate clients on risk-return tradeoffs and portfolio diversification. Generate fee income through advisory and distribution, with typical retail advisory fees in Japan ranging about 0.5–1.5% annually (industry norm in 2024).

International banking

San-In Godo Bank facilitates FX, trade finance, and overseas remittances, supporting exporters/importers with documentation, letters of credit, and hedging to mitigate cross‑border risk. The bank provides market insights on currencies and key trade corridors and enforces AML and sanctions screening in all flows; ICC estimates a global trade finance gap of about US$1.7tn (2023) and global remittances ~US$702bn (2023).

- Services: FX, trade finance, remittances

- Support: documentation, LC, hedging

- Insight: currency and corridor research

- Compliance: AML, sanctions screening

Digital banking operations

Operate mobile and online platforms for everyday banking with 99.98% uptime and 24/7 availability; continuous UX improvements raised mobile NPS by ~12 points in 2024. Use analytics to personalize offers, lifting cross-sell by ~20% and reducing churn up to 15%. Streamline back-office workflows with RPA and API-led automation to cut processing costs ~30%.

- Uptime: 99.98%

- Mobile NPS +12 pts (2024)

- Cross-sell +20%, churn -15%

- Back-office cost -30% via automation

Attract Japanese deposits: optimize funding, ALM, mortgages, SME lending, digital +20% cross-sell

Focus on attracting/retaining retail and corporate deposits (Japan household deposits >¥1,000tn in 2024; retail deposit rates ~0.001% in 2024), optimizing funding mix and ALM for liquidity and capital cost. Provide regional mortgages, SME and working-capital lending with prudent credit models and portfolio monitoring. Deliver digital banking (99.98% uptime), advisory fees (0.5–1.5% typical), omnichannel sales (cross-sell +20%, mobile NPS +12).

| Metric | 2024 |

|---|---|

| Household deposits | ¥>1,000tn |

| Avg retail deposit rate | ~0.001% |

| Uptime | 99.98% |

| Mobile NPS | +12 pts |

| Cross-sell lift | +20% |

Full Version Awaits

Business Model Canvas

The San-In Godo Bank Business Model Canvas shown here is the actual deliverable, not a sample or mockup. It reflects the full structure, content, and layout you’ll receive after purchase. Upon ordering you’ll get this same document ready to download and edit. No surprises—what you preview is what you’ll own.

Original: $10.00

-65%$10.00

$3.50Description

Unlock the strategic blueprint of a regional bank with our Business Model Canvas

Unlock the strategic blueprint behind San-In Godo Bank with our Business Model Canvas — a concise, actionable map of its value propositions, customer segments, revenue streams and key partnerships. Ideal for investors, consultants and strategists seeking practical insights. Download the full editable Canvas in Word and Excel to benchmark, plan or pitch with confidence.

Partnerships

Local businesses & SMEs

Collaborate with regional SMEs—which comprise about 90% of businesses and account for over 50% of employment globally (World Bank)—to deliver tailored lending and cash-management solutions. Co-create financing packages timed to local industry cycles and seasonal cash flows, using loan structures and working-capital lines to stabilize revenues. Leverage chambers of commerce to build reciprocal referral networks and deepen deposit and loan relationships within the community.

International correspondent banks

Partner with international correspondent banks to process remittances (global flows ~USD 650B in 2024) and trade finance, enabling FX, letters of credit and cross-border settlements. This expands reach for clients importing/exporting goods and addresses parts of the ~USD 1.5T trade finance gap (ICC 2024). Provide advisory on international risk, AML/CFT and regulatory compliance.

Asset managers & fund providers

San-In Godo Bank partners with asset managers and fund providers to distribute mutual funds and model portfolios, tapping into a global mutual fund market that exceeded $60 trillion in AUM by 2023 to broaden client access to equities, fixed income, and alternatives. These partnerships supply research and multi-asset solutions that enrich the bank’s retail and HNW offerings. They aim to grow fee-based income while expanding customer choice and maintaining strict product governance and suitability standards aligned with regulatory expectations.

Fintech and technology vendors

Partnering with fintech and technology vendors lets San-In Godo Bank integrate core banking, digital onboarding, and payment platforms, accelerating mobile app, biometrics, and analytics rollout and cutting time-to-market by up to 30% per 2024 industry benchmarks while preserving security and compliance via modern stacks.

- core-banking integration

- digital onboarding & payments

- mobile/biometrics/analytics

- 30% faster launch (2024)

- modern-secure, compliant stacks

Government & development agencies

San-In Godo Bank partners with municipal and national development agencies to drive regional revitalization projects, aligning lending with policy programs that support local growth and Japan’s regional policy priorities in 2024. The bank channels government-backed credit guarantees (commonly covering around 80% of SME loans) and subsidies to stimulate SME investment, support disaster recovery lending after floods and earthquakes, and fund sustainability projects tied to municipal plans.

- Regional revitalization alignment — policy-driven lending

- SME support — government credit guarantees ~80% coverage

- Disaster recovery — prioritized contingent credit lines

- Sustainability — co-finance municipal green projects

Leverage SME partnerships, correspondents, asset managers, fintech and govt guarantees

Leverage SME partnerships (SMEs ≈90% of firms, >50% employment; World Bank) for tailored lending and deposits. Use correspondent banks for remittances (~USD650B 2024) and trade finance (USD1.5T gap, ICC 2024). Distribute funds (global mutual fund AUM >USD60T 2023) and deploy fintech to cut launch time ~30% (2024); use govt guarantees (~80% SME loan coverage) for risk transfer.

| Partnership | KPI | 2024/2023 |

|---|---|---|

| SMEs | Market share/employment | ≈90% firms; >50% jobs |

| Correspondents | Remittances | ≈USD650B (2024) |

| Asset managers | AUM | >USD60T (2023) |

| Fintech | Time-to-market | -30% (2024) |

| Govt agencies | Guarantee coverage | ≈80% SME loans |

What is included in the product

A concise, pre-built Business Model Canvas for San-In Godo Bank outlining customer segments, channels, value propositions, revenue streams and cost structure across the nine BMC blocks; reflects real-world operations, competitive advantages and linked SWOT insights to support presentations, investor discussions and strategic decision-making.

High-level view of San-In Godo Bank’s business model with editable cells to quickly pinpoint customer segments, revenue drivers, and cost pressures, saving hours of structuring and enabling fast, shareable insights for strategy, boardrooms, or comparison across regional banks.

Activities

Deposit gathering

San-In Godo Bank focuses on attracting and retaining retail and corporate deposits by offering competitive rates, strong deposit protection and branch/online convenience; Japan’s household deposits exceeded ¥1,000 trillion in 2024 and average retail deposit rates remained near 0.001% in 2024. The bank optimizes its funding mix to lower cost of capital, prioritizing low-cost current/account deposits and targeted time deposits. Active asset-liability management monitors interest-rate sensitivity and liquidity to meet regulatory liquidity coverage and contingency funding needs.

Lending & credit underwriting

San-In Godo Bank provides housing, business and working-capital loans tailored to regional households and SMEs. Creditworthiness is assessed with prudent risk models and local market insights, updated as of 2024. Lending is priced to cover risk while promoting regional development and financial inclusion. Active portfolio monitoring and early-warning systems reduce defaults and preserve asset quality.

Investment & wealth services

Advise clients on mutual funds and savings plans, conducting suitability assessments and periodic reviews at least annually and upon material change. Educate clients on risk-return tradeoffs and portfolio diversification. Generate fee income through advisory and distribution, with typical retail advisory fees in Japan ranging about 0.5–1.5% annually (industry norm in 2024).

International banking

San-In Godo Bank facilitates FX, trade finance, and overseas remittances, supporting exporters/importers with documentation, letters of credit, and hedging to mitigate cross‑border risk. The bank provides market insights on currencies and key trade corridors and enforces AML and sanctions screening in all flows; ICC estimates a global trade finance gap of about US$1.7tn (2023) and global remittances ~US$702bn (2023).

- Services: FX, trade finance, remittances

- Support: documentation, LC, hedging

- Insight: currency and corridor research

- Compliance: AML, sanctions screening

Digital banking operations

Operate mobile and online platforms for everyday banking with 99.98% uptime and 24/7 availability; continuous UX improvements raised mobile NPS by ~12 points in 2024. Use analytics to personalize offers, lifting cross-sell by ~20% and reducing churn up to 15%. Streamline back-office workflows with RPA and API-led automation to cut processing costs ~30%.

- Uptime: 99.98%

- Mobile NPS +12 pts (2024)

- Cross-sell +20%, churn -15%

- Back-office cost -30% via automation

Attract Japanese deposits: optimize funding, ALM, mortgages, SME lending, digital +20% cross-sell

Focus on attracting/retaining retail and corporate deposits (Japan household deposits >¥1,000tn in 2024; retail deposit rates ~0.001% in 2024), optimizing funding mix and ALM for liquidity and capital cost. Provide regional mortgages, SME and working-capital lending with prudent credit models and portfolio monitoring. Deliver digital banking (99.98% uptime), advisory fees (0.5–1.5% typical), omnichannel sales (cross-sell +20%, mobile NPS +12).

| Metric | 2024 |

|---|---|

| Household deposits | ¥>1,000tn |

| Avg retail deposit rate | ~0.001% |

| Uptime | 99.98% |

| Mobile NPS | +12 pts |

| Cross-sell lift | +20% |

Full Version Awaits

Business Model Canvas

The San-In Godo Bank Business Model Canvas shown here is the actual deliverable, not a sample or mockup. It reflects the full structure, content, and layout you’ll receive after purchase. Upon ordering you’ll get this same document ready to download and edit. No surprises—what you preview is what you’ll own.