goeasy Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

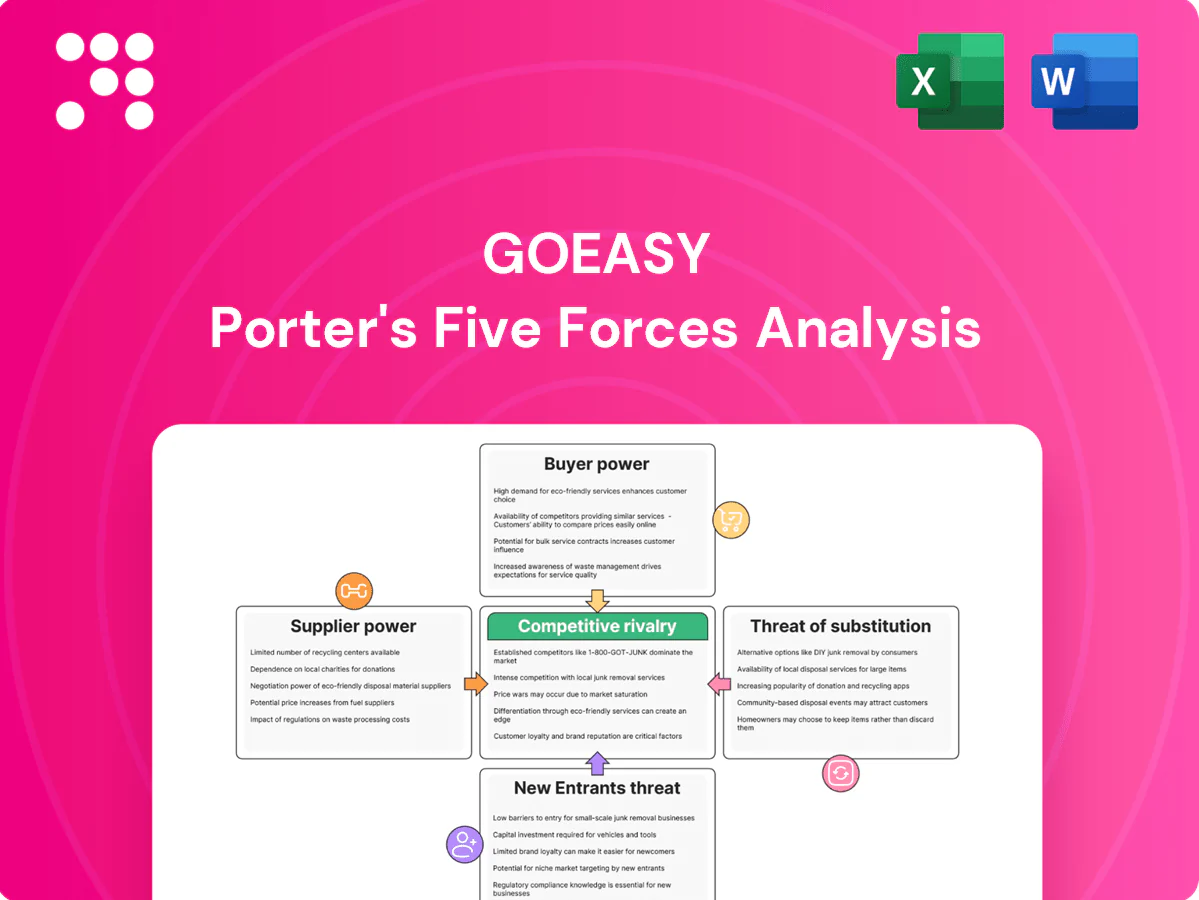

This concise Porter's Five Forces snapshot highlights goeasy's competitive pressures—buyer and supplier power, threat of new entrants, substitutes, and rivalry—and how they shape margins and growth. The full report unpacks force-by-force ratings, data visuals and strategic implications. Unlock the complete analysis to inform investment and strategy decisions.

Suppliers Bargaining Power

Concentration of funding sources

goeasy funds loan growth via bank credit lines, securitizations and capital markets; its managed receivables totaled about CAD 2.1 billion in 2024, making funding counterparties strategically important. A concentrated lender/investor base can force wider spreads, tighter covenants and higher haircuts, squeezing net yield. Diversifying maturities and counterparties mitigates pricing risk but raises liquidity and transaction costs to maintain.

Interest rate sensitivity

Rising benchmark rates—Bank of Canada policy rate at 5.00% in 2024—directly lift goeasy’s funding costs and can compress net interest margins when consumer loan repricing lags. Capital suppliers (term lenders, securitization buyers) gain leverage during tight cycles, increasing covenant pressure and cost of incremental funding. Hedging can blunt rate volatility but introduces hedging costs, operational complexity and counterparty exposure.

Critical data and tech vendors

Credit bureaus and scoring/decisioning platforms (Equifax and TransUnion provide over 90% of Canadian consumer credit data) are essential inputs with few substitutes. Vendor switching is risky—model recalibration, validation and regulatory compliance can take 3–6 months and disrupt underwriting performance. This dependency grants niche suppliers moderate bargaining power.

Leased goods supply chain

easyhome relies on furniture, appliance and electronics distributors for leased inventory, giving large manufacturers intermittent pricing and availability leverage during supply shocks such as the 2023–24 component and shipping disruptions.

Multi-sourcing across regional distributors and flexible SKU substitution reduced procurement risk and helped maintain same‑store inventory fill rates in 2024.

These measures limit supplier bargaining power but do not eliminate exposure to concentrated OEM pricing moves and seasonal capacity constraints.

- Supplier concentration: mitigated by multi-sourcing

- Supply shocks: 2023–24 component/shipping disruptions increased OEM leverage

- SKU flexibility: reduces stockouts and pricing pressure

Specialized talent as a supplier

Underwriters, data scientists and collections specialists are scarce in non-prime lending; a 2024 industry survey found 62% of firms report critical talent shortages. Tight 2024 labor markets pushed salary premiums roughly 15–25% above comparable prime-lending roles, elevating recruitment and retention costs. Building in-house training lowers dependency but typically takes 9–18 months to produce productive hires.

Moderate supplier power: CAD 2.1bn receivables, BoC 5.00%, credit data >90%

goeasy faces moderate supplier power: CAD 2.1bn managed receivables make funding counterparties critical. Bank of Canada rate at 5.00% (2024) raises funding costs and covenant leverage. Credit data concentrated (>90% Equifax/TransUnion) and OEM/distributor shocks (2023–24) add pressure. Talent shortages (62%) and 15–25% salary premiums increase operating supplier dependence.

| Metric | Value (2024) |

|---|---|

| Managed receivables | CAD 2.1bn |

| BoC policy rate | 5.00% |

| Credit data share | >90% |

| Talent shortage | 62% |

| Salary premium | 15–25% |

| Upskill time | 9–18 months |

What is included in the product

Uncovers competitive drivers, buyer and supplier power, threat of substitutes, and entry barriers specific to goeasy, highlighting disruptive risks and strategic levers to protect margins and market share.

One-sheet Porter’s Five Forces for goeasy that instantly visualizes competitive pressure via a spider chart and lets you customize scores and labels to reflect changing market conditions. Clean, no-macro layout ready to drop into pitch decks or integrate with wider reports.

Customers Bargaining Power

Limited alternatives for non-prime borrowers

Non-prime borrowers often face limited bank options, reducing direct price bargaining; goeasy’s niche focus on subprime segments served roughly 200,000 customers in 2024, reinforcing captive demand. Yet these customers are payment-sensitive and will switch for lower weekly or biweekly costs, making short-term price elasticity high. Growth of online comparison and transparency tools in 2024 modestly increased buyer power.

Channel partners in POS financing

Channel partners in goeasy POS financing can steer approval flows, take rates and promotional terms; in 2024 goeasy worked with over 1,000 merchant partners, letting high-volume partners negotiate lower take rates or exclusivity. Top partners concentrate volume, so losing a single key merchant materially raises customer-acquisition costs and strengthens buyer leverage. Retailer bargaining power thus compresses unit economics and margins.

Switching ease across digital lenders

Competing digital lenders enable instant rate comparisons and soft pre-approvals, increasing customer mobility and making goeasy vulnerable to rapid switching; in fiscal 2024 goeasy reported CAD 1.03 billion revenue, highlighting scale but also exposure to digital churn. Minimal physical switching costs amplify elasticity to rate and fee changes, pressuring margins. Loyalty hinges on speed, approval certainty and superior UX to retain customers.

Regulatory and reputational scrutiny

Regulatory consumer-protection rules in Canada empower goeasy borrowers to contest fees and practices, increasing bargaining leverage and complaint risk; as of 2024 goeasy serves roughly 200,000 customers, magnifying reputational exposure. Negative publicity can drive churn and regulatory probes, boosting buyer clout. Clear disclosures and hardship programs reduce disputes and restore trust.

- Regulatory recourse: empowered borrowers

- Reputation risk: churn amplifies clout

- Mitigation: disclosures & hardship programs

Cross-sell and relationship depth

Deeper relationships from repeat loans and ancillary services reduce price sensitivity as customers value convenience and account continuity.

Non-prime borrowers still prioritize affordability and flexible payment terms over product breadth, limiting upsell pricing power.

- Retention via structured renewals must balance customer lifetime value with fair pricing and regulatory compliance

- Cross-sell increases switching costs but cannot override core affordability needs

- Relationship depth moderates but does not eliminate customer bargaining power

High switching risk for ~200,000 price-sensitive customers; CAD 1.03B at stake

Customers (~200,000 in 2024) have limited bank options but high price sensitivity; short-term elasticity is high and digital competitors raise switching risk. goeasy's CAD 1.03B 2024 revenue and 1,000+ merchant partners concentrate bargaining power; regulatory recourse amplifies buyer leverage.

| Metric | 2024 |

|---|---|

| Customers | ~200,000 |

| Revenue | CAD 1.03B |

| Merchant partners | 1,000+ |

Same Document Delivered

goeasy Porter's Five Forces Analysis

This goeasy Porter's Five Forces analysis evaluates competitive rivalry, buyer and supplier power, threats of substitutes, and barriers to entry to clarify the company's strategic position and risk exposure. It highlights key industry dynamics, regulatory influences, and implications for profitability and growth. You're looking at the actual document. Once you complete your purchase, you’ll get instant access to this exact file.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

This concise Porter's Five Forces snapshot highlights goeasy's competitive pressures—buyer and supplier power, threat of new entrants, substitutes, and rivalry—and how they shape margins and growth. The full report unpacks force-by-force ratings, data visuals and strategic implications. Unlock the complete analysis to inform investment and strategy decisions.

Suppliers Bargaining Power

Concentration of funding sources

goeasy funds loan growth via bank credit lines, securitizations and capital markets; its managed receivables totaled about CAD 2.1 billion in 2024, making funding counterparties strategically important. A concentrated lender/investor base can force wider spreads, tighter covenants and higher haircuts, squeezing net yield. Diversifying maturities and counterparties mitigates pricing risk but raises liquidity and transaction costs to maintain.

Interest rate sensitivity

Rising benchmark rates—Bank of Canada policy rate at 5.00% in 2024—directly lift goeasy’s funding costs and can compress net interest margins when consumer loan repricing lags. Capital suppliers (term lenders, securitization buyers) gain leverage during tight cycles, increasing covenant pressure and cost of incremental funding. Hedging can blunt rate volatility but introduces hedging costs, operational complexity and counterparty exposure.

Critical data and tech vendors

Credit bureaus and scoring/decisioning platforms (Equifax and TransUnion provide over 90% of Canadian consumer credit data) are essential inputs with few substitutes. Vendor switching is risky—model recalibration, validation and regulatory compliance can take 3–6 months and disrupt underwriting performance. This dependency grants niche suppliers moderate bargaining power.

Leased goods supply chain

easyhome relies on furniture, appliance and electronics distributors for leased inventory, giving large manufacturers intermittent pricing and availability leverage during supply shocks such as the 2023–24 component and shipping disruptions.

Multi-sourcing across regional distributors and flexible SKU substitution reduced procurement risk and helped maintain same‑store inventory fill rates in 2024.

These measures limit supplier bargaining power but do not eliminate exposure to concentrated OEM pricing moves and seasonal capacity constraints.

- Supplier concentration: mitigated by multi-sourcing

- Supply shocks: 2023–24 component/shipping disruptions increased OEM leverage

- SKU flexibility: reduces stockouts and pricing pressure

Specialized talent as a supplier

Underwriters, data scientists and collections specialists are scarce in non-prime lending; a 2024 industry survey found 62% of firms report critical talent shortages. Tight 2024 labor markets pushed salary premiums roughly 15–25% above comparable prime-lending roles, elevating recruitment and retention costs. Building in-house training lowers dependency but typically takes 9–18 months to produce productive hires.

Moderate supplier power: CAD 2.1bn receivables, BoC 5.00%, credit data >90%

goeasy faces moderate supplier power: CAD 2.1bn managed receivables make funding counterparties critical. Bank of Canada rate at 5.00% (2024) raises funding costs and covenant leverage. Credit data concentrated (>90% Equifax/TransUnion) and OEM/distributor shocks (2023–24) add pressure. Talent shortages (62%) and 15–25% salary premiums increase operating supplier dependence.

| Metric | Value (2024) |

|---|---|

| Managed receivables | CAD 2.1bn |

| BoC policy rate | 5.00% |

| Credit data share | >90% |

| Talent shortage | 62% |

| Salary premium | 15–25% |

| Upskill time | 9–18 months |

What is included in the product

Uncovers competitive drivers, buyer and supplier power, threat of substitutes, and entry barriers specific to goeasy, highlighting disruptive risks and strategic levers to protect margins and market share.

One-sheet Porter’s Five Forces for goeasy that instantly visualizes competitive pressure via a spider chart and lets you customize scores and labels to reflect changing market conditions. Clean, no-macro layout ready to drop into pitch decks or integrate with wider reports.

Customers Bargaining Power

Limited alternatives for non-prime borrowers

Non-prime borrowers often face limited bank options, reducing direct price bargaining; goeasy’s niche focus on subprime segments served roughly 200,000 customers in 2024, reinforcing captive demand. Yet these customers are payment-sensitive and will switch for lower weekly or biweekly costs, making short-term price elasticity high. Growth of online comparison and transparency tools in 2024 modestly increased buyer power.

Channel partners in POS financing

Channel partners in goeasy POS financing can steer approval flows, take rates and promotional terms; in 2024 goeasy worked with over 1,000 merchant partners, letting high-volume partners negotiate lower take rates or exclusivity. Top partners concentrate volume, so losing a single key merchant materially raises customer-acquisition costs and strengthens buyer leverage. Retailer bargaining power thus compresses unit economics and margins.

Switching ease across digital lenders

Competing digital lenders enable instant rate comparisons and soft pre-approvals, increasing customer mobility and making goeasy vulnerable to rapid switching; in fiscal 2024 goeasy reported CAD 1.03 billion revenue, highlighting scale but also exposure to digital churn. Minimal physical switching costs amplify elasticity to rate and fee changes, pressuring margins. Loyalty hinges on speed, approval certainty and superior UX to retain customers.

Regulatory and reputational scrutiny

Regulatory consumer-protection rules in Canada empower goeasy borrowers to contest fees and practices, increasing bargaining leverage and complaint risk; as of 2024 goeasy serves roughly 200,000 customers, magnifying reputational exposure. Negative publicity can drive churn and regulatory probes, boosting buyer clout. Clear disclosures and hardship programs reduce disputes and restore trust.

- Regulatory recourse: empowered borrowers

- Reputation risk: churn amplifies clout

- Mitigation: disclosures & hardship programs

Cross-sell and relationship depth

Deeper relationships from repeat loans and ancillary services reduce price sensitivity as customers value convenience and account continuity.

Non-prime borrowers still prioritize affordability and flexible payment terms over product breadth, limiting upsell pricing power.

- Retention via structured renewals must balance customer lifetime value with fair pricing and regulatory compliance

- Cross-sell increases switching costs but cannot override core affordability needs

- Relationship depth moderates but does not eliminate customer bargaining power

High switching risk for ~200,000 price-sensitive customers; CAD 1.03B at stake

Customers (~200,000 in 2024) have limited bank options but high price sensitivity; short-term elasticity is high and digital competitors raise switching risk. goeasy's CAD 1.03B 2024 revenue and 1,000+ merchant partners concentrate bargaining power; regulatory recourse amplifies buyer leverage.

| Metric | 2024 |

|---|---|

| Customers | ~200,000 |

| Revenue | CAD 1.03B |

| Merchant partners | 1,000+ |

Same Document Delivered

goeasy Porter's Five Forces Analysis

This goeasy Porter's Five Forces analysis evaluates competitive rivalry, buyer and supplier power, threats of substitutes, and barriers to entry to clarify the company's strategic position and risk exposure. It highlights key industry dynamics, regulatory influences, and implications for profitability and growth. You're looking at the actual document. Once you complete your purchase, you’ll get instant access to this exact file.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

This concise Porter's Five Forces snapshot highlights goeasy's competitive pressures—buyer and supplier power, threat of new entrants, substitutes, and rivalry—and how they shape margins and growth. The full report unpacks force-by-force ratings, data visuals and strategic implications. Unlock the complete analysis to inform investment and strategy decisions.

Suppliers Bargaining Power

Concentration of funding sources

goeasy funds loan growth via bank credit lines, securitizations and capital markets; its managed receivables totaled about CAD 2.1 billion in 2024, making funding counterparties strategically important. A concentrated lender/investor base can force wider spreads, tighter covenants and higher haircuts, squeezing net yield. Diversifying maturities and counterparties mitigates pricing risk but raises liquidity and transaction costs to maintain.

Interest rate sensitivity

Rising benchmark rates—Bank of Canada policy rate at 5.00% in 2024—directly lift goeasy’s funding costs and can compress net interest margins when consumer loan repricing lags. Capital suppliers (term lenders, securitization buyers) gain leverage during tight cycles, increasing covenant pressure and cost of incremental funding. Hedging can blunt rate volatility but introduces hedging costs, operational complexity and counterparty exposure.

Critical data and tech vendors

Credit bureaus and scoring/decisioning platforms (Equifax and TransUnion provide over 90% of Canadian consumer credit data) are essential inputs with few substitutes. Vendor switching is risky—model recalibration, validation and regulatory compliance can take 3–6 months and disrupt underwriting performance. This dependency grants niche suppliers moderate bargaining power.

Leased goods supply chain

easyhome relies on furniture, appliance and electronics distributors for leased inventory, giving large manufacturers intermittent pricing and availability leverage during supply shocks such as the 2023–24 component and shipping disruptions.

Multi-sourcing across regional distributors and flexible SKU substitution reduced procurement risk and helped maintain same‑store inventory fill rates in 2024.

These measures limit supplier bargaining power but do not eliminate exposure to concentrated OEM pricing moves and seasonal capacity constraints.

- Supplier concentration: mitigated by multi-sourcing

- Supply shocks: 2023–24 component/shipping disruptions increased OEM leverage

- SKU flexibility: reduces stockouts and pricing pressure

Specialized talent as a supplier

Underwriters, data scientists and collections specialists are scarce in non-prime lending; a 2024 industry survey found 62% of firms report critical talent shortages. Tight 2024 labor markets pushed salary premiums roughly 15–25% above comparable prime-lending roles, elevating recruitment and retention costs. Building in-house training lowers dependency but typically takes 9–18 months to produce productive hires.

Moderate supplier power: CAD 2.1bn receivables, BoC 5.00%, credit data >90%

goeasy faces moderate supplier power: CAD 2.1bn managed receivables make funding counterparties critical. Bank of Canada rate at 5.00% (2024) raises funding costs and covenant leverage. Credit data concentrated (>90% Equifax/TransUnion) and OEM/distributor shocks (2023–24) add pressure. Talent shortages (62%) and 15–25% salary premiums increase operating supplier dependence.

| Metric | Value (2024) |

|---|---|

| Managed receivables | CAD 2.1bn |

| BoC policy rate | 5.00% |

| Credit data share | >90% |

| Talent shortage | 62% |

| Salary premium | 15–25% |

| Upskill time | 9–18 months |

What is included in the product

Uncovers competitive drivers, buyer and supplier power, threat of substitutes, and entry barriers specific to goeasy, highlighting disruptive risks and strategic levers to protect margins and market share.

One-sheet Porter’s Five Forces for goeasy that instantly visualizes competitive pressure via a spider chart and lets you customize scores and labels to reflect changing market conditions. Clean, no-macro layout ready to drop into pitch decks or integrate with wider reports.

Customers Bargaining Power

Limited alternatives for non-prime borrowers

Non-prime borrowers often face limited bank options, reducing direct price bargaining; goeasy’s niche focus on subprime segments served roughly 200,000 customers in 2024, reinforcing captive demand. Yet these customers are payment-sensitive and will switch for lower weekly or biweekly costs, making short-term price elasticity high. Growth of online comparison and transparency tools in 2024 modestly increased buyer power.

Channel partners in POS financing

Channel partners in goeasy POS financing can steer approval flows, take rates and promotional terms; in 2024 goeasy worked with over 1,000 merchant partners, letting high-volume partners negotiate lower take rates or exclusivity. Top partners concentrate volume, so losing a single key merchant materially raises customer-acquisition costs and strengthens buyer leverage. Retailer bargaining power thus compresses unit economics and margins.

Switching ease across digital lenders

Competing digital lenders enable instant rate comparisons and soft pre-approvals, increasing customer mobility and making goeasy vulnerable to rapid switching; in fiscal 2024 goeasy reported CAD 1.03 billion revenue, highlighting scale but also exposure to digital churn. Minimal physical switching costs amplify elasticity to rate and fee changes, pressuring margins. Loyalty hinges on speed, approval certainty and superior UX to retain customers.

Regulatory and reputational scrutiny

Regulatory consumer-protection rules in Canada empower goeasy borrowers to contest fees and practices, increasing bargaining leverage and complaint risk; as of 2024 goeasy serves roughly 200,000 customers, magnifying reputational exposure. Negative publicity can drive churn and regulatory probes, boosting buyer clout. Clear disclosures and hardship programs reduce disputes and restore trust.

- Regulatory recourse: empowered borrowers

- Reputation risk: churn amplifies clout

- Mitigation: disclosures & hardship programs

Cross-sell and relationship depth

Deeper relationships from repeat loans and ancillary services reduce price sensitivity as customers value convenience and account continuity.

Non-prime borrowers still prioritize affordability and flexible payment terms over product breadth, limiting upsell pricing power.

- Retention via structured renewals must balance customer lifetime value with fair pricing and regulatory compliance

- Cross-sell increases switching costs but cannot override core affordability needs

- Relationship depth moderates but does not eliminate customer bargaining power

High switching risk for ~200,000 price-sensitive customers; CAD 1.03B at stake

Customers (~200,000 in 2024) have limited bank options but high price sensitivity; short-term elasticity is high and digital competitors raise switching risk. goeasy's CAD 1.03B 2024 revenue and 1,000+ merchant partners concentrate bargaining power; regulatory recourse amplifies buyer leverage.

| Metric | 2024 |

|---|---|

| Customers | ~200,000 |

| Revenue | CAD 1.03B |

| Merchant partners | 1,000+ |

Same Document Delivered

goeasy Porter's Five Forces Analysis

This goeasy Porter's Five Forces analysis evaluates competitive rivalry, buyer and supplier power, threats of substitutes, and barriers to entry to clarify the company's strategic position and risk exposure. It highlights key industry dynamics, regulatory influences, and implications for profitability and growth. You're looking at the actual document. Once you complete your purchase, you’ll get instant access to this exact file.