Gokaldas PESTLE Analysis

Your Shortcut to Market Insight Starts Here

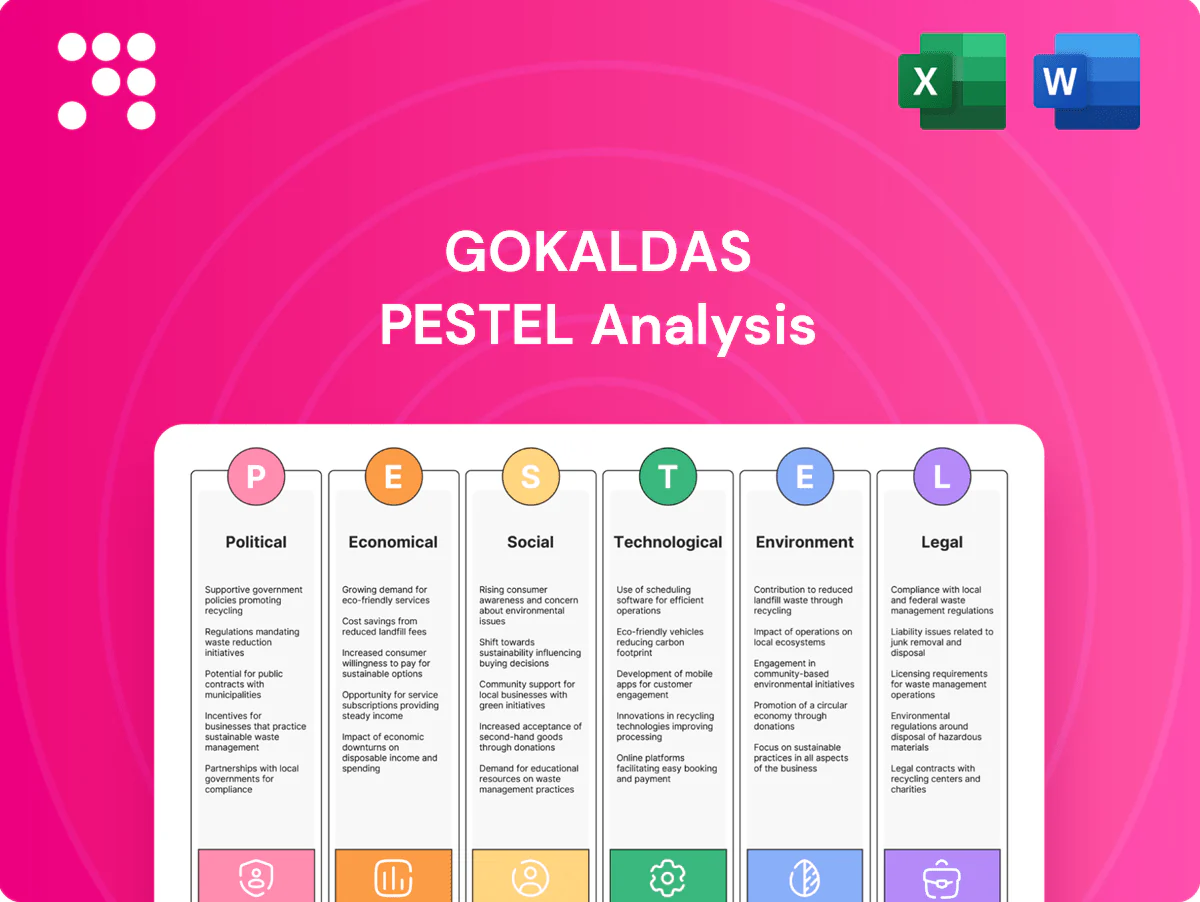

Our PESTLE analysis of Gokaldas reveals how political shifts, economic cycles, social trends, technological advances, legal changes and environmental pressures shape its prospects. Use these insights to anticipate risks and spot growth levers. Download the full, ready-to-use report now for actionable intelligence.

Political factors

Export-trade policy volatility

India’s export incentives, tariffs and FTAs—including the Rs 10,683 crore PLI textile scheme—directly shape apparel margins; India's apparel exports were about $18 billion in FY2023‑24, with EU/US/UK taking over 60% of volumes. Shifts in RoDTEP or duty‑drawback rates can materially change pricing power and margins, so monitoring EU/UK/US trade rules and origin criteria is critical. Proactive advocacy and diversified markets reduce policy shock risk.

Geopolitical tensions and logistics

Global flashpoints and Red Sea/Suez disruptions pushed container freight rates up over 30% and added 10–14 days to transit in 2023–24, raising costs and lead times for exporters. Sanctions and supplier shifts from China, Vietnam and Bangladesh have helped India capture re-routed demand, with apparel exports rising ~15% in 2024. Gokaldas must preserve multi-route logistics and near-shore options, hedging capacity and buffering delivery windows to protect service levels.

Labor and industrial relations

State-level implementation of the Code on Wages (2019) and divergent minimum wages across states materially affect Gokaldas’s unit labour costs and productivity; labour can account for a quarter to a third of factory operating costs in Indian apparel manufacturing. Stable industrial relations lower strike risk and allow flexible OT in peak seasons, while government skilling drives such as PMKVY expand skilled workforce and engagement with local authorities smooths plant operations.

Infrastructure and manufacturing policy

- PLI outlay: Rs 10,683 crore

- PM MITRA parks: 7 mega parks

- 2024–25 infra capex: Rs 11.1 lakh crore

- Key risks: power, port capacity, container shortages

- Benefit: supportive states = incentives + faster clearances

ESG-driven procurement norms

- EU CSRD ~50,000 companies covered

- Germany LkSG thresholds: >3,000 (2023) → >1,000 (2024)

- Due diligence laws drive more audits and supplier scrutiny

- Compliance readiness = higher probability of strategic contracts

PLI Rs 10,683 crore, apparel exports $18bn; freight +30%, volumes +15%

India PLI Rs 10,683 crore and apparel exports ~$18bn (FY2023‑24) drive margins; RoDTEP/duty‑drawback shifts can materially affect pricing. Red Sea/Suez shocks pushed freight >30% and exports re‑routing lifted India apparel volumes ~15% in 2024, so logistics resilience is critical. EU CSRD (~50,000 firms) and Germany LkSG (>1,000) raise ESG due diligence; documented compliance secures strategic buyers.

| Metric | Value |

|---|---|

| PLI outlay | Rs 10,683 crore |

| Apparel exports FY2023‑24 | $18bn |

| Freight rise (2023–24) | +30%+ |

| Export volume shift 2024 | ~+15% |

| EU CSRD | ~50,000 firms |

| Germany LkSG threshold 2024 | >1,000 employees |

What is included in the product

Provides a data-backed PESTLE assessment of Gokaldas across Political, Economic, Social, Technological, Environmental, and Legal dimensions, highlighting region- and industry-specific risks and opportunities with forward-looking insights to support executives, investors, and strategists in scenario planning and decision-making.

A concise, visually segmented Gokaldas PESTLE summary that relieves meeting prep pain by condensing external risk and market positioning into an easily shareable, editable format ideal for presentations, planning sessions, and quick team alignment.

Economic factors

Currency and hedging exposure

INR volatility versus USD/EUR materially affects Gokaldas export realizations and input costs; INR traded around 82–83 per USD in 2024 with several 3–6% intra‑year swings that pressured margins.

Effective hedging policies—using forwards and options—have been shown to cut FX P&L volatility by mid‑single digits, helping stabilize margins amid swings.

A weak INR improves price competitiveness for garments but raises imported machinery and input costs; a balanced currency book and natural hedges (local sourcing, USD receipts) are essential.

Global demand cycles

US/EU consumer spending drives Gokaldas order volumes and mix; the global apparel market was about 1.7 trillion USD in 2024, so shifts in Western demand materially impact exports. Recessions push sales toward value/basic categories while recoveries lift fashion and athleisure, changing price points and margins. Retail inventory corrections in 2023–24 caused short-term order deferrals, making agile capacity and category diversification key to smoothing revenues.

Raw material price fluctuations

Cotton, MMF, dyes and trims face cyclical and weather-driven swings that pressure costs; cotton made ~24% of global fiber production in 2023–24 while MMF accounted for roughly 60%, amplifying exposure to fibre-price moves. Input price spikes compress apparel margins when pass-through clauses are absent. Strategic sourcing and tighter inventory planning lower volatility. Blended fabrics and supplier diversification increase resilience.

Wage inflation and productivity

Rising statutory wages in India and export markets force Gokaldas to offset higher labor costs with productivity gains; industrial engineering, line balancing and targeted automation protect unit economics. Incentive-linked pay and attendance bonuses measurably lift throughput and retention. Continuous improvement programs (Kaizen, TPM) sustain cost competitiveness and margin resilience.

- IE methods: unit-cost focus

- Line balancing: reduce WIP

- Automation: lower touch labor

- Incentives: higher OEE and retention

Cost of capital and capex

Rising interest rates raise funding costs for Gokaldas’ capacity expansion and automation; RBI repo rate stood at 6.50% (June 2024), increasing loan pricing and payback thresholds. Efficient working-capital management reduces reliance on short-term debt during seasonal peaks, lowering financing strain. Targeted capex in high-ROI automation shortens payback even as rates stay elevated. Access to export credit lines (ECGC, EXIM Bank) underpins export-led growth.

- Interest rate backdrop: RBI repo 6.50% (Jun 2024)

- Working capital: reduces seasonal short-term borrowing

- Capex focus: high-ROI automation improves payback

- Financing support: ECGC/EXIM export credit lines

PLI Rs 10,683 crore, apparel exports $18bn; freight +30%, volumes +15%

INR ~82–83 per USD in 2024 with 3–6% intra‑year swings materially pressured export realizations and margins.

Active hedging (forwards/options) cut FX P&L volatility by mid‑single digits, stabilizing cashflows.

Global apparel market ~1.7 trillion USD (2024); cotton ~24% and MMF ~60% of fiber mix (2023–24), driving input-price exposure.

RBI repo 6.50% (Jun 2024) raises funding costs; working‑capital and targeted automation improve payback.

| Metric | Value |

|---|---|

| INR/USD (2024) | 82–83 |

| FX swings (2024) | 3–6% |

| Apparel market (2024) | 1.7T USD |

| Cotton share (2023–24) | 24% |

| MMF share (2023–24) | 60% |

| RBI repo (Jun 2024) | 6.50% |

Same Document Delivered

Gokaldas PESTLE Analysis

The Gokaldas PESTLE analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible in this sample are exactly what you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured file.

Your Shortcut to Market Insight Starts Here

Our PESTLE analysis of Gokaldas reveals how political shifts, economic cycles, social trends, technological advances, legal changes and environmental pressures shape its prospects. Use these insights to anticipate risks and spot growth levers. Download the full, ready-to-use report now for actionable intelligence.

Political factors

Export-trade policy volatility

India’s export incentives, tariffs and FTAs—including the Rs 10,683 crore PLI textile scheme—directly shape apparel margins; India's apparel exports were about $18 billion in FY2023‑24, with EU/US/UK taking over 60% of volumes. Shifts in RoDTEP or duty‑drawback rates can materially change pricing power and margins, so monitoring EU/UK/US trade rules and origin criteria is critical. Proactive advocacy and diversified markets reduce policy shock risk.

Geopolitical tensions and logistics

Global flashpoints and Red Sea/Suez disruptions pushed container freight rates up over 30% and added 10–14 days to transit in 2023–24, raising costs and lead times for exporters. Sanctions and supplier shifts from China, Vietnam and Bangladesh have helped India capture re-routed demand, with apparel exports rising ~15% in 2024. Gokaldas must preserve multi-route logistics and near-shore options, hedging capacity and buffering delivery windows to protect service levels.

Labor and industrial relations

State-level implementation of the Code on Wages (2019) and divergent minimum wages across states materially affect Gokaldas’s unit labour costs and productivity; labour can account for a quarter to a third of factory operating costs in Indian apparel manufacturing. Stable industrial relations lower strike risk and allow flexible OT in peak seasons, while government skilling drives such as PMKVY expand skilled workforce and engagement with local authorities smooths plant operations.

Infrastructure and manufacturing policy

- PLI outlay: Rs 10,683 crore

- PM MITRA parks: 7 mega parks

- 2024–25 infra capex: Rs 11.1 lakh crore

- Key risks: power, port capacity, container shortages

- Benefit: supportive states = incentives + faster clearances

ESG-driven procurement norms

- EU CSRD ~50,000 companies covered

- Germany LkSG thresholds: >3,000 (2023) → >1,000 (2024)

- Due diligence laws drive more audits and supplier scrutiny

- Compliance readiness = higher probability of strategic contracts

PLI Rs 10,683 crore, apparel exports $18bn; freight +30%, volumes +15%

India PLI Rs 10,683 crore and apparel exports ~$18bn (FY2023‑24) drive margins; RoDTEP/duty‑drawback shifts can materially affect pricing. Red Sea/Suez shocks pushed freight >30% and exports re‑routing lifted India apparel volumes ~15% in 2024, so logistics resilience is critical. EU CSRD (~50,000 firms) and Germany LkSG (>1,000) raise ESG due diligence; documented compliance secures strategic buyers.

| Metric | Value |

|---|---|

| PLI outlay | Rs 10,683 crore |

| Apparel exports FY2023‑24 | $18bn |

| Freight rise (2023–24) | +30%+ |

| Export volume shift 2024 | ~+15% |

| EU CSRD | ~50,000 firms |

| Germany LkSG threshold 2024 | >1,000 employees |

What is included in the product

Provides a data-backed PESTLE assessment of Gokaldas across Political, Economic, Social, Technological, Environmental, and Legal dimensions, highlighting region- and industry-specific risks and opportunities with forward-looking insights to support executives, investors, and strategists in scenario planning and decision-making.

A concise, visually segmented Gokaldas PESTLE summary that relieves meeting prep pain by condensing external risk and market positioning into an easily shareable, editable format ideal for presentations, planning sessions, and quick team alignment.

Economic factors

Currency and hedging exposure

INR volatility versus USD/EUR materially affects Gokaldas export realizations and input costs; INR traded around 82–83 per USD in 2024 with several 3–6% intra‑year swings that pressured margins.

Effective hedging policies—using forwards and options—have been shown to cut FX P&L volatility by mid‑single digits, helping stabilize margins amid swings.

A weak INR improves price competitiveness for garments but raises imported machinery and input costs; a balanced currency book and natural hedges (local sourcing, USD receipts) are essential.

Global demand cycles

US/EU consumer spending drives Gokaldas order volumes and mix; the global apparel market was about 1.7 trillion USD in 2024, so shifts in Western demand materially impact exports. Recessions push sales toward value/basic categories while recoveries lift fashion and athleisure, changing price points and margins. Retail inventory corrections in 2023–24 caused short-term order deferrals, making agile capacity and category diversification key to smoothing revenues.

Raw material price fluctuations

Cotton, MMF, dyes and trims face cyclical and weather-driven swings that pressure costs; cotton made ~24% of global fiber production in 2023–24 while MMF accounted for roughly 60%, amplifying exposure to fibre-price moves. Input price spikes compress apparel margins when pass-through clauses are absent. Strategic sourcing and tighter inventory planning lower volatility. Blended fabrics and supplier diversification increase resilience.

Wage inflation and productivity

Rising statutory wages in India and export markets force Gokaldas to offset higher labor costs with productivity gains; industrial engineering, line balancing and targeted automation protect unit economics. Incentive-linked pay and attendance bonuses measurably lift throughput and retention. Continuous improvement programs (Kaizen, TPM) sustain cost competitiveness and margin resilience.

- IE methods: unit-cost focus

- Line balancing: reduce WIP

- Automation: lower touch labor

- Incentives: higher OEE and retention

Cost of capital and capex

Rising interest rates raise funding costs for Gokaldas’ capacity expansion and automation; RBI repo rate stood at 6.50% (June 2024), increasing loan pricing and payback thresholds. Efficient working-capital management reduces reliance on short-term debt during seasonal peaks, lowering financing strain. Targeted capex in high-ROI automation shortens payback even as rates stay elevated. Access to export credit lines (ECGC, EXIM Bank) underpins export-led growth.

- Interest rate backdrop: RBI repo 6.50% (Jun 2024)

- Working capital: reduces seasonal short-term borrowing

- Capex focus: high-ROI automation improves payback

- Financing support: ECGC/EXIM export credit lines

PLI Rs 10,683 crore, apparel exports $18bn; freight +30%, volumes +15%

INR ~82–83 per USD in 2024 with 3–6% intra‑year swings materially pressured export realizations and margins.

Active hedging (forwards/options) cut FX P&L volatility by mid‑single digits, stabilizing cashflows.

Global apparel market ~1.7 trillion USD (2024); cotton ~24% and MMF ~60% of fiber mix (2023–24), driving input-price exposure.

RBI repo 6.50% (Jun 2024) raises funding costs; working‑capital and targeted automation improve payback.

| Metric | Value |

|---|---|

| INR/USD (2024) | 82–83 |

| FX swings (2024) | 3–6% |

| Apparel market (2024) | 1.7T USD |

| Cotton share (2023–24) | 24% |

| MMF share (2023–24) | 60% |

| RBI repo (Jun 2024) | 6.50% |

Same Document Delivered

Gokaldas PESTLE Analysis

The Gokaldas PESTLE analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible in this sample are exactly what you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured file.

Description

Your Shortcut to Market Insight Starts Here

Our PESTLE analysis of Gokaldas reveals how political shifts, economic cycles, social trends, technological advances, legal changes and environmental pressures shape its prospects. Use these insights to anticipate risks and spot growth levers. Download the full, ready-to-use report now for actionable intelligence.

Political factors

Export-trade policy volatility

India’s export incentives, tariffs and FTAs—including the Rs 10,683 crore PLI textile scheme—directly shape apparel margins; India's apparel exports were about $18 billion in FY2023‑24, with EU/US/UK taking over 60% of volumes. Shifts in RoDTEP or duty‑drawback rates can materially change pricing power and margins, so monitoring EU/UK/US trade rules and origin criteria is critical. Proactive advocacy and diversified markets reduce policy shock risk.

Geopolitical tensions and logistics

Global flashpoints and Red Sea/Suez disruptions pushed container freight rates up over 30% and added 10–14 days to transit in 2023–24, raising costs and lead times for exporters. Sanctions and supplier shifts from China, Vietnam and Bangladesh have helped India capture re-routed demand, with apparel exports rising ~15% in 2024. Gokaldas must preserve multi-route logistics and near-shore options, hedging capacity and buffering delivery windows to protect service levels.

Labor and industrial relations

State-level implementation of the Code on Wages (2019) and divergent minimum wages across states materially affect Gokaldas’s unit labour costs and productivity; labour can account for a quarter to a third of factory operating costs in Indian apparel manufacturing. Stable industrial relations lower strike risk and allow flexible OT in peak seasons, while government skilling drives such as PMKVY expand skilled workforce and engagement with local authorities smooths plant operations.

Infrastructure and manufacturing policy

- PLI outlay: Rs 10,683 crore

- PM MITRA parks: 7 mega parks

- 2024–25 infra capex: Rs 11.1 lakh crore

- Key risks: power, port capacity, container shortages

- Benefit: supportive states = incentives + faster clearances

ESG-driven procurement norms

- EU CSRD ~50,000 companies covered

- Germany LkSG thresholds: >3,000 (2023) → >1,000 (2024)

- Due diligence laws drive more audits and supplier scrutiny

- Compliance readiness = higher probability of strategic contracts

PLI Rs 10,683 crore, apparel exports $18bn; freight +30%, volumes +15%

India PLI Rs 10,683 crore and apparel exports ~$18bn (FY2023‑24) drive margins; RoDTEP/duty‑drawback shifts can materially affect pricing. Red Sea/Suez shocks pushed freight >30% and exports re‑routing lifted India apparel volumes ~15% in 2024, so logistics resilience is critical. EU CSRD (~50,000 firms) and Germany LkSG (>1,000) raise ESG due diligence; documented compliance secures strategic buyers.

| Metric | Value |

|---|---|

| PLI outlay | Rs 10,683 crore |

| Apparel exports FY2023‑24 | $18bn |

| Freight rise (2023–24) | +30%+ |

| Export volume shift 2024 | ~+15% |

| EU CSRD | ~50,000 firms |

| Germany LkSG threshold 2024 | >1,000 employees |

What is included in the product

Provides a data-backed PESTLE assessment of Gokaldas across Political, Economic, Social, Technological, Environmental, and Legal dimensions, highlighting region- and industry-specific risks and opportunities with forward-looking insights to support executives, investors, and strategists in scenario planning and decision-making.

A concise, visually segmented Gokaldas PESTLE summary that relieves meeting prep pain by condensing external risk and market positioning into an easily shareable, editable format ideal for presentations, planning sessions, and quick team alignment.

Economic factors

Currency and hedging exposure

INR volatility versus USD/EUR materially affects Gokaldas export realizations and input costs; INR traded around 82–83 per USD in 2024 with several 3–6% intra‑year swings that pressured margins.

Effective hedging policies—using forwards and options—have been shown to cut FX P&L volatility by mid‑single digits, helping stabilize margins amid swings.

A weak INR improves price competitiveness for garments but raises imported machinery and input costs; a balanced currency book and natural hedges (local sourcing, USD receipts) are essential.

Global demand cycles

US/EU consumer spending drives Gokaldas order volumes and mix; the global apparel market was about 1.7 trillion USD in 2024, so shifts in Western demand materially impact exports. Recessions push sales toward value/basic categories while recoveries lift fashion and athleisure, changing price points and margins. Retail inventory corrections in 2023–24 caused short-term order deferrals, making agile capacity and category diversification key to smoothing revenues.

Raw material price fluctuations

Cotton, MMF, dyes and trims face cyclical and weather-driven swings that pressure costs; cotton made ~24% of global fiber production in 2023–24 while MMF accounted for roughly 60%, amplifying exposure to fibre-price moves. Input price spikes compress apparel margins when pass-through clauses are absent. Strategic sourcing and tighter inventory planning lower volatility. Blended fabrics and supplier diversification increase resilience.

Wage inflation and productivity

Rising statutory wages in India and export markets force Gokaldas to offset higher labor costs with productivity gains; industrial engineering, line balancing and targeted automation protect unit economics. Incentive-linked pay and attendance bonuses measurably lift throughput and retention. Continuous improvement programs (Kaizen, TPM) sustain cost competitiveness and margin resilience.

- IE methods: unit-cost focus

- Line balancing: reduce WIP

- Automation: lower touch labor

- Incentives: higher OEE and retention

Cost of capital and capex

Rising interest rates raise funding costs for Gokaldas’ capacity expansion and automation; RBI repo rate stood at 6.50% (June 2024), increasing loan pricing and payback thresholds. Efficient working-capital management reduces reliance on short-term debt during seasonal peaks, lowering financing strain. Targeted capex in high-ROI automation shortens payback even as rates stay elevated. Access to export credit lines (ECGC, EXIM Bank) underpins export-led growth.

- Interest rate backdrop: RBI repo 6.50% (Jun 2024)

- Working capital: reduces seasonal short-term borrowing

- Capex focus: high-ROI automation improves payback

- Financing support: ECGC/EXIM export credit lines

PLI Rs 10,683 crore, apparel exports $18bn; freight +30%, volumes +15%

INR ~82–83 per USD in 2024 with 3–6% intra‑year swings materially pressured export realizations and margins.

Active hedging (forwards/options) cut FX P&L volatility by mid‑single digits, stabilizing cashflows.

Global apparel market ~1.7 trillion USD (2024); cotton ~24% and MMF ~60% of fiber mix (2023–24), driving input-price exposure.

RBI repo 6.50% (Jun 2024) raises funding costs; working‑capital and targeted automation improve payback.

| Metric | Value |

|---|---|

| INR/USD (2024) | 82–83 |

| FX swings (2024) | 3–6% |

| Apparel market (2024) | 1.7T USD |

| Cotton share (2023–24) | 24% |

| MMF share (2023–24) | 60% |

| RBI repo (Jun 2024) | 6.50% |

Same Document Delivered

Gokaldas PESTLE Analysis

The Gokaldas PESTLE analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible in this sample are exactly what you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured file.