Grupo Herdez Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

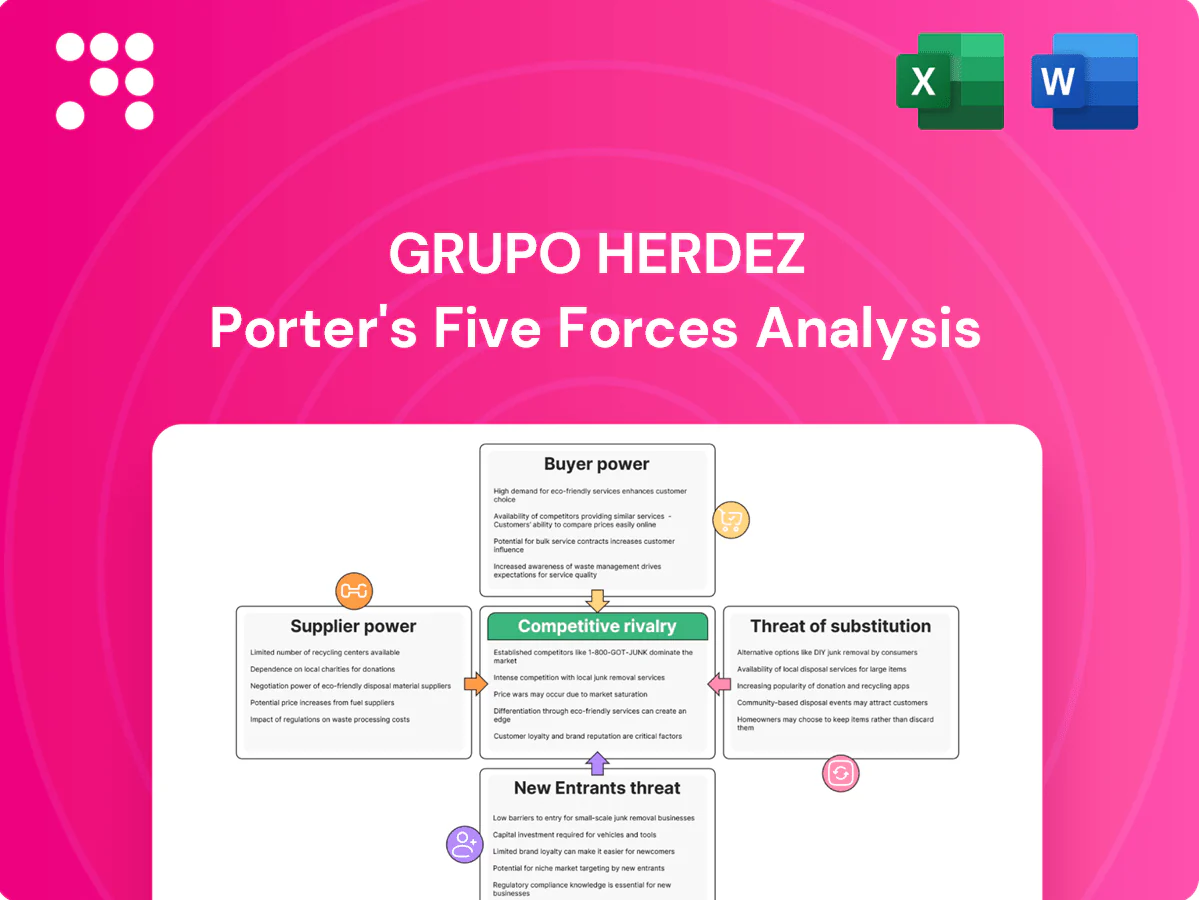

Grupo Herdez faces moderate supplier power due to branded inputs and scale, high buyer pressure from concentrated retailers, and limited new-entrant threats thanks to strong brand loyalty and distribution networks. Rivalry and substitute risk vary by category, influencing margin resilience and pricing flexibility. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Grupo Herdez’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diversified agri-sourcing

Grupo Herdez sources tomatoes, peppers, fruits, sugar, dairy and grains from multiple regions, diluting individual supplier leverage and lowering single-source risk. Seasonal and climate shocks, notably the 2023–24 El Niño pattern, tightened supply windows and pushed raw-material prices higher. Diversification and dual-sourcing mitigate but do not fully insulate the company, since crop shocks still transmit through markets. Long-term contracts smooth volatility but rarely eliminate price spikes.

Packaging and input concentration

Cans, glass, labels and resin-based plastics are supplied by a concentrated global set of vendors — Ball and Crown alone account for over 60% of global can capacity in 2024 — giving suppliers leverage. Global metal and resin price cycles in 2024 transmitted to finished-pack prices within 2–3 months, compressing margin flexibility. Switching suppliers is feasible but requires qualification and tooling changes, while Grupo Herdez’s scale purchasing and long-term contracts partially offset supplier concentration.

Dairy dependence for ice cream

Dairy inputs for Grupo Herdez ice-cream are sourced from localized, volatile milk and cream markets, with Mexico producing roughly 12.5 million tonnes of milk in 2024, reinforcing supplier leverage. Cold-chain constraints make rapid supplier switching costly and slow. Hedging and formula pricing are used to blunt spot spikes. Co-manufacturing is feasible but raises logistics and margin pressure.

FX and import exposure

Imported inputs expose Grupo Herdez costs to USD/MXN volatility; in 2024 the peso traded roughly 17–19 per USD, amplifying cost pass-through and indirectly strengthening foreign suppliers. Currency hedges reduce but do not eliminate exposure. Many suppliers invoice in USD, limiting negotiation room; ongoing localization of sourcing and packaging can rebalance supplier power over time.

- USD/MXN 2024 range: ~17–19

- Hedges mitigate but leave basis risk

- USD-invoiced inputs reduce bargaining leverage

- Localization lowers import dependence

Brand pull offsets

Well-known Herdez brands give the company volume stability that suppliers value, tempering supplier bargaining power; as of 2024 Herdez remains listed on BMV (HERDEZ B) and its strong portfolio supports predictable demand and better allocation in tight markets. Joint planning with key suppliers improves service levels, though scarce commodities (oils, tomatoes) still retain pricing power.

- Brand pull: stabilizes volumes

- Predictable demand: better terms/allocations

- Joint planning: improved service

- Commodity shortages: sustain supplier pricing power

Can supply >60%, milk ~12.5m t, USD/MXN ~17–19 squeeze margins

Supplier power is moderate-high: concentrated can/plastics suppliers (Ball and Crown >60% of global can capacity in 2024) and volatile dairy/produce markets (Mexico milk ~12.5m tonnes in 2024) give pricing leverage. USD/MXN ~17–19 in 2024 amplifies imported-input cost pass-through. Long-term contracts, dual-sourcing and brand volume mitigate but do not remove spot-driven margin pressure.

| Metric | 2024 | Implication |

|---|---|---|

| Can capacity | >60% Ball/Crown | High supplier leverage |

| Milk supply (Mexico) | ~12.5m t | Volatile dairy costs |

| USD/MXN | ~17–19 | Import cost pass-through |

What is included in the product

Tailored Porter's Five Forces analysis of Grupo Herdez revealing competitive rivalry, buyer and supplier bargaining power, threats from substitutes and new entrants, and strategic levers to protect market share and margins.

A concise, one-sheet Porter’s Five Forces for Grupo Herdez—clearly maps supplier, buyer, rivalry, substitute, and entrant pressures to relieve strategic uncertainty and speed decision-making.

Customers Bargaining Power

Dominant modern retail

Large modern retailers control shelf access and extract slotting fees, promotional funding and extended payment terms, amplifying price pressure across categories; modern trade accounted for about 66% of Mexico's food retail in 2024 (Euromonitor). These chains’ scale forces Herdez to absorb or fund promotions and longer receivables, though Herdez’s must-have SKUs and leading brand positions help preserve negotiating leverage and shelf presence.

Traditional trade fragmentation

Traditional trade fragmentation limits customer bargaining: with over 4 million small stores and wholesalers in Mexico, individual buyers lack leverage, while distributors gain importance for reach but intensely compete among themselves. Grupo Herdez’s strong route-to-market and direct distribution enhance pricing discipline and margin protection. Credit terms and differential service levels remain primary levers to secure shelf space and loyalty.

Private label leverage

Retailers leverage private labels—which reached roughly 12% penetration in Mexican grocery in 2024—to push for lower supplier prices, especially in low-margin staples where switching costs for consumers are minimal. Herdez defends shelf space through product differentiation, strict quality controls and ongoing innovation. The company must keep price gaps narrow versus private labels to protect volume and margins.

US channel dynamics

In the US, big-box and Hispanic-focused retailers centralize buying and demand promotions, driving higher trade spend via slotting fees and scan-downs. Strong salsa and guacamole brands help Grupo Herdez retain presence, but retailers can reallocate facings quickly, compressing margins and increasing promo dependence. 2024 US Hispanic population ≈63 million supports steady category demand.

- Centralized buying — top retailers set terms

- Higher trade spend — slotting/scan-downs pressure suppliers

- Brand strength — salsa/guac sustain shelf presence

- Facings fluid — rapid reallocation risks volume

Consumer price sensitivity

Staple foods sold by Grupo Herdez show higher price sensitivity, with volumes rising on promotions during downturns and retailers increasingly pressuring for trade funding; sauces and salsas retain lower elasticity due to brand equity and convenience, while premium ice cream faces significant trade-down risk as consumers shift to mainstream options.

- Staples: elastic, promotion-driven

- Sauces/salsas: brand lowers elasticity

- Retailers: demand promotional funding

- Premium ice cream: high trade-down risk

Modern trade 66% / 4M / 12% market snapshot

Retail chains (66% modern trade Mexico 2024) and US big-box centralize buying, extracting slotting fees and promotions, pressuring margins. Fragmented traditional trade (≈4M small stores) limits buyer power; Herdez’s brands and direct distribution protect shelf space. Private labels ~12% penetration push price cuts; staples are promotion-sensitive while sauces/salsas retain brand resilience.

| Metric | 2024 Value |

|---|---|

| Mexico modern trade share | 66% |

| Small stores/wholesalers | ≈4,000,000 |

| Private label penetration | 12% |

| US Hispanic population | ≈63,000,000 |

What You See Is What You Get

Grupo Herdez Porter's Five Forces Analysis

This preview is the Grupo Herdez Porter's Five Forces analysis and exactly matches the full document you'll receive after purchase. It is fully formatted, professionally written, and ready for immediate download and use. No placeholders or samples—what you see is the deliverable.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Grupo Herdez faces moderate supplier power due to branded inputs and scale, high buyer pressure from concentrated retailers, and limited new-entrant threats thanks to strong brand loyalty and distribution networks. Rivalry and substitute risk vary by category, influencing margin resilience and pricing flexibility. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Grupo Herdez’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diversified agri-sourcing

Grupo Herdez sources tomatoes, peppers, fruits, sugar, dairy and grains from multiple regions, diluting individual supplier leverage and lowering single-source risk. Seasonal and climate shocks, notably the 2023–24 El Niño pattern, tightened supply windows and pushed raw-material prices higher. Diversification and dual-sourcing mitigate but do not fully insulate the company, since crop shocks still transmit through markets. Long-term contracts smooth volatility but rarely eliminate price spikes.

Packaging and input concentration

Cans, glass, labels and resin-based plastics are supplied by a concentrated global set of vendors — Ball and Crown alone account for over 60% of global can capacity in 2024 — giving suppliers leverage. Global metal and resin price cycles in 2024 transmitted to finished-pack prices within 2–3 months, compressing margin flexibility. Switching suppliers is feasible but requires qualification and tooling changes, while Grupo Herdez’s scale purchasing and long-term contracts partially offset supplier concentration.

Dairy dependence for ice cream

Dairy inputs for Grupo Herdez ice-cream are sourced from localized, volatile milk and cream markets, with Mexico producing roughly 12.5 million tonnes of milk in 2024, reinforcing supplier leverage. Cold-chain constraints make rapid supplier switching costly and slow. Hedging and formula pricing are used to blunt spot spikes. Co-manufacturing is feasible but raises logistics and margin pressure.

FX and import exposure

Imported inputs expose Grupo Herdez costs to USD/MXN volatility; in 2024 the peso traded roughly 17–19 per USD, amplifying cost pass-through and indirectly strengthening foreign suppliers. Currency hedges reduce but do not eliminate exposure. Many suppliers invoice in USD, limiting negotiation room; ongoing localization of sourcing and packaging can rebalance supplier power over time.

- USD/MXN 2024 range: ~17–19

- Hedges mitigate but leave basis risk

- USD-invoiced inputs reduce bargaining leverage

- Localization lowers import dependence

Brand pull offsets

Well-known Herdez brands give the company volume stability that suppliers value, tempering supplier bargaining power; as of 2024 Herdez remains listed on BMV (HERDEZ B) and its strong portfolio supports predictable demand and better allocation in tight markets. Joint planning with key suppliers improves service levels, though scarce commodities (oils, tomatoes) still retain pricing power.

- Brand pull: stabilizes volumes

- Predictable demand: better terms/allocations

- Joint planning: improved service

- Commodity shortages: sustain supplier pricing power

Can supply >60%, milk ~12.5m t, USD/MXN ~17–19 squeeze margins

Supplier power is moderate-high: concentrated can/plastics suppliers (Ball and Crown >60% of global can capacity in 2024) and volatile dairy/produce markets (Mexico milk ~12.5m tonnes in 2024) give pricing leverage. USD/MXN ~17–19 in 2024 amplifies imported-input cost pass-through. Long-term contracts, dual-sourcing and brand volume mitigate but do not remove spot-driven margin pressure.

| Metric | 2024 | Implication |

|---|---|---|

| Can capacity | >60% Ball/Crown | High supplier leverage |

| Milk supply (Mexico) | ~12.5m t | Volatile dairy costs |

| USD/MXN | ~17–19 | Import cost pass-through |

What is included in the product

Tailored Porter's Five Forces analysis of Grupo Herdez revealing competitive rivalry, buyer and supplier bargaining power, threats from substitutes and new entrants, and strategic levers to protect market share and margins.

A concise, one-sheet Porter’s Five Forces for Grupo Herdez—clearly maps supplier, buyer, rivalry, substitute, and entrant pressures to relieve strategic uncertainty and speed decision-making.

Customers Bargaining Power

Dominant modern retail

Large modern retailers control shelf access and extract slotting fees, promotional funding and extended payment terms, amplifying price pressure across categories; modern trade accounted for about 66% of Mexico's food retail in 2024 (Euromonitor). These chains’ scale forces Herdez to absorb or fund promotions and longer receivables, though Herdez’s must-have SKUs and leading brand positions help preserve negotiating leverage and shelf presence.

Traditional trade fragmentation

Traditional trade fragmentation limits customer bargaining: with over 4 million small stores and wholesalers in Mexico, individual buyers lack leverage, while distributors gain importance for reach but intensely compete among themselves. Grupo Herdez’s strong route-to-market and direct distribution enhance pricing discipline and margin protection. Credit terms and differential service levels remain primary levers to secure shelf space and loyalty.

Private label leverage

Retailers leverage private labels—which reached roughly 12% penetration in Mexican grocery in 2024—to push for lower supplier prices, especially in low-margin staples where switching costs for consumers are minimal. Herdez defends shelf space through product differentiation, strict quality controls and ongoing innovation. The company must keep price gaps narrow versus private labels to protect volume and margins.

US channel dynamics

In the US, big-box and Hispanic-focused retailers centralize buying and demand promotions, driving higher trade spend via slotting fees and scan-downs. Strong salsa and guacamole brands help Grupo Herdez retain presence, but retailers can reallocate facings quickly, compressing margins and increasing promo dependence. 2024 US Hispanic population ≈63 million supports steady category demand.

- Centralized buying — top retailers set terms

- Higher trade spend — slotting/scan-downs pressure suppliers

- Brand strength — salsa/guac sustain shelf presence

- Facings fluid — rapid reallocation risks volume

Consumer price sensitivity

Staple foods sold by Grupo Herdez show higher price sensitivity, with volumes rising on promotions during downturns and retailers increasingly pressuring for trade funding; sauces and salsas retain lower elasticity due to brand equity and convenience, while premium ice cream faces significant trade-down risk as consumers shift to mainstream options.

- Staples: elastic, promotion-driven

- Sauces/salsas: brand lowers elasticity

- Retailers: demand promotional funding

- Premium ice cream: high trade-down risk

Modern trade 66% / 4M / 12% market snapshot

Retail chains (66% modern trade Mexico 2024) and US big-box centralize buying, extracting slotting fees and promotions, pressuring margins. Fragmented traditional trade (≈4M small stores) limits buyer power; Herdez’s brands and direct distribution protect shelf space. Private labels ~12% penetration push price cuts; staples are promotion-sensitive while sauces/salsas retain brand resilience.

| Metric | 2024 Value |

|---|---|

| Mexico modern trade share | 66% |

| Small stores/wholesalers | ≈4,000,000 |

| Private label penetration | 12% |

| US Hispanic population | ≈63,000,000 |

What You See Is What You Get

Grupo Herdez Porter's Five Forces Analysis

This preview is the Grupo Herdez Porter's Five Forces analysis and exactly matches the full document you'll receive after purchase. It is fully formatted, professionally written, and ready for immediate download and use. No placeholders or samples—what you see is the deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Grupo Herdez faces moderate supplier power due to branded inputs and scale, high buyer pressure from concentrated retailers, and limited new-entrant threats thanks to strong brand loyalty and distribution networks. Rivalry and substitute risk vary by category, influencing margin resilience and pricing flexibility. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Grupo Herdez’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diversified agri-sourcing

Grupo Herdez sources tomatoes, peppers, fruits, sugar, dairy and grains from multiple regions, diluting individual supplier leverage and lowering single-source risk. Seasonal and climate shocks, notably the 2023–24 El Niño pattern, tightened supply windows and pushed raw-material prices higher. Diversification and dual-sourcing mitigate but do not fully insulate the company, since crop shocks still transmit through markets. Long-term contracts smooth volatility but rarely eliminate price spikes.

Packaging and input concentration

Cans, glass, labels and resin-based plastics are supplied by a concentrated global set of vendors — Ball and Crown alone account for over 60% of global can capacity in 2024 — giving suppliers leverage. Global metal and resin price cycles in 2024 transmitted to finished-pack prices within 2–3 months, compressing margin flexibility. Switching suppliers is feasible but requires qualification and tooling changes, while Grupo Herdez’s scale purchasing and long-term contracts partially offset supplier concentration.

Dairy dependence for ice cream

Dairy inputs for Grupo Herdez ice-cream are sourced from localized, volatile milk and cream markets, with Mexico producing roughly 12.5 million tonnes of milk in 2024, reinforcing supplier leverage. Cold-chain constraints make rapid supplier switching costly and slow. Hedging and formula pricing are used to blunt spot spikes. Co-manufacturing is feasible but raises logistics and margin pressure.

FX and import exposure

Imported inputs expose Grupo Herdez costs to USD/MXN volatility; in 2024 the peso traded roughly 17–19 per USD, amplifying cost pass-through and indirectly strengthening foreign suppliers. Currency hedges reduce but do not eliminate exposure. Many suppliers invoice in USD, limiting negotiation room; ongoing localization of sourcing and packaging can rebalance supplier power over time.

- USD/MXN 2024 range: ~17–19

- Hedges mitigate but leave basis risk

- USD-invoiced inputs reduce bargaining leverage

- Localization lowers import dependence

Brand pull offsets

Well-known Herdez brands give the company volume stability that suppliers value, tempering supplier bargaining power; as of 2024 Herdez remains listed on BMV (HERDEZ B) and its strong portfolio supports predictable demand and better allocation in tight markets. Joint planning with key suppliers improves service levels, though scarce commodities (oils, tomatoes) still retain pricing power.

- Brand pull: stabilizes volumes

- Predictable demand: better terms/allocations

- Joint planning: improved service

- Commodity shortages: sustain supplier pricing power

Can supply >60%, milk ~12.5m t, USD/MXN ~17–19 squeeze margins

Supplier power is moderate-high: concentrated can/plastics suppliers (Ball and Crown >60% of global can capacity in 2024) and volatile dairy/produce markets (Mexico milk ~12.5m tonnes in 2024) give pricing leverage. USD/MXN ~17–19 in 2024 amplifies imported-input cost pass-through. Long-term contracts, dual-sourcing and brand volume mitigate but do not remove spot-driven margin pressure.

| Metric | 2024 | Implication |

|---|---|---|

| Can capacity | >60% Ball/Crown | High supplier leverage |

| Milk supply (Mexico) | ~12.5m t | Volatile dairy costs |

| USD/MXN | ~17–19 | Import cost pass-through |

What is included in the product

Tailored Porter's Five Forces analysis of Grupo Herdez revealing competitive rivalry, buyer and supplier bargaining power, threats from substitutes and new entrants, and strategic levers to protect market share and margins.

A concise, one-sheet Porter’s Five Forces for Grupo Herdez—clearly maps supplier, buyer, rivalry, substitute, and entrant pressures to relieve strategic uncertainty and speed decision-making.

Customers Bargaining Power

Dominant modern retail

Large modern retailers control shelf access and extract slotting fees, promotional funding and extended payment terms, amplifying price pressure across categories; modern trade accounted for about 66% of Mexico's food retail in 2024 (Euromonitor). These chains’ scale forces Herdez to absorb or fund promotions and longer receivables, though Herdez’s must-have SKUs and leading brand positions help preserve negotiating leverage and shelf presence.

Traditional trade fragmentation

Traditional trade fragmentation limits customer bargaining: with over 4 million small stores and wholesalers in Mexico, individual buyers lack leverage, while distributors gain importance for reach but intensely compete among themselves. Grupo Herdez’s strong route-to-market and direct distribution enhance pricing discipline and margin protection. Credit terms and differential service levels remain primary levers to secure shelf space and loyalty.

Private label leverage

Retailers leverage private labels—which reached roughly 12% penetration in Mexican grocery in 2024—to push for lower supplier prices, especially in low-margin staples where switching costs for consumers are minimal. Herdez defends shelf space through product differentiation, strict quality controls and ongoing innovation. The company must keep price gaps narrow versus private labels to protect volume and margins.

US channel dynamics

In the US, big-box and Hispanic-focused retailers centralize buying and demand promotions, driving higher trade spend via slotting fees and scan-downs. Strong salsa and guacamole brands help Grupo Herdez retain presence, but retailers can reallocate facings quickly, compressing margins and increasing promo dependence. 2024 US Hispanic population ≈63 million supports steady category demand.

- Centralized buying — top retailers set terms

- Higher trade spend — slotting/scan-downs pressure suppliers

- Brand strength — salsa/guac sustain shelf presence

- Facings fluid — rapid reallocation risks volume

Consumer price sensitivity

Staple foods sold by Grupo Herdez show higher price sensitivity, with volumes rising on promotions during downturns and retailers increasingly pressuring for trade funding; sauces and salsas retain lower elasticity due to brand equity and convenience, while premium ice cream faces significant trade-down risk as consumers shift to mainstream options.

- Staples: elastic, promotion-driven

- Sauces/salsas: brand lowers elasticity

- Retailers: demand promotional funding

- Premium ice cream: high trade-down risk

Modern trade 66% / 4M / 12% market snapshot

Retail chains (66% modern trade Mexico 2024) and US big-box centralize buying, extracting slotting fees and promotions, pressuring margins. Fragmented traditional trade (≈4M small stores) limits buyer power; Herdez’s brands and direct distribution protect shelf space. Private labels ~12% penetration push price cuts; staples are promotion-sensitive while sauces/salsas retain brand resilience.

| Metric | 2024 Value |

|---|---|

| Mexico modern trade share | 66% |

| Small stores/wholesalers | ≈4,000,000 |

| Private label penetration | 12% |

| US Hispanic population | ≈63,000,000 |

What You See Is What You Get

Grupo Herdez Porter's Five Forces Analysis

This preview is the Grupo Herdez Porter's Five Forces analysis and exactly matches the full document you'll receive after purchase. It is fully formatted, professionally written, and ready for immediate download and use. No placeholders or samples—what you see is the deliverable.