Greencoat UK Wind Business Model Canvas

Wind Portfolio Business Model Canvas: Value Propositions, Revenue & Scaling

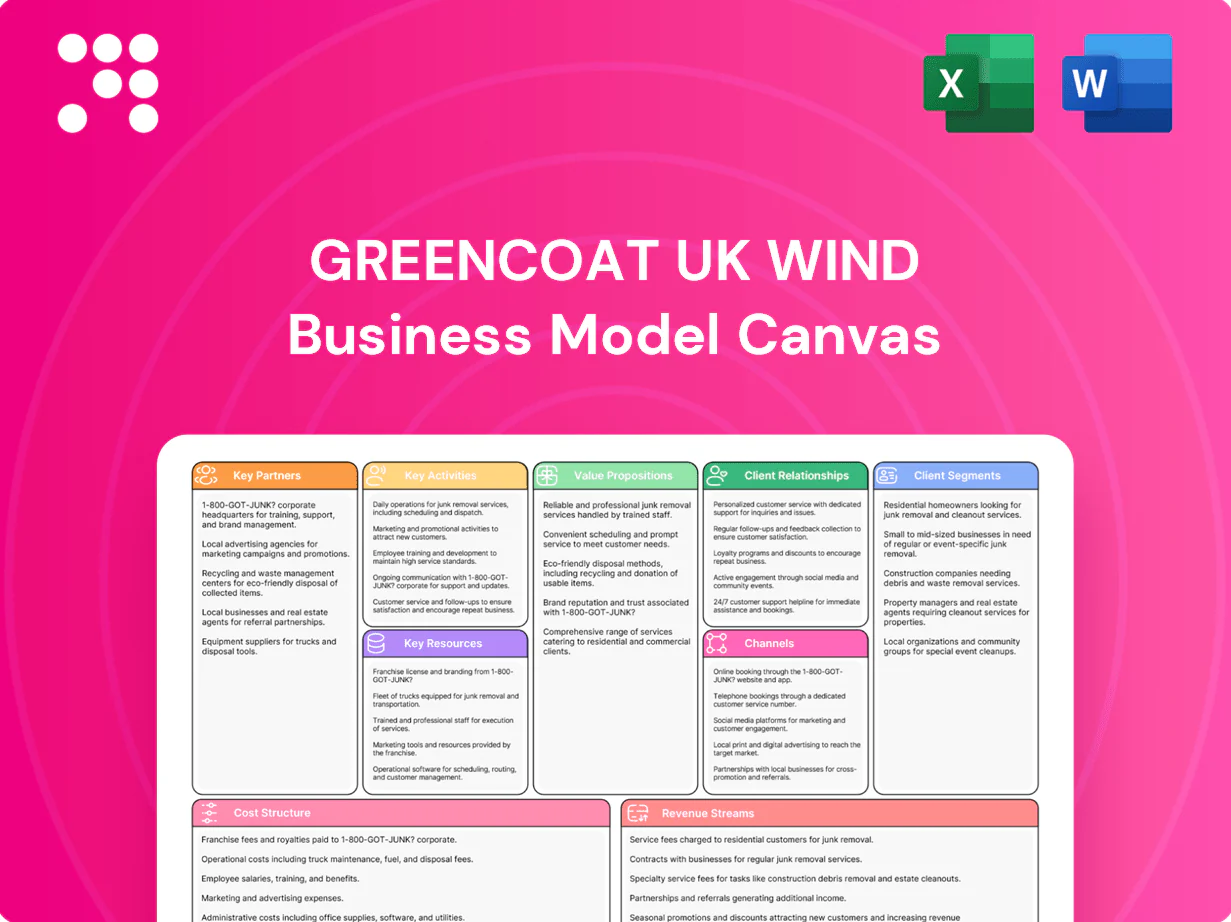

Unlock the full strategic blueprint behind Greencoat UK Wind’s business model with our in-depth Business Model Canvas that maps value propositions, revenue streams, key partnerships and operational levers. Ideal for investors, consultants, and executives, this concise yet comprehensive canvas reveals how the company scales and captures market share. Purchase the complete, editable Word & Excel files to benchmark, plan, and act on proven wind-farm strategies today.

Partnerships

Utility and corporate offtakers

Power purchase agreements with utilities and corporate offtakers underpin long-term cash flows, with common PPA tenors of 10–15 years providing revenue visibility. Fixed-price or floor PPAs materially reduce merchant exposure and help stabilize dividend distributions. Contract lengths are structured to align with typical wind asset lives of 20–25 years and financing schedules. Counterparty credit quality is actively monitored, prioritizing investment-grade counterparties to protect revenue certainty.

OEMs and O&M service providers

OEMs and O&M contractors deliver industry availability of 97–99%, ensuring high plant uptime for Greencoat UK Wind. Long-term service agreements, typically 10–20 years, lock in performance guarantees and predictable O&M costs. Data-driven maintenance can cut unplanned downtime by up to 30% and extend asset life by 5–10 years. Aligned incentives in contracts drive sustained uptime and stronger safety outcomes.

Grid operators and market platforms

Partnerships with National Grid ESO and 14 distribution network operators (DNOs) ensure reliable GB grid access. Balancing and trading partners operate in the Balancing Mechanism and intraday/forward markets to manage dispatch, curtailment and imbalance exposure. Grid-code compliance is maintained via coordinated network upgrades and connection programmes. Market interfaces—Elexon, ICE and Nord Pool—enable efficient route-to-market execution.

Developers, sellers, and co-investors

Pipeline mainly originates from developers and infrastructure owners seeking capital recycling; Greencoat UK Wind had c.£1.5bn AUM in 2024, enabling purchases of operational UK wind farms. Co-investment structures (often alongside institutional partners) enable scale and diversification across sites and technologies. Robust due diligence frameworks standardize technical, commercial and ESG acquisition checks, while seller relationships secure off-market opportunities.

- Pipeline: developers, owners

- Scale: co-investment for diversification

- Due diligence: standardized frameworks

- Off-market: strong seller ties

Banks, insurers, and advisors

Banks and debt providers (typical project finance LTV 60–75%) optimise Greencoat UK Wind capital structure to lower WACC and enhance returns; insurers underwrite construction legacy risks, operational liability and revenue curtailment; legal, technical and ESG advisors support transactions and stewardship; hedging counterparties manage power price and inflation exposures via PPAs and swaps.

- Typical LTV: 60–75%

- Use of PPAs and inflation swaps

- Insurance for construction/operational risks

- Advisors on legal, technical, ESG

UK wind: 10–15yr PPAs, £1.5bn AUM, 97–99% availability

Greencoat UK Wind secures revenue via 10–15yr PPAs with investment-grade offtakers, supported by c.£1.5bn AUM (2024). OEM/O&M partners deliver 97–99% availability under 10–20yr service agreements, cutting unplanned downtime ~30%. Banks provide project debt at 60–75% LTV; insurers and hedging counterparties cover construction, operational and price risks.

| Partnership | Role | Key metric |

|---|---|---|

| PPAs | Revenue certainty | 10–15yr tenors |

| OEM/O&M | Availability | 97–99% |

| Banks/Insurers | Financing & risk transfer | 60–75% LTV |

| Investors | Acquisition pipeline | £1.5bn AUM (2024) |

What is included in the product

A concise, pre-written Business Model Canvas for Greencoat UK Wind outlining customer segments, channels, value propositions, revenue streams, key partners, resources, activities, cost structure and investor-focused metrics. Ideal for presentations and funding discussions, it reflects real-world wind-asset operations, competitive advantages and SWOT-linked insights to support strategic and financial decision-making.

High-level view of Greencoat UK Wind’s business model with editable cells, simplifying asset, revenue and stakeholder mapping for rapid clarity. Perfect for comparing projects, saving hours of formatting and creating board-ready summaries.

Activities

Acquiring operational wind assets

Identify, evaluate and transact on UK onshore and offshore wind farms—targeting operational assets with proven generation that contribute to GB supply (wind supplied about 27% of UK electricity in 2024). Structure acquisitions to preserve accretion to dividends and maintain yield accretion per share. Execute rapid integration into portfolio oversight for operational continuity and centralized asset management.

Portfolio and performance management

Monitor production, availability (targeting c.97%) and curtailment in real time via SCADA to minimise estimated industry curtailment of c.2–3%; optimise O&M schedules and contract terms to reduce lifecycle costs by 5–10%; implement performance upgrades and repowering where IRR and LCOE improvements justify (repowering uplifts often c.30%); benchmark KPIs (AEP/MW, availability, OPEX/MWh) across sites to drive continuous improvement.

Revenue contracting and hedging

Negotiate PPAs, CfDs and floor contracts to lock predictable cash flows across Greencoat UK Wind's c.1.8GW portfolio, prioritising multi-year tenor to match dividend targets and debt maturities. Layer OTC and exchange hedges to manage merchant, shape and imbalance risk while targeting hedge coverage through peak-price months. Maintain counterparty diversification across banks and utilities to reduce concentration risk.

Capital allocation and financing

Greencoat UK Wind raises equity and debt to fund accretive acquisitions and refinance maturing facilities, maintaining disciplined leverage within its stated policy range of around 30–40% net debt to portfolio value (2024). The company recycles capital through selective disposals to preserve portfolio quality and align deployment with inflation‑linked, long‑term returns, targeting stable distributions (2024 dividend yield ~6%).

- Equity and debt raises: fund acquisitions/refinancing (2024)

- Leverage: ~30–40% net debt/portfolio value (policy, 2024)

- Capital recycling: selective disposals

- Focus: accretive, inflation‑linked returns; ~6% yield (2024)

Reporting, governance, and ESG stewardship

Greencoat UK Wind (LSE: GCW) publishes transparent NAV, generation and dividend reporting on a quarterly basis, with market disclosures and investor presentations to support dividend guidance.

Governance ensures compliance with UK Listing rules, the UK Corporate Governance Code and auditor oversight, and aligns sustainability reporting with TCFD/climate-risk and resilience expectations.

- NAV & reporting: quarterly disclosures

- Compliance: UK Listing, Corporate Governance Code, external audit

- ESG focus: biodiversity, community benefits, safety

- Climate: TCFD-aligned risk/asset resilience

Acquire UK 1.8GW wind, lock cashflows, target ~6% yield

Acquire and integrate UK onshore/offshore wind assets (GCW ~1.8GW, wind ~27% of UK power in 2024) to preserve dividend accretion.

Operate via SCADA to target c.97% availability, minimise c.2–3% curtailment, optimise O&M and repower where IRR/LCOE justify.

Lock cashflows with PPAs/CfDs, hedge merchant risk, maintain leverage ~30–40% and target ~6% dividend yield (2024).

| Metric | 2024 |

|---|---|

| Portfolio | 1.8GW |

| Availability | c.97% |

| Curtailment | 2–3% |

| Leverage | 30–40% |

| Yield | ~6% |

Full Version Awaits

Business Model Canvas

The Greencoat UK Wind Business Model Canvas you’re previewing is the actual deliverable, not a mockup or teaser. It’s the same professionally structured document you’ll receive after purchase, with all content and pages included. Upon checkout you’ll instantly get this exact file, ready to edit, present, or share.

Wind Portfolio Business Model Canvas: Value Propositions, Revenue & Scaling

Unlock the full strategic blueprint behind Greencoat UK Wind’s business model with our in-depth Business Model Canvas that maps value propositions, revenue streams, key partnerships and operational levers. Ideal for investors, consultants, and executives, this concise yet comprehensive canvas reveals how the company scales and captures market share. Purchase the complete, editable Word & Excel files to benchmark, plan, and act on proven wind-farm strategies today.

Partnerships

Utility and corporate offtakers

Power purchase agreements with utilities and corporate offtakers underpin long-term cash flows, with common PPA tenors of 10–15 years providing revenue visibility. Fixed-price or floor PPAs materially reduce merchant exposure and help stabilize dividend distributions. Contract lengths are structured to align with typical wind asset lives of 20–25 years and financing schedules. Counterparty credit quality is actively monitored, prioritizing investment-grade counterparties to protect revenue certainty.

OEMs and O&M service providers

OEMs and O&M contractors deliver industry availability of 97–99%, ensuring high plant uptime for Greencoat UK Wind. Long-term service agreements, typically 10–20 years, lock in performance guarantees and predictable O&M costs. Data-driven maintenance can cut unplanned downtime by up to 30% and extend asset life by 5–10 years. Aligned incentives in contracts drive sustained uptime and stronger safety outcomes.

Grid operators and market platforms

Partnerships with National Grid ESO and 14 distribution network operators (DNOs) ensure reliable GB grid access. Balancing and trading partners operate in the Balancing Mechanism and intraday/forward markets to manage dispatch, curtailment and imbalance exposure. Grid-code compliance is maintained via coordinated network upgrades and connection programmes. Market interfaces—Elexon, ICE and Nord Pool—enable efficient route-to-market execution.

Developers, sellers, and co-investors

Pipeline mainly originates from developers and infrastructure owners seeking capital recycling; Greencoat UK Wind had c.£1.5bn AUM in 2024, enabling purchases of operational UK wind farms. Co-investment structures (often alongside institutional partners) enable scale and diversification across sites and technologies. Robust due diligence frameworks standardize technical, commercial and ESG acquisition checks, while seller relationships secure off-market opportunities.

- Pipeline: developers, owners

- Scale: co-investment for diversification

- Due diligence: standardized frameworks

- Off-market: strong seller ties

Banks, insurers, and advisors

Banks and debt providers (typical project finance LTV 60–75%) optimise Greencoat UK Wind capital structure to lower WACC and enhance returns; insurers underwrite construction legacy risks, operational liability and revenue curtailment; legal, technical and ESG advisors support transactions and stewardship; hedging counterparties manage power price and inflation exposures via PPAs and swaps.

- Typical LTV: 60–75%

- Use of PPAs and inflation swaps

- Insurance for construction/operational risks

- Advisors on legal, technical, ESG

UK wind: 10–15yr PPAs, £1.5bn AUM, 97–99% availability

Greencoat UK Wind secures revenue via 10–15yr PPAs with investment-grade offtakers, supported by c.£1.5bn AUM (2024). OEM/O&M partners deliver 97–99% availability under 10–20yr service agreements, cutting unplanned downtime ~30%. Banks provide project debt at 60–75% LTV; insurers and hedging counterparties cover construction, operational and price risks.

| Partnership | Role | Key metric |

|---|---|---|

| PPAs | Revenue certainty | 10–15yr tenors |

| OEM/O&M | Availability | 97–99% |

| Banks/Insurers | Financing & risk transfer | 60–75% LTV |

| Investors | Acquisition pipeline | £1.5bn AUM (2024) |

What is included in the product

A concise, pre-written Business Model Canvas for Greencoat UK Wind outlining customer segments, channels, value propositions, revenue streams, key partners, resources, activities, cost structure and investor-focused metrics. Ideal for presentations and funding discussions, it reflects real-world wind-asset operations, competitive advantages and SWOT-linked insights to support strategic and financial decision-making.

High-level view of Greencoat UK Wind’s business model with editable cells, simplifying asset, revenue and stakeholder mapping for rapid clarity. Perfect for comparing projects, saving hours of formatting and creating board-ready summaries.

Activities

Acquiring operational wind assets

Identify, evaluate and transact on UK onshore and offshore wind farms—targeting operational assets with proven generation that contribute to GB supply (wind supplied about 27% of UK electricity in 2024). Structure acquisitions to preserve accretion to dividends and maintain yield accretion per share. Execute rapid integration into portfolio oversight for operational continuity and centralized asset management.

Portfolio and performance management

Monitor production, availability (targeting c.97%) and curtailment in real time via SCADA to minimise estimated industry curtailment of c.2–3%; optimise O&M schedules and contract terms to reduce lifecycle costs by 5–10%; implement performance upgrades and repowering where IRR and LCOE improvements justify (repowering uplifts often c.30%); benchmark KPIs (AEP/MW, availability, OPEX/MWh) across sites to drive continuous improvement.

Revenue contracting and hedging

Negotiate PPAs, CfDs and floor contracts to lock predictable cash flows across Greencoat UK Wind's c.1.8GW portfolio, prioritising multi-year tenor to match dividend targets and debt maturities. Layer OTC and exchange hedges to manage merchant, shape and imbalance risk while targeting hedge coverage through peak-price months. Maintain counterparty diversification across banks and utilities to reduce concentration risk.

Capital allocation and financing

Greencoat UK Wind raises equity and debt to fund accretive acquisitions and refinance maturing facilities, maintaining disciplined leverage within its stated policy range of around 30–40% net debt to portfolio value (2024). The company recycles capital through selective disposals to preserve portfolio quality and align deployment with inflation‑linked, long‑term returns, targeting stable distributions (2024 dividend yield ~6%).

- Equity and debt raises: fund acquisitions/refinancing (2024)

- Leverage: ~30–40% net debt/portfolio value (policy, 2024)

- Capital recycling: selective disposals

- Focus: accretive, inflation‑linked returns; ~6% yield (2024)

Reporting, governance, and ESG stewardship

Greencoat UK Wind (LSE: GCW) publishes transparent NAV, generation and dividend reporting on a quarterly basis, with market disclosures and investor presentations to support dividend guidance.

Governance ensures compliance with UK Listing rules, the UK Corporate Governance Code and auditor oversight, and aligns sustainability reporting with TCFD/climate-risk and resilience expectations.

- NAV & reporting: quarterly disclosures

- Compliance: UK Listing, Corporate Governance Code, external audit

- ESG focus: biodiversity, community benefits, safety

- Climate: TCFD-aligned risk/asset resilience

Acquire UK 1.8GW wind, lock cashflows, target ~6% yield

Acquire and integrate UK onshore/offshore wind assets (GCW ~1.8GW, wind ~27% of UK power in 2024) to preserve dividend accretion.

Operate via SCADA to target c.97% availability, minimise c.2–3% curtailment, optimise O&M and repower where IRR/LCOE justify.

Lock cashflows with PPAs/CfDs, hedge merchant risk, maintain leverage ~30–40% and target ~6% dividend yield (2024).

| Metric | 2024 |

|---|---|

| Portfolio | 1.8GW |

| Availability | c.97% |

| Curtailment | 2–3% |

| Leverage | 30–40% |

| Yield | ~6% |

Full Version Awaits

Business Model Canvas

The Greencoat UK Wind Business Model Canvas you’re previewing is the actual deliverable, not a mockup or teaser. It’s the same professionally structured document you’ll receive after purchase, with all content and pages included. Upon checkout you’ll instantly get this exact file, ready to edit, present, or share.

Description

Wind Portfolio Business Model Canvas: Value Propositions, Revenue & Scaling

Unlock the full strategic blueprint behind Greencoat UK Wind’s business model with our in-depth Business Model Canvas that maps value propositions, revenue streams, key partnerships and operational levers. Ideal for investors, consultants, and executives, this concise yet comprehensive canvas reveals how the company scales and captures market share. Purchase the complete, editable Word & Excel files to benchmark, plan, and act on proven wind-farm strategies today.

Partnerships

Utility and corporate offtakers

Power purchase agreements with utilities and corporate offtakers underpin long-term cash flows, with common PPA tenors of 10–15 years providing revenue visibility. Fixed-price or floor PPAs materially reduce merchant exposure and help stabilize dividend distributions. Contract lengths are structured to align with typical wind asset lives of 20–25 years and financing schedules. Counterparty credit quality is actively monitored, prioritizing investment-grade counterparties to protect revenue certainty.

OEMs and O&M service providers

OEMs and O&M contractors deliver industry availability of 97–99%, ensuring high plant uptime for Greencoat UK Wind. Long-term service agreements, typically 10–20 years, lock in performance guarantees and predictable O&M costs. Data-driven maintenance can cut unplanned downtime by up to 30% and extend asset life by 5–10 years. Aligned incentives in contracts drive sustained uptime and stronger safety outcomes.

Grid operators and market platforms

Partnerships with National Grid ESO and 14 distribution network operators (DNOs) ensure reliable GB grid access. Balancing and trading partners operate in the Balancing Mechanism and intraday/forward markets to manage dispatch, curtailment and imbalance exposure. Grid-code compliance is maintained via coordinated network upgrades and connection programmes. Market interfaces—Elexon, ICE and Nord Pool—enable efficient route-to-market execution.

Developers, sellers, and co-investors

Pipeline mainly originates from developers and infrastructure owners seeking capital recycling; Greencoat UK Wind had c.£1.5bn AUM in 2024, enabling purchases of operational UK wind farms. Co-investment structures (often alongside institutional partners) enable scale and diversification across sites and technologies. Robust due diligence frameworks standardize technical, commercial and ESG acquisition checks, while seller relationships secure off-market opportunities.

- Pipeline: developers, owners

- Scale: co-investment for diversification

- Due diligence: standardized frameworks

- Off-market: strong seller ties

Banks, insurers, and advisors

Banks and debt providers (typical project finance LTV 60–75%) optimise Greencoat UK Wind capital structure to lower WACC and enhance returns; insurers underwrite construction legacy risks, operational liability and revenue curtailment; legal, technical and ESG advisors support transactions and stewardship; hedging counterparties manage power price and inflation exposures via PPAs and swaps.

- Typical LTV: 60–75%

- Use of PPAs and inflation swaps

- Insurance for construction/operational risks

- Advisors on legal, technical, ESG

UK wind: 10–15yr PPAs, £1.5bn AUM, 97–99% availability

Greencoat UK Wind secures revenue via 10–15yr PPAs with investment-grade offtakers, supported by c.£1.5bn AUM (2024). OEM/O&M partners deliver 97–99% availability under 10–20yr service agreements, cutting unplanned downtime ~30%. Banks provide project debt at 60–75% LTV; insurers and hedging counterparties cover construction, operational and price risks.

| Partnership | Role | Key metric |

|---|---|---|

| PPAs | Revenue certainty | 10–15yr tenors |

| OEM/O&M | Availability | 97–99% |

| Banks/Insurers | Financing & risk transfer | 60–75% LTV |

| Investors | Acquisition pipeline | £1.5bn AUM (2024) |

What is included in the product

A concise, pre-written Business Model Canvas for Greencoat UK Wind outlining customer segments, channels, value propositions, revenue streams, key partners, resources, activities, cost structure and investor-focused metrics. Ideal for presentations and funding discussions, it reflects real-world wind-asset operations, competitive advantages and SWOT-linked insights to support strategic and financial decision-making.

High-level view of Greencoat UK Wind’s business model with editable cells, simplifying asset, revenue and stakeholder mapping for rapid clarity. Perfect for comparing projects, saving hours of formatting and creating board-ready summaries.

Activities

Acquiring operational wind assets

Identify, evaluate and transact on UK onshore and offshore wind farms—targeting operational assets with proven generation that contribute to GB supply (wind supplied about 27% of UK electricity in 2024). Structure acquisitions to preserve accretion to dividends and maintain yield accretion per share. Execute rapid integration into portfolio oversight for operational continuity and centralized asset management.

Portfolio and performance management

Monitor production, availability (targeting c.97%) and curtailment in real time via SCADA to minimise estimated industry curtailment of c.2–3%; optimise O&M schedules and contract terms to reduce lifecycle costs by 5–10%; implement performance upgrades and repowering where IRR and LCOE improvements justify (repowering uplifts often c.30%); benchmark KPIs (AEP/MW, availability, OPEX/MWh) across sites to drive continuous improvement.

Revenue contracting and hedging

Negotiate PPAs, CfDs and floor contracts to lock predictable cash flows across Greencoat UK Wind's c.1.8GW portfolio, prioritising multi-year tenor to match dividend targets and debt maturities. Layer OTC and exchange hedges to manage merchant, shape and imbalance risk while targeting hedge coverage through peak-price months. Maintain counterparty diversification across banks and utilities to reduce concentration risk.

Capital allocation and financing

Greencoat UK Wind raises equity and debt to fund accretive acquisitions and refinance maturing facilities, maintaining disciplined leverage within its stated policy range of around 30–40% net debt to portfolio value (2024). The company recycles capital through selective disposals to preserve portfolio quality and align deployment with inflation‑linked, long‑term returns, targeting stable distributions (2024 dividend yield ~6%).

- Equity and debt raises: fund acquisitions/refinancing (2024)

- Leverage: ~30–40% net debt/portfolio value (policy, 2024)

- Capital recycling: selective disposals

- Focus: accretive, inflation‑linked returns; ~6% yield (2024)

Reporting, governance, and ESG stewardship

Greencoat UK Wind (LSE: GCW) publishes transparent NAV, generation and dividend reporting on a quarterly basis, with market disclosures and investor presentations to support dividend guidance.

Governance ensures compliance with UK Listing rules, the UK Corporate Governance Code and auditor oversight, and aligns sustainability reporting with TCFD/climate-risk and resilience expectations.

- NAV & reporting: quarterly disclosures

- Compliance: UK Listing, Corporate Governance Code, external audit

- ESG focus: biodiversity, community benefits, safety

- Climate: TCFD-aligned risk/asset resilience

Acquire UK 1.8GW wind, lock cashflows, target ~6% yield

Acquire and integrate UK onshore/offshore wind assets (GCW ~1.8GW, wind ~27% of UK power in 2024) to preserve dividend accretion.

Operate via SCADA to target c.97% availability, minimise c.2–3% curtailment, optimise O&M and repower where IRR/LCOE justify.

Lock cashflows with PPAs/CfDs, hedge merchant risk, maintain leverage ~30–40% and target ~6% dividend yield (2024).

| Metric | 2024 |

|---|---|

| Portfolio | 1.8GW |

| Availability | c.97% |

| Curtailment | 2–3% |

| Leverage | 30–40% |

| Yield | ~6% |

Full Version Awaits

Business Model Canvas

The Greencoat UK Wind Business Model Canvas you’re previewing is the actual deliverable, not a mockup or teaser. It’s the same professionally structured document you’ll receive after purchase, with all content and pages included. Upon checkout you’ll instantly get this exact file, ready to edit, present, or share.