Greencore PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic pressures, social trends, and environmental regulation are reshaping Greencore’s competitive landscape in this concise PESTLE overview. Use these strategic signals to anticipate risks and spot growth opportunities. Purchase the full, downloadable PESTLE for an actionable, board-ready briefing now.

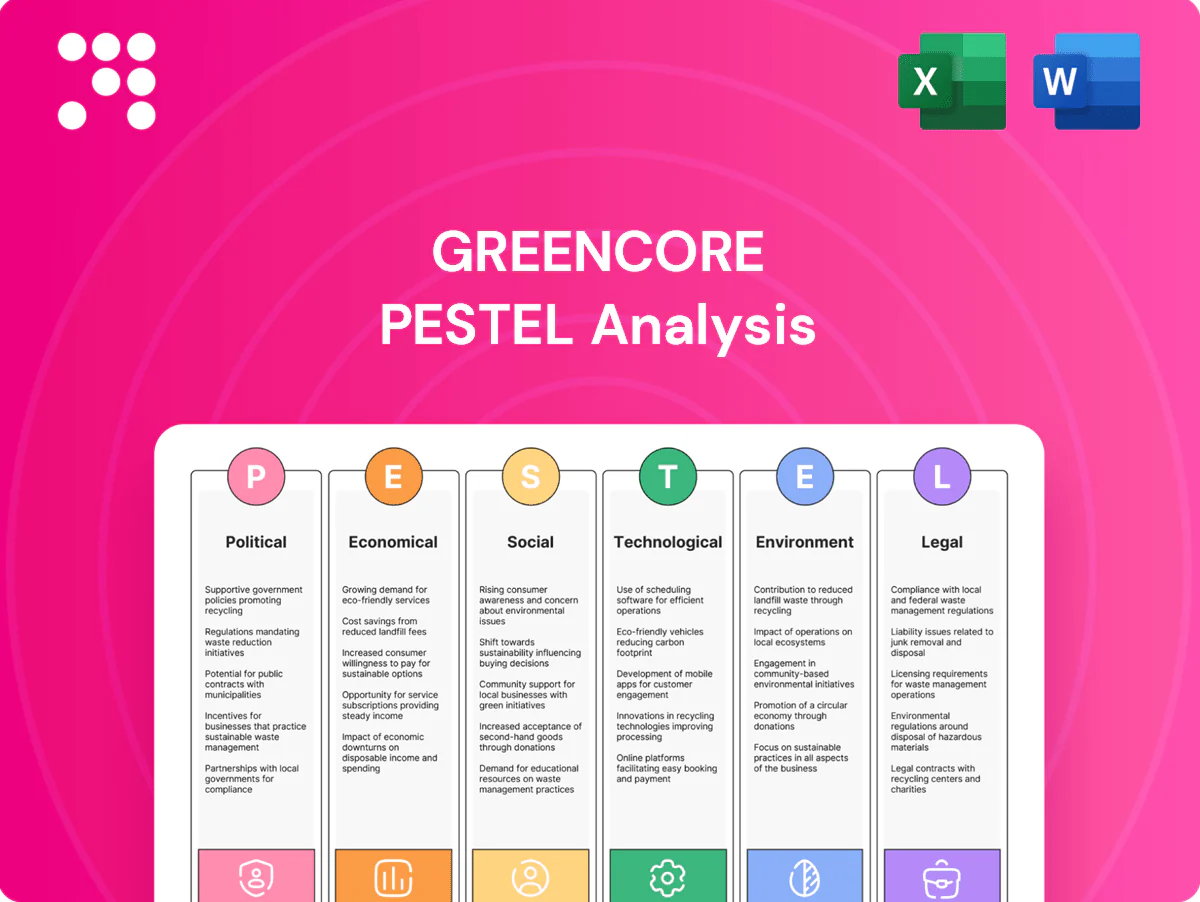

Political factors

Post-Brexit trade and customs

Post-Brexit rules of origin and the full roll‑out of SPS checks on 30 April 2024 have added customs frictions for inbound ingredients and outbound finished goods, creating multi‑day lead times that strain Greencore’s quick‑turnaround model and complicate inventory planning. Greencore (FY2024 revenue ~£1.6bn) mitigates via preferred suppliers, AEO status and dual sourcing. Political shifts could tighten or loosen UK‑EU food border regimes.

UK food policy and nutrition agenda

UK obesity drives tightened food policy: adult obesity around 28% (England, 2021–22) and obesity costs the NHS ~£6.1bn annually, pushing HFSS reformulation and promotional limits that constrain recipe choices and marketing. Retailer nutrition commitments cascade to private-label suppliers like Greencore, affecting contract terms and product specs. Policy shifts and potential taxes or targeted funding can accelerate reformulation timetables and shift demand toward healthier, portion-controlled SKUs, impacting Greencore’s SKU mix and margins.

Energy policy and industrial support

Price caps and relief schemes such as the UK Energy Bill Relief Scheme (2022–23) materially cut chilled manufacturing bills but their removal increases exposure to volatile wholesale markets; wholesale gas and power spikes in 2022–23 showed vulnerability. UK ETS carbon prices traded around £65–75/t in 2024, directly raising refrigeration operating costs. Grants like the Industrial Energy Transformation Fund offering awards up to £20m can de-risk capex for refrigeration and electrification, but ongoing policy uncertainty complicates long-term plant investment decisions.

Labour and immigration stance

Points-based immigration (introduced 1 January 2021) and the UK seasonal worker visa framework (cap around 30,000 places since 2022) directly affect Greencore’s factory staffing and logistics, tightening labour supply across UK food manufacturing hubs. Restrictive policies drive wage inflation and higher training costs, while any political relaxation could reduce peak-season bottlenecks and protect service levels for retailer contracts.

- points-based system: impact on recruitment

- seasonal quota ≈ 30,000: peak-season supply risk

- wage/training inflation: pressure on margins

- workforce availability: critical for retailer SLAs

Public procurement and food standards

Public-sector food standards often set benchmarks retailers adopt, forcing Greencore to align recipes, labelling and traceability; UK–Irish regulatory divergence increases complexity and may require parallel specs for the same SKU. Political emphasis on domestic sourcing can push procurement toward local suppliers, while standards changes drive capex in kitchens, allergen controls and third‑party auditing.

- benchmarks

- dual_compliance

- domestic_sourcing

- capex_kitchens

- allergen_audit

Post-Brexit checks, HFSS rules and energy/visa pressures lift costs and lead times

Post‑Brexit checks (full SPS rollout 30 Apr 2024) and UK–EU divergence increase lead times and complexity for Greencore (FY2024 rev ≈£1.6bn). UK obesity (~28% adults, 2021–22) and HFSS policy tighten reformulation and SKUs. Energy volatility and UK ETS (~£65–75/t in 2024) raise refrigeration costs; seasonal visa cap ≈30,000 strains labour and lifts wage pressure.

| Metric | Value |

|---|---|

| FY revenue | ~£1.6bn (2024) |

| Adult obesity | ~28% (England 2021–22) |

| UK ETS | £65–75/t (2024) |

| Seasonal visas | ~30,000 cap |

What is included in the product

Explores how macro-environmental factors uniquely affect Greencore across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and forward-looking insights to help executives and investors identify threats, opportunities and strategic responses.

A concise, visually segmented Greencore PESTLE summary for quick reference in meetings or presentations, easily editable for region- or product-specific notes and shareable across teams to streamline risk discussions and strategic planning.

Economic factors

Retailer margin pressure and pricing power

UK grocers, led by Tesco (about 27% market share) and the big four controlling roughly 60% of grocery sales, exert strong bargaining power over private-label suppliers like Greencore. Rapid cost pass-through is vital amid volatile input costs and tight margins. Tender cycles and EDLC models can compress supplier margins if not hedged. Strategic partnerships often trade lower prices for guaranteed volume and higher capacity utilisation.

Input cost volatility

Protein, wheat, veg and packaging costs remain highly weather- and geopolitics-sensitive; global wheat prices fell about 30% from 2022 peaks by 2024 but volatility persists, while European vegetable and protein markets saw seasonal swings. Energy and logistics can shift chilled cost-to-serve materially, with gas and freight swings moving margins by low-double-digit percentages. Greencore uses hedging, index-linked contracts and recipe engineering to manage OTIF penalty risk and working capital strain.

Consumer trade-down and mix shifts

Inflation-driven trade-down has boosted private-label volumes, with Kantar reporting private-label share near 51% in 2023, supporting Greencore's contract volumes into 2024. Premium and food-to-go remain cyclical—IGD/ONS data showed food-to-go spend and footfall still below pre-pandemic peaks through 2023–24. Mix shifts increase line-change frequency, lowering line efficiency and raising waste rates by several percentage points. Promotions and pack-size architecture (smaller SKUs) help defend throughput and unit economics.

Interest rates and capex funding

Higher interest rates — UK base rate around 5% in 2024–25 — raise required hurdle returns for automation, cold‑chain and sustainability capex, lengthening payback and pushing some projects below investment thresholds. Rising financing and lease costs for fleet and equipment compress margins and raise total cost of ownership. Strong contracted volumes and multi‑year customer agreements enhance bankability and can secure cheaper financing; economic easing would unlock deferred efficiency spend.

- UK base rate ~5% (2024–25)

- Higher hurdle rates → slower payback

- Lease/fleet costs ↑, margins pressured

- Contracted volumes improve financing

- Rate cuts would release deferred capex

Urban mobility and on-the-go demand

Urban footfall recovered to roughly 85–90% of 2019 levels in 2024, with commuting at c.60% of pre-pandemic peaks, so sandwiches and salads see strong lunchtime demand in city centres and tourist hubs; hybrid work keeps weekday peaks unevenly concentrated. Recovery in tourism and city throughput lifted short‑shelf‑life line volumes by mid‑single digits in 2023–24, while macro slowdowns trimmed impulse spend at c‑stores and forecourts.

- City footfall ~85–90% of 2019 (2024)

- Commuting ~60% of pre‑pandemic peaks (2024)

- Short‑shelf throughput +mid single digits (2023–24)

- Impulse purchases down in slowdowns — pressure on c‑store/forecourt sales

Post-Brexit checks, HFSS rules and energy/visa pressures lift costs and lead times

UK grocers' buying power and 51% private‑label share (2023) keep pricing pressure; input cost volatility (wheat down ~30% from 2022 peaks by 2024) and energy/logistics swings move margins materially. Higher base rate ~5% (2024–25) raises hurdle rates, delaying capex; urban footfall ~85–90% of 2019 (2024) supports food‑to‑go recovery.

| Metric | Value |

|---|---|

| Private‑label share (Kantar) | 51% (2023) |

| Wheat price change | -30% vs 2022 peak (2024) |

| UK base rate | ~5% (2024–25) |

| Urban footfall | 85–90% of 2019 (2024) |

Preview Before You Purchase

Greencore PESTLE Analysis

The preview shown here is the exact Greencore PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers Political, Economic, Social, Technological, Legal and Environmental factors affecting Greencore with sourced insights and clear implications. No placeholders or teasers—this is the final, downloadable file.

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic pressures, social trends, and environmental regulation are reshaping Greencore’s competitive landscape in this concise PESTLE overview. Use these strategic signals to anticipate risks and spot growth opportunities. Purchase the full, downloadable PESTLE for an actionable, board-ready briefing now.

Political factors

Post-Brexit trade and customs

Post-Brexit rules of origin and the full roll‑out of SPS checks on 30 April 2024 have added customs frictions for inbound ingredients and outbound finished goods, creating multi‑day lead times that strain Greencore’s quick‑turnaround model and complicate inventory planning. Greencore (FY2024 revenue ~£1.6bn) mitigates via preferred suppliers, AEO status and dual sourcing. Political shifts could tighten or loosen UK‑EU food border regimes.

UK food policy and nutrition agenda

UK obesity drives tightened food policy: adult obesity around 28% (England, 2021–22) and obesity costs the NHS ~£6.1bn annually, pushing HFSS reformulation and promotional limits that constrain recipe choices and marketing. Retailer nutrition commitments cascade to private-label suppliers like Greencore, affecting contract terms and product specs. Policy shifts and potential taxes or targeted funding can accelerate reformulation timetables and shift demand toward healthier, portion-controlled SKUs, impacting Greencore’s SKU mix and margins.

Energy policy and industrial support

Price caps and relief schemes such as the UK Energy Bill Relief Scheme (2022–23) materially cut chilled manufacturing bills but their removal increases exposure to volatile wholesale markets; wholesale gas and power spikes in 2022–23 showed vulnerability. UK ETS carbon prices traded around £65–75/t in 2024, directly raising refrigeration operating costs. Grants like the Industrial Energy Transformation Fund offering awards up to £20m can de-risk capex for refrigeration and electrification, but ongoing policy uncertainty complicates long-term plant investment decisions.

Labour and immigration stance

Points-based immigration (introduced 1 January 2021) and the UK seasonal worker visa framework (cap around 30,000 places since 2022) directly affect Greencore’s factory staffing and logistics, tightening labour supply across UK food manufacturing hubs. Restrictive policies drive wage inflation and higher training costs, while any political relaxation could reduce peak-season bottlenecks and protect service levels for retailer contracts.

- points-based system: impact on recruitment

- seasonal quota ≈ 30,000: peak-season supply risk

- wage/training inflation: pressure on margins

- workforce availability: critical for retailer SLAs

Public procurement and food standards

Public-sector food standards often set benchmarks retailers adopt, forcing Greencore to align recipes, labelling and traceability; UK–Irish regulatory divergence increases complexity and may require parallel specs for the same SKU. Political emphasis on domestic sourcing can push procurement toward local suppliers, while standards changes drive capex in kitchens, allergen controls and third‑party auditing.

- benchmarks

- dual_compliance

- domestic_sourcing

- capex_kitchens

- allergen_audit

Post-Brexit checks, HFSS rules and energy/visa pressures lift costs and lead times

Post‑Brexit checks (full SPS rollout 30 Apr 2024) and UK–EU divergence increase lead times and complexity for Greencore (FY2024 rev ≈£1.6bn). UK obesity (~28% adults, 2021–22) and HFSS policy tighten reformulation and SKUs. Energy volatility and UK ETS (~£65–75/t in 2024) raise refrigeration costs; seasonal visa cap ≈30,000 strains labour and lifts wage pressure.

| Metric | Value |

|---|---|

| FY revenue | ~£1.6bn (2024) |

| Adult obesity | ~28% (England 2021–22) |

| UK ETS | £65–75/t (2024) |

| Seasonal visas | ~30,000 cap |

What is included in the product

Explores how macro-environmental factors uniquely affect Greencore across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and forward-looking insights to help executives and investors identify threats, opportunities and strategic responses.

A concise, visually segmented Greencore PESTLE summary for quick reference in meetings or presentations, easily editable for region- or product-specific notes and shareable across teams to streamline risk discussions and strategic planning.

Economic factors

Retailer margin pressure and pricing power

UK grocers, led by Tesco (about 27% market share) and the big four controlling roughly 60% of grocery sales, exert strong bargaining power over private-label suppliers like Greencore. Rapid cost pass-through is vital amid volatile input costs and tight margins. Tender cycles and EDLC models can compress supplier margins if not hedged. Strategic partnerships often trade lower prices for guaranteed volume and higher capacity utilisation.

Input cost volatility

Protein, wheat, veg and packaging costs remain highly weather- and geopolitics-sensitive; global wheat prices fell about 30% from 2022 peaks by 2024 but volatility persists, while European vegetable and protein markets saw seasonal swings. Energy and logistics can shift chilled cost-to-serve materially, with gas and freight swings moving margins by low-double-digit percentages. Greencore uses hedging, index-linked contracts and recipe engineering to manage OTIF penalty risk and working capital strain.

Consumer trade-down and mix shifts

Inflation-driven trade-down has boosted private-label volumes, with Kantar reporting private-label share near 51% in 2023, supporting Greencore's contract volumes into 2024. Premium and food-to-go remain cyclical—IGD/ONS data showed food-to-go spend and footfall still below pre-pandemic peaks through 2023–24. Mix shifts increase line-change frequency, lowering line efficiency and raising waste rates by several percentage points. Promotions and pack-size architecture (smaller SKUs) help defend throughput and unit economics.

Interest rates and capex funding

Higher interest rates — UK base rate around 5% in 2024–25 — raise required hurdle returns for automation, cold‑chain and sustainability capex, lengthening payback and pushing some projects below investment thresholds. Rising financing and lease costs for fleet and equipment compress margins and raise total cost of ownership. Strong contracted volumes and multi‑year customer agreements enhance bankability and can secure cheaper financing; economic easing would unlock deferred efficiency spend.

- UK base rate ~5% (2024–25)

- Higher hurdle rates → slower payback

- Lease/fleet costs ↑, margins pressured

- Contracted volumes improve financing

- Rate cuts would release deferred capex

Urban mobility and on-the-go demand

Urban footfall recovered to roughly 85–90% of 2019 levels in 2024, with commuting at c.60% of pre-pandemic peaks, so sandwiches and salads see strong lunchtime demand in city centres and tourist hubs; hybrid work keeps weekday peaks unevenly concentrated. Recovery in tourism and city throughput lifted short‑shelf‑life line volumes by mid‑single digits in 2023–24, while macro slowdowns trimmed impulse spend at c‑stores and forecourts.

- City footfall ~85–90% of 2019 (2024)

- Commuting ~60% of pre‑pandemic peaks (2024)

- Short‑shelf throughput +mid single digits (2023–24)

- Impulse purchases down in slowdowns — pressure on c‑store/forecourt sales

Post-Brexit checks, HFSS rules and energy/visa pressures lift costs and lead times

UK grocers' buying power and 51% private‑label share (2023) keep pricing pressure; input cost volatility (wheat down ~30% from 2022 peaks by 2024) and energy/logistics swings move margins materially. Higher base rate ~5% (2024–25) raises hurdle rates, delaying capex; urban footfall ~85–90% of 2019 (2024) supports food‑to‑go recovery.

| Metric | Value |

|---|---|

| Private‑label share (Kantar) | 51% (2023) |

| Wheat price change | -30% vs 2022 peak (2024) |

| UK base rate | ~5% (2024–25) |

| Urban footfall | 85–90% of 2019 (2024) |

Preview Before You Purchase

Greencore PESTLE Analysis

The preview shown here is the exact Greencore PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers Political, Economic, Social, Technological, Legal and Environmental factors affecting Greencore with sourced insights and clear implications. No placeholders or teasers—this is the final, downloadable file.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic pressures, social trends, and environmental regulation are reshaping Greencore’s competitive landscape in this concise PESTLE overview. Use these strategic signals to anticipate risks and spot growth opportunities. Purchase the full, downloadable PESTLE for an actionable, board-ready briefing now.

Political factors

Post-Brexit trade and customs

Post-Brexit rules of origin and the full roll‑out of SPS checks on 30 April 2024 have added customs frictions for inbound ingredients and outbound finished goods, creating multi‑day lead times that strain Greencore’s quick‑turnaround model and complicate inventory planning. Greencore (FY2024 revenue ~£1.6bn) mitigates via preferred suppliers, AEO status and dual sourcing. Political shifts could tighten or loosen UK‑EU food border regimes.

UK food policy and nutrition agenda

UK obesity drives tightened food policy: adult obesity around 28% (England, 2021–22) and obesity costs the NHS ~£6.1bn annually, pushing HFSS reformulation and promotional limits that constrain recipe choices and marketing. Retailer nutrition commitments cascade to private-label suppliers like Greencore, affecting contract terms and product specs. Policy shifts and potential taxes or targeted funding can accelerate reformulation timetables and shift demand toward healthier, portion-controlled SKUs, impacting Greencore’s SKU mix and margins.

Energy policy and industrial support

Price caps and relief schemes such as the UK Energy Bill Relief Scheme (2022–23) materially cut chilled manufacturing bills but their removal increases exposure to volatile wholesale markets; wholesale gas and power spikes in 2022–23 showed vulnerability. UK ETS carbon prices traded around £65–75/t in 2024, directly raising refrigeration operating costs. Grants like the Industrial Energy Transformation Fund offering awards up to £20m can de-risk capex for refrigeration and electrification, but ongoing policy uncertainty complicates long-term plant investment decisions.

Labour and immigration stance

Points-based immigration (introduced 1 January 2021) and the UK seasonal worker visa framework (cap around 30,000 places since 2022) directly affect Greencore’s factory staffing and logistics, tightening labour supply across UK food manufacturing hubs. Restrictive policies drive wage inflation and higher training costs, while any political relaxation could reduce peak-season bottlenecks and protect service levels for retailer contracts.

- points-based system: impact on recruitment

- seasonal quota ≈ 30,000: peak-season supply risk

- wage/training inflation: pressure on margins

- workforce availability: critical for retailer SLAs

Public procurement and food standards

Public-sector food standards often set benchmarks retailers adopt, forcing Greencore to align recipes, labelling and traceability; UK–Irish regulatory divergence increases complexity and may require parallel specs for the same SKU. Political emphasis on domestic sourcing can push procurement toward local suppliers, while standards changes drive capex in kitchens, allergen controls and third‑party auditing.

- benchmarks

- dual_compliance

- domestic_sourcing

- capex_kitchens

- allergen_audit

Post-Brexit checks, HFSS rules and energy/visa pressures lift costs and lead times

Post‑Brexit checks (full SPS rollout 30 Apr 2024) and UK–EU divergence increase lead times and complexity for Greencore (FY2024 rev ≈£1.6bn). UK obesity (~28% adults, 2021–22) and HFSS policy tighten reformulation and SKUs. Energy volatility and UK ETS (~£65–75/t in 2024) raise refrigeration costs; seasonal visa cap ≈30,000 strains labour and lifts wage pressure.

| Metric | Value |

|---|---|

| FY revenue | ~£1.6bn (2024) |

| Adult obesity | ~28% (England 2021–22) |

| UK ETS | £65–75/t (2024) |

| Seasonal visas | ~30,000 cap |

What is included in the product

Explores how macro-environmental factors uniquely affect Greencore across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and forward-looking insights to help executives and investors identify threats, opportunities and strategic responses.

A concise, visually segmented Greencore PESTLE summary for quick reference in meetings or presentations, easily editable for region- or product-specific notes and shareable across teams to streamline risk discussions and strategic planning.

Economic factors

Retailer margin pressure and pricing power

UK grocers, led by Tesco (about 27% market share) and the big four controlling roughly 60% of grocery sales, exert strong bargaining power over private-label suppliers like Greencore. Rapid cost pass-through is vital amid volatile input costs and tight margins. Tender cycles and EDLC models can compress supplier margins if not hedged. Strategic partnerships often trade lower prices for guaranteed volume and higher capacity utilisation.

Input cost volatility

Protein, wheat, veg and packaging costs remain highly weather- and geopolitics-sensitive; global wheat prices fell about 30% from 2022 peaks by 2024 but volatility persists, while European vegetable and protein markets saw seasonal swings. Energy and logistics can shift chilled cost-to-serve materially, with gas and freight swings moving margins by low-double-digit percentages. Greencore uses hedging, index-linked contracts and recipe engineering to manage OTIF penalty risk and working capital strain.

Consumer trade-down and mix shifts

Inflation-driven trade-down has boosted private-label volumes, with Kantar reporting private-label share near 51% in 2023, supporting Greencore's contract volumes into 2024. Premium and food-to-go remain cyclical—IGD/ONS data showed food-to-go spend and footfall still below pre-pandemic peaks through 2023–24. Mix shifts increase line-change frequency, lowering line efficiency and raising waste rates by several percentage points. Promotions and pack-size architecture (smaller SKUs) help defend throughput and unit economics.

Interest rates and capex funding

Higher interest rates — UK base rate around 5% in 2024–25 — raise required hurdle returns for automation, cold‑chain and sustainability capex, lengthening payback and pushing some projects below investment thresholds. Rising financing and lease costs for fleet and equipment compress margins and raise total cost of ownership. Strong contracted volumes and multi‑year customer agreements enhance bankability and can secure cheaper financing; economic easing would unlock deferred efficiency spend.

- UK base rate ~5% (2024–25)

- Higher hurdle rates → slower payback

- Lease/fleet costs ↑, margins pressured

- Contracted volumes improve financing

- Rate cuts would release deferred capex

Urban mobility and on-the-go demand

Urban footfall recovered to roughly 85–90% of 2019 levels in 2024, with commuting at c.60% of pre-pandemic peaks, so sandwiches and salads see strong lunchtime demand in city centres and tourist hubs; hybrid work keeps weekday peaks unevenly concentrated. Recovery in tourism and city throughput lifted short‑shelf‑life line volumes by mid‑single digits in 2023–24, while macro slowdowns trimmed impulse spend at c‑stores and forecourts.

- City footfall ~85–90% of 2019 (2024)

- Commuting ~60% of pre‑pandemic peaks (2024)

- Short‑shelf throughput +mid single digits (2023–24)

- Impulse purchases down in slowdowns — pressure on c‑store/forecourt sales

Post-Brexit checks, HFSS rules and energy/visa pressures lift costs and lead times

UK grocers' buying power and 51% private‑label share (2023) keep pricing pressure; input cost volatility (wheat down ~30% from 2022 peaks by 2024) and energy/logistics swings move margins materially. Higher base rate ~5% (2024–25) raises hurdle rates, delaying capex; urban footfall ~85–90% of 2019 (2024) supports food‑to‑go recovery.

| Metric | Value |

|---|---|

| Private‑label share (Kantar) | 51% (2023) |

| Wheat price change | -30% vs 2022 peak (2024) |

| UK base rate | ~5% (2024–25) |

| Urban footfall | 85–90% of 2019 (2024) |

Preview Before You Purchase

Greencore PESTLE Analysis

The preview shown here is the exact Greencore PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers Political, Economic, Social, Technological, Legal and Environmental factors affecting Greencore with sourced insights and clear implications. No placeholders or teasers—this is the final, downloadable file.