Goodwin Procter Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

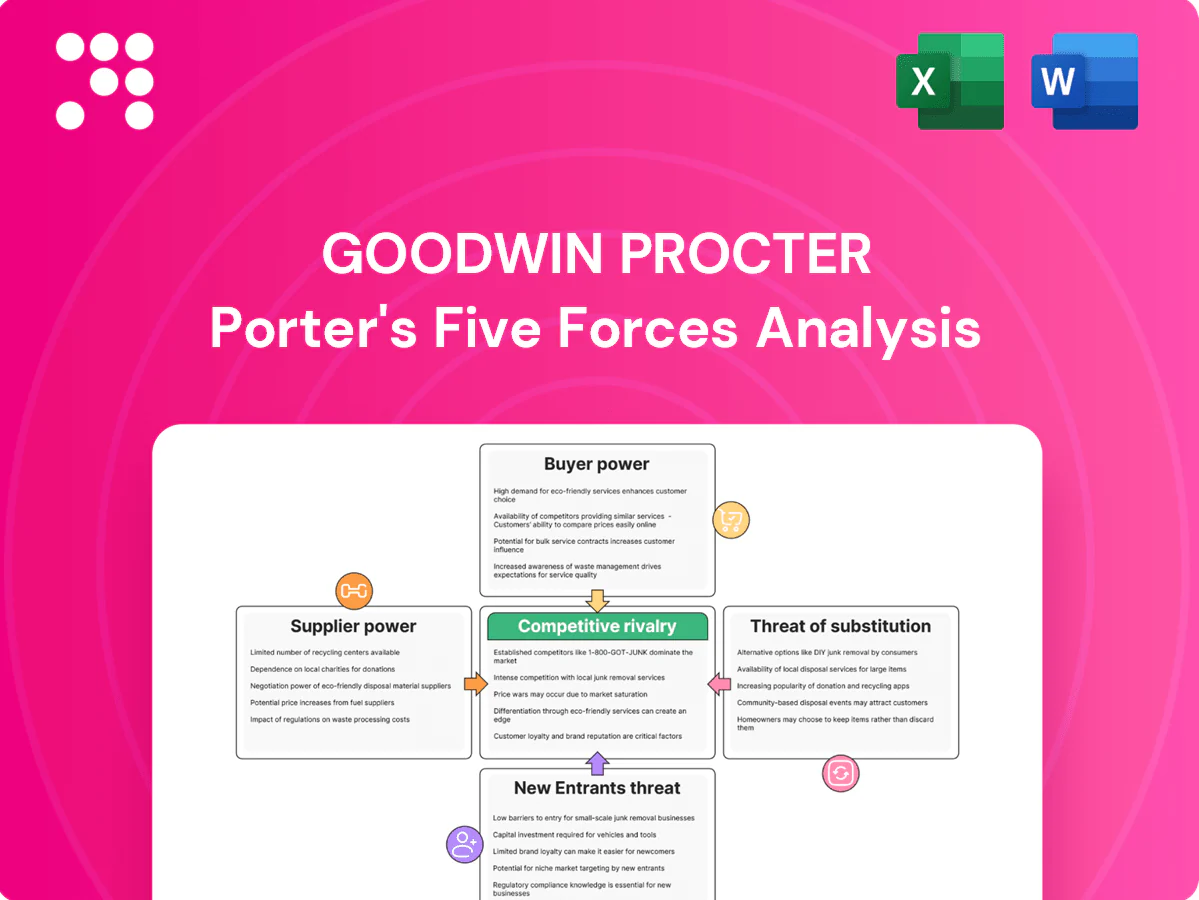

Goodwin Procter’s Porter's Five Forces snapshot highlights competitive intensity, client bargaining power, substitute legal services, supplier influence, and entry barriers shaping firm strategy. It reveals where pressure points and advantages lie. Want the full, consultant-grade force-by-force breakdown with visuals and ratings? Purchase the complete analysis to inform strategy and investments.

Suppliers Bargaining Power

Elite legal talent scarcity

Partners and top associates are the critical inputs and their scarcity raises supplier power; 2024 BigLaw first-year associate pay remained at $215,000, anchoring compensation expectations while lateral premiums and signing bonuses squeeze margins. Retention depends on culture, platform, and deal flow, giving star lawyers leverage, and wage inflation plus cyclical bonus ramps in hot PE and tech sectors amplify short-term cost pressure.

Specialist experts and co-counsel

Specialist expert witnesses, niche regulatory counsel and foreign local counsel are often indispensable in life sciences, fintech and cross-border matters, and in 2024 their scarcity and reputational prominence continued to strengthen bargaining leverage. Switching mid-matter is costly—both financially and procedurally—so firms like Goodwin face lock-in effects that sustain premium rates. Volume discounts and preferred networks can moderate fees but do not eliminate dependence on these scarce suppliers.

Legal tech and e-discovery stack

Platforms for e-discovery, AI review, and knowledge management are concentrated among a few vendors—the global e-discovery market was around $10.5B in 2024 with a ~12% CAGR, giving market leaders outsized pricing power.

Integration costs, complex data security and compliance needs raise switching friction, enabling vendors to push premium features and volume-based pricing.

Counterweights include multi-vendor strategies, Relativity-like alternatives, and growing in-house tooling that trim supplier leverage.

Data, research, and filing services

Legal research, market data, and filing providers are oligopolistic, led by Thomson Reuters, RELX (LexisNexis) and Bloomberg, which together account for over two-thirds of the legal research market in 2024. License bundling and seat-based pricing lock in spend; enterprise contracts improve negotiation leverage but baseline dependence on these vendors persists. High quality and speed needs in litigation and deals limit firms’ ability to cut back.

- Oligopoly: top three >66% share (2024)

- Pricing: seat-based + bundled licenses

- Leverage: better with enterprise deals

- Constraint: quality/speed needs sustain demand

Prime real estate and support services

Prestige locations and Class A offices remain central for client signaling and talent retention, with trophy rents often 10–30% above submarket averages in 2024; landlords in core markets therefore retain pricing power even as hybrid work trims overall space needs. Facilities, court services and translation vendors materially affect the cost base, and long leases—commonly 7–15 years—create rigidity but permit renegotiation at renewal cycles.

- Pricing power: landlords in core markets — premium 10–30%

- Lease length: common 7–15 years

- Cost drivers: facilities, court services, translation vendors

- Hybrid impact: reduced but not eliminated demand

Supplier dominance fuels BigLaw wage and vendor pricing pressure, squeezing margins

Partners, star associates and niche experts wield high supplier power—BigLaw 1L pay anchored at $215,000 in 2024 and retention drives wage pressure; e-discovery vendors lead a ~$10.5B market (2024) with ~12% CAGR, strengthening vendor pricing. Legal research/top-three vendors hold >66% share (2024), while core-office rents remain 10–30% above submarkets, raising fixed costs.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Associate pay | $215,000 | Wage anchor |

| E-discovery | $10.5B, 12% CAGR | Pricing power |

| Legal research | Top3 >66% | Lock-in |

| Office rents | +10–30% | Fixed cost |

What is included in the product

Tailored exclusively for Goodwin Procter, this Porter’s Five Forces analysis uncovers key drivers of competition, customer influence, and market entry risks while evaluating supplier and buyer power, substitutes, and disruptive threats to the firm’s profitability and market position.

A concise Goodwin Procter Porter's Five Forces one-sheet that clarifies competitive pressures, offers adjustable pressure sliders and an instant radar chart for strategic insight, and delivers a clean, slide-ready layout with no macros—easy to swap data, embed in dashboards, or pair with Word reports.

Customers Bargaining Power

Sophisticated corporate procurement

Clients in PE, tech, life sciences, real estate and financial services increasingly use panels and RFPs, driving comparative evaluations that heighten fee pressure and service-level demands. Metrics-driven oversight—KPIs, SLAs and outcome-linked fees—has grown alongside industry capital; private equity dry powder was about $2.5 trillion in 2024, intensifying accountability on efficiency. Consolidation to fewer firms concentrates spend and raises client negotiating leverage.

Alternatives and in-house leverage

ALSPs (~$18B market in 2023) plus Big Four legal arms and expanding in-house teams give clients credible outside options, driving unbundling of tasks to lower‑cost providers while reserving outside counsel for high‑value work. That modularity compresses blended rates and hours and, per 2023–24 surveys showing 40–60% of legal departments growing headcount, forces process innovation and rapid tech adoption to defend share.

Price sensitivity and AFAs

Buyers push Goodwin for capped fees, success fees and subscription models, with 2024 surveys showing rising demand for AFAs as a primary procurement criterion. AFAs shift risk to the firm and reward process discipline and efficiency improvements. Rate increases face client resistance unless tied to demonstrable value or sector scarcity, and budget predictability often trumps open-ended hourly billing.

Switching costs and relationship stickiness

Deep sector knowledge, deal history, and client trust raise switching costs for complex Goodwin Procter matters; conflicts, confidentiality risks, and ramp-up time further deter rapid moves. For commoditized tasks (due diligence, routine filings) switching is easier and more frequent, while multi-firm panels—in 2024 commonly 2–4 firms per client—maintain competitive tension.

- Deep knowledge = higher stickiness

- Conflicts/confidentiality increase switching barriers

- Routine work = low switching cost

- Multi-firm panels (2024: typically 2–4) sustain competition

Global capability and speed demands

Buyers now demand seamless cross-border coverage and 24/7 responsiveness, reallocating work after any delay or coverage gap; reliability under time pressure is treated as table-stakes rather than a premium service.

Firms must efficiently coordinate multi-jurisdictional teams and tech-enabled handoffs to retain clients and prevent revenue leakage tied to missed timelines.

- 24/7 responsiveness: client expectation

- Coverage gaps → client reallocations

- Coordination of multi-jurisdictional teams

- Reliability = retention differentiator

PE dry powder and ALSP growth fuel panel RFPs, AFAs and in‑house legal expansion

Clients in PE, tech, life sciences, real estate and financial services use panels/RFPs, raising fee pressure and service demands. Private equity dry powder was about $2.5 trillion in 2024, intensifying KPI/SLA oversight. ALSPs (~$18B market in 2023) and in‑house hiring (40–60% headcount growth in 2023–24 surveys) create credible alternatives and drive AFAs. Multi‑firm panels (2024: typically 2–4) and 24/7 cross‑border needs increase buyer leverage on commoditized work.

| Metric | 2023–24 data |

|---|---|

| PE dry powder | $2.5 trillion (2024) |

| ALSP market | ~$18 billion (2023) |

| In‑house growth | 40–60% headcount rise (2023–24 surveys) |

| Panel size | Typically 2–4 firms (2024) |

What You See Is What You Get

Goodwin Procter Porter's Five Forces Analysis

This preview is the exact Goodwin Procter Porter’s Five Forces analysis you’ll receive upon purchase — no samples, no placeholders. The full document is professionally written, fully formatted, and ready for immediate download and use. What you see here is precisely what will be delivered instantly after payment.

A Must-Have Tool for Decision-Makers

Goodwin Procter’s Porter's Five Forces snapshot highlights competitive intensity, client bargaining power, substitute legal services, supplier influence, and entry barriers shaping firm strategy. It reveals where pressure points and advantages lie. Want the full, consultant-grade force-by-force breakdown with visuals and ratings? Purchase the complete analysis to inform strategy and investments.

Suppliers Bargaining Power

Elite legal talent scarcity

Partners and top associates are the critical inputs and their scarcity raises supplier power; 2024 BigLaw first-year associate pay remained at $215,000, anchoring compensation expectations while lateral premiums and signing bonuses squeeze margins. Retention depends on culture, platform, and deal flow, giving star lawyers leverage, and wage inflation plus cyclical bonus ramps in hot PE and tech sectors amplify short-term cost pressure.

Specialist experts and co-counsel

Specialist expert witnesses, niche regulatory counsel and foreign local counsel are often indispensable in life sciences, fintech and cross-border matters, and in 2024 their scarcity and reputational prominence continued to strengthen bargaining leverage. Switching mid-matter is costly—both financially and procedurally—so firms like Goodwin face lock-in effects that sustain premium rates. Volume discounts and preferred networks can moderate fees but do not eliminate dependence on these scarce suppliers.

Legal tech and e-discovery stack

Platforms for e-discovery, AI review, and knowledge management are concentrated among a few vendors—the global e-discovery market was around $10.5B in 2024 with a ~12% CAGR, giving market leaders outsized pricing power.

Integration costs, complex data security and compliance needs raise switching friction, enabling vendors to push premium features and volume-based pricing.

Counterweights include multi-vendor strategies, Relativity-like alternatives, and growing in-house tooling that trim supplier leverage.

Data, research, and filing services

Legal research, market data, and filing providers are oligopolistic, led by Thomson Reuters, RELX (LexisNexis) and Bloomberg, which together account for over two-thirds of the legal research market in 2024. License bundling and seat-based pricing lock in spend; enterprise contracts improve negotiation leverage but baseline dependence on these vendors persists. High quality and speed needs in litigation and deals limit firms’ ability to cut back.

- Oligopoly: top three >66% share (2024)

- Pricing: seat-based + bundled licenses

- Leverage: better with enterprise deals

- Constraint: quality/speed needs sustain demand

Prime real estate and support services

Prestige locations and Class A offices remain central for client signaling and talent retention, with trophy rents often 10–30% above submarket averages in 2024; landlords in core markets therefore retain pricing power even as hybrid work trims overall space needs. Facilities, court services and translation vendors materially affect the cost base, and long leases—commonly 7–15 years—create rigidity but permit renegotiation at renewal cycles.

- Pricing power: landlords in core markets — premium 10–30%

- Lease length: common 7–15 years

- Cost drivers: facilities, court services, translation vendors

- Hybrid impact: reduced but not eliminated demand

Supplier dominance fuels BigLaw wage and vendor pricing pressure, squeezing margins

Partners, star associates and niche experts wield high supplier power—BigLaw 1L pay anchored at $215,000 in 2024 and retention drives wage pressure; e-discovery vendors lead a ~$10.5B market (2024) with ~12% CAGR, strengthening vendor pricing. Legal research/top-three vendors hold >66% share (2024), while core-office rents remain 10–30% above submarkets, raising fixed costs.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Associate pay | $215,000 | Wage anchor |

| E-discovery | $10.5B, 12% CAGR | Pricing power |

| Legal research | Top3 >66% | Lock-in |

| Office rents | +10–30% | Fixed cost |

What is included in the product

Tailored exclusively for Goodwin Procter, this Porter’s Five Forces analysis uncovers key drivers of competition, customer influence, and market entry risks while evaluating supplier and buyer power, substitutes, and disruptive threats to the firm’s profitability and market position.

A concise Goodwin Procter Porter's Five Forces one-sheet that clarifies competitive pressures, offers adjustable pressure sliders and an instant radar chart for strategic insight, and delivers a clean, slide-ready layout with no macros—easy to swap data, embed in dashboards, or pair with Word reports.

Customers Bargaining Power

Sophisticated corporate procurement

Clients in PE, tech, life sciences, real estate and financial services increasingly use panels and RFPs, driving comparative evaluations that heighten fee pressure and service-level demands. Metrics-driven oversight—KPIs, SLAs and outcome-linked fees—has grown alongside industry capital; private equity dry powder was about $2.5 trillion in 2024, intensifying accountability on efficiency. Consolidation to fewer firms concentrates spend and raises client negotiating leverage.

Alternatives and in-house leverage

ALSPs (~$18B market in 2023) plus Big Four legal arms and expanding in-house teams give clients credible outside options, driving unbundling of tasks to lower‑cost providers while reserving outside counsel for high‑value work. That modularity compresses blended rates and hours and, per 2023–24 surveys showing 40–60% of legal departments growing headcount, forces process innovation and rapid tech adoption to defend share.

Price sensitivity and AFAs

Buyers push Goodwin for capped fees, success fees and subscription models, with 2024 surveys showing rising demand for AFAs as a primary procurement criterion. AFAs shift risk to the firm and reward process discipline and efficiency improvements. Rate increases face client resistance unless tied to demonstrable value or sector scarcity, and budget predictability often trumps open-ended hourly billing.

Switching costs and relationship stickiness

Deep sector knowledge, deal history, and client trust raise switching costs for complex Goodwin Procter matters; conflicts, confidentiality risks, and ramp-up time further deter rapid moves. For commoditized tasks (due diligence, routine filings) switching is easier and more frequent, while multi-firm panels—in 2024 commonly 2–4 firms per client—maintain competitive tension.

- Deep knowledge = higher stickiness

- Conflicts/confidentiality increase switching barriers

- Routine work = low switching cost

- Multi-firm panels (2024: typically 2–4) sustain competition

Global capability and speed demands

Buyers now demand seamless cross-border coverage and 24/7 responsiveness, reallocating work after any delay or coverage gap; reliability under time pressure is treated as table-stakes rather than a premium service.

Firms must efficiently coordinate multi-jurisdictional teams and tech-enabled handoffs to retain clients and prevent revenue leakage tied to missed timelines.

- 24/7 responsiveness: client expectation

- Coverage gaps → client reallocations

- Coordination of multi-jurisdictional teams

- Reliability = retention differentiator

PE dry powder and ALSP growth fuel panel RFPs, AFAs and in‑house legal expansion

Clients in PE, tech, life sciences, real estate and financial services use panels/RFPs, raising fee pressure and service demands. Private equity dry powder was about $2.5 trillion in 2024, intensifying KPI/SLA oversight. ALSPs (~$18B market in 2023) and in‑house hiring (40–60% headcount growth in 2023–24 surveys) create credible alternatives and drive AFAs. Multi‑firm panels (2024: typically 2–4) and 24/7 cross‑border needs increase buyer leverage on commoditized work.

| Metric | 2023–24 data |

|---|---|

| PE dry powder | $2.5 trillion (2024) |

| ALSP market | ~$18 billion (2023) |

| In‑house growth | 40–60% headcount rise (2023–24 surveys) |

| Panel size | Typically 2–4 firms (2024) |

What You See Is What You Get

Goodwin Procter Porter's Five Forces Analysis

This preview is the exact Goodwin Procter Porter’s Five Forces analysis you’ll receive upon purchase — no samples, no placeholders. The full document is professionally written, fully formatted, and ready for immediate download and use. What you see here is precisely what will be delivered instantly after payment.

Description

A Must-Have Tool for Decision-Makers

Goodwin Procter’s Porter's Five Forces snapshot highlights competitive intensity, client bargaining power, substitute legal services, supplier influence, and entry barriers shaping firm strategy. It reveals where pressure points and advantages lie. Want the full, consultant-grade force-by-force breakdown with visuals and ratings? Purchase the complete analysis to inform strategy and investments.

Suppliers Bargaining Power

Elite legal talent scarcity

Partners and top associates are the critical inputs and their scarcity raises supplier power; 2024 BigLaw first-year associate pay remained at $215,000, anchoring compensation expectations while lateral premiums and signing bonuses squeeze margins. Retention depends on culture, platform, and deal flow, giving star lawyers leverage, and wage inflation plus cyclical bonus ramps in hot PE and tech sectors amplify short-term cost pressure.

Specialist experts and co-counsel

Specialist expert witnesses, niche regulatory counsel and foreign local counsel are often indispensable in life sciences, fintech and cross-border matters, and in 2024 their scarcity and reputational prominence continued to strengthen bargaining leverage. Switching mid-matter is costly—both financially and procedurally—so firms like Goodwin face lock-in effects that sustain premium rates. Volume discounts and preferred networks can moderate fees but do not eliminate dependence on these scarce suppliers.

Legal tech and e-discovery stack

Platforms for e-discovery, AI review, and knowledge management are concentrated among a few vendors—the global e-discovery market was around $10.5B in 2024 with a ~12% CAGR, giving market leaders outsized pricing power.

Integration costs, complex data security and compliance needs raise switching friction, enabling vendors to push premium features and volume-based pricing.

Counterweights include multi-vendor strategies, Relativity-like alternatives, and growing in-house tooling that trim supplier leverage.

Data, research, and filing services

Legal research, market data, and filing providers are oligopolistic, led by Thomson Reuters, RELX (LexisNexis) and Bloomberg, which together account for over two-thirds of the legal research market in 2024. License bundling and seat-based pricing lock in spend; enterprise contracts improve negotiation leverage but baseline dependence on these vendors persists. High quality and speed needs in litigation and deals limit firms’ ability to cut back.

- Oligopoly: top three >66% share (2024)

- Pricing: seat-based + bundled licenses

- Leverage: better with enterprise deals

- Constraint: quality/speed needs sustain demand

Prime real estate and support services

Prestige locations and Class A offices remain central for client signaling and talent retention, with trophy rents often 10–30% above submarket averages in 2024; landlords in core markets therefore retain pricing power even as hybrid work trims overall space needs. Facilities, court services and translation vendors materially affect the cost base, and long leases—commonly 7–15 years—create rigidity but permit renegotiation at renewal cycles.

- Pricing power: landlords in core markets — premium 10–30%

- Lease length: common 7–15 years

- Cost drivers: facilities, court services, translation vendors

- Hybrid impact: reduced but not eliminated demand

Supplier dominance fuels BigLaw wage and vendor pricing pressure, squeezing margins

Partners, star associates and niche experts wield high supplier power—BigLaw 1L pay anchored at $215,000 in 2024 and retention drives wage pressure; e-discovery vendors lead a ~$10.5B market (2024) with ~12% CAGR, strengthening vendor pricing. Legal research/top-three vendors hold >66% share (2024), while core-office rents remain 10–30% above submarkets, raising fixed costs.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Associate pay | $215,000 | Wage anchor |

| E-discovery | $10.5B, 12% CAGR | Pricing power |

| Legal research | Top3 >66% | Lock-in |

| Office rents | +10–30% | Fixed cost |

What is included in the product

Tailored exclusively for Goodwin Procter, this Porter’s Five Forces analysis uncovers key drivers of competition, customer influence, and market entry risks while evaluating supplier and buyer power, substitutes, and disruptive threats to the firm’s profitability and market position.

A concise Goodwin Procter Porter's Five Forces one-sheet that clarifies competitive pressures, offers adjustable pressure sliders and an instant radar chart for strategic insight, and delivers a clean, slide-ready layout with no macros—easy to swap data, embed in dashboards, or pair with Word reports.

Customers Bargaining Power

Sophisticated corporate procurement

Clients in PE, tech, life sciences, real estate and financial services increasingly use panels and RFPs, driving comparative evaluations that heighten fee pressure and service-level demands. Metrics-driven oversight—KPIs, SLAs and outcome-linked fees—has grown alongside industry capital; private equity dry powder was about $2.5 trillion in 2024, intensifying accountability on efficiency. Consolidation to fewer firms concentrates spend and raises client negotiating leverage.

Alternatives and in-house leverage

ALSPs (~$18B market in 2023) plus Big Four legal arms and expanding in-house teams give clients credible outside options, driving unbundling of tasks to lower‑cost providers while reserving outside counsel for high‑value work. That modularity compresses blended rates and hours and, per 2023–24 surveys showing 40–60% of legal departments growing headcount, forces process innovation and rapid tech adoption to defend share.

Price sensitivity and AFAs

Buyers push Goodwin for capped fees, success fees and subscription models, with 2024 surveys showing rising demand for AFAs as a primary procurement criterion. AFAs shift risk to the firm and reward process discipline and efficiency improvements. Rate increases face client resistance unless tied to demonstrable value or sector scarcity, and budget predictability often trumps open-ended hourly billing.

Switching costs and relationship stickiness

Deep sector knowledge, deal history, and client trust raise switching costs for complex Goodwin Procter matters; conflicts, confidentiality risks, and ramp-up time further deter rapid moves. For commoditized tasks (due diligence, routine filings) switching is easier and more frequent, while multi-firm panels—in 2024 commonly 2–4 firms per client—maintain competitive tension.

- Deep knowledge = higher stickiness

- Conflicts/confidentiality increase switching barriers

- Routine work = low switching cost

- Multi-firm panels (2024: typically 2–4) sustain competition

Global capability and speed demands

Buyers now demand seamless cross-border coverage and 24/7 responsiveness, reallocating work after any delay or coverage gap; reliability under time pressure is treated as table-stakes rather than a premium service.

Firms must efficiently coordinate multi-jurisdictional teams and tech-enabled handoffs to retain clients and prevent revenue leakage tied to missed timelines.

- 24/7 responsiveness: client expectation

- Coverage gaps → client reallocations

- Coordination of multi-jurisdictional teams

- Reliability = retention differentiator

PE dry powder and ALSP growth fuel panel RFPs, AFAs and in‑house legal expansion

Clients in PE, tech, life sciences, real estate and financial services use panels/RFPs, raising fee pressure and service demands. Private equity dry powder was about $2.5 trillion in 2024, intensifying KPI/SLA oversight. ALSPs (~$18B market in 2023) and in‑house hiring (40–60% headcount growth in 2023–24 surveys) create credible alternatives and drive AFAs. Multi‑firm panels (2024: typically 2–4) and 24/7 cross‑border needs increase buyer leverage on commoditized work.

| Metric | 2023–24 data |

|---|---|

| PE dry powder | $2.5 trillion (2024) |

| ALSP market | ~$18 billion (2023) |

| In‑house growth | 40–60% headcount rise (2023–24 surveys) |

| Panel size | Typically 2–4 firms (2024) |

What You See Is What You Get

Goodwin Procter Porter's Five Forces Analysis

This preview is the exact Goodwin Procter Porter’s Five Forces analysis you’ll receive upon purchase — no samples, no placeholders. The full document is professionally written, fully formatted, and ready for immediate download and use. What you see here is precisely what will be delivered instantly after payment.