Greencoat UK Wind Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

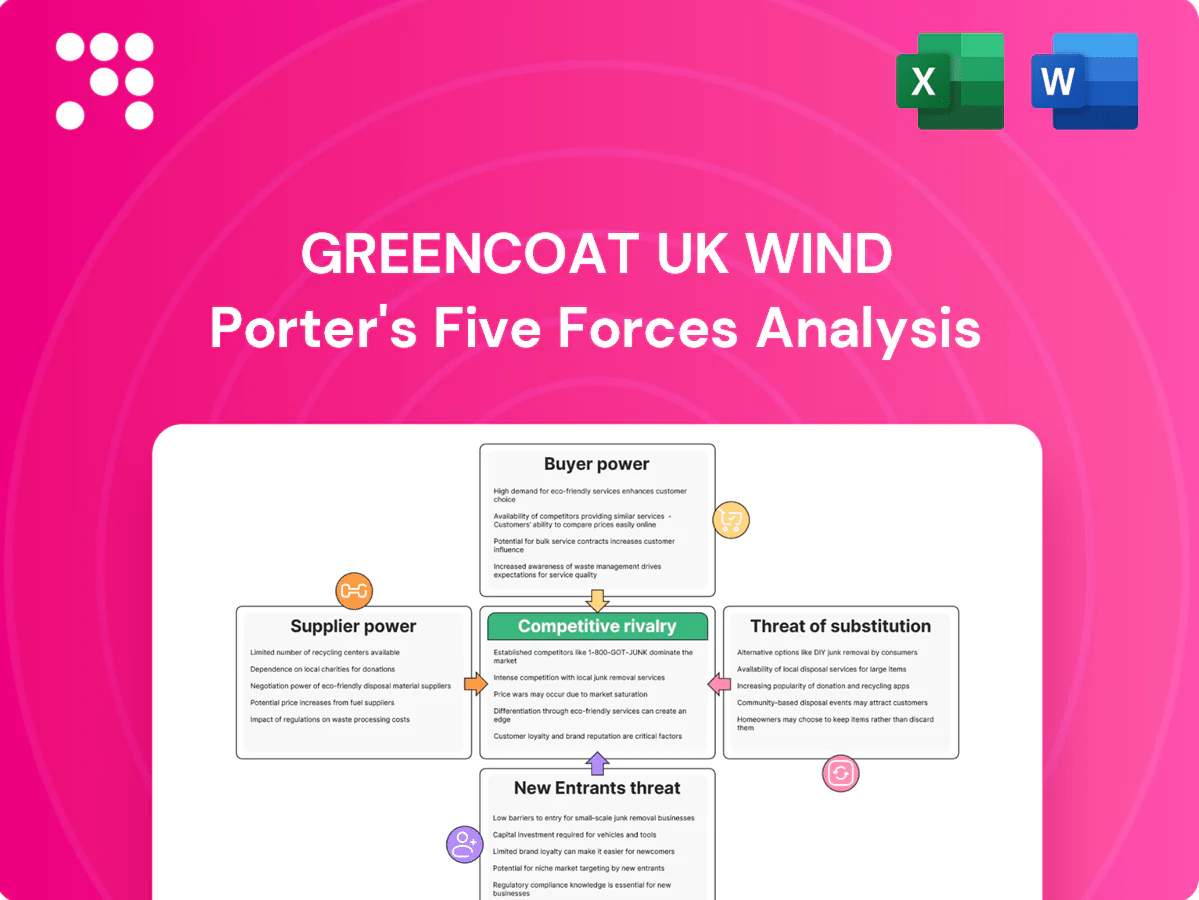

Greencoat UK Wind faces moderate buyer power, concentrated supplier influence, limited substitutes, regulatory tailwinds, and high capital barriers shaping its competitive dynamics. This snapshot highlights the principal pressures and strategic levers influencing returns. Ready to move beyond the basics? Get the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated turbine OEMs

Wind farms depend heavily on a few OEMs—Vestas, Siemens Gamesa and peers—whose concentrated share (top five OEMs supply roughly 75% of turbines globally in 2023–24) limits alternatives, raising switching costs and extending lead times. That concentration gives OEMs leverage on spares, upgrades and service pricing. Greencoat counters risk with diversified asset mix and long-term service agreements to lock capacity and predictable terms.

Specialized O&M service providers

Operational availability for Greencoat UK Wind hinges on specialist O&M contractors, with typical availability targets around 95–98% in UK wind portfolios. Performance-linked contracts align incentives but do not remove supplier dependency; outages still concentrate risk. O&M represents roughly 20% of operating costs and 2024 labor scarcity has pushed service rates up, encouraging multi-supplier frameworks to cut single-provider exposure.

Grid connection and curtailment exposure

Distribution and transmission operators control connections and outages; the GB connection queue stood at roughly 100 GW in 2024, concentrating negotiating power. Constraints and curtailment can cut generation in congested zones—estimates suggest up to 5% lost output in highly constrained areas—effectively boosting supplier-like power. Connection upgrades are typically procured on monopoly terms, so proactive grid engagement and geographic diversification reduce exposure.

Landowners and lease terms

Site leases are long-dated but periodically renegotiated, giving landowners renewal leverage where suitable sites are scarce; indexed rent escalators pass part of inflation into operating costs, tightening margins during high inflation periods; Greencoat limits landlord concentration by spreading assets across its portfolio to reduce single-landlord exposure.

- Long-dated leases with renegotiation

- Scarcity elevates landlord renewal leverage

- Indexed escalators transfer inflation risk

- Portfolio spread limits single-landlord concentration

Insurance and specialist services

Coverage for mechanical breakdown, business interruption and liability is essential; hard insurance markets lifted premiums and deductibles (Marsh Global Insurance Market Index Q1 2024: average rate change +8%), giving underwriters greater leverage. Few underwriters fully understand wind risks, increasing supplier bargaining power, though robust risk engineering and a clean claims history can materially temper pricing.

Supplier leverage: Top 5 OEMs ~75%, GB queue ~100 GW

Wind OEM concentration (top five ~75% in 2023–24) and specialist O&M (95–98% availability targets; ~20% of operating costs) give suppliers pricing and outage leverage. Grid constraints (GB connection queue ~100 GW in 2024; curtailment ~up to 5% in hotspots) and long-dated indexed leases increase landlord bargaining power. Insurance hardening (Marsh Q1 2024 +8% avg rates) further tightens supplier influence; diversification and long-term contracts mitigate.

| Metric | 2024 value | Impact |

|---|---|---|

| OEM concentration | Top 5 ~75% | High switching cost |

| O&M | ~20% costs; 95–98% target | Operational dependency |

| GB queue | ~100 GW | Curtailment risk |

| Insurance | +8% avg rates (Marsh Q1 2024) | Higher premiums |

| Leases | Indexed escalators | Inflation pass-through |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks for Greencoat UK Wind, assessing supplier power, buyer leverage, threat of new entrants and substitutes, and intra-industry rivalry. Includes strategic commentary on regulatory and subsidy dynamics shaping pricing, profitability and barriers protecting incumbents.

Greencoat UK Wind Porter's Five Forces provides a clear one-sheet summary that distills competitive pressures on UK wind assets for quick, confident decisions. Customizable scores and an instant spider chart let you model scenarios, communicate risk, and drop visuals directly into decks or reports.

Customers Bargaining Power

Offtaker concentration

Utilities and large traders dominate PPAs, concentrating buying power and driving standardized contracts with creditworthy counterparties that compress margins; in 2024 long‑term fixed‑price PPAs commonly span 10–15 years, providing revenue visibility for owners. Greencoat can mitigate concentration risk by diversifying offtakers across multiple contracts and tenors to smooth counterparty exposure.

Government-backed pricing schemes

CfDs and legacy ROCs reduce revenue volatility for Greencoat UK Wind while capping upside by fixing or floor-pricing payments; the ROC scheme closed to new capacity in 2017. Policy frameworks set terms via auctioned strike prices and regulatory rules rather than bilateral negotiation, lowering classic buyer power but imposing pricing discipline. Balancing CfD/ROC-backed assets with merchant exposure manages market upside and wholesale risk amid the UK 50 GW offshore target by 2030.

Merchant exposure to wholesale markets

Unhedged output sells into volatile spot markets with no single buyer, making Greencoat UK Wind a price-taker that has limited influence on contract terms. By 2024 Greencoat had hedged and staggered PPAs covering roughly 60% of near-term generation, materially cutting buyer leverage. Market liquidity in UK wholesale power allows execution of volumes but does not translate into pricing power for sellers.

Switching costs and contract tenors

Long-dated PPAs, typically 10–15 years in 2024, limit offtaker churn and materially reduce mid-tenor buyer renegotiation leverage for Greencoat UK Wind, while renewal windows remain the main channel for buyer power if market prices soften. Credit terms and collateral are usually fixed at origination, constraining mid-contract leverage, and strong asset availability and generation outperformance improves the seller negotiating stance.

- Tenor: 10–15 years (2024)

- Offtaker churn: low mid-term

- Renewals: key vulnerability

- Origination: credit/collateral set

- Performance: raises seller leverage

Corporate PPA alternatives

Rising corporate demand for renewables in 2024 (c.3 GW of UK corporate PPAs signed) expands buyer options and ramps competition among generators, pushing discounts as buyers prioritize price and ESG attributes and pressuring merchant returns.

Longer tenors and stronger corporate credit can offset lower tariffs; optionality across utility and corporate PPAs reduces dependence on any single channel.

- buyer options

- price pressure

- ESG premium

- tenor/credit offset

- utility vs corporate optionality

Buyers dominate 10-15y PPAs; policy/credit limit renegotiation — ~60% hedged

Buyers (utilities, large traders, corporates) hold concentrated power in long‑dated PPAs (10–15y) but policy CfDs/ROCs and strong origination credit constrain mid‑term renegotiation; Greencoat had ~60% hedged in 2024, cutting buyer leverage. Corporate PPAs (~3 GW UK 2024) increase seller competition but higher corporate credit/tenor offsets lower tariffs.

| Metric | 2024 |

|---|---|

| Typical PPA tenor | 10–15y |

| Hedged generation | ~60% |

| UK corporate PPAs | ~3 GW |

Full Version Awaits

Greencoat UK Wind Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Greencoat UK Wind you'll receive immediately after purchase—no surprises or placeholders. The document examines supplier power, buyer power, competitive rivalry, threat of entrants, and threat of substitutes with sector-specific evidence and valuation implications. It's fully formatted and ready for download the moment you buy. You're looking at the actual deliverable.

A Must-Have Tool for Decision-Makers

Greencoat UK Wind faces moderate buyer power, concentrated supplier influence, limited substitutes, regulatory tailwinds, and high capital barriers shaping its competitive dynamics. This snapshot highlights the principal pressures and strategic levers influencing returns. Ready to move beyond the basics? Get the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated turbine OEMs

Wind farms depend heavily on a few OEMs—Vestas, Siemens Gamesa and peers—whose concentrated share (top five OEMs supply roughly 75% of turbines globally in 2023–24) limits alternatives, raising switching costs and extending lead times. That concentration gives OEMs leverage on spares, upgrades and service pricing. Greencoat counters risk with diversified asset mix and long-term service agreements to lock capacity and predictable terms.

Specialized O&M service providers

Operational availability for Greencoat UK Wind hinges on specialist O&M contractors, with typical availability targets around 95–98% in UK wind portfolios. Performance-linked contracts align incentives but do not remove supplier dependency; outages still concentrate risk. O&M represents roughly 20% of operating costs and 2024 labor scarcity has pushed service rates up, encouraging multi-supplier frameworks to cut single-provider exposure.

Grid connection and curtailment exposure

Distribution and transmission operators control connections and outages; the GB connection queue stood at roughly 100 GW in 2024, concentrating negotiating power. Constraints and curtailment can cut generation in congested zones—estimates suggest up to 5% lost output in highly constrained areas—effectively boosting supplier-like power. Connection upgrades are typically procured on monopoly terms, so proactive grid engagement and geographic diversification reduce exposure.

Landowners and lease terms

Site leases are long-dated but periodically renegotiated, giving landowners renewal leverage where suitable sites are scarce; indexed rent escalators pass part of inflation into operating costs, tightening margins during high inflation periods; Greencoat limits landlord concentration by spreading assets across its portfolio to reduce single-landlord exposure.

- Long-dated leases with renegotiation

- Scarcity elevates landlord renewal leverage

- Indexed escalators transfer inflation risk

- Portfolio spread limits single-landlord concentration

Insurance and specialist services

Coverage for mechanical breakdown, business interruption and liability is essential; hard insurance markets lifted premiums and deductibles (Marsh Global Insurance Market Index Q1 2024: average rate change +8%), giving underwriters greater leverage. Few underwriters fully understand wind risks, increasing supplier bargaining power, though robust risk engineering and a clean claims history can materially temper pricing.

Supplier leverage: Top 5 OEMs ~75%, GB queue ~100 GW

Wind OEM concentration (top five ~75% in 2023–24) and specialist O&M (95–98% availability targets; ~20% of operating costs) give suppliers pricing and outage leverage. Grid constraints (GB connection queue ~100 GW in 2024; curtailment ~up to 5% in hotspots) and long-dated indexed leases increase landlord bargaining power. Insurance hardening (Marsh Q1 2024 +8% avg rates) further tightens supplier influence; diversification and long-term contracts mitigate.

| Metric | 2024 value | Impact |

|---|---|---|

| OEM concentration | Top 5 ~75% | High switching cost |

| O&M | ~20% costs; 95–98% target | Operational dependency |

| GB queue | ~100 GW | Curtailment risk |

| Insurance | +8% avg rates (Marsh Q1 2024) | Higher premiums |

| Leases | Indexed escalators | Inflation pass-through |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks for Greencoat UK Wind, assessing supplier power, buyer leverage, threat of new entrants and substitutes, and intra-industry rivalry. Includes strategic commentary on regulatory and subsidy dynamics shaping pricing, profitability and barriers protecting incumbents.

Greencoat UK Wind Porter's Five Forces provides a clear one-sheet summary that distills competitive pressures on UK wind assets for quick, confident decisions. Customizable scores and an instant spider chart let you model scenarios, communicate risk, and drop visuals directly into decks or reports.

Customers Bargaining Power

Offtaker concentration

Utilities and large traders dominate PPAs, concentrating buying power and driving standardized contracts with creditworthy counterparties that compress margins; in 2024 long‑term fixed‑price PPAs commonly span 10–15 years, providing revenue visibility for owners. Greencoat can mitigate concentration risk by diversifying offtakers across multiple contracts and tenors to smooth counterparty exposure.

Government-backed pricing schemes

CfDs and legacy ROCs reduce revenue volatility for Greencoat UK Wind while capping upside by fixing or floor-pricing payments; the ROC scheme closed to new capacity in 2017. Policy frameworks set terms via auctioned strike prices and regulatory rules rather than bilateral negotiation, lowering classic buyer power but imposing pricing discipline. Balancing CfD/ROC-backed assets with merchant exposure manages market upside and wholesale risk amid the UK 50 GW offshore target by 2030.

Merchant exposure to wholesale markets

Unhedged output sells into volatile spot markets with no single buyer, making Greencoat UK Wind a price-taker that has limited influence on contract terms. By 2024 Greencoat had hedged and staggered PPAs covering roughly 60% of near-term generation, materially cutting buyer leverage. Market liquidity in UK wholesale power allows execution of volumes but does not translate into pricing power for sellers.

Switching costs and contract tenors

Long-dated PPAs, typically 10–15 years in 2024, limit offtaker churn and materially reduce mid-tenor buyer renegotiation leverage for Greencoat UK Wind, while renewal windows remain the main channel for buyer power if market prices soften. Credit terms and collateral are usually fixed at origination, constraining mid-contract leverage, and strong asset availability and generation outperformance improves the seller negotiating stance.

- Tenor: 10–15 years (2024)

- Offtaker churn: low mid-term

- Renewals: key vulnerability

- Origination: credit/collateral set

- Performance: raises seller leverage

Corporate PPA alternatives

Rising corporate demand for renewables in 2024 (c.3 GW of UK corporate PPAs signed) expands buyer options and ramps competition among generators, pushing discounts as buyers prioritize price and ESG attributes and pressuring merchant returns.

Longer tenors and stronger corporate credit can offset lower tariffs; optionality across utility and corporate PPAs reduces dependence on any single channel.

- buyer options

- price pressure

- ESG premium

- tenor/credit offset

- utility vs corporate optionality

Buyers dominate 10-15y PPAs; policy/credit limit renegotiation — ~60% hedged

Buyers (utilities, large traders, corporates) hold concentrated power in long‑dated PPAs (10–15y) but policy CfDs/ROCs and strong origination credit constrain mid‑term renegotiation; Greencoat had ~60% hedged in 2024, cutting buyer leverage. Corporate PPAs (~3 GW UK 2024) increase seller competition but higher corporate credit/tenor offsets lower tariffs.

| Metric | 2024 |

|---|---|

| Typical PPA tenor | 10–15y |

| Hedged generation | ~60% |

| UK corporate PPAs | ~3 GW |

Full Version Awaits

Greencoat UK Wind Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Greencoat UK Wind you'll receive immediately after purchase—no surprises or placeholders. The document examines supplier power, buyer power, competitive rivalry, threat of entrants, and threat of substitutes with sector-specific evidence and valuation implications. It's fully formatted and ready for download the moment you buy. You're looking at the actual deliverable.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Greencoat UK Wind faces moderate buyer power, concentrated supplier influence, limited substitutes, regulatory tailwinds, and high capital barriers shaping its competitive dynamics. This snapshot highlights the principal pressures and strategic levers influencing returns. Ready to move beyond the basics? Get the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated turbine OEMs

Wind farms depend heavily on a few OEMs—Vestas, Siemens Gamesa and peers—whose concentrated share (top five OEMs supply roughly 75% of turbines globally in 2023–24) limits alternatives, raising switching costs and extending lead times. That concentration gives OEMs leverage on spares, upgrades and service pricing. Greencoat counters risk with diversified asset mix and long-term service agreements to lock capacity and predictable terms.

Specialized O&M service providers

Operational availability for Greencoat UK Wind hinges on specialist O&M contractors, with typical availability targets around 95–98% in UK wind portfolios. Performance-linked contracts align incentives but do not remove supplier dependency; outages still concentrate risk. O&M represents roughly 20% of operating costs and 2024 labor scarcity has pushed service rates up, encouraging multi-supplier frameworks to cut single-provider exposure.

Grid connection and curtailment exposure

Distribution and transmission operators control connections and outages; the GB connection queue stood at roughly 100 GW in 2024, concentrating negotiating power. Constraints and curtailment can cut generation in congested zones—estimates suggest up to 5% lost output in highly constrained areas—effectively boosting supplier-like power. Connection upgrades are typically procured on monopoly terms, so proactive grid engagement and geographic diversification reduce exposure.

Landowners and lease terms

Site leases are long-dated but periodically renegotiated, giving landowners renewal leverage where suitable sites are scarce; indexed rent escalators pass part of inflation into operating costs, tightening margins during high inflation periods; Greencoat limits landlord concentration by spreading assets across its portfolio to reduce single-landlord exposure.

- Long-dated leases with renegotiation

- Scarcity elevates landlord renewal leverage

- Indexed escalators transfer inflation risk

- Portfolio spread limits single-landlord concentration

Insurance and specialist services

Coverage for mechanical breakdown, business interruption and liability is essential; hard insurance markets lifted premiums and deductibles (Marsh Global Insurance Market Index Q1 2024: average rate change +8%), giving underwriters greater leverage. Few underwriters fully understand wind risks, increasing supplier bargaining power, though robust risk engineering and a clean claims history can materially temper pricing.

Supplier leverage: Top 5 OEMs ~75%, GB queue ~100 GW

Wind OEM concentration (top five ~75% in 2023–24) and specialist O&M (95–98% availability targets; ~20% of operating costs) give suppliers pricing and outage leverage. Grid constraints (GB connection queue ~100 GW in 2024; curtailment ~up to 5% in hotspots) and long-dated indexed leases increase landlord bargaining power. Insurance hardening (Marsh Q1 2024 +8% avg rates) further tightens supplier influence; diversification and long-term contracts mitigate.

| Metric | 2024 value | Impact |

|---|---|---|

| OEM concentration | Top 5 ~75% | High switching cost |

| O&M | ~20% costs; 95–98% target | Operational dependency |

| GB queue | ~100 GW | Curtailment risk |

| Insurance | +8% avg rates (Marsh Q1 2024) | Higher premiums |

| Leases | Indexed escalators | Inflation pass-through |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks for Greencoat UK Wind, assessing supplier power, buyer leverage, threat of new entrants and substitutes, and intra-industry rivalry. Includes strategic commentary on regulatory and subsidy dynamics shaping pricing, profitability and barriers protecting incumbents.

Greencoat UK Wind Porter's Five Forces provides a clear one-sheet summary that distills competitive pressures on UK wind assets for quick, confident decisions. Customizable scores and an instant spider chart let you model scenarios, communicate risk, and drop visuals directly into decks or reports.

Customers Bargaining Power

Offtaker concentration

Utilities and large traders dominate PPAs, concentrating buying power and driving standardized contracts with creditworthy counterparties that compress margins; in 2024 long‑term fixed‑price PPAs commonly span 10–15 years, providing revenue visibility for owners. Greencoat can mitigate concentration risk by diversifying offtakers across multiple contracts and tenors to smooth counterparty exposure.

Government-backed pricing schemes

CfDs and legacy ROCs reduce revenue volatility for Greencoat UK Wind while capping upside by fixing or floor-pricing payments; the ROC scheme closed to new capacity in 2017. Policy frameworks set terms via auctioned strike prices and regulatory rules rather than bilateral negotiation, lowering classic buyer power but imposing pricing discipline. Balancing CfD/ROC-backed assets with merchant exposure manages market upside and wholesale risk amid the UK 50 GW offshore target by 2030.

Merchant exposure to wholesale markets

Unhedged output sells into volatile spot markets with no single buyer, making Greencoat UK Wind a price-taker that has limited influence on contract terms. By 2024 Greencoat had hedged and staggered PPAs covering roughly 60% of near-term generation, materially cutting buyer leverage. Market liquidity in UK wholesale power allows execution of volumes but does not translate into pricing power for sellers.

Switching costs and contract tenors

Long-dated PPAs, typically 10–15 years in 2024, limit offtaker churn and materially reduce mid-tenor buyer renegotiation leverage for Greencoat UK Wind, while renewal windows remain the main channel for buyer power if market prices soften. Credit terms and collateral are usually fixed at origination, constraining mid-contract leverage, and strong asset availability and generation outperformance improves the seller negotiating stance.

- Tenor: 10–15 years (2024)

- Offtaker churn: low mid-term

- Renewals: key vulnerability

- Origination: credit/collateral set

- Performance: raises seller leverage

Corporate PPA alternatives

Rising corporate demand for renewables in 2024 (c.3 GW of UK corporate PPAs signed) expands buyer options and ramps competition among generators, pushing discounts as buyers prioritize price and ESG attributes and pressuring merchant returns.

Longer tenors and stronger corporate credit can offset lower tariffs; optionality across utility and corporate PPAs reduces dependence on any single channel.

- buyer options

- price pressure

- ESG premium

- tenor/credit offset

- utility vs corporate optionality

Buyers dominate 10-15y PPAs; policy/credit limit renegotiation — ~60% hedged

Buyers (utilities, large traders, corporates) hold concentrated power in long‑dated PPAs (10–15y) but policy CfDs/ROCs and strong origination credit constrain mid‑term renegotiation; Greencoat had ~60% hedged in 2024, cutting buyer leverage. Corporate PPAs (~3 GW UK 2024) increase seller competition but higher corporate credit/tenor offsets lower tariffs.

| Metric | 2024 |

|---|---|

| Typical PPA tenor | 10–15y |

| Hedged generation | ~60% |

| UK corporate PPAs | ~3 GW |

Full Version Awaits

Greencoat UK Wind Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Greencoat UK Wind you'll receive immediately after purchase—no surprises or placeholders. The document examines supplier power, buyer power, competitive rivalry, threat of entrants, and threat of substitutes with sector-specific evidence and valuation implications. It's fully formatted and ready for download the moment you buy. You're looking at the actual deliverable.