GoldMoney Porter's Five Forces Analysis

From Overview to Strategy Blueprint

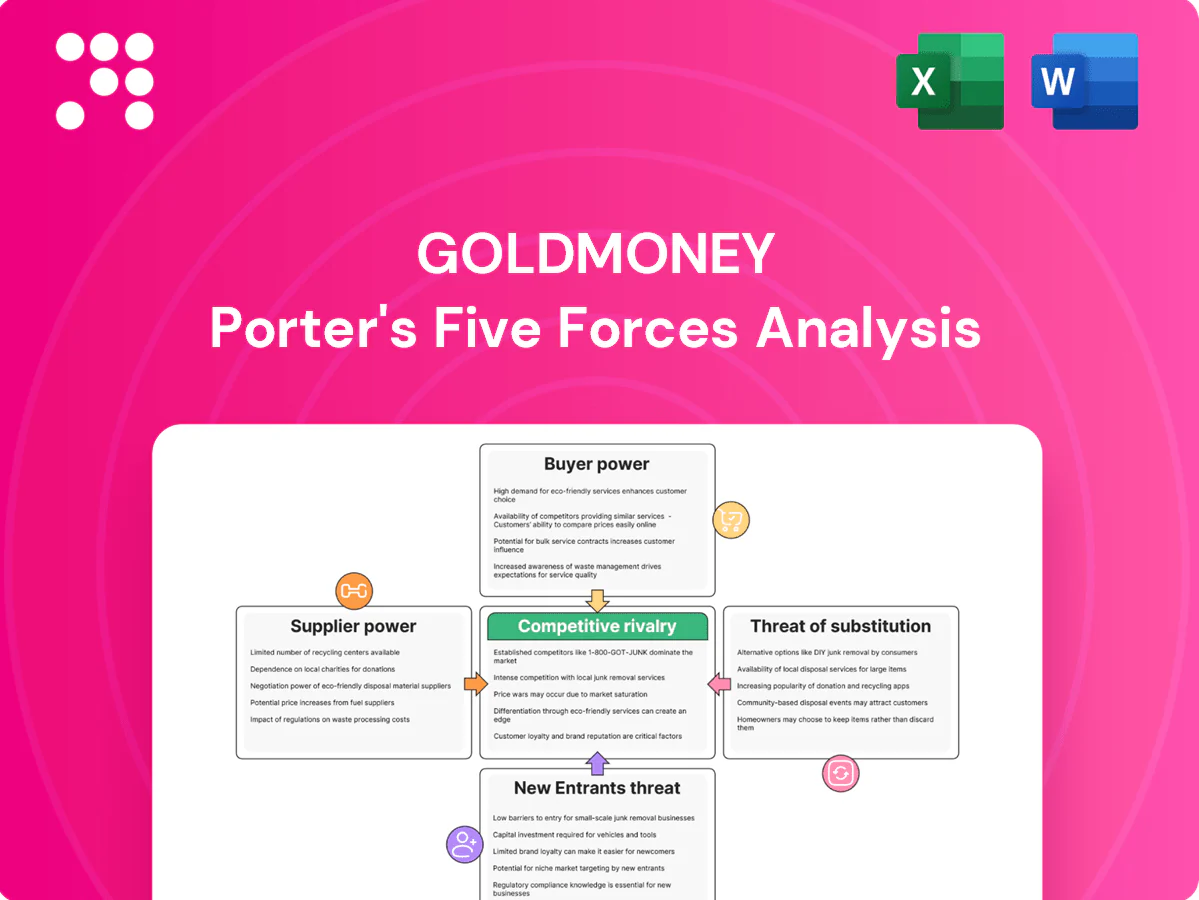

GoldMoney’s Porter's Five Forces snapshot highlights supplier concentration, buyer leverage, substitute threats, competitive rivalry, and entry barriers shaping its gold custody and fintech niche. We identify pressure points like regulatory shifts and digital payment trends that can alter margins and growth. This brief shows structural risks and strategic levers—actionable for investors and strategists. Unlock the full Porter's Five Forces Analysis to explore GoldMoney’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated refiners and mints

Precious metal supply depends on a limited set of LBMA-accredited refiners and sovereign mints, giving suppliers leverage over premiums, allocation and lead times; global above-ground gold stock is about 200,000 tonnes (2024). Goldmoney can mitigate via multi-sourcing and inventory, but quality and brand constraints limit substitution. Tight markets amplify supplier influence on spreads and delivery times.

Vaulting and logistics partners

Secure storage for GoldMoney relies on a small global network of vault operators and armored carriers concentrated in hubs like London, Zurich and Toronto; by 2024 these hubs remained the primary custody centers for allocated bullion. Switching vaults is operationally complex because of security, insurance and required client reassurances. Suppliers can influence pricing and service terms in these hubs, and long-term contracts mitigate price volatility but constrain operational flexibility.

Insurance underwriters

Insurance capacity for bullion remained specialized and constrained in 2024, making underwriters a tight supplier group and increasing their bargaining power. After loss events and market stress underwriters have demonstrated the ability to raise rates or impose exclusions, pressuring buyers. GoldMoney’s need for comprehensive bullion coverage limits its negotiation room; diversifying carriers reduces vendor risk but raises coordination complexity.

Market makers and liquidity

Market makers and bank liquidity providers directly affect execution quality for GoldMoney client trades and hedges; wider interbank spreads during market stress raise GoldMoney’s transaction and hedging costs, and reliance on a small set of counterparties concentrates exposure to their pricing, terms and credit limits. Building internal liquidity pools can mitigate supplier power but requires significant capital, technology and risk controls.

- Spot liquidity providers: execution quality

- Wider interbank spreads: higher costs in volatility

- Concentration risk: few counterparties

- Internal pools: capital and systems required

Regulatory and compliance vendors

Regulatory and compliance vendors for eKYC/AML, audit and custody are highly specialized and hard to replace; in 2024 regtech adoption grew ~25% YoY, concentrating dependence on a few providers. Price increases or capacity limits pass directly into unit economics, pressuring margins. Vendor reliability directly affects onboarding speed and client experience, sometimes changing activation times by weeks.

- Concentration risk: few specialist vendors

- Cost passthrough: impacts unit economics

- Operational risk: onboarding delays harm CX

- Mitigation: multi-vendor reduces risk but raises overhead

Concentrated gold suppliers drive higher custody and insurance premiums in 2024

Suppliers (refiners, mints, vaults, insurers, liquidity and regtech vendors) hold elevated bargaining power from concentration, specialized capacity and delivery constraints; global above‑ground gold stock ~200,000 tonnes (2024). Tight custody and insurance markets raise premiums and friction; regtech adoption grew ~25% YoY (2024), concentrating vendor dependence.

| Supplier | Concentration | 2024 metric | Impact |

|---|---|---|---|

| Refiners/mints | High | Allocation/lead times constrained | Premiums, limited substitution |

| Vaults | Regional hubs | London/Zurich/Toronto primary | Switching costs, service pricing |

| Insurers | Specialized | Capacity constrained | Higher rates, exclusions |

| Regtech | Few providers | Adoption +25% YoY | Onboarding delays, cost passthrough |

| Liquidity | Concentrated | Wider spreads in stress | Higher transaction/hedge costs |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored to GoldMoney, revealing competitive intensity, buyer/supplier power, threats from substitutes and entrants, and strategic levers to protect margin and market share.

GoldMoney's Porter's Five Forces delivers a single-sheet, customizable analysis with an instant radar chart to visualize competitive pressure—model pre/post-regulation or new-entrant scenarios without macros and drop-ready for decks or dashboards.

Customers Bargaining Power

High price transparency

Spot metal prices are publicly listed on LBMA and platforms like Kitco, letting clients compare fees and premiums in real time; retail premiums typically range 1–5% and online dealer spreads often under 1%. This transparency lets customers benchmark Goldmoney’s spreads against dealers and platforms, compressing margins and raising switching incentives. Goldmoney must justify any premium through value-added services.

Low switching costs

Low switching costs mean clients can sell and repurchase bullion elsewhere with minimal frictions, increasing buyer leverage over GoldMoney in pricing and service terms.

Digital competitors in 2024 reduced onboarding and transfer times to under 48 hours on average, further easing migration and negotiating power.

That heightened leverage forces stronger retention efforts; loyalty programs and tiered fees have proven effective to damp churn by rewarding larger balances and activity.

Segment mix and ticket size

In 2024 institutional and high‑net‑worth GoldMoney clients continued to leverage scale to negotiate lower fees and bespoke service levels, while retail customers remained price sensitive but lack individual bargaining power. Shifts in product mix between allocated and unallocated holdings alter perceived value and custody costs, with allocated assets commanding premium pricing. Concentration in a few large accounts raises buyer‑power and revenue-at-risk if renegotiations occur.

Service quality and trust sensitivity

Storage safety, redemption reliability and audit transparency drive buyer expectations for GoldMoney; any custody lapse quickly erodes trust in a custodial model, and in 2024 global allocated precious-metals custody surpassed $200 billion, raising scrutiny on proof of allocation and insurance. Buyers demand clear, third-party attestations and insured, segregated holdings; strong reporting raises perceived switching costs and weakens bargaining power.

- Storage safety: segregated vaults, insured

- Redemption reliability: timely physical delivery

- Audit transparency: regular third-party attestations

- Impact: higher switching risk reduces buyer leverage

Alternative access demands

Clients demand multi-currency wallets, instant liquidity and card spend; unmet needs drive buyers toward payment-first platforms, raising functional bargaining power and forcing GoldMoney to reprioritize roadmap items. In 2024 global digital wallet users reached 4.4 billion (Statista), amplifying urgency; partnerships can deliver payments utility faster than full in-house builds.

- multi-currency wallets

- instant liquidity

- card spend

- partnerships over full builds

Price transparency, low switching squeeze margins; premiums 1-5%, wallets 4.4bn

High price transparency (LBMA/Kitco) and low switching costs give buyers strong leverage; retail premiums 1–5% and online spreads often <1% compress margins. Institutional clients use scale to negotiate bespoke fees; concentration raises revenue risk. Custody trust matters—allocated custody >$200bn in 2024; digital-wallet demand (4.4bn users in 2024) raises functional bargaining power.

| Metric | 2024 Value |

|---|---|

| Retail premiums | 1–5% |

| Online spreads | <1% |

| Allocated custody | >$200bn |

| Digital wallet users | 4.4bn |

Preview the Actual Deliverable

GoldMoney Porter's Five Forces Analysis

This preview shows the exact GoldMoney Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, final and ready to use. You're viewing the same professionally written document available for instant download with no placeholders or samples. Purchase grants immediate access to this identical file for your analysis and decision-making.

From Overview to Strategy Blueprint

GoldMoney’s Porter's Five Forces snapshot highlights supplier concentration, buyer leverage, substitute threats, competitive rivalry, and entry barriers shaping its gold custody and fintech niche. We identify pressure points like regulatory shifts and digital payment trends that can alter margins and growth. This brief shows structural risks and strategic levers—actionable for investors and strategists. Unlock the full Porter's Five Forces Analysis to explore GoldMoney’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated refiners and mints

Precious metal supply depends on a limited set of LBMA-accredited refiners and sovereign mints, giving suppliers leverage over premiums, allocation and lead times; global above-ground gold stock is about 200,000 tonnes (2024). Goldmoney can mitigate via multi-sourcing and inventory, but quality and brand constraints limit substitution. Tight markets amplify supplier influence on spreads and delivery times.

Vaulting and logistics partners

Secure storage for GoldMoney relies on a small global network of vault operators and armored carriers concentrated in hubs like London, Zurich and Toronto; by 2024 these hubs remained the primary custody centers for allocated bullion. Switching vaults is operationally complex because of security, insurance and required client reassurances. Suppliers can influence pricing and service terms in these hubs, and long-term contracts mitigate price volatility but constrain operational flexibility.

Insurance underwriters

Insurance capacity for bullion remained specialized and constrained in 2024, making underwriters a tight supplier group and increasing their bargaining power. After loss events and market stress underwriters have demonstrated the ability to raise rates or impose exclusions, pressuring buyers. GoldMoney’s need for comprehensive bullion coverage limits its negotiation room; diversifying carriers reduces vendor risk but raises coordination complexity.

Market makers and liquidity

Market makers and bank liquidity providers directly affect execution quality for GoldMoney client trades and hedges; wider interbank spreads during market stress raise GoldMoney’s transaction and hedging costs, and reliance on a small set of counterparties concentrates exposure to their pricing, terms and credit limits. Building internal liquidity pools can mitigate supplier power but requires significant capital, technology and risk controls.

- Spot liquidity providers: execution quality

- Wider interbank spreads: higher costs in volatility

- Concentration risk: few counterparties

- Internal pools: capital and systems required

Regulatory and compliance vendors

Regulatory and compliance vendors for eKYC/AML, audit and custody are highly specialized and hard to replace; in 2024 regtech adoption grew ~25% YoY, concentrating dependence on a few providers. Price increases or capacity limits pass directly into unit economics, pressuring margins. Vendor reliability directly affects onboarding speed and client experience, sometimes changing activation times by weeks.

- Concentration risk: few specialist vendors

- Cost passthrough: impacts unit economics

- Operational risk: onboarding delays harm CX

- Mitigation: multi-vendor reduces risk but raises overhead

Concentrated gold suppliers drive higher custody and insurance premiums in 2024

Suppliers (refiners, mints, vaults, insurers, liquidity and regtech vendors) hold elevated bargaining power from concentration, specialized capacity and delivery constraints; global above‑ground gold stock ~200,000 tonnes (2024). Tight custody and insurance markets raise premiums and friction; regtech adoption grew ~25% YoY (2024), concentrating vendor dependence.

| Supplier | Concentration | 2024 metric | Impact |

|---|---|---|---|

| Refiners/mints | High | Allocation/lead times constrained | Premiums, limited substitution |

| Vaults | Regional hubs | London/Zurich/Toronto primary | Switching costs, service pricing |

| Insurers | Specialized | Capacity constrained | Higher rates, exclusions |

| Regtech | Few providers | Adoption +25% YoY | Onboarding delays, cost passthrough |

| Liquidity | Concentrated | Wider spreads in stress | Higher transaction/hedge costs |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored to GoldMoney, revealing competitive intensity, buyer/supplier power, threats from substitutes and entrants, and strategic levers to protect margin and market share.

GoldMoney's Porter's Five Forces delivers a single-sheet, customizable analysis with an instant radar chart to visualize competitive pressure—model pre/post-regulation or new-entrant scenarios without macros and drop-ready for decks or dashboards.

Customers Bargaining Power

High price transparency

Spot metal prices are publicly listed on LBMA and platforms like Kitco, letting clients compare fees and premiums in real time; retail premiums typically range 1–5% and online dealer spreads often under 1%. This transparency lets customers benchmark Goldmoney’s spreads against dealers and platforms, compressing margins and raising switching incentives. Goldmoney must justify any premium through value-added services.

Low switching costs

Low switching costs mean clients can sell and repurchase bullion elsewhere with minimal frictions, increasing buyer leverage over GoldMoney in pricing and service terms.

Digital competitors in 2024 reduced onboarding and transfer times to under 48 hours on average, further easing migration and negotiating power.

That heightened leverage forces stronger retention efforts; loyalty programs and tiered fees have proven effective to damp churn by rewarding larger balances and activity.

Segment mix and ticket size

In 2024 institutional and high‑net‑worth GoldMoney clients continued to leverage scale to negotiate lower fees and bespoke service levels, while retail customers remained price sensitive but lack individual bargaining power. Shifts in product mix between allocated and unallocated holdings alter perceived value and custody costs, with allocated assets commanding premium pricing. Concentration in a few large accounts raises buyer‑power and revenue-at-risk if renegotiations occur.

Service quality and trust sensitivity

Storage safety, redemption reliability and audit transparency drive buyer expectations for GoldMoney; any custody lapse quickly erodes trust in a custodial model, and in 2024 global allocated precious-metals custody surpassed $200 billion, raising scrutiny on proof of allocation and insurance. Buyers demand clear, third-party attestations and insured, segregated holdings; strong reporting raises perceived switching costs and weakens bargaining power.

- Storage safety: segregated vaults, insured

- Redemption reliability: timely physical delivery

- Audit transparency: regular third-party attestations

- Impact: higher switching risk reduces buyer leverage

Alternative access demands

Clients demand multi-currency wallets, instant liquidity and card spend; unmet needs drive buyers toward payment-first platforms, raising functional bargaining power and forcing GoldMoney to reprioritize roadmap items. In 2024 global digital wallet users reached 4.4 billion (Statista), amplifying urgency; partnerships can deliver payments utility faster than full in-house builds.

- multi-currency wallets

- instant liquidity

- card spend

- partnerships over full builds

Price transparency, low switching squeeze margins; premiums 1-5%, wallets 4.4bn

High price transparency (LBMA/Kitco) and low switching costs give buyers strong leverage; retail premiums 1–5% and online spreads often <1% compress margins. Institutional clients use scale to negotiate bespoke fees; concentration raises revenue risk. Custody trust matters—allocated custody >$200bn in 2024; digital-wallet demand (4.4bn users in 2024) raises functional bargaining power.

| Metric | 2024 Value |

|---|---|

| Retail premiums | 1–5% |

| Online spreads | <1% |

| Allocated custody | >$200bn |

| Digital wallet users | 4.4bn |

Preview the Actual Deliverable

GoldMoney Porter's Five Forces Analysis

This preview shows the exact GoldMoney Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, final and ready to use. You're viewing the same professionally written document available for instant download with no placeholders or samples. Purchase grants immediate access to this identical file for your analysis and decision-making.

Description

From Overview to Strategy Blueprint

GoldMoney’s Porter's Five Forces snapshot highlights supplier concentration, buyer leverage, substitute threats, competitive rivalry, and entry barriers shaping its gold custody and fintech niche. We identify pressure points like regulatory shifts and digital payment trends that can alter margins and growth. This brief shows structural risks and strategic levers—actionable for investors and strategists. Unlock the full Porter's Five Forces Analysis to explore GoldMoney’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated refiners and mints

Precious metal supply depends on a limited set of LBMA-accredited refiners and sovereign mints, giving suppliers leverage over premiums, allocation and lead times; global above-ground gold stock is about 200,000 tonnes (2024). Goldmoney can mitigate via multi-sourcing and inventory, but quality and brand constraints limit substitution. Tight markets amplify supplier influence on spreads and delivery times.

Vaulting and logistics partners

Secure storage for GoldMoney relies on a small global network of vault operators and armored carriers concentrated in hubs like London, Zurich and Toronto; by 2024 these hubs remained the primary custody centers for allocated bullion. Switching vaults is operationally complex because of security, insurance and required client reassurances. Suppliers can influence pricing and service terms in these hubs, and long-term contracts mitigate price volatility but constrain operational flexibility.

Insurance underwriters

Insurance capacity for bullion remained specialized and constrained in 2024, making underwriters a tight supplier group and increasing their bargaining power. After loss events and market stress underwriters have demonstrated the ability to raise rates or impose exclusions, pressuring buyers. GoldMoney’s need for comprehensive bullion coverage limits its negotiation room; diversifying carriers reduces vendor risk but raises coordination complexity.

Market makers and liquidity

Market makers and bank liquidity providers directly affect execution quality for GoldMoney client trades and hedges; wider interbank spreads during market stress raise GoldMoney’s transaction and hedging costs, and reliance on a small set of counterparties concentrates exposure to their pricing, terms and credit limits. Building internal liquidity pools can mitigate supplier power but requires significant capital, technology and risk controls.

- Spot liquidity providers: execution quality

- Wider interbank spreads: higher costs in volatility

- Concentration risk: few counterparties

- Internal pools: capital and systems required

Regulatory and compliance vendors

Regulatory and compliance vendors for eKYC/AML, audit and custody are highly specialized and hard to replace; in 2024 regtech adoption grew ~25% YoY, concentrating dependence on a few providers. Price increases or capacity limits pass directly into unit economics, pressuring margins. Vendor reliability directly affects onboarding speed and client experience, sometimes changing activation times by weeks.

- Concentration risk: few specialist vendors

- Cost passthrough: impacts unit economics

- Operational risk: onboarding delays harm CX

- Mitigation: multi-vendor reduces risk but raises overhead

Concentrated gold suppliers drive higher custody and insurance premiums in 2024

Suppliers (refiners, mints, vaults, insurers, liquidity and regtech vendors) hold elevated bargaining power from concentration, specialized capacity and delivery constraints; global above‑ground gold stock ~200,000 tonnes (2024). Tight custody and insurance markets raise premiums and friction; regtech adoption grew ~25% YoY (2024), concentrating vendor dependence.

| Supplier | Concentration | 2024 metric | Impact |

|---|---|---|---|

| Refiners/mints | High | Allocation/lead times constrained | Premiums, limited substitution |

| Vaults | Regional hubs | London/Zurich/Toronto primary | Switching costs, service pricing |

| Insurers | Specialized | Capacity constrained | Higher rates, exclusions |

| Regtech | Few providers | Adoption +25% YoY | Onboarding delays, cost passthrough |

| Liquidity | Concentrated | Wider spreads in stress | Higher transaction/hedge costs |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored to GoldMoney, revealing competitive intensity, buyer/supplier power, threats from substitutes and entrants, and strategic levers to protect margin and market share.

GoldMoney's Porter's Five Forces delivers a single-sheet, customizable analysis with an instant radar chart to visualize competitive pressure—model pre/post-regulation or new-entrant scenarios without macros and drop-ready for decks or dashboards.

Customers Bargaining Power

High price transparency

Spot metal prices are publicly listed on LBMA and platforms like Kitco, letting clients compare fees and premiums in real time; retail premiums typically range 1–5% and online dealer spreads often under 1%. This transparency lets customers benchmark Goldmoney’s spreads against dealers and platforms, compressing margins and raising switching incentives. Goldmoney must justify any premium through value-added services.

Low switching costs

Low switching costs mean clients can sell and repurchase bullion elsewhere with minimal frictions, increasing buyer leverage over GoldMoney in pricing and service terms.

Digital competitors in 2024 reduced onboarding and transfer times to under 48 hours on average, further easing migration and negotiating power.

That heightened leverage forces stronger retention efforts; loyalty programs and tiered fees have proven effective to damp churn by rewarding larger balances and activity.

Segment mix and ticket size

In 2024 institutional and high‑net‑worth GoldMoney clients continued to leverage scale to negotiate lower fees and bespoke service levels, while retail customers remained price sensitive but lack individual bargaining power. Shifts in product mix between allocated and unallocated holdings alter perceived value and custody costs, with allocated assets commanding premium pricing. Concentration in a few large accounts raises buyer‑power and revenue-at-risk if renegotiations occur.

Service quality and trust sensitivity

Storage safety, redemption reliability and audit transparency drive buyer expectations for GoldMoney; any custody lapse quickly erodes trust in a custodial model, and in 2024 global allocated precious-metals custody surpassed $200 billion, raising scrutiny on proof of allocation and insurance. Buyers demand clear, third-party attestations and insured, segregated holdings; strong reporting raises perceived switching costs and weakens bargaining power.

- Storage safety: segregated vaults, insured

- Redemption reliability: timely physical delivery

- Audit transparency: regular third-party attestations

- Impact: higher switching risk reduces buyer leverage

Alternative access demands

Clients demand multi-currency wallets, instant liquidity and card spend; unmet needs drive buyers toward payment-first platforms, raising functional bargaining power and forcing GoldMoney to reprioritize roadmap items. In 2024 global digital wallet users reached 4.4 billion (Statista), amplifying urgency; partnerships can deliver payments utility faster than full in-house builds.

- multi-currency wallets

- instant liquidity

- card spend

- partnerships over full builds

Price transparency, low switching squeeze margins; premiums 1-5%, wallets 4.4bn

High price transparency (LBMA/Kitco) and low switching costs give buyers strong leverage; retail premiums 1–5% and online spreads often <1% compress margins. Institutional clients use scale to negotiate bespoke fees; concentration raises revenue risk. Custody trust matters—allocated custody >$200bn in 2024; digital-wallet demand (4.4bn users in 2024) raises functional bargaining power.

| Metric | 2024 Value |

|---|---|

| Retail premiums | 1–5% |

| Online spreads | <1% |

| Allocated custody | >$200bn |

| Digital wallet users | 4.4bn |

Preview the Actual Deliverable

GoldMoney Porter's Five Forces Analysis

This preview shows the exact GoldMoney Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, final and ready to use. You're viewing the same professionally written document available for instant download with no placeholders or samples. Purchase grants immediate access to this identical file for your analysis and decision-making.