Grove Collaborative Porter's Five Forces Analysis

From Overview to Strategy Blueprint

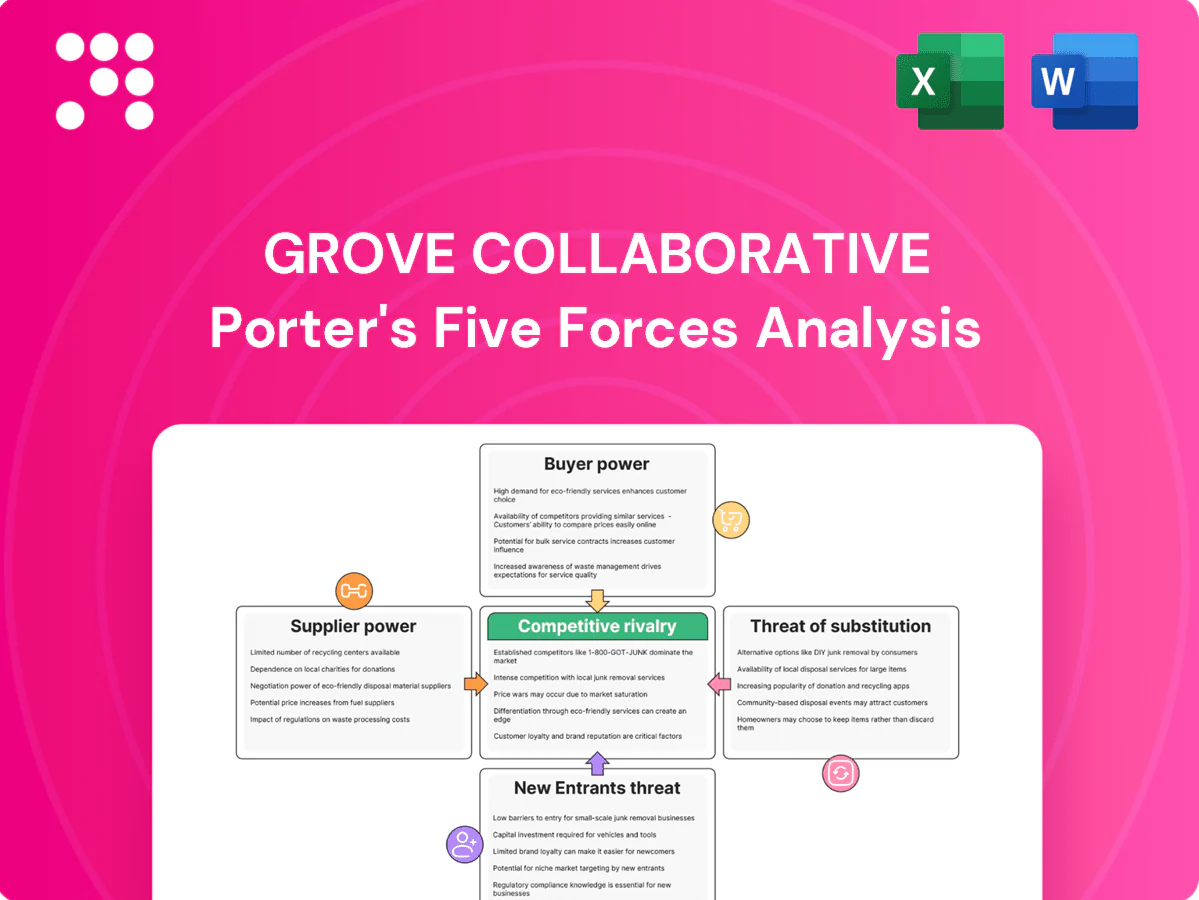

Grove Collaborative faces intense buyer power and growing substitute threats as consumers shift to sustainable, cost-conscious options; supplier influence and channel dynamics further pressure margins. Competitive rivalry is strong across DTC and retail, while entry barriers remain moderate amid brand and distribution investments. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Grove Collaborative’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated eco-suppliers

Concentrated eco-suppliers give Grove leverage challenges as many certified sustainable raw-material and packaging sources are limited, creating price and contractual power for suppliers. Niche inputs like plant-based surfactants, FSC paper and aluminum packaging can bottleneck supply, forcing Grove to balance ethics and availability; FSC-certified forests exceed 200 million hectares (2024). This concentration raises switching costs and stockout risk, pressuring margins and inventory management.

Private label leverage

Grove’s private-label assortment shifts volume to controlled formulations, diluting supplier power and improving margin capture; private-label penetration in U.S. household and personal care reached about 18% in 2024. Contract manufacturers can be multi-sourced to drive 5–10% procurement savings, but stringent quality and certification requirements limit vendor pools. Sustained bargaining strength hinges on scale efficiencies and SKU rationalization.

Logistics and fulfillment dependence

Grove Collaborative relies heavily on 3PLs, carriers and packaging vendors, exposing it to fuel surcharges and carrier capacity prioritization that the US 3PL market — about $239 billion in 2024 — helped dictate; peak-season constraints often compress margins. Sustainable packaging specs narrow qualified vendor pools and raise unit costs. Diversifying carriers and packaging SKUs reduces single-supplier leverage and improves negotiating flexibility.

Certification and compliance gatekeepers

Certifiers and testing labs like EPA Safer Choice and Leaping Bunny act as indirect suppliers whose standards and approval timelines directly affect Grove Collaborative’s cost structure and speed-to-market; delays can defer product launches and compress margins. Losing certification erodes brand equity and pricing power, while compliance costs—testing, reformulation, audits—are often passed through by upstream vendors, squeezing EBIT.

- 2024: certifications gate product entry

- Compliance raises COGS and time-to-revenue

- Certification loss damages pricing leverage

Branded partner dependence

Some third-party eco-brands carry strong customer loyalty that constrains Grove Collaborative’s negotiating leverage; exclusive SKUs and MAP policies from those partners limit Grove’s ability to offer deeper discounts and compress margin flexibility. Grove’s core value rests on assortment breadth, which reduces its walk-away power because removing a popular partner risks customer churn. Strategic co-marketing and shared promotions can help rebalance economics by improving joint sell-through and offsetting supplier constraints.

- Branded partner pull limits price negotiation

- Exclusive SKUs and MAP cap discounting

- Assortment breadth reduces Grove walk-away power

- Co-marketing can rebalance supplier economics

Concentrated eco-suppliers raise price risk; private-labels and CM cut margin pressure

Concentrated eco-suppliers and niche inputs (FSC >200M ha, 2024) give suppliers price and contractual leverage, raising switching costs and stockout risk. Grove’s private-label (18% US household/personal care, 2024) and multi-sourced CM strategies (5–10% savings) partially offset supplier power. 3PL/packaging market size ~$239B (US, 2024) and certification bottlenecks further constrain margins.

| Metric | 2024 |

|---|---|

| FSC area | 200M ha |

| Private-label share | 18% |

| US 3PL market | $239B |

What is included in the product

Tailored Porter's Five Forces analysis for Grove Collaborative that uncovers key drivers of competition, buyer and supplier power, and market entry risks specific to sustainable household products. Identifies disruptive substitutes, emerging threats, and strategic barriers that shape pricing, profitability, and long-term market position.

A concise one-sheet Porter's Five Forces for Grove Collaborative that highlights supplier power, buyer dynamics, competitive threats and substitution risk—perfect for quick strategic decisions, pitch decks, or aligning teams on priority pain points.

Customers Bargaining Power

Low switching costs

Low switching costs let consumers jump to Amazon (roughly 40% of US e‑commerce in 2024) or brand sites with a few clicks; cleaning and personal‑care SKUs are highly comparable. Free‑shipping incentives (typical $35 threshold) and promotions, plus Amazon Prime’s >200 million members, intensify churn. Grove must defend via tight curation, values alignment, and superior convenience.

Price sensitivity amid essentials

Household essentials are basket-driven so even 5% price gaps shift brand choice; 2024 US CPI ran near 3% year-over-year (BLS), increasing price elasticity for staples. Grove’s subscription model smooths perceived price volatility but industry subscription churn rose toward ~30% annual in 2024 if perceived value dropped. Transparent savings and bundled pricing have proven effective countermeasures.

Subscription stickiness vs churn risk

Auto-ship at Grove Collaborative increases predictability and reduces active comparison, lowering buyer power, and in 2024 the company emphasized subscription experiences to boost lifetime value. Yet pausing or canceling remains trivial online, keeping retention fragile. Personalization and accurate refill timing raise perceived utility and reduce friction. Loyalty perks and targeted discounts further cushion churn by raising switching costs.

Values-driven but choice-rich

Eco-conscious buyers prioritize sustainability but face many retailers' green lines, raising switching options and price sensitivity; reviews and UGC magnify collective bargaining power, demanding transparency in ingredients, lifecycle and certifications. Grove Collaborative reported revenue near $169M in FY2023, so clear impact metrics can justify premiums and reduce churn.

- Buyers demand proof: certifications, full ingredients

- UGC/reviews amplify leverage

- Clear metrics justify premium pricing

Bulk and bundle negotiators

High-LTV customers at Grove Collaborative use bundles, subscriptions, and seasonal buys to improve unit economics, pressuring promo cadence and inventory allocation. They demand free shipping and flexible returns, forcing higher fulfillment costs and tighter margin management. Their purchase patterns increasingly dictate dynamic pricing and margin mix; tiered rewards can steer volume toward profitable SKUs.

- Customers: bundle/subscription driven

- Expectations: free shipping, flexible returns

- Impact: pricing strategy, margin mix

- Levers: tiered rewards to align volume with profitability

Moderate-high consumer power: low switching vs Amazon, rev $169M, churn ~30%

Customers hold moderate-to-high bargaining power: low switching costs vs Amazon (~40% US e‑commerce 2024) and Prime >200M, price sensitivity up as 2024 US CPI ~3%, subscription churn ~30% (2024). Grove revenue $169M FY2023; curation, bundles and subscription UX are key retention levers.

| Metric | Value |

|---|---|

| Amazon share | ~40% |

| Prime members | >200M |

| CPI 2024 | ~3% |

| Grove rev | $169M FY2023 |

| Sub churn 2024 | ~30% |

Preview the Actual Deliverable

Grove Collaborative Porter's Five Forces Analysis

This Grove Collaborative Porter’s Five Forces analysis evaluates competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry with concise, actionable insights. The preview you see is the exact, professionally formatted document you’ll receive upon purchase. No placeholders or samples — it’s ready for immediate download and use. The findings support strategic and investment decisions.

From Overview to Strategy Blueprint

Grove Collaborative faces intense buyer power and growing substitute threats as consumers shift to sustainable, cost-conscious options; supplier influence and channel dynamics further pressure margins. Competitive rivalry is strong across DTC and retail, while entry barriers remain moderate amid brand and distribution investments. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Grove Collaborative’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated eco-suppliers

Concentrated eco-suppliers give Grove leverage challenges as many certified sustainable raw-material and packaging sources are limited, creating price and contractual power for suppliers. Niche inputs like plant-based surfactants, FSC paper and aluminum packaging can bottleneck supply, forcing Grove to balance ethics and availability; FSC-certified forests exceed 200 million hectares (2024). This concentration raises switching costs and stockout risk, pressuring margins and inventory management.

Private label leverage

Grove’s private-label assortment shifts volume to controlled formulations, diluting supplier power and improving margin capture; private-label penetration in U.S. household and personal care reached about 18% in 2024. Contract manufacturers can be multi-sourced to drive 5–10% procurement savings, but stringent quality and certification requirements limit vendor pools. Sustained bargaining strength hinges on scale efficiencies and SKU rationalization.

Logistics and fulfillment dependence

Grove Collaborative relies heavily on 3PLs, carriers and packaging vendors, exposing it to fuel surcharges and carrier capacity prioritization that the US 3PL market — about $239 billion in 2024 — helped dictate; peak-season constraints often compress margins. Sustainable packaging specs narrow qualified vendor pools and raise unit costs. Diversifying carriers and packaging SKUs reduces single-supplier leverage and improves negotiating flexibility.

Certification and compliance gatekeepers

Certifiers and testing labs like EPA Safer Choice and Leaping Bunny act as indirect suppliers whose standards and approval timelines directly affect Grove Collaborative’s cost structure and speed-to-market; delays can defer product launches and compress margins. Losing certification erodes brand equity and pricing power, while compliance costs—testing, reformulation, audits—are often passed through by upstream vendors, squeezing EBIT.

- 2024: certifications gate product entry

- Compliance raises COGS and time-to-revenue

- Certification loss damages pricing leverage

Branded partner dependence

Some third-party eco-brands carry strong customer loyalty that constrains Grove Collaborative’s negotiating leverage; exclusive SKUs and MAP policies from those partners limit Grove’s ability to offer deeper discounts and compress margin flexibility. Grove’s core value rests on assortment breadth, which reduces its walk-away power because removing a popular partner risks customer churn. Strategic co-marketing and shared promotions can help rebalance economics by improving joint sell-through and offsetting supplier constraints.

- Branded partner pull limits price negotiation

- Exclusive SKUs and MAP cap discounting

- Assortment breadth reduces Grove walk-away power

- Co-marketing can rebalance supplier economics

Concentrated eco-suppliers raise price risk; private-labels and CM cut margin pressure

Concentrated eco-suppliers and niche inputs (FSC >200M ha, 2024) give suppliers price and contractual leverage, raising switching costs and stockout risk. Grove’s private-label (18% US household/personal care, 2024) and multi-sourced CM strategies (5–10% savings) partially offset supplier power. 3PL/packaging market size ~$239B (US, 2024) and certification bottlenecks further constrain margins.

| Metric | 2024 |

|---|---|

| FSC area | 200M ha |

| Private-label share | 18% |

| US 3PL market | $239B |

What is included in the product

Tailored Porter's Five Forces analysis for Grove Collaborative that uncovers key drivers of competition, buyer and supplier power, and market entry risks specific to sustainable household products. Identifies disruptive substitutes, emerging threats, and strategic barriers that shape pricing, profitability, and long-term market position.

A concise one-sheet Porter's Five Forces for Grove Collaborative that highlights supplier power, buyer dynamics, competitive threats and substitution risk—perfect for quick strategic decisions, pitch decks, or aligning teams on priority pain points.

Customers Bargaining Power

Low switching costs

Low switching costs let consumers jump to Amazon (roughly 40% of US e‑commerce in 2024) or brand sites with a few clicks; cleaning and personal‑care SKUs are highly comparable. Free‑shipping incentives (typical $35 threshold) and promotions, plus Amazon Prime’s >200 million members, intensify churn. Grove must defend via tight curation, values alignment, and superior convenience.

Price sensitivity amid essentials

Household essentials are basket-driven so even 5% price gaps shift brand choice; 2024 US CPI ran near 3% year-over-year (BLS), increasing price elasticity for staples. Grove’s subscription model smooths perceived price volatility but industry subscription churn rose toward ~30% annual in 2024 if perceived value dropped. Transparent savings and bundled pricing have proven effective countermeasures.

Subscription stickiness vs churn risk

Auto-ship at Grove Collaborative increases predictability and reduces active comparison, lowering buyer power, and in 2024 the company emphasized subscription experiences to boost lifetime value. Yet pausing or canceling remains trivial online, keeping retention fragile. Personalization and accurate refill timing raise perceived utility and reduce friction. Loyalty perks and targeted discounts further cushion churn by raising switching costs.

Values-driven but choice-rich

Eco-conscious buyers prioritize sustainability but face many retailers' green lines, raising switching options and price sensitivity; reviews and UGC magnify collective bargaining power, demanding transparency in ingredients, lifecycle and certifications. Grove Collaborative reported revenue near $169M in FY2023, so clear impact metrics can justify premiums and reduce churn.

- Buyers demand proof: certifications, full ingredients

- UGC/reviews amplify leverage

- Clear metrics justify premium pricing

Bulk and bundle negotiators

High-LTV customers at Grove Collaborative use bundles, subscriptions, and seasonal buys to improve unit economics, pressuring promo cadence and inventory allocation. They demand free shipping and flexible returns, forcing higher fulfillment costs and tighter margin management. Their purchase patterns increasingly dictate dynamic pricing and margin mix; tiered rewards can steer volume toward profitable SKUs.

- Customers: bundle/subscription driven

- Expectations: free shipping, flexible returns

- Impact: pricing strategy, margin mix

- Levers: tiered rewards to align volume with profitability

Moderate-high consumer power: low switching vs Amazon, rev $169M, churn ~30%

Customers hold moderate-to-high bargaining power: low switching costs vs Amazon (~40% US e‑commerce 2024) and Prime >200M, price sensitivity up as 2024 US CPI ~3%, subscription churn ~30% (2024). Grove revenue $169M FY2023; curation, bundles and subscription UX are key retention levers.

| Metric | Value |

|---|---|

| Amazon share | ~40% |

| Prime members | >200M |

| CPI 2024 | ~3% |

| Grove rev | $169M FY2023 |

| Sub churn 2024 | ~30% |

Preview the Actual Deliverable

Grove Collaborative Porter's Five Forces Analysis

This Grove Collaborative Porter’s Five Forces analysis evaluates competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry with concise, actionable insights. The preview you see is the exact, professionally formatted document you’ll receive upon purchase. No placeholders or samples — it’s ready for immediate download and use. The findings support strategic and investment decisions.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Grove Collaborative faces intense buyer power and growing substitute threats as consumers shift to sustainable, cost-conscious options; supplier influence and channel dynamics further pressure margins. Competitive rivalry is strong across DTC and retail, while entry barriers remain moderate amid brand and distribution investments. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Grove Collaborative’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated eco-suppliers

Concentrated eco-suppliers give Grove leverage challenges as many certified sustainable raw-material and packaging sources are limited, creating price and contractual power for suppliers. Niche inputs like plant-based surfactants, FSC paper and aluminum packaging can bottleneck supply, forcing Grove to balance ethics and availability; FSC-certified forests exceed 200 million hectares (2024). This concentration raises switching costs and stockout risk, pressuring margins and inventory management.

Private label leverage

Grove’s private-label assortment shifts volume to controlled formulations, diluting supplier power and improving margin capture; private-label penetration in U.S. household and personal care reached about 18% in 2024. Contract manufacturers can be multi-sourced to drive 5–10% procurement savings, but stringent quality and certification requirements limit vendor pools. Sustained bargaining strength hinges on scale efficiencies and SKU rationalization.

Logistics and fulfillment dependence

Grove Collaborative relies heavily on 3PLs, carriers and packaging vendors, exposing it to fuel surcharges and carrier capacity prioritization that the US 3PL market — about $239 billion in 2024 — helped dictate; peak-season constraints often compress margins. Sustainable packaging specs narrow qualified vendor pools and raise unit costs. Diversifying carriers and packaging SKUs reduces single-supplier leverage and improves negotiating flexibility.

Certification and compliance gatekeepers

Certifiers and testing labs like EPA Safer Choice and Leaping Bunny act as indirect suppliers whose standards and approval timelines directly affect Grove Collaborative’s cost structure and speed-to-market; delays can defer product launches and compress margins. Losing certification erodes brand equity and pricing power, while compliance costs—testing, reformulation, audits—are often passed through by upstream vendors, squeezing EBIT.

- 2024: certifications gate product entry

- Compliance raises COGS and time-to-revenue

- Certification loss damages pricing leverage

Branded partner dependence

Some third-party eco-brands carry strong customer loyalty that constrains Grove Collaborative’s negotiating leverage; exclusive SKUs and MAP policies from those partners limit Grove’s ability to offer deeper discounts and compress margin flexibility. Grove’s core value rests on assortment breadth, which reduces its walk-away power because removing a popular partner risks customer churn. Strategic co-marketing and shared promotions can help rebalance economics by improving joint sell-through and offsetting supplier constraints.

- Branded partner pull limits price negotiation

- Exclusive SKUs and MAP cap discounting

- Assortment breadth reduces Grove walk-away power

- Co-marketing can rebalance supplier economics

Concentrated eco-suppliers raise price risk; private-labels and CM cut margin pressure

Concentrated eco-suppliers and niche inputs (FSC >200M ha, 2024) give suppliers price and contractual leverage, raising switching costs and stockout risk. Grove’s private-label (18% US household/personal care, 2024) and multi-sourced CM strategies (5–10% savings) partially offset supplier power. 3PL/packaging market size ~$239B (US, 2024) and certification bottlenecks further constrain margins.

| Metric | 2024 |

|---|---|

| FSC area | 200M ha |

| Private-label share | 18% |

| US 3PL market | $239B |

What is included in the product

Tailored Porter's Five Forces analysis for Grove Collaborative that uncovers key drivers of competition, buyer and supplier power, and market entry risks specific to sustainable household products. Identifies disruptive substitutes, emerging threats, and strategic barriers that shape pricing, profitability, and long-term market position.

A concise one-sheet Porter's Five Forces for Grove Collaborative that highlights supplier power, buyer dynamics, competitive threats and substitution risk—perfect for quick strategic decisions, pitch decks, or aligning teams on priority pain points.

Customers Bargaining Power

Low switching costs

Low switching costs let consumers jump to Amazon (roughly 40% of US e‑commerce in 2024) or brand sites with a few clicks; cleaning and personal‑care SKUs are highly comparable. Free‑shipping incentives (typical $35 threshold) and promotions, plus Amazon Prime’s >200 million members, intensify churn. Grove must defend via tight curation, values alignment, and superior convenience.

Price sensitivity amid essentials

Household essentials are basket-driven so even 5% price gaps shift brand choice; 2024 US CPI ran near 3% year-over-year (BLS), increasing price elasticity for staples. Grove’s subscription model smooths perceived price volatility but industry subscription churn rose toward ~30% annual in 2024 if perceived value dropped. Transparent savings and bundled pricing have proven effective countermeasures.

Subscription stickiness vs churn risk

Auto-ship at Grove Collaborative increases predictability and reduces active comparison, lowering buyer power, and in 2024 the company emphasized subscription experiences to boost lifetime value. Yet pausing or canceling remains trivial online, keeping retention fragile. Personalization and accurate refill timing raise perceived utility and reduce friction. Loyalty perks and targeted discounts further cushion churn by raising switching costs.

Values-driven but choice-rich

Eco-conscious buyers prioritize sustainability but face many retailers' green lines, raising switching options and price sensitivity; reviews and UGC magnify collective bargaining power, demanding transparency in ingredients, lifecycle and certifications. Grove Collaborative reported revenue near $169M in FY2023, so clear impact metrics can justify premiums and reduce churn.

- Buyers demand proof: certifications, full ingredients

- UGC/reviews amplify leverage

- Clear metrics justify premium pricing

Bulk and bundle negotiators

High-LTV customers at Grove Collaborative use bundles, subscriptions, and seasonal buys to improve unit economics, pressuring promo cadence and inventory allocation. They demand free shipping and flexible returns, forcing higher fulfillment costs and tighter margin management. Their purchase patterns increasingly dictate dynamic pricing and margin mix; tiered rewards can steer volume toward profitable SKUs.

- Customers: bundle/subscription driven

- Expectations: free shipping, flexible returns

- Impact: pricing strategy, margin mix

- Levers: tiered rewards to align volume with profitability

Moderate-high consumer power: low switching vs Amazon, rev $169M, churn ~30%

Customers hold moderate-to-high bargaining power: low switching costs vs Amazon (~40% US e‑commerce 2024) and Prime >200M, price sensitivity up as 2024 US CPI ~3%, subscription churn ~30% (2024). Grove revenue $169M FY2023; curation, bundles and subscription UX are key retention levers.

| Metric | Value |

|---|---|

| Amazon share | ~40% |

| Prime members | >200M |

| CPI 2024 | ~3% |

| Grove rev | $169M FY2023 |

| Sub churn 2024 | ~30% |

Preview the Actual Deliverable

Grove Collaborative Porter's Five Forces Analysis

This Grove Collaborative Porter’s Five Forces analysis evaluates competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry with concise, actionable insights. The preview you see is the exact, professionally formatted document you’ll receive upon purchase. No placeholders or samples — it’s ready for immediate download and use. The findings support strategic and investment decisions.