Greenyard Porter's Five Forces Analysis

From Overview to Strategy Blueprint

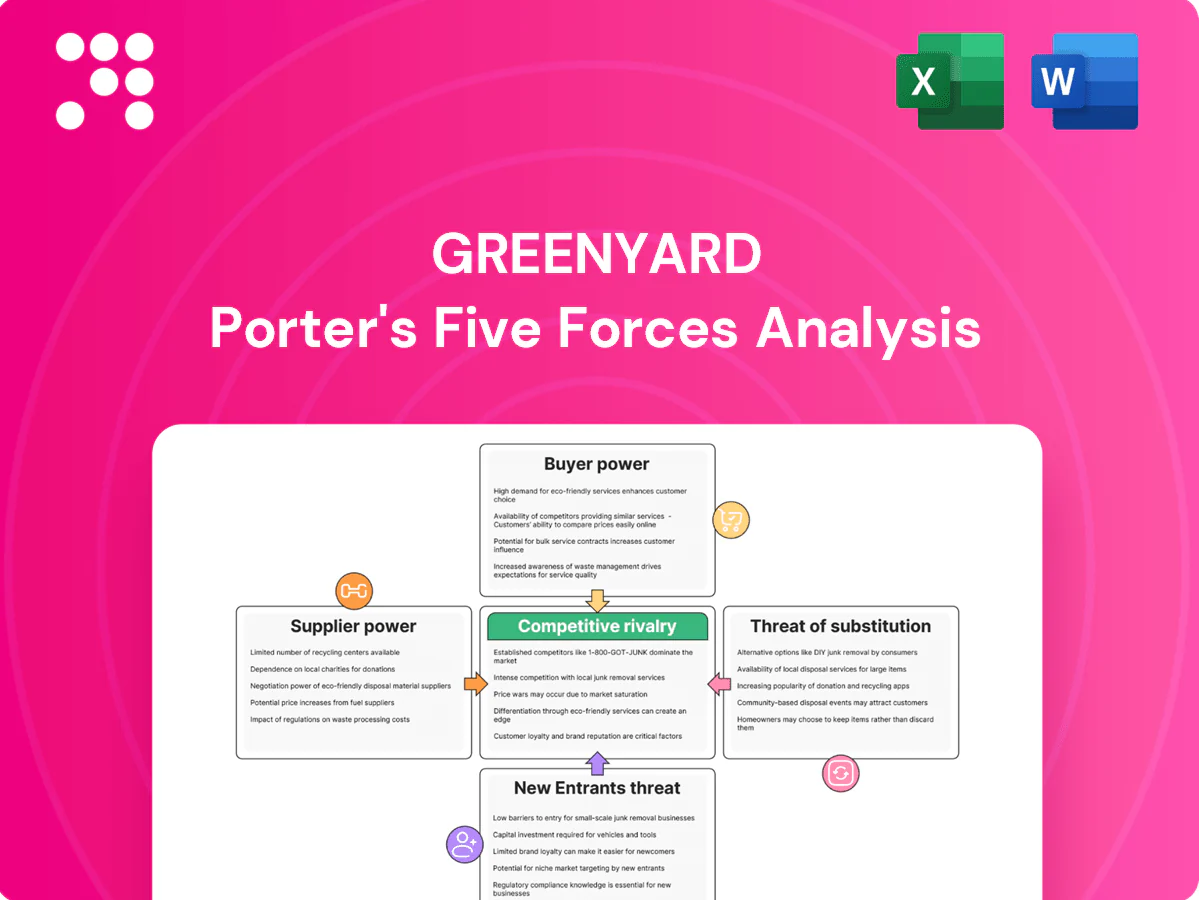

Greenyard faces strong buyer power and margin pressure, significant rivalry in fresh and frozen produce, moderate supplier leverage, and limited but growing threats from substitutes and niche entrants. This snapshot highlights key competitive pressures shaping margins and strategy. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations for Greenyard.

Suppliers Bargaining Power

Fragmented farm base vs. specialty growers

Greenyard sources from a wide network of small and mid-sized farmers, which reduces individual supplier leverage and fragments bargaining power. Niche or counter-seasonal producers with certified quality or unique varieties can still command premiums and stronger terms. Dependence on origin-specific crops such as berries or exotics increases supplier influence. Greenyard’s integrated supply programs provide volume stability and mitigate this supplier power.

Seasonality, weather, and yield volatility

Climate risk—Copernicus recorded 2023 as Europe’s warmest year, with summer anomalies up to +3°C in parts—heightened droughts and pest outbreaks, tightening supply and increasing supplier leverage as limited volumes are repriced or rerouted to highest bidders. Greenyard’s multi-origin sourcing and frozen stock buffers reduce but do not eliminate this structural volatility in fresh categories.

Certification and sustainability requirements

Standards like GlobalG.A.P., organic and ESG traceability—GlobalG.A.P. certifying over 200,000 producers worldwide—shrink the pool of compliant suppliers and raise compliance costs, boosting certified growers’ bargaining power. Greenyard’s public sustainability targets increase entry hurdles for entrants while securing reliable, certified partners. Over time this creates mutual dependence that helps moderate price friction between Greenyard and suppliers.

Input cost inflation and currency swings

Input inflation for fertilizers, energy, labor, packaging and freight largely feeds into farm‑gate prices; suppliers increasingly demand index‑linked contracts, shifting cost volatility to buyers, while FX swings in origin markets amplify supplier claims. Greenyard mitigates via hedging, SKU mix management and multi‑year supply frameworks.

- Fertilizers ~25–40% above 2019 levels

- Freight ~2x pre‑COVID rates

- Energy volatility drives index clauses

- Hedging and long‑term contracts reduce passthrough

Consolidation of key upstream partners

Consolidation of packhouses and cooperatives concentrates supplier negotiating clout in some crops, enabling larger upstream players to demand volume commitments and favorable payment terms, especially in high-value, capital-intensive post-harvest categories. Greenyard’s scale (FY 2024 revenue ~€3.0bn) and integrated sourcing secure priority access to volumes and help temper spot-price escalations, reducing supply disruption risk and margin pressure.

- Consolidated suppliers: higher bargaining power

- High-value crops: greater leverage for packhouses

- Greenyard scale (FY 2024 ~€3.0bn): priority access

- Outcome: mitigated price spikes, improved supply reliability

Fragmented suppliers but origin concentration lifts grower power; €3.0bn

Greenyard’s fragmented supplier base lowers individual leverage, but origin‑specific crops, certified growers and packhouse consolidation raise supplier power; FY 2024 revenue ~€3.0bn underpins sourcing scale. Input shocks (fertilizers +25–40% vs 2019; freight ~2x) and 2023 Europe heat anomalies (Copernicus) tighten supply.

| Metric | Value | Impact |

|---|---|---|

| FY 2024 rev | €3.0bn | Priority access |

| Fertilizer | +25–40% vs 2019 | Higher farm costs |

| Freight | ~2x pre‑COVID | Price pass‑through |

What is included in the product

Tailored Porter’s Five Forces analysis for Greenyard uncovering competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect margins and market share.

One-sheet Porter's Five Forces for Greenyard that instantly highlights competitive pressures with a clean spider chart and customizable pressure levels—easy to copy into decks, swap in your data, and duplicate for different market scenarios without macros.

Customers Bargaining Power

Concentrated European retailers

Concentrated European retailers wield strong bargaining power: through volume, private label (about one-third of grocery sales in many European markets), and centralized buying they switch suppliers across tenders and demand annual cost-downs; service-level penalties further compress margins. Greenyard mitigates pressure via strategic partnerships and category captaincy agreements that secure shelf space and collaborative promotions.

Private label and specification control

Retailers increasingly dictate specs, packaging, audits and sustainability KPIs—boosting buyer leverage as private label penetration in European grocery reached roughly 30–40% in 2024 and Greenyard reported ~€3.0bn revenue. Private label compresses brand differentiation and raises price sensitivity. Greenyard’s convenience, ripening and ready-to-eat innovation adds value to defend commercial terms, yet buyers still have strong alternative suppliers and sourcing options.

Multi-year integrated supply contracts

Multi-year integrated supply contracts (typically 3–5 years) stabilize volumes for Greenyard while embedding performance-based pricing tied to quality and on-time delivery; retailers leverage benchmarking and open-book cost models to squeeze margins. In return Greenyard gains forecast visibility and planning efficiency, reducing supply variability and inventory swings. This mutual dependency moderates extreme swings in buyer power.

Foodservice and industry diversification

Exposure to foodservice and processors diversifies Greenyard away from retail dominance; foodservice contributed roughly 30% of volumes in 2024, reducing pure price pressure and increasing focus on reliability and tailored pack formats. These buyers still run competitive bids, but Greenyard’s product breadth across fresh, frozen and prepared lines and presence in >20 markets (2024 revenue ~€2.1bn) strengthens its negotiating position.

- Diversification: foodservice ~30% (2024)

- Revenue: ~€2.1bn (2024)

- Strength: fresh/frozen/prepared breadth

- Risk: competitive bidding persists

Switching costs and service complexity

Greenyard’s end-to-end services—ripening, cold chain, just-in-time delivery and category management—create tangible switching frictions that raise the operational and administrative costs for buyers, as requalifying suppliers and retooling logistics chains typically require multi-week onboarding and capital outlays. Consistent quality and availability across retail channels further embed Greenyard, reducing buyer leverage at the margin despite frequent price-driven tenders.

- Service integration: ripening+cold chain+JIT

- Hidden costs: supplier requalification, logistics retooling

- Embedding effect: quality and availability

- Net impact: reduced buyer leverage in tenders

Retail consolidation tightens margins; supplier offsets with long contracts, service and foodservice

Concentrated European retailers exert strong bargaining power via volume, private label (30–40% in 2024) and centralized buying, forcing annual cost-downs and service penalties. Greenyard leverages multi-year 3–5y contracts, category captaincy and service integration (ripening, cold chain, JIT) to partially offset pressure. Foodservice diversification (~30% volumes, 2024) and product breadth reduce pure price vulnerability.

| Metric | 2024 |

|---|---|

| Private label penetration | 30–40% |

| Greenyard revenue | ~€3.0bn |

| Foodservice share | ~30% volumes |

Full Version Awaits

Greenyard Porter's Five Forces Analysis

This preview shows the exact Greenyard Porter’s Five Forces Analysis you'll receive after purchase — no mockups or placeholders. The document is the final, fully formatted file and will be available for immediate download upon payment. Use it directly for strategic or investment decisions.

From Overview to Strategy Blueprint

Greenyard faces strong buyer power and margin pressure, significant rivalry in fresh and frozen produce, moderate supplier leverage, and limited but growing threats from substitutes and niche entrants. This snapshot highlights key competitive pressures shaping margins and strategy. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations for Greenyard.

Suppliers Bargaining Power

Fragmented farm base vs. specialty growers

Greenyard sources from a wide network of small and mid-sized farmers, which reduces individual supplier leverage and fragments bargaining power. Niche or counter-seasonal producers with certified quality or unique varieties can still command premiums and stronger terms. Dependence on origin-specific crops such as berries or exotics increases supplier influence. Greenyard’s integrated supply programs provide volume stability and mitigate this supplier power.

Seasonality, weather, and yield volatility

Climate risk—Copernicus recorded 2023 as Europe’s warmest year, with summer anomalies up to +3°C in parts—heightened droughts and pest outbreaks, tightening supply and increasing supplier leverage as limited volumes are repriced or rerouted to highest bidders. Greenyard’s multi-origin sourcing and frozen stock buffers reduce but do not eliminate this structural volatility in fresh categories.

Certification and sustainability requirements

Standards like GlobalG.A.P., organic and ESG traceability—GlobalG.A.P. certifying over 200,000 producers worldwide—shrink the pool of compliant suppliers and raise compliance costs, boosting certified growers’ bargaining power. Greenyard’s public sustainability targets increase entry hurdles for entrants while securing reliable, certified partners. Over time this creates mutual dependence that helps moderate price friction between Greenyard and suppliers.

Input cost inflation and currency swings

Input inflation for fertilizers, energy, labor, packaging and freight largely feeds into farm‑gate prices; suppliers increasingly demand index‑linked contracts, shifting cost volatility to buyers, while FX swings in origin markets amplify supplier claims. Greenyard mitigates via hedging, SKU mix management and multi‑year supply frameworks.

- Fertilizers ~25–40% above 2019 levels

- Freight ~2x pre‑COVID rates

- Energy volatility drives index clauses

- Hedging and long‑term contracts reduce passthrough

Consolidation of key upstream partners

Consolidation of packhouses and cooperatives concentrates supplier negotiating clout in some crops, enabling larger upstream players to demand volume commitments and favorable payment terms, especially in high-value, capital-intensive post-harvest categories. Greenyard’s scale (FY 2024 revenue ~€3.0bn) and integrated sourcing secure priority access to volumes and help temper spot-price escalations, reducing supply disruption risk and margin pressure.

- Consolidated suppliers: higher bargaining power

- High-value crops: greater leverage for packhouses

- Greenyard scale (FY 2024 ~€3.0bn): priority access

- Outcome: mitigated price spikes, improved supply reliability

Fragmented suppliers but origin concentration lifts grower power; €3.0bn

Greenyard’s fragmented supplier base lowers individual leverage, but origin‑specific crops, certified growers and packhouse consolidation raise supplier power; FY 2024 revenue ~€3.0bn underpins sourcing scale. Input shocks (fertilizers +25–40% vs 2019; freight ~2x) and 2023 Europe heat anomalies (Copernicus) tighten supply.

| Metric | Value | Impact |

|---|---|---|

| FY 2024 rev | €3.0bn | Priority access |

| Fertilizer | +25–40% vs 2019 | Higher farm costs |

| Freight | ~2x pre‑COVID | Price pass‑through |

What is included in the product

Tailored Porter’s Five Forces analysis for Greenyard uncovering competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect margins and market share.

One-sheet Porter's Five Forces for Greenyard that instantly highlights competitive pressures with a clean spider chart and customizable pressure levels—easy to copy into decks, swap in your data, and duplicate for different market scenarios without macros.

Customers Bargaining Power

Concentrated European retailers

Concentrated European retailers wield strong bargaining power: through volume, private label (about one-third of grocery sales in many European markets), and centralized buying they switch suppliers across tenders and demand annual cost-downs; service-level penalties further compress margins. Greenyard mitigates pressure via strategic partnerships and category captaincy agreements that secure shelf space and collaborative promotions.

Private label and specification control

Retailers increasingly dictate specs, packaging, audits and sustainability KPIs—boosting buyer leverage as private label penetration in European grocery reached roughly 30–40% in 2024 and Greenyard reported ~€3.0bn revenue. Private label compresses brand differentiation and raises price sensitivity. Greenyard’s convenience, ripening and ready-to-eat innovation adds value to defend commercial terms, yet buyers still have strong alternative suppliers and sourcing options.

Multi-year integrated supply contracts

Multi-year integrated supply contracts (typically 3–5 years) stabilize volumes for Greenyard while embedding performance-based pricing tied to quality and on-time delivery; retailers leverage benchmarking and open-book cost models to squeeze margins. In return Greenyard gains forecast visibility and planning efficiency, reducing supply variability and inventory swings. This mutual dependency moderates extreme swings in buyer power.

Foodservice and industry diversification

Exposure to foodservice and processors diversifies Greenyard away from retail dominance; foodservice contributed roughly 30% of volumes in 2024, reducing pure price pressure and increasing focus on reliability and tailored pack formats. These buyers still run competitive bids, but Greenyard’s product breadth across fresh, frozen and prepared lines and presence in >20 markets (2024 revenue ~€2.1bn) strengthens its negotiating position.

- Diversification: foodservice ~30% (2024)

- Revenue: ~€2.1bn (2024)

- Strength: fresh/frozen/prepared breadth

- Risk: competitive bidding persists

Switching costs and service complexity

Greenyard’s end-to-end services—ripening, cold chain, just-in-time delivery and category management—create tangible switching frictions that raise the operational and administrative costs for buyers, as requalifying suppliers and retooling logistics chains typically require multi-week onboarding and capital outlays. Consistent quality and availability across retail channels further embed Greenyard, reducing buyer leverage at the margin despite frequent price-driven tenders.

- Service integration: ripening+cold chain+JIT

- Hidden costs: supplier requalification, logistics retooling

- Embedding effect: quality and availability

- Net impact: reduced buyer leverage in tenders

Retail consolidation tightens margins; supplier offsets with long contracts, service and foodservice

Concentrated European retailers exert strong bargaining power via volume, private label (30–40% in 2024) and centralized buying, forcing annual cost-downs and service penalties. Greenyard leverages multi-year 3–5y contracts, category captaincy and service integration (ripening, cold chain, JIT) to partially offset pressure. Foodservice diversification (~30% volumes, 2024) and product breadth reduce pure price vulnerability.

| Metric | 2024 |

|---|---|

| Private label penetration | 30–40% |

| Greenyard revenue | ~€3.0bn |

| Foodservice share | ~30% volumes |

Full Version Awaits

Greenyard Porter's Five Forces Analysis

This preview shows the exact Greenyard Porter’s Five Forces Analysis you'll receive after purchase — no mockups or placeholders. The document is the final, fully formatted file and will be available for immediate download upon payment. Use it directly for strategic or investment decisions.

Description

From Overview to Strategy Blueprint

Greenyard faces strong buyer power and margin pressure, significant rivalry in fresh and frozen produce, moderate supplier leverage, and limited but growing threats from substitutes and niche entrants. This snapshot highlights key competitive pressures shaping margins and strategy. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations for Greenyard.

Suppliers Bargaining Power

Fragmented farm base vs. specialty growers

Greenyard sources from a wide network of small and mid-sized farmers, which reduces individual supplier leverage and fragments bargaining power. Niche or counter-seasonal producers with certified quality or unique varieties can still command premiums and stronger terms. Dependence on origin-specific crops such as berries or exotics increases supplier influence. Greenyard’s integrated supply programs provide volume stability and mitigate this supplier power.

Seasonality, weather, and yield volatility

Climate risk—Copernicus recorded 2023 as Europe’s warmest year, with summer anomalies up to +3°C in parts—heightened droughts and pest outbreaks, tightening supply and increasing supplier leverage as limited volumes are repriced or rerouted to highest bidders. Greenyard’s multi-origin sourcing and frozen stock buffers reduce but do not eliminate this structural volatility in fresh categories.

Certification and sustainability requirements

Standards like GlobalG.A.P., organic and ESG traceability—GlobalG.A.P. certifying over 200,000 producers worldwide—shrink the pool of compliant suppliers and raise compliance costs, boosting certified growers’ bargaining power. Greenyard’s public sustainability targets increase entry hurdles for entrants while securing reliable, certified partners. Over time this creates mutual dependence that helps moderate price friction between Greenyard and suppliers.

Input cost inflation and currency swings

Input inflation for fertilizers, energy, labor, packaging and freight largely feeds into farm‑gate prices; suppliers increasingly demand index‑linked contracts, shifting cost volatility to buyers, while FX swings in origin markets amplify supplier claims. Greenyard mitigates via hedging, SKU mix management and multi‑year supply frameworks.

- Fertilizers ~25–40% above 2019 levels

- Freight ~2x pre‑COVID rates

- Energy volatility drives index clauses

- Hedging and long‑term contracts reduce passthrough

Consolidation of key upstream partners

Consolidation of packhouses and cooperatives concentrates supplier negotiating clout in some crops, enabling larger upstream players to demand volume commitments and favorable payment terms, especially in high-value, capital-intensive post-harvest categories. Greenyard’s scale (FY 2024 revenue ~€3.0bn) and integrated sourcing secure priority access to volumes and help temper spot-price escalations, reducing supply disruption risk and margin pressure.

- Consolidated suppliers: higher bargaining power

- High-value crops: greater leverage for packhouses

- Greenyard scale (FY 2024 ~€3.0bn): priority access

- Outcome: mitigated price spikes, improved supply reliability

Fragmented suppliers but origin concentration lifts grower power; €3.0bn

Greenyard’s fragmented supplier base lowers individual leverage, but origin‑specific crops, certified growers and packhouse consolidation raise supplier power; FY 2024 revenue ~€3.0bn underpins sourcing scale. Input shocks (fertilizers +25–40% vs 2019; freight ~2x) and 2023 Europe heat anomalies (Copernicus) tighten supply.

| Metric | Value | Impact |

|---|---|---|

| FY 2024 rev | €3.0bn | Priority access |

| Fertilizer | +25–40% vs 2019 | Higher farm costs |

| Freight | ~2x pre‑COVID | Price pass‑through |

What is included in the product

Tailored Porter’s Five Forces analysis for Greenyard uncovering competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect margins and market share.

One-sheet Porter's Five Forces for Greenyard that instantly highlights competitive pressures with a clean spider chart and customizable pressure levels—easy to copy into decks, swap in your data, and duplicate for different market scenarios without macros.

Customers Bargaining Power

Concentrated European retailers

Concentrated European retailers wield strong bargaining power: through volume, private label (about one-third of grocery sales in many European markets), and centralized buying they switch suppliers across tenders and demand annual cost-downs; service-level penalties further compress margins. Greenyard mitigates pressure via strategic partnerships and category captaincy agreements that secure shelf space and collaborative promotions.

Private label and specification control

Retailers increasingly dictate specs, packaging, audits and sustainability KPIs—boosting buyer leverage as private label penetration in European grocery reached roughly 30–40% in 2024 and Greenyard reported ~€3.0bn revenue. Private label compresses brand differentiation and raises price sensitivity. Greenyard’s convenience, ripening and ready-to-eat innovation adds value to defend commercial terms, yet buyers still have strong alternative suppliers and sourcing options.

Multi-year integrated supply contracts

Multi-year integrated supply contracts (typically 3–5 years) stabilize volumes for Greenyard while embedding performance-based pricing tied to quality and on-time delivery; retailers leverage benchmarking and open-book cost models to squeeze margins. In return Greenyard gains forecast visibility and planning efficiency, reducing supply variability and inventory swings. This mutual dependency moderates extreme swings in buyer power.

Foodservice and industry diversification

Exposure to foodservice and processors diversifies Greenyard away from retail dominance; foodservice contributed roughly 30% of volumes in 2024, reducing pure price pressure and increasing focus on reliability and tailored pack formats. These buyers still run competitive bids, but Greenyard’s product breadth across fresh, frozen and prepared lines and presence in >20 markets (2024 revenue ~€2.1bn) strengthens its negotiating position.

- Diversification: foodservice ~30% (2024)

- Revenue: ~€2.1bn (2024)

- Strength: fresh/frozen/prepared breadth

- Risk: competitive bidding persists

Switching costs and service complexity

Greenyard’s end-to-end services—ripening, cold chain, just-in-time delivery and category management—create tangible switching frictions that raise the operational and administrative costs for buyers, as requalifying suppliers and retooling logistics chains typically require multi-week onboarding and capital outlays. Consistent quality and availability across retail channels further embed Greenyard, reducing buyer leverage at the margin despite frequent price-driven tenders.

- Service integration: ripening+cold chain+JIT

- Hidden costs: supplier requalification, logistics retooling

- Embedding effect: quality and availability

- Net impact: reduced buyer leverage in tenders

Retail consolidation tightens margins; supplier offsets with long contracts, service and foodservice

Concentrated European retailers exert strong bargaining power via volume, private label (30–40% in 2024) and centralized buying, forcing annual cost-downs and service penalties. Greenyard leverages multi-year 3–5y contracts, category captaincy and service integration (ripening, cold chain, JIT) to partially offset pressure. Foodservice diversification (~30% volumes, 2024) and product breadth reduce pure price vulnerability.

| Metric | 2024 |

|---|---|

| Private label penetration | 30–40% |

| Greenyard revenue | ~€3.0bn |

| Foodservice share | ~30% volumes |

Full Version Awaits

Greenyard Porter's Five Forces Analysis

This preview shows the exact Greenyard Porter’s Five Forces Analysis you'll receive after purchase — no mockups or placeholders. The document is the final, fully formatted file and will be available for immediate download upon payment. Use it directly for strategic or investment decisions.