Grosbill SA SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Grosbill SA’s SWOT highlights strong e‑commerce positioning and loyal customer base, tempered by competitive pressure and inventory risks. Discover strategic opportunities and hidden vulnerabilities that matter for investors and managers. Purchase the full SWOT analysis to get a research-backed, editable Word and Excel package for planning and pitching.

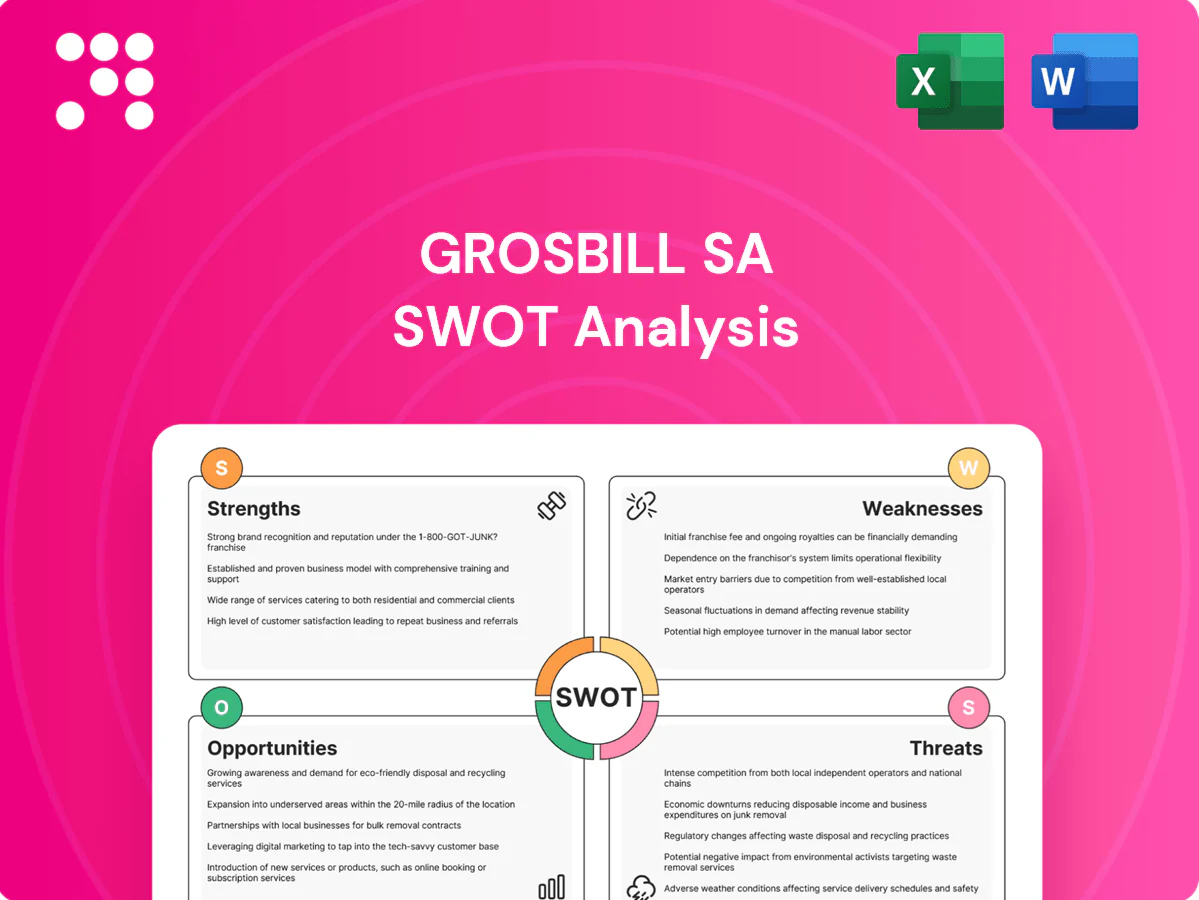

Strengths

Omnichannel presence

Operating both e-commerce and physical stores lets Grosbill meet customers where they are, enabling click-and-collect, in-store advice and nationwide delivery. This omnichannel model raises conversion by capturing intent across touchpoints and supports higher-margin upsells through personalized in-store advice. It also buffers demand fluctuations by shifting fulfillment between online and offline channels.

Wide tech assortment

Grosbill offers a broad catalog of computer hardware, electronics and high‑tech accessories with over 50,000 SKUs, supporting deep component selection that appeals to enthusiasts and professional buyers. This depth drives higher average order values and repeat purchases among specialist segments; in 2024 electronics categories accounted for a majority of site sales. Breadth enables basket‑building and cross‑selling, positioning Grosbill as a one‑stop shop for tech needs.

Value-added services

Product assembly, configuration and technical assistance let Grosbill SA compete on service rather than price, addressing complex PC and appliance purchases; McKinsey estimates strong after-sales can raise customer lifetime value by up to 20%. Services reduce purchase friction and build trust, with studies showing service-driven repeat rates add 10–20% incremental revenue. Robust post-sale support also boosts stickiness and referrals, increasing retention and word-of-mouth acquisition.

Consumer and B2B reach

Serving both consumers and professional clients diversifies Grosbill SA revenue, with B2B contracts delivering repeat, higher-ticket orders that smooth seasonality and stabilize cash flow. Mixed segments enhance purchasing leverage, strengthening vendor relationships through volume commitments and preferential terms.

- Diversified revenue: consumer + B2B

- Higher AOV from B2B repeat orders

- Smoother seasonality across segments

- Stronger vendor terms via volume commitments

Category expertise

Category expertise in IT and electronics gives Grosbill SA strong credibility with demanding tech buyers, translating into higher conversion rates among informed shoppers.

Deep staff expertise enables accurate product recommendations and faster problem-solving, reducing mispurchases and service load.

Fewer returns and higher satisfaction lower operating costs and support repeat purchases.

Expert positioning allows premium pricing on value-added services and curated bundles.

- Credibility with tech buyers

- Staff-driven accuracy

- Lower returns, higher NPS

- Premium services pricing

Omnichannel: 50,000+ SKUs, electronics-led, 20% CLV

Omnichannel retail (stores + e-commerce) boosts conversion via click-and-collect and in-store advice, smoothing demand across channels. A catalog of over 50,000 SKUs and 2024 electronics majority sales attract enthusiasts and raise AOV. Value-added assembly, technical support and B2B contracts increase retention and lifetime value (after-sales can add up to 20%).

| Metric | Value |

|---|---|

| SKUs | 50,000+ |

| Electronics share (2024) | Majority of site sales |

| CLV uplift from after-sales | Up to 20% |

What is included in the product

Provides a concise strategic overview of Grosbill SA’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decision-making.

Provides a concise, Grosbill SA–focused SWOT matrix for fast, visual strategy alignment, highlighting e‑commerce strengths, competitive threats, and supply‑chain risks for quick stakeholder decisions.

Weaknesses

Price sensitivity exposure

PC hardware and electronics retail typically operate on gross margins below 15%, leaving little room for error while shoppers—about 70–80% per recent e-commerce surveys—routinely benchmark prices against global e-tailers. Heavy reliance on discount-driven traffic, with promo depths often 10–30% during peak events, compresses profitability. Sustaining differentiation therefore requires continuous service, warranty and bundle innovation to protect margins.

Inventory risk

Rapid obsolescence in consumer electronics—global e‑waste reached 57.4 Mt in 2021 (UN) and smartphone replacement cycles averaged ~34 months in 2022 (Counterpoint)—raises markdown and write‑down risk for Grosbill. Managing thousands of SKUs across stores and online complicates forecasting, while launch-driven demand swings cause stockouts or overstock. Volatile cycles strain working capital and compress margins.

Scale disadvantages

Face à des géants comme Amazon (ventes nettes mondiales 2023: 514 milliards USD), Grosbill souffre d'un déficit d'échelle qui réduit son pouvoir d'achat et donc les remises fournisseurs et allocations exclusives.

Les coûts logistiques et du dernier kilomètre par unité sont généralement plus élevés pour un acteur local, et sa portée marketing reste nettement plus limitée.

Service capacity limits

Customized assembly and support are labor-intensive, limiting throughput and scaling. Peaks in demand create bottlenecks and longer lead times when technician capacity is exceeded. Quality hinges on technician availability and training, and variability in service can harm customer satisfaction and online reviews.

- Labor-intensive assembly reduces throughput

- Demand peaks cause bottlenecks and longer lead times

- Service quality depends on technician availability and training

- Variability can depress customer satisfaction and reviews

Brand awareness variability

Recognition is strong in Grosbill SA core regions but noticeably weaker nationally, limiting organic discovery outside established catchments. Limited mass-media spend reduces top-of-funnel acquisition, increasing dependence on performance channels; that reliance tends to raise customer acquisition cost and compress margins. This hinders scalable expansion into new areas.

- Regional brand concentration

- Low mass-media reach

- High reliance on performance marketing

- Raised CAC, constrained expansion

Electronics retail: thin margins, 70-80% price benchmarking, promos, market-leader scale

Thin retail gross margins (typically <15%) and heavy price-benchmarking (70–80% shoppers) compress profits; promos of 10–30% on peak events deepen the pressure. Fast obsolescence (global e‑waste 57.4 Mt in 2021) and thousands of SKUs raise markdown/write‑down and working‑capital risk. Scale gap vs Amazon (net sales 2023: 514 bn USD) limits purchasing power and logistics efficiency.

| Metric | Value |

|---|---|

| Typical gross margin | <15% |

| Shopper price‑benchmarks | 70–80% |

| Global e‑waste | 57.4 Mt (2021) |

| Amazon net sales | 514 bn USD (2023) |

Full Version Awaits

Grosbill SA SWOT Analysis

This is a real excerpt from the Grosbill SA SWOT analysis you’ll receive upon purchase—no placeholders or samples. The preview below is taken directly from the full, editable report, so what you see is what you’ll download after checkout. Purchase unlocks the complete, professionally structured document ready for use in strategy or valuation work.

Make Insightful Decisions Backed by Expert Research

Grosbill SA’s SWOT highlights strong e‑commerce positioning and loyal customer base, tempered by competitive pressure and inventory risks. Discover strategic opportunities and hidden vulnerabilities that matter for investors and managers. Purchase the full SWOT analysis to get a research-backed, editable Word and Excel package for planning and pitching.

Strengths

Omnichannel presence

Operating both e-commerce and physical stores lets Grosbill meet customers where they are, enabling click-and-collect, in-store advice and nationwide delivery. This omnichannel model raises conversion by capturing intent across touchpoints and supports higher-margin upsells through personalized in-store advice. It also buffers demand fluctuations by shifting fulfillment between online and offline channels.

Wide tech assortment

Grosbill offers a broad catalog of computer hardware, electronics and high‑tech accessories with over 50,000 SKUs, supporting deep component selection that appeals to enthusiasts and professional buyers. This depth drives higher average order values and repeat purchases among specialist segments; in 2024 electronics categories accounted for a majority of site sales. Breadth enables basket‑building and cross‑selling, positioning Grosbill as a one‑stop shop for tech needs.

Value-added services

Product assembly, configuration and technical assistance let Grosbill SA compete on service rather than price, addressing complex PC and appliance purchases; McKinsey estimates strong after-sales can raise customer lifetime value by up to 20%. Services reduce purchase friction and build trust, with studies showing service-driven repeat rates add 10–20% incremental revenue. Robust post-sale support also boosts stickiness and referrals, increasing retention and word-of-mouth acquisition.

Consumer and B2B reach

Serving both consumers and professional clients diversifies Grosbill SA revenue, with B2B contracts delivering repeat, higher-ticket orders that smooth seasonality and stabilize cash flow. Mixed segments enhance purchasing leverage, strengthening vendor relationships through volume commitments and preferential terms.

- Diversified revenue: consumer + B2B

- Higher AOV from B2B repeat orders

- Smoother seasonality across segments

- Stronger vendor terms via volume commitments

Category expertise

Category expertise in IT and electronics gives Grosbill SA strong credibility with demanding tech buyers, translating into higher conversion rates among informed shoppers.

Deep staff expertise enables accurate product recommendations and faster problem-solving, reducing mispurchases and service load.

Fewer returns and higher satisfaction lower operating costs and support repeat purchases.

Expert positioning allows premium pricing on value-added services and curated bundles.

- Credibility with tech buyers

- Staff-driven accuracy

- Lower returns, higher NPS

- Premium services pricing

Omnichannel: 50,000+ SKUs, electronics-led, 20% CLV

Omnichannel retail (stores + e-commerce) boosts conversion via click-and-collect and in-store advice, smoothing demand across channels. A catalog of over 50,000 SKUs and 2024 electronics majority sales attract enthusiasts and raise AOV. Value-added assembly, technical support and B2B contracts increase retention and lifetime value (after-sales can add up to 20%).

| Metric | Value |

|---|---|

| SKUs | 50,000+ |

| Electronics share (2024) | Majority of site sales |

| CLV uplift from after-sales | Up to 20% |

What is included in the product

Provides a concise strategic overview of Grosbill SA’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decision-making.

Provides a concise, Grosbill SA–focused SWOT matrix for fast, visual strategy alignment, highlighting e‑commerce strengths, competitive threats, and supply‑chain risks for quick stakeholder decisions.

Weaknesses

Price sensitivity exposure

PC hardware and electronics retail typically operate on gross margins below 15%, leaving little room for error while shoppers—about 70–80% per recent e-commerce surveys—routinely benchmark prices against global e-tailers. Heavy reliance on discount-driven traffic, with promo depths often 10–30% during peak events, compresses profitability. Sustaining differentiation therefore requires continuous service, warranty and bundle innovation to protect margins.

Inventory risk

Rapid obsolescence in consumer electronics—global e‑waste reached 57.4 Mt in 2021 (UN) and smartphone replacement cycles averaged ~34 months in 2022 (Counterpoint)—raises markdown and write‑down risk for Grosbill. Managing thousands of SKUs across stores and online complicates forecasting, while launch-driven demand swings cause stockouts or overstock. Volatile cycles strain working capital and compress margins.

Scale disadvantages

Face à des géants comme Amazon (ventes nettes mondiales 2023: 514 milliards USD), Grosbill souffre d'un déficit d'échelle qui réduit son pouvoir d'achat et donc les remises fournisseurs et allocations exclusives.

Les coûts logistiques et du dernier kilomètre par unité sont généralement plus élevés pour un acteur local, et sa portée marketing reste nettement plus limitée.

Service capacity limits

Customized assembly and support are labor-intensive, limiting throughput and scaling. Peaks in demand create bottlenecks and longer lead times when technician capacity is exceeded. Quality hinges on technician availability and training, and variability in service can harm customer satisfaction and online reviews.

- Labor-intensive assembly reduces throughput

- Demand peaks cause bottlenecks and longer lead times

- Service quality depends on technician availability and training

- Variability can depress customer satisfaction and reviews

Brand awareness variability

Recognition is strong in Grosbill SA core regions but noticeably weaker nationally, limiting organic discovery outside established catchments. Limited mass-media spend reduces top-of-funnel acquisition, increasing dependence on performance channels; that reliance tends to raise customer acquisition cost and compress margins. This hinders scalable expansion into new areas.

- Regional brand concentration

- Low mass-media reach

- High reliance on performance marketing

- Raised CAC, constrained expansion

Electronics retail: thin margins, 70-80% price benchmarking, promos, market-leader scale

Thin retail gross margins (typically <15%) and heavy price-benchmarking (70–80% shoppers) compress profits; promos of 10–30% on peak events deepen the pressure. Fast obsolescence (global e‑waste 57.4 Mt in 2021) and thousands of SKUs raise markdown/write‑down and working‑capital risk. Scale gap vs Amazon (net sales 2023: 514 bn USD) limits purchasing power and logistics efficiency.

| Metric | Value |

|---|---|

| Typical gross margin | <15% |

| Shopper price‑benchmarks | 70–80% |

| Global e‑waste | 57.4 Mt (2021) |

| Amazon net sales | 514 bn USD (2023) |

Full Version Awaits

Grosbill SA SWOT Analysis

This is a real excerpt from the Grosbill SA SWOT analysis you’ll receive upon purchase—no placeholders or samples. The preview below is taken directly from the full, editable report, so what you see is what you’ll download after checkout. Purchase unlocks the complete, professionally structured document ready for use in strategy or valuation work.

Description

Make Insightful Decisions Backed by Expert Research

Grosbill SA’s SWOT highlights strong e‑commerce positioning and loyal customer base, tempered by competitive pressure and inventory risks. Discover strategic opportunities and hidden vulnerabilities that matter for investors and managers. Purchase the full SWOT analysis to get a research-backed, editable Word and Excel package for planning and pitching.

Strengths

Omnichannel presence

Operating both e-commerce and physical stores lets Grosbill meet customers where they are, enabling click-and-collect, in-store advice and nationwide delivery. This omnichannel model raises conversion by capturing intent across touchpoints and supports higher-margin upsells through personalized in-store advice. It also buffers demand fluctuations by shifting fulfillment between online and offline channels.

Wide tech assortment

Grosbill offers a broad catalog of computer hardware, electronics and high‑tech accessories with over 50,000 SKUs, supporting deep component selection that appeals to enthusiasts and professional buyers. This depth drives higher average order values and repeat purchases among specialist segments; in 2024 electronics categories accounted for a majority of site sales. Breadth enables basket‑building and cross‑selling, positioning Grosbill as a one‑stop shop for tech needs.

Value-added services

Product assembly, configuration and technical assistance let Grosbill SA compete on service rather than price, addressing complex PC and appliance purchases; McKinsey estimates strong after-sales can raise customer lifetime value by up to 20%. Services reduce purchase friction and build trust, with studies showing service-driven repeat rates add 10–20% incremental revenue. Robust post-sale support also boosts stickiness and referrals, increasing retention and word-of-mouth acquisition.

Consumer and B2B reach

Serving both consumers and professional clients diversifies Grosbill SA revenue, with B2B contracts delivering repeat, higher-ticket orders that smooth seasonality and stabilize cash flow. Mixed segments enhance purchasing leverage, strengthening vendor relationships through volume commitments and preferential terms.

- Diversified revenue: consumer + B2B

- Higher AOV from B2B repeat orders

- Smoother seasonality across segments

- Stronger vendor terms via volume commitments

Category expertise

Category expertise in IT and electronics gives Grosbill SA strong credibility with demanding tech buyers, translating into higher conversion rates among informed shoppers.

Deep staff expertise enables accurate product recommendations and faster problem-solving, reducing mispurchases and service load.

Fewer returns and higher satisfaction lower operating costs and support repeat purchases.

Expert positioning allows premium pricing on value-added services and curated bundles.

- Credibility with tech buyers

- Staff-driven accuracy

- Lower returns, higher NPS

- Premium services pricing

Omnichannel: 50,000+ SKUs, electronics-led, 20% CLV

Omnichannel retail (stores + e-commerce) boosts conversion via click-and-collect and in-store advice, smoothing demand across channels. A catalog of over 50,000 SKUs and 2024 electronics majority sales attract enthusiasts and raise AOV. Value-added assembly, technical support and B2B contracts increase retention and lifetime value (after-sales can add up to 20%).

| Metric | Value |

|---|---|

| SKUs | 50,000+ |

| Electronics share (2024) | Majority of site sales |

| CLV uplift from after-sales | Up to 20% |

What is included in the product

Provides a concise strategic overview of Grosbill SA’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decision-making.

Provides a concise, Grosbill SA–focused SWOT matrix for fast, visual strategy alignment, highlighting e‑commerce strengths, competitive threats, and supply‑chain risks for quick stakeholder decisions.

Weaknesses

Price sensitivity exposure

PC hardware and electronics retail typically operate on gross margins below 15%, leaving little room for error while shoppers—about 70–80% per recent e-commerce surveys—routinely benchmark prices against global e-tailers. Heavy reliance on discount-driven traffic, with promo depths often 10–30% during peak events, compresses profitability. Sustaining differentiation therefore requires continuous service, warranty and bundle innovation to protect margins.

Inventory risk

Rapid obsolescence in consumer electronics—global e‑waste reached 57.4 Mt in 2021 (UN) and smartphone replacement cycles averaged ~34 months in 2022 (Counterpoint)—raises markdown and write‑down risk for Grosbill. Managing thousands of SKUs across stores and online complicates forecasting, while launch-driven demand swings cause stockouts or overstock. Volatile cycles strain working capital and compress margins.

Scale disadvantages

Face à des géants comme Amazon (ventes nettes mondiales 2023: 514 milliards USD), Grosbill souffre d'un déficit d'échelle qui réduit son pouvoir d'achat et donc les remises fournisseurs et allocations exclusives.

Les coûts logistiques et du dernier kilomètre par unité sont généralement plus élevés pour un acteur local, et sa portée marketing reste nettement plus limitée.

Service capacity limits

Customized assembly and support are labor-intensive, limiting throughput and scaling. Peaks in demand create bottlenecks and longer lead times when technician capacity is exceeded. Quality hinges on technician availability and training, and variability in service can harm customer satisfaction and online reviews.

- Labor-intensive assembly reduces throughput

- Demand peaks cause bottlenecks and longer lead times

- Service quality depends on technician availability and training

- Variability can depress customer satisfaction and reviews

Brand awareness variability

Recognition is strong in Grosbill SA core regions but noticeably weaker nationally, limiting organic discovery outside established catchments. Limited mass-media spend reduces top-of-funnel acquisition, increasing dependence on performance channels; that reliance tends to raise customer acquisition cost and compress margins. This hinders scalable expansion into new areas.

- Regional brand concentration

- Low mass-media reach

- High reliance on performance marketing

- Raised CAC, constrained expansion

Electronics retail: thin margins, 70-80% price benchmarking, promos, market-leader scale

Thin retail gross margins (typically <15%) and heavy price-benchmarking (70–80% shoppers) compress profits; promos of 10–30% on peak events deepen the pressure. Fast obsolescence (global e‑waste 57.4 Mt in 2021) and thousands of SKUs raise markdown/write‑down and working‑capital risk. Scale gap vs Amazon (net sales 2023: 514 bn USD) limits purchasing power and logistics efficiency.

| Metric | Value |

|---|---|

| Typical gross margin | <15% |

| Shopper price‑benchmarks | 70–80% |

| Global e‑waste | 57.4 Mt (2021) |

| Amazon net sales | 514 bn USD (2023) |

Full Version Awaits

Grosbill SA SWOT Analysis

This is a real excerpt from the Grosbill SA SWOT analysis you’ll receive upon purchase—no placeholders or samples. The preview below is taken directly from the full, editable report, so what you see is what you’ll download after checkout. Purchase unlocks the complete, professionally structured document ready for use in strategy or valuation work.