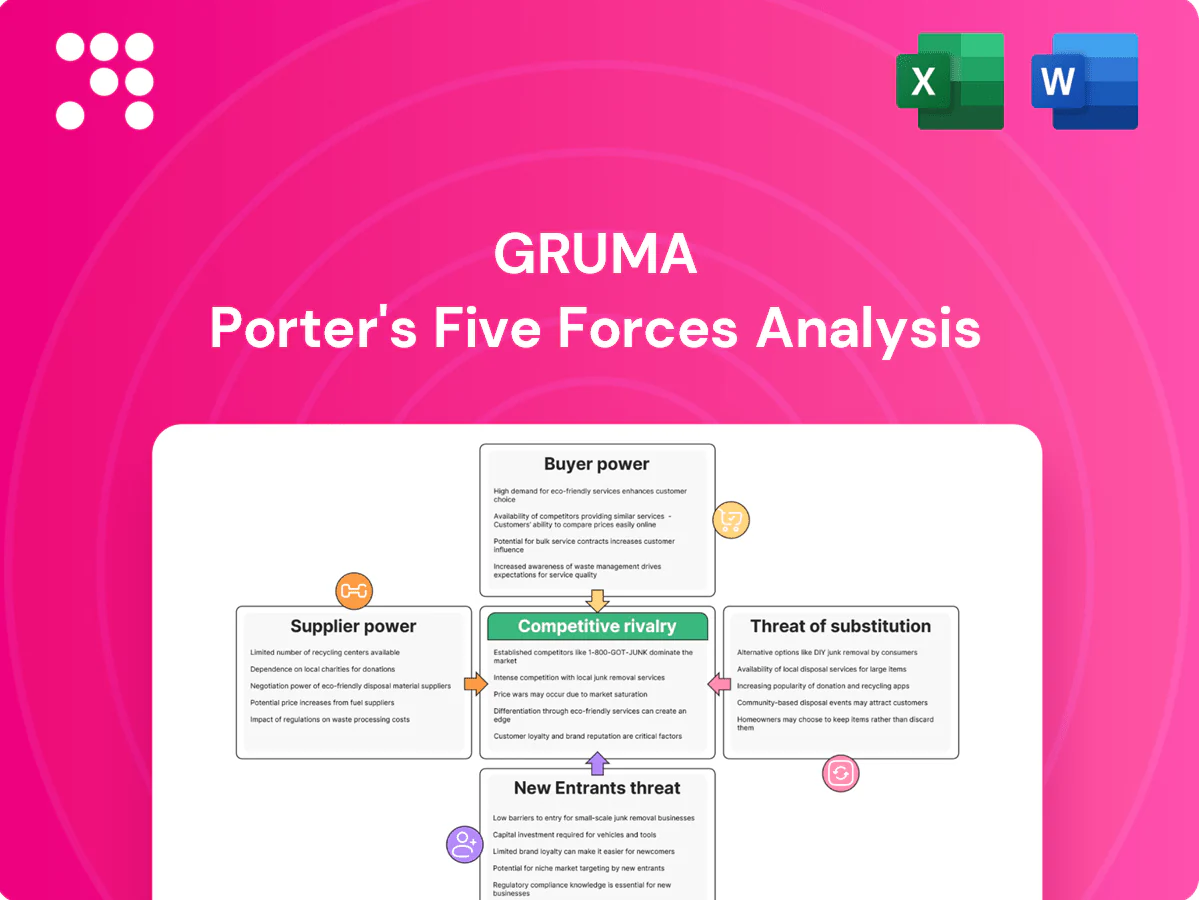

Gruma Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Gruma faces moderate supplier power, strong buyer bargaining in developed markets, intense rivalry from regional millers, and growing substitute threats from alternative grains and private labels. This snapshot highlights core tensions but omits force-level scores and scenarios. Unlock the full Porter's Five Forces Analysis to explore Gruma’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated corn suppliers

Maize is the core input and regional growers/traders can be locally concentrated, with the United States supplying roughly one-third of global corn exports in 2024, amplifying supplier leverage in tight markets. Weather, yields and input costs can spike local basis and freight, intermittently shifting pricing power to suppliers. Gruma mitigates risk through multi‑geography sourcing and long‑term contracts, though logistic dislocations can rapidly reassert supplier bargaining power.

Commodity price volatility

Corn and energy price swings — historically moving 20–30% in volatile years — feed through quickly to Gruma’s flour costs while customer pricing often lags, giving suppliers temporary bargaining power and squeezing margins; hedging and 60–90 day inventory buffers reduce but do not eliminate exposure, and Gruma’s ability to pass costs through varies by channel and contract terms (spot retail vs long‑term industrial agreements).

Quality/spec standards

Specific kernel quality, GMO/non‑GMO status and strict food safety standards narrow Gruma’s acceptable supplier pool, raising switching costs and increasing supplier leverage. Certifications and third‑party audits heighten compliance burdens for upstream partners and add cost and time to sourcing. As of 2024 Gruma’s global scale enables enforcement of tight specs, but in some regions limited alternative suppliers constrain flexibility.

Packaging and logistics dependencies

Packaging for Gruma relies on resin-based films, paper and specialized logistics, creating multiple supplier layers; tight freight capacity or resin shortages in 2024 shifted bargaining leverage toward vendors, though multi-sourcing and vertical coordination have mitigated exposure, yet sudden disruptions can still compress negotiating room.

- Resin, paper, logistics add supplier layers

- 2024 market tightness increased vendor leverage

- Multi-sourcing and vertical integration reduce risk

- Sudden disruptions still tighten negotiating space

Government and trade effects

Tariffs, quotas and sanitary rules in 2024 constrained cross‑border corn flows, with Mexico producing about 27.6 Mt and US exports around 44.5 Mt in 2023/24, letting export policy shift prices; export bans or subsidies have boosted supplier leverage. Gruma’s footprint in 100+ countries allows arbitrage but not always at needed volumes, so policy shocks can spike supplier power.

- Tariffs/quotas: restrict flows

- Export bans/subsidies: raise local prices

- Gruma: global reach, limited volume cover

- 2024: policy shocks = temporary supplier power

US exports (44.5 Mt) & Mexico (27.6 Mt) lift supplier bargaining power

US ~1/3 of global corn exports (44.5 Mt in 2023/24) and Mexico 27.6 Mt concentrate supplier power; weather, input costs and 2024 resin tightness intermittently boost vendor leverage. Gruma’s multi‑geography sourcing, long‑term contracts, hedging and 60–90 day inventories limit but do not eliminate exposure. Policy shocks and freight dislocations can rapidly reassert supplier bargaining power.

| Metric | 2023/24 |

|---|---|

| US corn exports | 44.5 Mt |

| Mexico production | 27.6 Mt |

| Inventory buffer | 60–90 days |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and market entry risks for Gruma, identifying disruptive forces, substitutes, and strategic safeguards that shape its pricing and profitability.

A concise one-sheet Porter's Five Forces for Gruma—perfect for quick strategic decisions and boardroom decks, with customizable pressure levels and an instant spider chart to visualize competitive intensity.

Customers Bargaining Power

Concentrated retail chains

Large concentrated retail chains like Walmart (≈25% of US grocery sales) and major club stores command shelf space and force trade spend, which in CPG averages roughly 10–15% of net sales, pressuring margins.

Their scale enables tough pricing and private label expansion; Gruma leverages Mission and category leadership to defend share, but retailer resets and vendor consolidation keep buyer power elevated.

Foodservice and industrial clients

Foodservice and industrial clients buy under long-term contracts with strict specifications and financial penalties for nonconformance, forcing suppliers like Gruma to meet tight quality and delivery metrics. Large QSRs and manufacturers concentrate purchasing power—top chains account for over 50% of US QSR channel sales—giving them leverage on price and service. Switching costs exist but are manageable due to qualified alternates and commodity-like products. Performance-based agreements and KPIs further strengthen buyer bargaining.

Price sensitivity in staples

Tortillas and corn flour are highly price‑visible staples; retail tortilla prices rose roughly 6% in 2024, prompting measurable trade‑downs to private label, whose grocery share climbed to about 18% in 2024 (PLMA). Consumers switch to promos or store brands when prices spike, though elasticity differs by region and brand loyalty, softening the impact for premium SKUs. Sustained inflation in 2024 increased buyer pushback and promo sensitivity.

Private label alternatives

Switching and service expectations

- Quality & delivery expectations

- Rapid switching behavior

- Gruma: 100+ countries (2024)

- Penalties increase buyer leverage

Retail and QSR consolidation squeeze margins for global tortilla producer despite scale

Large retail chains (Walmart ≈25% US grocery sales) and rising private label (18.3% US grocery 2023) extract trade spend (CPG ~10–15% of net sales) and price concessions, pressuring Gruma margins. Foodservice/QSR concentration (>50% US QSR sales top chains) enforces strict contracts, KPIs and penalties, increasing buyer leverage. Gruma scale (100+ countries, 2024) and brands (Mission, Maseca) mitigate but do not eliminate this power.

| Metric | Value |

|---|---|

| Walmart share | ≈25% US grocery |

| Private label | 18.3% (2023) |

| Trade spend | 10–15% net sales |

| Gruma footprint | 100+ countries (2024) |

| Retail tortilla price | +6% (2024) |

What You See Is What You Get

Gruma Porter's Five Forces Analysis

This Gruma Porter's Five Forces Analysis provides a concise, professionally formatted assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry specific to Gruma. This preview is the exact document you’ll receive immediately after purchase—no placeholders, ready to download and use. Use it as your full, final deliverable for strategic or investment decisions.

A Must-Have Tool for Decision-Makers

Gruma faces moderate supplier power, strong buyer bargaining in developed markets, intense rivalry from regional millers, and growing substitute threats from alternative grains and private labels. This snapshot highlights core tensions but omits force-level scores and scenarios. Unlock the full Porter's Five Forces Analysis to explore Gruma’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated corn suppliers

Maize is the core input and regional growers/traders can be locally concentrated, with the United States supplying roughly one-third of global corn exports in 2024, amplifying supplier leverage in tight markets. Weather, yields and input costs can spike local basis and freight, intermittently shifting pricing power to suppliers. Gruma mitigates risk through multi‑geography sourcing and long‑term contracts, though logistic dislocations can rapidly reassert supplier bargaining power.

Commodity price volatility

Corn and energy price swings — historically moving 20–30% in volatile years — feed through quickly to Gruma’s flour costs while customer pricing often lags, giving suppliers temporary bargaining power and squeezing margins; hedging and 60–90 day inventory buffers reduce but do not eliminate exposure, and Gruma’s ability to pass costs through varies by channel and contract terms (spot retail vs long‑term industrial agreements).

Quality/spec standards

Specific kernel quality, GMO/non‑GMO status and strict food safety standards narrow Gruma’s acceptable supplier pool, raising switching costs and increasing supplier leverage. Certifications and third‑party audits heighten compliance burdens for upstream partners and add cost and time to sourcing. As of 2024 Gruma’s global scale enables enforcement of tight specs, but in some regions limited alternative suppliers constrain flexibility.

Packaging and logistics dependencies

Packaging for Gruma relies on resin-based films, paper and specialized logistics, creating multiple supplier layers; tight freight capacity or resin shortages in 2024 shifted bargaining leverage toward vendors, though multi-sourcing and vertical coordination have mitigated exposure, yet sudden disruptions can still compress negotiating room.

- Resin, paper, logistics add supplier layers

- 2024 market tightness increased vendor leverage

- Multi-sourcing and vertical integration reduce risk

- Sudden disruptions still tighten negotiating space

Government and trade effects

Tariffs, quotas and sanitary rules in 2024 constrained cross‑border corn flows, with Mexico producing about 27.6 Mt and US exports around 44.5 Mt in 2023/24, letting export policy shift prices; export bans or subsidies have boosted supplier leverage. Gruma’s footprint in 100+ countries allows arbitrage but not always at needed volumes, so policy shocks can spike supplier power.

- Tariffs/quotas: restrict flows

- Export bans/subsidies: raise local prices

- Gruma: global reach, limited volume cover

- 2024: policy shocks = temporary supplier power

US exports (44.5 Mt) & Mexico (27.6 Mt) lift supplier bargaining power

US ~1/3 of global corn exports (44.5 Mt in 2023/24) and Mexico 27.6 Mt concentrate supplier power; weather, input costs and 2024 resin tightness intermittently boost vendor leverage. Gruma’s multi‑geography sourcing, long‑term contracts, hedging and 60–90 day inventories limit but do not eliminate exposure. Policy shocks and freight dislocations can rapidly reassert supplier bargaining power.

| Metric | 2023/24 |

|---|---|

| US corn exports | 44.5 Mt |

| Mexico production | 27.6 Mt |

| Inventory buffer | 60–90 days |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and market entry risks for Gruma, identifying disruptive forces, substitutes, and strategic safeguards that shape its pricing and profitability.

A concise one-sheet Porter's Five Forces for Gruma—perfect for quick strategic decisions and boardroom decks, with customizable pressure levels and an instant spider chart to visualize competitive intensity.

Customers Bargaining Power

Concentrated retail chains

Large concentrated retail chains like Walmart (≈25% of US grocery sales) and major club stores command shelf space and force trade spend, which in CPG averages roughly 10–15% of net sales, pressuring margins.

Their scale enables tough pricing and private label expansion; Gruma leverages Mission and category leadership to defend share, but retailer resets and vendor consolidation keep buyer power elevated.

Foodservice and industrial clients

Foodservice and industrial clients buy under long-term contracts with strict specifications and financial penalties for nonconformance, forcing suppliers like Gruma to meet tight quality and delivery metrics. Large QSRs and manufacturers concentrate purchasing power—top chains account for over 50% of US QSR channel sales—giving them leverage on price and service. Switching costs exist but are manageable due to qualified alternates and commodity-like products. Performance-based agreements and KPIs further strengthen buyer bargaining.

Price sensitivity in staples

Tortillas and corn flour are highly price‑visible staples; retail tortilla prices rose roughly 6% in 2024, prompting measurable trade‑downs to private label, whose grocery share climbed to about 18% in 2024 (PLMA). Consumers switch to promos or store brands when prices spike, though elasticity differs by region and brand loyalty, softening the impact for premium SKUs. Sustained inflation in 2024 increased buyer pushback and promo sensitivity.

Private label alternatives

Switching and service expectations

- Quality & delivery expectations

- Rapid switching behavior

- Gruma: 100+ countries (2024)

- Penalties increase buyer leverage

Retail and QSR consolidation squeeze margins for global tortilla producer despite scale

Large retail chains (Walmart ≈25% US grocery sales) and rising private label (18.3% US grocery 2023) extract trade spend (CPG ~10–15% of net sales) and price concessions, pressuring Gruma margins. Foodservice/QSR concentration (>50% US QSR sales top chains) enforces strict contracts, KPIs and penalties, increasing buyer leverage. Gruma scale (100+ countries, 2024) and brands (Mission, Maseca) mitigate but do not eliminate this power.

| Metric | Value |

|---|---|

| Walmart share | ≈25% US grocery |

| Private label | 18.3% (2023) |

| Trade spend | 10–15% net sales |

| Gruma footprint | 100+ countries (2024) |

| Retail tortilla price | +6% (2024) |

What You See Is What You Get

Gruma Porter's Five Forces Analysis

This Gruma Porter's Five Forces Analysis provides a concise, professionally formatted assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry specific to Gruma. This preview is the exact document you’ll receive immediately after purchase—no placeholders, ready to download and use. Use it as your full, final deliverable for strategic or investment decisions.

Description

A Must-Have Tool for Decision-Makers

Gruma faces moderate supplier power, strong buyer bargaining in developed markets, intense rivalry from regional millers, and growing substitute threats from alternative grains and private labels. This snapshot highlights core tensions but omits force-level scores and scenarios. Unlock the full Porter's Five Forces Analysis to explore Gruma’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated corn suppliers

Maize is the core input and regional growers/traders can be locally concentrated, with the United States supplying roughly one-third of global corn exports in 2024, amplifying supplier leverage in tight markets. Weather, yields and input costs can spike local basis and freight, intermittently shifting pricing power to suppliers. Gruma mitigates risk through multi‑geography sourcing and long‑term contracts, though logistic dislocations can rapidly reassert supplier bargaining power.

Commodity price volatility

Corn and energy price swings — historically moving 20–30% in volatile years — feed through quickly to Gruma’s flour costs while customer pricing often lags, giving suppliers temporary bargaining power and squeezing margins; hedging and 60–90 day inventory buffers reduce but do not eliminate exposure, and Gruma’s ability to pass costs through varies by channel and contract terms (spot retail vs long‑term industrial agreements).

Quality/spec standards

Specific kernel quality, GMO/non‑GMO status and strict food safety standards narrow Gruma’s acceptable supplier pool, raising switching costs and increasing supplier leverage. Certifications and third‑party audits heighten compliance burdens for upstream partners and add cost and time to sourcing. As of 2024 Gruma’s global scale enables enforcement of tight specs, but in some regions limited alternative suppliers constrain flexibility.

Packaging and logistics dependencies

Packaging for Gruma relies on resin-based films, paper and specialized logistics, creating multiple supplier layers; tight freight capacity or resin shortages in 2024 shifted bargaining leverage toward vendors, though multi-sourcing and vertical coordination have mitigated exposure, yet sudden disruptions can still compress negotiating room.

- Resin, paper, logistics add supplier layers

- 2024 market tightness increased vendor leverage

- Multi-sourcing and vertical integration reduce risk

- Sudden disruptions still tighten negotiating space

Government and trade effects

Tariffs, quotas and sanitary rules in 2024 constrained cross‑border corn flows, with Mexico producing about 27.6 Mt and US exports around 44.5 Mt in 2023/24, letting export policy shift prices; export bans or subsidies have boosted supplier leverage. Gruma’s footprint in 100+ countries allows arbitrage but not always at needed volumes, so policy shocks can spike supplier power.

- Tariffs/quotas: restrict flows

- Export bans/subsidies: raise local prices

- Gruma: global reach, limited volume cover

- 2024: policy shocks = temporary supplier power

US exports (44.5 Mt) & Mexico (27.6 Mt) lift supplier bargaining power

US ~1/3 of global corn exports (44.5 Mt in 2023/24) and Mexico 27.6 Mt concentrate supplier power; weather, input costs and 2024 resin tightness intermittently boost vendor leverage. Gruma’s multi‑geography sourcing, long‑term contracts, hedging and 60–90 day inventories limit but do not eliminate exposure. Policy shocks and freight dislocations can rapidly reassert supplier bargaining power.

| Metric | 2023/24 |

|---|---|

| US corn exports | 44.5 Mt |

| Mexico production | 27.6 Mt |

| Inventory buffer | 60–90 days |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and market entry risks for Gruma, identifying disruptive forces, substitutes, and strategic safeguards that shape its pricing and profitability.

A concise one-sheet Porter's Five Forces for Gruma—perfect for quick strategic decisions and boardroom decks, with customizable pressure levels and an instant spider chart to visualize competitive intensity.

Customers Bargaining Power

Concentrated retail chains

Large concentrated retail chains like Walmart (≈25% of US grocery sales) and major club stores command shelf space and force trade spend, which in CPG averages roughly 10–15% of net sales, pressuring margins.

Their scale enables tough pricing and private label expansion; Gruma leverages Mission and category leadership to defend share, but retailer resets and vendor consolidation keep buyer power elevated.

Foodservice and industrial clients

Foodservice and industrial clients buy under long-term contracts with strict specifications and financial penalties for nonconformance, forcing suppliers like Gruma to meet tight quality and delivery metrics. Large QSRs and manufacturers concentrate purchasing power—top chains account for over 50% of US QSR channel sales—giving them leverage on price and service. Switching costs exist but are manageable due to qualified alternates and commodity-like products. Performance-based agreements and KPIs further strengthen buyer bargaining.

Price sensitivity in staples

Tortillas and corn flour are highly price‑visible staples; retail tortilla prices rose roughly 6% in 2024, prompting measurable trade‑downs to private label, whose grocery share climbed to about 18% in 2024 (PLMA). Consumers switch to promos or store brands when prices spike, though elasticity differs by region and brand loyalty, softening the impact for premium SKUs. Sustained inflation in 2024 increased buyer pushback and promo sensitivity.

Private label alternatives

Switching and service expectations

- Quality & delivery expectations

- Rapid switching behavior

- Gruma: 100+ countries (2024)

- Penalties increase buyer leverage

Retail and QSR consolidation squeeze margins for global tortilla producer despite scale

Large retail chains (Walmart ≈25% US grocery sales) and rising private label (18.3% US grocery 2023) extract trade spend (CPG ~10–15% of net sales) and price concessions, pressuring Gruma margins. Foodservice/QSR concentration (>50% US QSR sales top chains) enforces strict contracts, KPIs and penalties, increasing buyer leverage. Gruma scale (100+ countries, 2024) and brands (Mission, Maseca) mitigate but do not eliminate this power.

| Metric | Value |

|---|---|

| Walmart share | ≈25% US grocery |

| Private label | 18.3% (2023) |

| Trade spend | 10–15% net sales |

| Gruma footprint | 100+ countries (2024) |

| Retail tortilla price | +6% (2024) |

What You See Is What You Get

Gruma Porter's Five Forces Analysis

This Gruma Porter's Five Forces Analysis provides a concise, professionally formatted assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry specific to Gruma. This preview is the exact document you’ll receive immediately after purchase—no placeholders, ready to download and use. Use it as your full, final deliverable for strategic or investment decisions.