Bel SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Discover Bel’s strategic position with our full SWOT analysis—three concise sections revealing strengths, vulnerabilities, and market opportunities to inform smarter decisions. Purchase the complete, research-backed report (Word + editable Excel) for actionable insights, valuation context, and ready-to-use slides for investors, advisors, and executives.

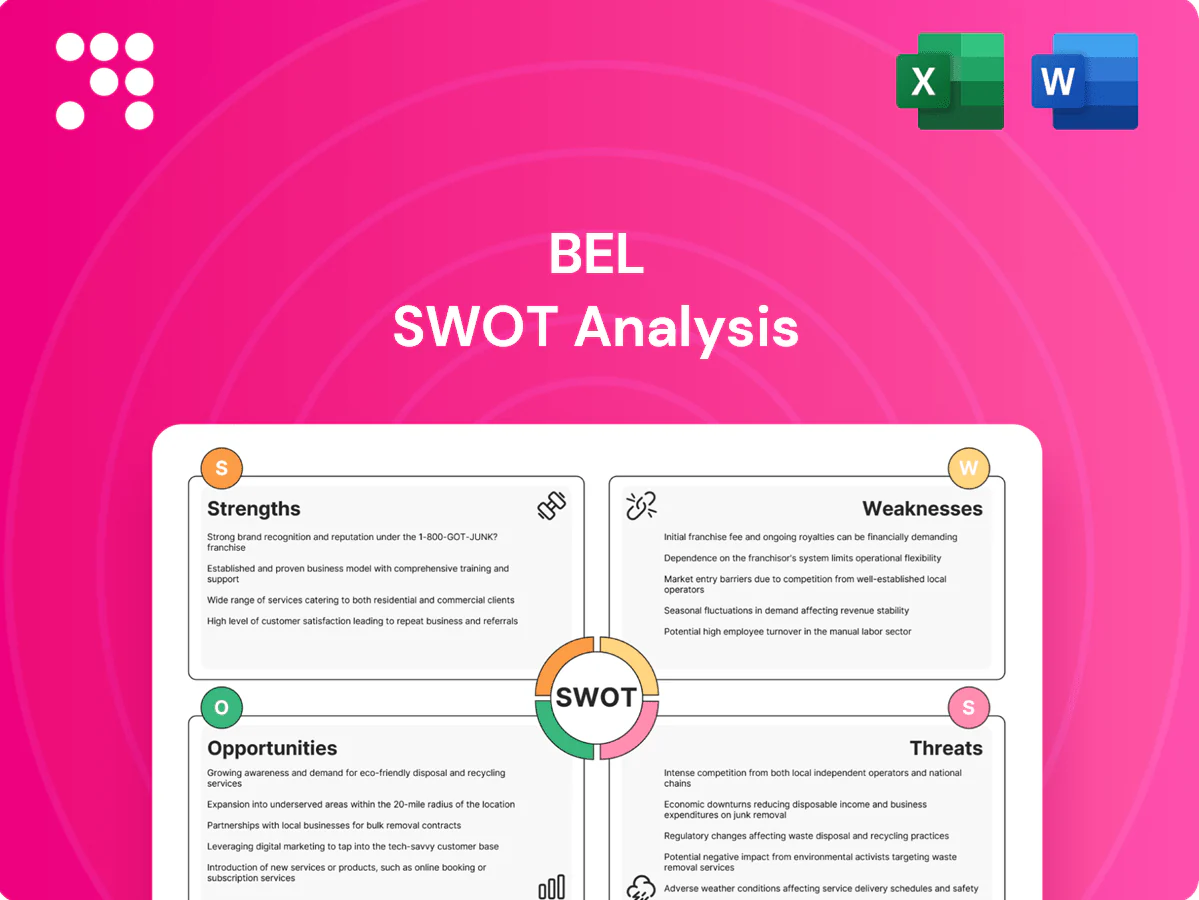

Strengths

Iconic global cheese brands

Core labels like The Laughing Cow boast 100+ years of heritage and recognition across 120+ countries, driving strong trust in portioned and snacking cheese.

Decades of consistent quality and marketing underpin pricing power and preferential shelf placement with major retailers.

Brands show cross-generational appeal and high repeat purchase patterns, while a diversified portfolio reduces single-brand exposure.

Portioned & snacking leadership

Groupe Bel’s portioned, ready-to-eat cheeses like Mini Babybel (standard 20 g wheels) are sold in more than 120 countries, aligning with on-the-go consumption. Consistent portion control, portable wax and film wrapping and shelf-lives up to six months support impulse channels and foodservice snacking. Specialized production lines and packaging know-how deliver high efficiency and scale for snacking formats.

Wide international footprint

Bel Group has a presence across Europe, North America, MENA and Asia, selling in over 120 countries which supports diversified revenue streams. Its ~30 production and packing sites in 13 countries shorten lead times and lower logistics costs. Route-to-market spans retail, convenience and e-commerce channels, and multi-market exposure lends resilience against regional demand shocks.

Innovation in health and reformulation

Bel drives continuous reformulation to improve nutrition profiles, increase portion transparency and add functional benefits, rolling reduced-salt and lower-fat variants alongside protein-forward propositions; plant-based and lactose-free extensions broaden the portfolio and support shifting consumer needs, while a steady innovation cadence protects brand and category relevance.

- Reduced-salt/reduced-fat SKUs

- Protein-forward launches

- Plant-based / lactose-free extensions

- Portion transparency & functional claims

Efficient supply chain partnerships

Bel leverages strategic sourcing of dairy inputs and multi-year supplier contracts to secure volumes and price stability, supporting group sales of about €3.7bn in 2023 and continued 2024 expansion into emerging markets.

Robust quality-assurance and end-to-end traceability meet EU standards, enabling scale benefits in procurement and co-manufacturing that compress COGS and improve margin visibility.

Advanced logistics and cold-chain expertise reduce spoilage and transport costs, supporting on-time delivery and tighter working capital versus peers.

- Long-term supplier contracts

- EU-grade traceability & QA

- Procurement scale & co-manufacturing

- Cold-chain reliability & cost control

Heritage cheese brands drive pricing power — €3.7bn, 120+ countries

Heritage brands (The Laughing Cow, Mini Babybel) drive global recognition and repeat purchases across 120+ countries, supporting pricing power and shelf prominence. Diversified portfolio and 30 production/packing sites in 13 countries lower logistics costs and shorten lead times. Strong procurement, EU-grade QA and cold-chain expertise compress COGS and supported group sales of about €3.7bn in 2023.

| Metric | Figure |

|---|---|

| Net sales (2023) | €3.7bn |

| Countries | 120+ |

| Production sites | ~30 (13 countries) |

| Brand heritage | 100+ years |

What is included in the product

Delivers a strategic overview of Bel’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position and future risks.

Provides a concise, Bel-specific SWOT matrix that relieves pain by enabling fast strategic alignment and clear stakeholder communication, with editable formatting for quick updates and easy integration into reports and presentations.

Weaknesses

High dairy input exposure

High exposure to milk makes Bel sensitive to dairy price volatility; EU farmgate milk jumped about 18% from 2021 to 2022 and remained elevated into 2024, compressing cheese margins. Cost spikes force either margin erosion or consumer price hikes, as passing through prices risks volume loss. Hedging is limited by contract timing and basis risk, while upstream weather and feed-cost swings (corn/soy) add further input volatility.

Concentration in cheese category

Bel derives the majority of its sales from cheese (core brands like Babybel and The Laughing Cow present in 120+ countries), creating exposure to category cyclicality and saturation in mature European markets where dairy volume growth is near zero; Bel has comparatively limited exposure to high-growth yogurts/beverages versus peers such as Danone, raising risk if consumer preferences pivot sharply away from processed cheese.

Dependence on hero SKUs

Dependence on hero SKUs concentrates a large share of Bel Group’s revenue—around €2.9bn in 2023—into flagship brands such as The Laughing Cow and Mini Babybel, amplifying single-product risk. This concentration heightens vulnerability to competitor imitation or retailer delisting, forcing sustained, high-intensity marketing spend to defend share. If a core SKU underperforms, portfolio turnover is slow, pressuring margins and cash flow.

Cold-chain and packaging intensity

Cold-chain needs drive higher logistics and energy costs, often 15–25% above ambient distribution, creating ongoing margin drag from complex multi-layer packaging and rising sustainability compliance (energy, refrigerants, recyclability). Significant capex is required for refrigeration units and specialized lines, and missed demand forecasting can produce perishables waste of 5–10% of volume.

- Higher logistics: +15–25% cost

- Packaging & sustainability: margin pressure

- Capex: refrigeration & specialized lines

- Waste risk: ~5–10% if forecasts fail

Regulatory and nutrition scrutiny

Bel faces rising regulatory and nutrition scrutiny—front-of-pack labeling and school food standards are expanding and UK HFSS rules (introduced Oct 2023) restrict promotions and enforce a 9pm TV watershed, forcing costly reformulation and potential margin pressure; advertising to children is limited in several markets and compliance varies across countries, increasing legal and operational complexity.

Milk +18% and logistics lift costs; €2.9bn cheese reliance squeezes margins

High milk exposure (EU farmgate milk +18% 2021–22; elevated into 2024) compresses cheese margins and limits hedging. Revenue concentration in cheese (flagships ~€2.9bn sales in 2023) raises single-SKU risk. Cold-chain/logistics add +15–25% cost and 5–10% waste; HFSS/FOPL rules drive reformulation costs.

| Metric | Value |

|---|---|

| Core cheese sales (2023) | €2.9bn |

| Milk price change 2021–22 | +18% |

| Logistics premium | +15–25% |

What You See Is What You Get

Bel SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the complete, editable version becomes available after payment. Buy now to download the full, structured file.

Dive Deeper Into the Company’s Strategic Blueprint

Discover Bel’s strategic position with our full SWOT analysis—three concise sections revealing strengths, vulnerabilities, and market opportunities to inform smarter decisions. Purchase the complete, research-backed report (Word + editable Excel) for actionable insights, valuation context, and ready-to-use slides for investors, advisors, and executives.

Strengths

Iconic global cheese brands

Core labels like The Laughing Cow boast 100+ years of heritage and recognition across 120+ countries, driving strong trust in portioned and snacking cheese.

Decades of consistent quality and marketing underpin pricing power and preferential shelf placement with major retailers.

Brands show cross-generational appeal and high repeat purchase patterns, while a diversified portfolio reduces single-brand exposure.

Portioned & snacking leadership

Groupe Bel’s portioned, ready-to-eat cheeses like Mini Babybel (standard 20 g wheels) are sold in more than 120 countries, aligning with on-the-go consumption. Consistent portion control, portable wax and film wrapping and shelf-lives up to six months support impulse channels and foodservice snacking. Specialized production lines and packaging know-how deliver high efficiency and scale for snacking formats.

Wide international footprint

Bel Group has a presence across Europe, North America, MENA and Asia, selling in over 120 countries which supports diversified revenue streams. Its ~30 production and packing sites in 13 countries shorten lead times and lower logistics costs. Route-to-market spans retail, convenience and e-commerce channels, and multi-market exposure lends resilience against regional demand shocks.

Innovation in health and reformulation

Bel drives continuous reformulation to improve nutrition profiles, increase portion transparency and add functional benefits, rolling reduced-salt and lower-fat variants alongside protein-forward propositions; plant-based and lactose-free extensions broaden the portfolio and support shifting consumer needs, while a steady innovation cadence protects brand and category relevance.

- Reduced-salt/reduced-fat SKUs

- Protein-forward launches

- Plant-based / lactose-free extensions

- Portion transparency & functional claims

Efficient supply chain partnerships

Bel leverages strategic sourcing of dairy inputs and multi-year supplier contracts to secure volumes and price stability, supporting group sales of about €3.7bn in 2023 and continued 2024 expansion into emerging markets.

Robust quality-assurance and end-to-end traceability meet EU standards, enabling scale benefits in procurement and co-manufacturing that compress COGS and improve margin visibility.

Advanced logistics and cold-chain expertise reduce spoilage and transport costs, supporting on-time delivery and tighter working capital versus peers.

- Long-term supplier contracts

- EU-grade traceability & QA

- Procurement scale & co-manufacturing

- Cold-chain reliability & cost control

Heritage cheese brands drive pricing power — €3.7bn, 120+ countries

Heritage brands (The Laughing Cow, Mini Babybel) drive global recognition and repeat purchases across 120+ countries, supporting pricing power and shelf prominence. Diversified portfolio and 30 production/packing sites in 13 countries lower logistics costs and shorten lead times. Strong procurement, EU-grade QA and cold-chain expertise compress COGS and supported group sales of about €3.7bn in 2023.

| Metric | Figure |

|---|---|

| Net sales (2023) | €3.7bn |

| Countries | 120+ |

| Production sites | ~30 (13 countries) |

| Brand heritage | 100+ years |

What is included in the product

Delivers a strategic overview of Bel’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position and future risks.

Provides a concise, Bel-specific SWOT matrix that relieves pain by enabling fast strategic alignment and clear stakeholder communication, with editable formatting for quick updates and easy integration into reports and presentations.

Weaknesses

High dairy input exposure

High exposure to milk makes Bel sensitive to dairy price volatility; EU farmgate milk jumped about 18% from 2021 to 2022 and remained elevated into 2024, compressing cheese margins. Cost spikes force either margin erosion or consumer price hikes, as passing through prices risks volume loss. Hedging is limited by contract timing and basis risk, while upstream weather and feed-cost swings (corn/soy) add further input volatility.

Concentration in cheese category

Bel derives the majority of its sales from cheese (core brands like Babybel and The Laughing Cow present in 120+ countries), creating exposure to category cyclicality and saturation in mature European markets where dairy volume growth is near zero; Bel has comparatively limited exposure to high-growth yogurts/beverages versus peers such as Danone, raising risk if consumer preferences pivot sharply away from processed cheese.

Dependence on hero SKUs

Dependence on hero SKUs concentrates a large share of Bel Group’s revenue—around €2.9bn in 2023—into flagship brands such as The Laughing Cow and Mini Babybel, amplifying single-product risk. This concentration heightens vulnerability to competitor imitation or retailer delisting, forcing sustained, high-intensity marketing spend to defend share. If a core SKU underperforms, portfolio turnover is slow, pressuring margins and cash flow.

Cold-chain and packaging intensity

Cold-chain needs drive higher logistics and energy costs, often 15–25% above ambient distribution, creating ongoing margin drag from complex multi-layer packaging and rising sustainability compliance (energy, refrigerants, recyclability). Significant capex is required for refrigeration units and specialized lines, and missed demand forecasting can produce perishables waste of 5–10% of volume.

- Higher logistics: +15–25% cost

- Packaging & sustainability: margin pressure

- Capex: refrigeration & specialized lines

- Waste risk: ~5–10% if forecasts fail

Regulatory and nutrition scrutiny

Bel faces rising regulatory and nutrition scrutiny—front-of-pack labeling and school food standards are expanding and UK HFSS rules (introduced Oct 2023) restrict promotions and enforce a 9pm TV watershed, forcing costly reformulation and potential margin pressure; advertising to children is limited in several markets and compliance varies across countries, increasing legal and operational complexity.

Milk +18% and logistics lift costs; €2.9bn cheese reliance squeezes margins

High milk exposure (EU farmgate milk +18% 2021–22; elevated into 2024) compresses cheese margins and limits hedging. Revenue concentration in cheese (flagships ~€2.9bn sales in 2023) raises single-SKU risk. Cold-chain/logistics add +15–25% cost and 5–10% waste; HFSS/FOPL rules drive reformulation costs.

| Metric | Value |

|---|---|

| Core cheese sales (2023) | €2.9bn |

| Milk price change 2021–22 | +18% |

| Logistics premium | +15–25% |

What You See Is What You Get

Bel SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the complete, editable version becomes available after payment. Buy now to download the full, structured file.

Description

Dive Deeper Into the Company’s Strategic Blueprint

Discover Bel’s strategic position with our full SWOT analysis—three concise sections revealing strengths, vulnerabilities, and market opportunities to inform smarter decisions. Purchase the complete, research-backed report (Word + editable Excel) for actionable insights, valuation context, and ready-to-use slides for investors, advisors, and executives.

Strengths

Iconic global cheese brands

Core labels like The Laughing Cow boast 100+ years of heritage and recognition across 120+ countries, driving strong trust in portioned and snacking cheese.

Decades of consistent quality and marketing underpin pricing power and preferential shelf placement with major retailers.

Brands show cross-generational appeal and high repeat purchase patterns, while a diversified portfolio reduces single-brand exposure.

Portioned & snacking leadership

Groupe Bel’s portioned, ready-to-eat cheeses like Mini Babybel (standard 20 g wheels) are sold in more than 120 countries, aligning with on-the-go consumption. Consistent portion control, portable wax and film wrapping and shelf-lives up to six months support impulse channels and foodservice snacking. Specialized production lines and packaging know-how deliver high efficiency and scale for snacking formats.

Wide international footprint

Bel Group has a presence across Europe, North America, MENA and Asia, selling in over 120 countries which supports diversified revenue streams. Its ~30 production and packing sites in 13 countries shorten lead times and lower logistics costs. Route-to-market spans retail, convenience and e-commerce channels, and multi-market exposure lends resilience against regional demand shocks.

Innovation in health and reformulation

Bel drives continuous reformulation to improve nutrition profiles, increase portion transparency and add functional benefits, rolling reduced-salt and lower-fat variants alongside protein-forward propositions; plant-based and lactose-free extensions broaden the portfolio and support shifting consumer needs, while a steady innovation cadence protects brand and category relevance.

- Reduced-salt/reduced-fat SKUs

- Protein-forward launches

- Plant-based / lactose-free extensions

- Portion transparency & functional claims

Efficient supply chain partnerships

Bel leverages strategic sourcing of dairy inputs and multi-year supplier contracts to secure volumes and price stability, supporting group sales of about €3.7bn in 2023 and continued 2024 expansion into emerging markets.

Robust quality-assurance and end-to-end traceability meet EU standards, enabling scale benefits in procurement and co-manufacturing that compress COGS and improve margin visibility.

Advanced logistics and cold-chain expertise reduce spoilage and transport costs, supporting on-time delivery and tighter working capital versus peers.

- Long-term supplier contracts

- EU-grade traceability & QA

- Procurement scale & co-manufacturing

- Cold-chain reliability & cost control

Heritage cheese brands drive pricing power — €3.7bn, 120+ countries

Heritage brands (The Laughing Cow, Mini Babybel) drive global recognition and repeat purchases across 120+ countries, supporting pricing power and shelf prominence. Diversified portfolio and 30 production/packing sites in 13 countries lower logistics costs and shorten lead times. Strong procurement, EU-grade QA and cold-chain expertise compress COGS and supported group sales of about €3.7bn in 2023.

| Metric | Figure |

|---|---|

| Net sales (2023) | €3.7bn |

| Countries | 120+ |

| Production sites | ~30 (13 countries) |

| Brand heritage | 100+ years |

What is included in the product

Delivers a strategic overview of Bel’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position and future risks.

Provides a concise, Bel-specific SWOT matrix that relieves pain by enabling fast strategic alignment and clear stakeholder communication, with editable formatting for quick updates and easy integration into reports and presentations.

Weaknesses

High dairy input exposure

High exposure to milk makes Bel sensitive to dairy price volatility; EU farmgate milk jumped about 18% from 2021 to 2022 and remained elevated into 2024, compressing cheese margins. Cost spikes force either margin erosion or consumer price hikes, as passing through prices risks volume loss. Hedging is limited by contract timing and basis risk, while upstream weather and feed-cost swings (corn/soy) add further input volatility.

Concentration in cheese category

Bel derives the majority of its sales from cheese (core brands like Babybel and The Laughing Cow present in 120+ countries), creating exposure to category cyclicality and saturation in mature European markets where dairy volume growth is near zero; Bel has comparatively limited exposure to high-growth yogurts/beverages versus peers such as Danone, raising risk if consumer preferences pivot sharply away from processed cheese.

Dependence on hero SKUs

Dependence on hero SKUs concentrates a large share of Bel Group’s revenue—around €2.9bn in 2023—into flagship brands such as The Laughing Cow and Mini Babybel, amplifying single-product risk. This concentration heightens vulnerability to competitor imitation or retailer delisting, forcing sustained, high-intensity marketing spend to defend share. If a core SKU underperforms, portfolio turnover is slow, pressuring margins and cash flow.

Cold-chain and packaging intensity

Cold-chain needs drive higher logistics and energy costs, often 15–25% above ambient distribution, creating ongoing margin drag from complex multi-layer packaging and rising sustainability compliance (energy, refrigerants, recyclability). Significant capex is required for refrigeration units and specialized lines, and missed demand forecasting can produce perishables waste of 5–10% of volume.

- Higher logistics: +15–25% cost

- Packaging & sustainability: margin pressure

- Capex: refrigeration & specialized lines

- Waste risk: ~5–10% if forecasts fail

Regulatory and nutrition scrutiny

Bel faces rising regulatory and nutrition scrutiny—front-of-pack labeling and school food standards are expanding and UK HFSS rules (introduced Oct 2023) restrict promotions and enforce a 9pm TV watershed, forcing costly reformulation and potential margin pressure; advertising to children is limited in several markets and compliance varies across countries, increasing legal and operational complexity.

Milk +18% and logistics lift costs; €2.9bn cheese reliance squeezes margins

High milk exposure (EU farmgate milk +18% 2021–22; elevated into 2024) compresses cheese margins and limits hedging. Revenue concentration in cheese (flagships ~€2.9bn sales in 2023) raises single-SKU risk. Cold-chain/logistics add +15–25% cost and 5–10% waste; HFSS/FOPL rules drive reformulation costs.

| Metric | Value |

|---|---|

| Core cheese sales (2023) | €2.9bn |

| Milk price change 2021–22 | +18% |

| Logistics premium | +15–25% |

What You See Is What You Get

Bel SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the complete, editable version becomes available after payment. Buy now to download the full, structured file.