Grohmann GmbH Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Grohmann GmbH operates in a capital-intensive, high-tech manufacturing niche where supplier specialization and advanced automation create both barriers and opportunities; competitive rivalry is moderate but innovation-driven. This snapshot highlights key pressures—supplier power, buyer expectations, and substitute risks—without full force ratings. Unlock the complete Porter’s Five Forces Analysis for actionable, consultant-grade insights and visuals to inform strategy and investment decisions.

Suppliers Bargaining Power

Concentrated high-tech component base

Grohmann relies on precision components such as servomotors, motion controllers, machine vision and industrial PCs produced by a limited set of advanced suppliers. This concentration increases supplier leverage over pricing and lead times and, as of 2024, keeps switching costs high because many parts lack direct substitutes. Unique component roadmaps from suppliers further constrain Grohmann’s design choices and product timelines.

Switching costs in qualification

Qualifying alternative suppliers for safety-critical, high-precision automation commonly requires 3–9 months of testing and revalidation and can incur €50k–€400k in engineering and certification costs, creating high switching costs that deter rapid changes even amid price rises. Project schedules for automotive and industrial clients often cannot absorb requalification delays, so suppliers gain bargaining power during tight delivery windows, reflected in 2024 industry on-time delivery premiums and contract waivers.

Lead-time volatility and scarcity

Semiconductor-heavy controls, sensors and drives face cyclical shortages and long lead times that force Grohmann to accept premium pricing or redesigns to maintain schedules. Time-to-ramp pressures on battery and automotive contracts compress procurement windows, increasing reliance on scarce suppliers. When components are constrained, suppliers can extract favorable payment, allocation and delivery terms.

Aftermarket parts and service lock-in

Installed Grohmann machinery relies on supplier-specific spare parts, firmware, and diagnostic tools, creating aftermarket lock-in that extends supplier influence beyond initial build, and as of 2024 Grohmann operates within Tesla Grohmann Automation in Prüm, Germany.

- Dependence on OEM parts drives requirement for OEM-approved components for uptime guarantees

- Warranty and access policies from suppliers constrain Grohmann’s service margins

- Supplier control over firmware/tools raises switching costs and bargaining power

Mitigation via dual-sourcing and design-for-availability

Grohmann GmbH, part of Tesla since the 2017 acquisition, reduces supplier power by engineering modular interfaces and qualifying multiple vendors to enable dual-sourcing and faster swaps.

Early demand visibility and frame agreements secure allocations, while interoperable component standards and strategic inventory buffers for critical parts smooth procurement risk.

- dual-sourcing

- modular-design

- frame-agreements

- interoperable-components

- inventory-buffers

Concentrated suppliers drive long requalification, high costs and premium delivery terms

Suppliers hold high leverage over Grohmann through concentrated supply of servomotors, controllers and vision systems, with requalification taking 3–9 months and costing €50k–€400k (2024), raising switching costs. Semiconductor-driven lead times and shortages push acceptance of premiums and constrained delivery terms. Aftermarket OEM parts and firmware lock-in extend supplier power despite Grohmann/Tesla mitigations.

| Metric | 2024 Value |

|---|---|

| Requalification time | 3–9 months |

| Requalification cost | €50k–€400k |

| Typical lead times (chips/controls) | 20–30 weeks |

What is included in the product

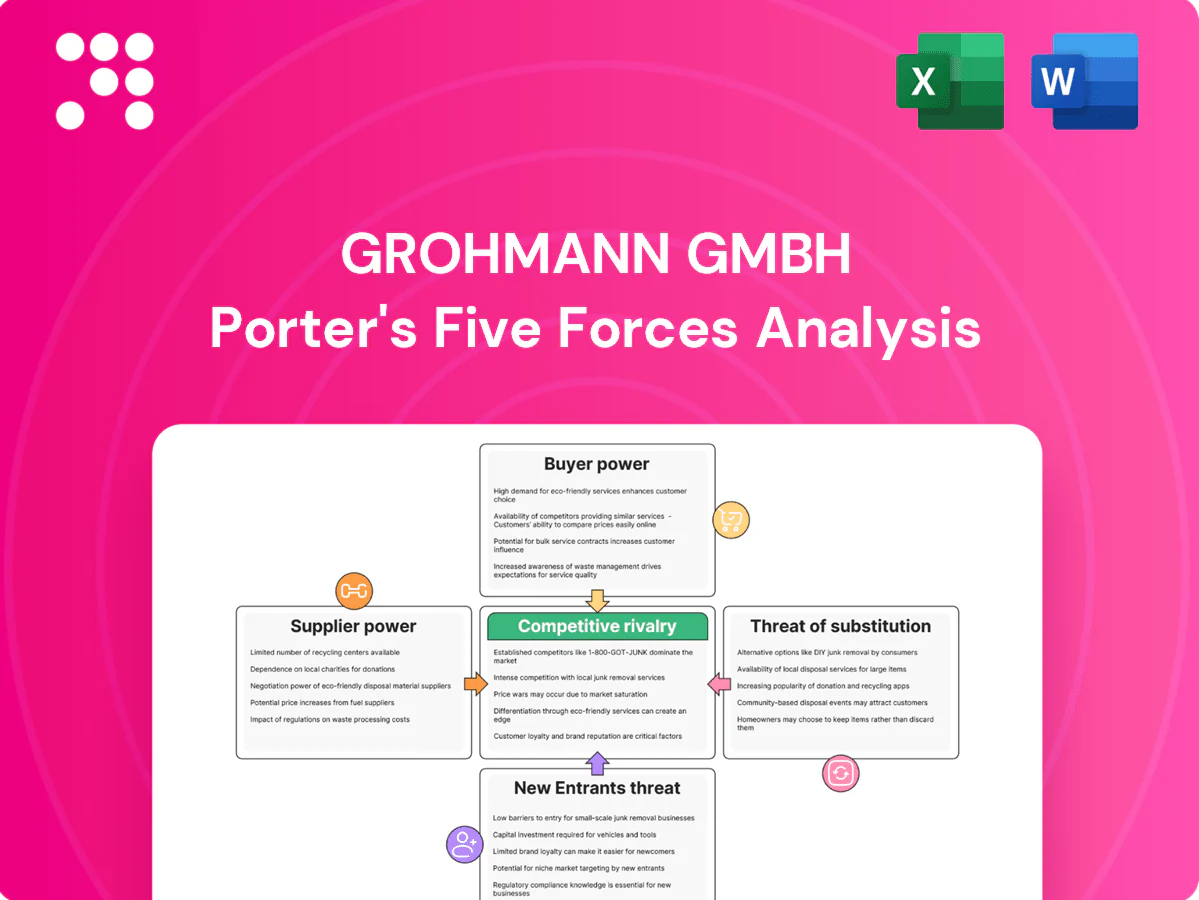

Tailored Porter's Five Forces analysis for Grohmann GmbH assessing competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and highlighting disruptive technologies and market dynamics that shape pricing, margins and strategic defenses.

A clear, one-sheet Porter's Five Forces for Grohmann GmbH—customizable pressure levels and instant spider-chart visualization to simplify competitive strategy and accelerate boardroom decision-making.

Customers Bargaining Power

Large OEMs and Tier-1s dominate demand

Customers in battery, automotive and electronics tend to be few, large and sophisticated—top OEMs (≈45% of global vehicle sales in 2024) and Tier‑1s drive demand and run competitive tenders that compress margins. Their purchasing scale forces customization without proportional price uplifts, while strict vendor lists and supplier audits (routine for >80% of OEMs) shift bargaining power decisively to buyers.

High switching costs post-installation

Once production lines are commissioned buyers face high switching costs tied to proprietary software, operator retraining and spare-part ecosystems, reinforcing lock-in; Grohmann (acquired by Tesla in 2017) leverages lifecycle service contracts and digital-twin offerings that extend dependency. These after-sales frameworks reduce buyer leverage over installed assets, while concentrating price pressure on new-capex expansions and upgrades.

Outcome-based KPIs drive concessions

Buyers demand throughput, yield and OEE KPIs with penalties for underperformance; average manufacturing OEE is ~60% versus world-class ~85% (2024 benchmarks). Performance guarantees and acceptance tests shift commissioning and uptime risk to suppliers, pressuring Grohmann to absorb performance risk. This dynamic often forces discounts, free engineering iterations and payment milestones tied to measurable outcomes.

Cyclical capex and budget timing

Cyclical capex in EV, battery and electronics—with global EV sales ~14.8 million units in 2024—makes OEM buyers highly timing-sensitive, using fiscal-deadline leverage to push deals and extract concessions. Project deferrals and backlog shifts during downturns compress supplier pricing power and increase negotiation leverage for buyers. Demand volatility in recessions materially boosts buyer bargaining power.

Preference for standardization

Buyers increasingly prefer platformed solutions to reduce site complexity; as of 2024 this trend raised pressure on suppliers to lower bespoke engineering margins and enabled easier price comparisons across vendors. For Grohmann this means balancing customization with configurable standard modules to protect margins while meeting customer demands.

- Reduced bespoke margins

- Stronger price transparency

- Need for configurable modules

OEMs ~45% influence, audits >80% squeeze margins; EVs 14.8M

Customers are few, large and powerful—top OEMs (~45% of global vehicle sales influence in 2024) run competitive tenders and >80% use strict audits, compressing margins. High switching costs and Grohmann’s lifecycle contracts create lock‑in, but price pressure remains on new capex. Buyers demand OEE/Yield guarantees (industry OEE ~60% vs world‑class 85% in 2024), and cyclical EV capex (14.8M EVs in 2024) amplifies timing leverage.

| Metric | 2024 Value |

|---|---|

| Global EV sales | 14.8M |

| OEM market influence | ~45% |

| OEM audits prevalence | >80% |

| Avg manufacturing OEE | ~60% (vs 85% world‑class) |

Preview the Actual Deliverable

Grohmann GmbH Porter's Five Forces Analysis

This preview shows the Grohmann GmbH Porter's Five Forces Analysis exactly as delivered—comprehensive, professionally formatted, and ready to download. The document you see is the final file you’ll receive immediately after purchase. No placeholders, no edits required.

A Must-Have Tool for Decision-Makers

Grohmann GmbH operates in a capital-intensive, high-tech manufacturing niche where supplier specialization and advanced automation create both barriers and opportunities; competitive rivalry is moderate but innovation-driven. This snapshot highlights key pressures—supplier power, buyer expectations, and substitute risks—without full force ratings. Unlock the complete Porter’s Five Forces Analysis for actionable, consultant-grade insights and visuals to inform strategy and investment decisions.

Suppliers Bargaining Power

Concentrated high-tech component base

Grohmann relies on precision components such as servomotors, motion controllers, machine vision and industrial PCs produced by a limited set of advanced suppliers. This concentration increases supplier leverage over pricing and lead times and, as of 2024, keeps switching costs high because many parts lack direct substitutes. Unique component roadmaps from suppliers further constrain Grohmann’s design choices and product timelines.

Switching costs in qualification

Qualifying alternative suppliers for safety-critical, high-precision automation commonly requires 3–9 months of testing and revalidation and can incur €50k–€400k in engineering and certification costs, creating high switching costs that deter rapid changes even amid price rises. Project schedules for automotive and industrial clients often cannot absorb requalification delays, so suppliers gain bargaining power during tight delivery windows, reflected in 2024 industry on-time delivery premiums and contract waivers.

Lead-time volatility and scarcity

Semiconductor-heavy controls, sensors and drives face cyclical shortages and long lead times that force Grohmann to accept premium pricing or redesigns to maintain schedules. Time-to-ramp pressures on battery and automotive contracts compress procurement windows, increasing reliance on scarce suppliers. When components are constrained, suppliers can extract favorable payment, allocation and delivery terms.

Aftermarket parts and service lock-in

Installed Grohmann machinery relies on supplier-specific spare parts, firmware, and diagnostic tools, creating aftermarket lock-in that extends supplier influence beyond initial build, and as of 2024 Grohmann operates within Tesla Grohmann Automation in Prüm, Germany.

- Dependence on OEM parts drives requirement for OEM-approved components for uptime guarantees

- Warranty and access policies from suppliers constrain Grohmann’s service margins

- Supplier control over firmware/tools raises switching costs and bargaining power

Mitigation via dual-sourcing and design-for-availability

Grohmann GmbH, part of Tesla since the 2017 acquisition, reduces supplier power by engineering modular interfaces and qualifying multiple vendors to enable dual-sourcing and faster swaps.

Early demand visibility and frame agreements secure allocations, while interoperable component standards and strategic inventory buffers for critical parts smooth procurement risk.

- dual-sourcing

- modular-design

- frame-agreements

- interoperable-components

- inventory-buffers

Concentrated suppliers drive long requalification, high costs and premium delivery terms

Suppliers hold high leverage over Grohmann through concentrated supply of servomotors, controllers and vision systems, with requalification taking 3–9 months and costing €50k–€400k (2024), raising switching costs. Semiconductor-driven lead times and shortages push acceptance of premiums and constrained delivery terms. Aftermarket OEM parts and firmware lock-in extend supplier power despite Grohmann/Tesla mitigations.

| Metric | 2024 Value |

|---|---|

| Requalification time | 3–9 months |

| Requalification cost | €50k–€400k |

| Typical lead times (chips/controls) | 20–30 weeks |

What is included in the product

Tailored Porter's Five Forces analysis for Grohmann GmbH assessing competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and highlighting disruptive technologies and market dynamics that shape pricing, margins and strategic defenses.

A clear, one-sheet Porter's Five Forces for Grohmann GmbH—customizable pressure levels and instant spider-chart visualization to simplify competitive strategy and accelerate boardroom decision-making.

Customers Bargaining Power

Large OEMs and Tier-1s dominate demand

Customers in battery, automotive and electronics tend to be few, large and sophisticated—top OEMs (≈45% of global vehicle sales in 2024) and Tier‑1s drive demand and run competitive tenders that compress margins. Their purchasing scale forces customization without proportional price uplifts, while strict vendor lists and supplier audits (routine for >80% of OEMs) shift bargaining power decisively to buyers.

High switching costs post-installation

Once production lines are commissioned buyers face high switching costs tied to proprietary software, operator retraining and spare-part ecosystems, reinforcing lock-in; Grohmann (acquired by Tesla in 2017) leverages lifecycle service contracts and digital-twin offerings that extend dependency. These after-sales frameworks reduce buyer leverage over installed assets, while concentrating price pressure on new-capex expansions and upgrades.

Outcome-based KPIs drive concessions

Buyers demand throughput, yield and OEE KPIs with penalties for underperformance; average manufacturing OEE is ~60% versus world-class ~85% (2024 benchmarks). Performance guarantees and acceptance tests shift commissioning and uptime risk to suppliers, pressuring Grohmann to absorb performance risk. This dynamic often forces discounts, free engineering iterations and payment milestones tied to measurable outcomes.

Cyclical capex and budget timing

Cyclical capex in EV, battery and electronics—with global EV sales ~14.8 million units in 2024—makes OEM buyers highly timing-sensitive, using fiscal-deadline leverage to push deals and extract concessions. Project deferrals and backlog shifts during downturns compress supplier pricing power and increase negotiation leverage for buyers. Demand volatility in recessions materially boosts buyer bargaining power.

Preference for standardization

Buyers increasingly prefer platformed solutions to reduce site complexity; as of 2024 this trend raised pressure on suppliers to lower bespoke engineering margins and enabled easier price comparisons across vendors. For Grohmann this means balancing customization with configurable standard modules to protect margins while meeting customer demands.

- Reduced bespoke margins

- Stronger price transparency

- Need for configurable modules

OEMs ~45% influence, audits >80% squeeze margins; EVs 14.8M

Customers are few, large and powerful—top OEMs (~45% of global vehicle sales influence in 2024) run competitive tenders and >80% use strict audits, compressing margins. High switching costs and Grohmann’s lifecycle contracts create lock‑in, but price pressure remains on new capex. Buyers demand OEE/Yield guarantees (industry OEE ~60% vs world‑class 85% in 2024), and cyclical EV capex (14.8M EVs in 2024) amplifies timing leverage.

| Metric | 2024 Value |

|---|---|

| Global EV sales | 14.8M |

| OEM market influence | ~45% |

| OEM audits prevalence | >80% |

| Avg manufacturing OEE | ~60% (vs 85% world‑class) |

Preview the Actual Deliverable

Grohmann GmbH Porter's Five Forces Analysis

This preview shows the Grohmann GmbH Porter's Five Forces Analysis exactly as delivered—comprehensive, professionally formatted, and ready to download. The document you see is the final file you’ll receive immediately after purchase. No placeholders, no edits required.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Grohmann GmbH operates in a capital-intensive, high-tech manufacturing niche where supplier specialization and advanced automation create both barriers and opportunities; competitive rivalry is moderate but innovation-driven. This snapshot highlights key pressures—supplier power, buyer expectations, and substitute risks—without full force ratings. Unlock the complete Porter’s Five Forces Analysis for actionable, consultant-grade insights and visuals to inform strategy and investment decisions.

Suppliers Bargaining Power

Concentrated high-tech component base

Grohmann relies on precision components such as servomotors, motion controllers, machine vision and industrial PCs produced by a limited set of advanced suppliers. This concentration increases supplier leverage over pricing and lead times and, as of 2024, keeps switching costs high because many parts lack direct substitutes. Unique component roadmaps from suppliers further constrain Grohmann’s design choices and product timelines.

Switching costs in qualification

Qualifying alternative suppliers for safety-critical, high-precision automation commonly requires 3–9 months of testing and revalidation and can incur €50k–€400k in engineering and certification costs, creating high switching costs that deter rapid changes even amid price rises. Project schedules for automotive and industrial clients often cannot absorb requalification delays, so suppliers gain bargaining power during tight delivery windows, reflected in 2024 industry on-time delivery premiums and contract waivers.

Lead-time volatility and scarcity

Semiconductor-heavy controls, sensors and drives face cyclical shortages and long lead times that force Grohmann to accept premium pricing or redesigns to maintain schedules. Time-to-ramp pressures on battery and automotive contracts compress procurement windows, increasing reliance on scarce suppliers. When components are constrained, suppliers can extract favorable payment, allocation and delivery terms.

Aftermarket parts and service lock-in

Installed Grohmann machinery relies on supplier-specific spare parts, firmware, and diagnostic tools, creating aftermarket lock-in that extends supplier influence beyond initial build, and as of 2024 Grohmann operates within Tesla Grohmann Automation in Prüm, Germany.

- Dependence on OEM parts drives requirement for OEM-approved components for uptime guarantees

- Warranty and access policies from suppliers constrain Grohmann’s service margins

- Supplier control over firmware/tools raises switching costs and bargaining power

Mitigation via dual-sourcing and design-for-availability

Grohmann GmbH, part of Tesla since the 2017 acquisition, reduces supplier power by engineering modular interfaces and qualifying multiple vendors to enable dual-sourcing and faster swaps.

Early demand visibility and frame agreements secure allocations, while interoperable component standards and strategic inventory buffers for critical parts smooth procurement risk.

- dual-sourcing

- modular-design

- frame-agreements

- interoperable-components

- inventory-buffers

Concentrated suppliers drive long requalification, high costs and premium delivery terms

Suppliers hold high leverage over Grohmann through concentrated supply of servomotors, controllers and vision systems, with requalification taking 3–9 months and costing €50k–€400k (2024), raising switching costs. Semiconductor-driven lead times and shortages push acceptance of premiums and constrained delivery terms. Aftermarket OEM parts and firmware lock-in extend supplier power despite Grohmann/Tesla mitigations.

| Metric | 2024 Value |

|---|---|

| Requalification time | 3–9 months |

| Requalification cost | €50k–€400k |

| Typical lead times (chips/controls) | 20–30 weeks |

What is included in the product

Tailored Porter's Five Forces analysis for Grohmann GmbH assessing competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and highlighting disruptive technologies and market dynamics that shape pricing, margins and strategic defenses.

A clear, one-sheet Porter's Five Forces for Grohmann GmbH—customizable pressure levels and instant spider-chart visualization to simplify competitive strategy and accelerate boardroom decision-making.

Customers Bargaining Power

Large OEMs and Tier-1s dominate demand

Customers in battery, automotive and electronics tend to be few, large and sophisticated—top OEMs (≈45% of global vehicle sales in 2024) and Tier‑1s drive demand and run competitive tenders that compress margins. Their purchasing scale forces customization without proportional price uplifts, while strict vendor lists and supplier audits (routine for >80% of OEMs) shift bargaining power decisively to buyers.

High switching costs post-installation

Once production lines are commissioned buyers face high switching costs tied to proprietary software, operator retraining and spare-part ecosystems, reinforcing lock-in; Grohmann (acquired by Tesla in 2017) leverages lifecycle service contracts and digital-twin offerings that extend dependency. These after-sales frameworks reduce buyer leverage over installed assets, while concentrating price pressure on new-capex expansions and upgrades.

Outcome-based KPIs drive concessions

Buyers demand throughput, yield and OEE KPIs with penalties for underperformance; average manufacturing OEE is ~60% versus world-class ~85% (2024 benchmarks). Performance guarantees and acceptance tests shift commissioning and uptime risk to suppliers, pressuring Grohmann to absorb performance risk. This dynamic often forces discounts, free engineering iterations and payment milestones tied to measurable outcomes.

Cyclical capex and budget timing

Cyclical capex in EV, battery and electronics—with global EV sales ~14.8 million units in 2024—makes OEM buyers highly timing-sensitive, using fiscal-deadline leverage to push deals and extract concessions. Project deferrals and backlog shifts during downturns compress supplier pricing power and increase negotiation leverage for buyers. Demand volatility in recessions materially boosts buyer bargaining power.

Preference for standardization

Buyers increasingly prefer platformed solutions to reduce site complexity; as of 2024 this trend raised pressure on suppliers to lower bespoke engineering margins and enabled easier price comparisons across vendors. For Grohmann this means balancing customization with configurable standard modules to protect margins while meeting customer demands.

- Reduced bespoke margins

- Stronger price transparency

- Need for configurable modules

OEMs ~45% influence, audits >80% squeeze margins; EVs 14.8M

Customers are few, large and powerful—top OEMs (~45% of global vehicle sales influence in 2024) run competitive tenders and >80% use strict audits, compressing margins. High switching costs and Grohmann’s lifecycle contracts create lock‑in, but price pressure remains on new capex. Buyers demand OEE/Yield guarantees (industry OEE ~60% vs world‑class 85% in 2024), and cyclical EV capex (14.8M EVs in 2024) amplifies timing leverage.

| Metric | 2024 Value |

|---|---|

| Global EV sales | 14.8M |

| OEM market influence | ~45% |

| OEM audits prevalence | >80% |

| Avg manufacturing OEE | ~60% (vs 85% world‑class) |

Preview the Actual Deliverable

Grohmann GmbH Porter's Five Forces Analysis

This preview shows the Grohmann GmbH Porter's Five Forces Analysis exactly as delivered—comprehensive, professionally formatted, and ready to download. The document you see is the final file you’ll receive immediately after purchase. No placeholders, no edits required.