Segur Ibérica, S.A. Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

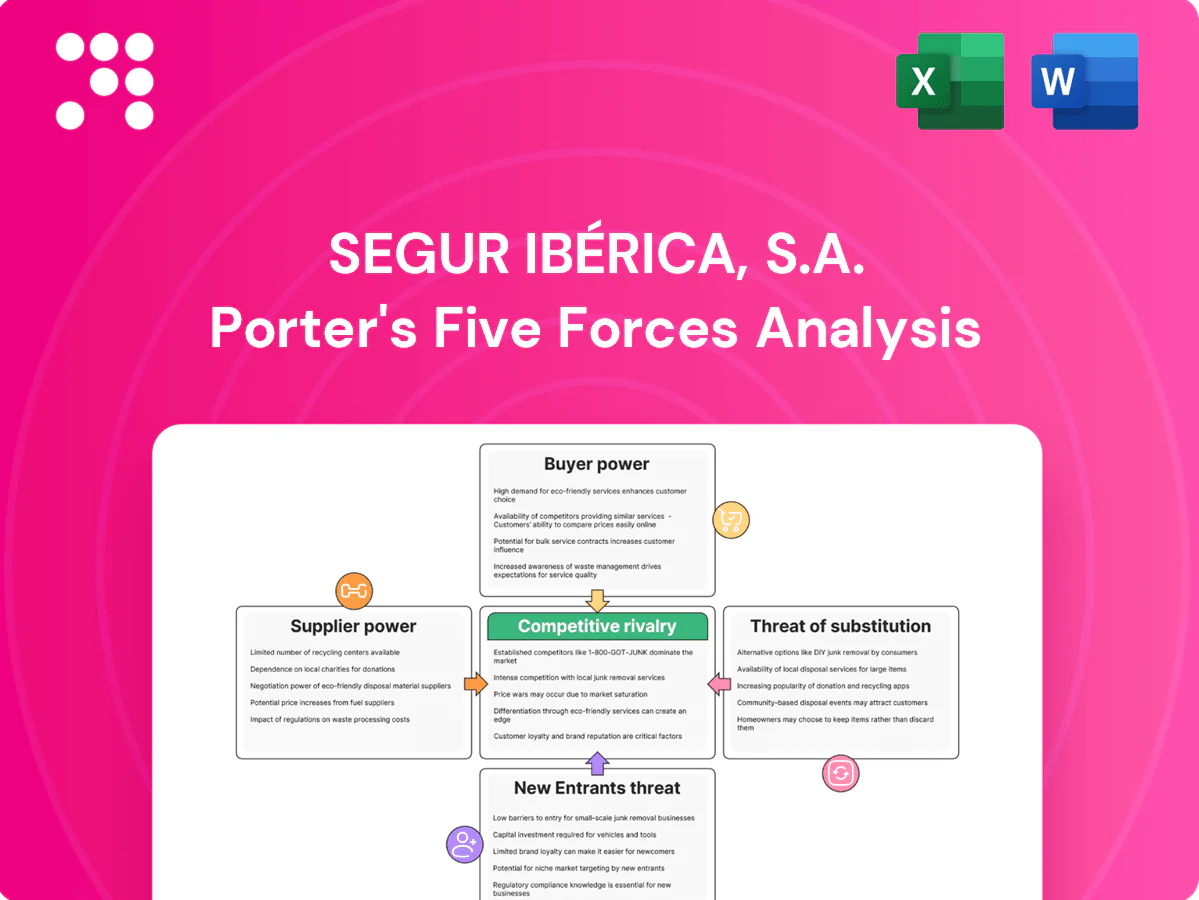

Segur Ibérica, S.A. faces moderate buyer power, concentrated supplier relationships, and rising substitute and entrant threats driven by tech-enabled security services; rivalry is intense among national and regional players. This snapshot highlights key pressure points and strategic levers. This preview is just the beginning—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Reliance on licensed guard labor

Guard supply for Segur Ibérica is critical and highly regulated (Real Decreto 2364/1994) with unionized labor, giving workers measurable bargaining power; wage floors and collective agreements anchored to the 2024 SMI of €1,080/mo plus overtime premiums and mandatory certifications limit cost flexibility. Regional shortages can compress margins, and retention/training reduce disruption but raise fixed costs.

Dependence on security tech vendors

Hardware for CCTV, access control, alarms and sensors is concentrated among a handful of global OEMs, giving those suppliers de facto leverage while interoperability standards limit absolute lock-in. Proprietary ecosystems still create switching frictions and volume discounts advantage large buyers, though the 2021–22 component shortage briefly shifted bargaining power toward suppliers. Long-term framework agreements are used to stabilize pricing and secure supply.

Software platforms and monitoring infrastructure

Alarm receiving centers and analytics depend on specialized software and telecom services with strict 99.9% uptime SLAs and continuous cybersecurity monitoring, embedding recurring supplier leverage through subscription licensing and data‑hosting terms. These contracts drive predictable OPEX and create dependency on vendor roadmaps and patch cycles. Building in‑house stacks or multisourcing reduces single‑vendor risk and strengthens negotiation leverage.

Specialized training and compliance providers

Regulatory training, firearms instruction where applicable, and compliance audits rely on accredited external providers, giving suppliers leverage in niche certifications and audit windows. Limited accredited providers for specialized courses tighten scheduling and certification timelines, creating operational bottlenecks for Segur Ibérica. Building internal academies and in-house auditors can reduce reliance and recover bargaining power.

- Accredited providers concentrated in niches

- Certification timelines as bottlenecks

- Firearms training requires strict accreditation

- Internal academy development reduces supplier influence

Equipment, uniforms, and fleet logistics

Uniforms, vehicles and wearable devices are largely commoditized, but 2024 fuel volatility (Brent ~83 USD/bbl) and input-price swings increase operating cost exposure; low switching costs keep supplier power moderate, though bulk orders and rapid-replacement SLAs tilt leverage toward established vendors; strategic sourcing and inventory planning materially curb this risk.

Regulated labor, concentrated suppliers and fuel volatility tighten margins

Guard labor is highly regulated (SMI €1,080/mo, 2024) and unionized, raising supplier power; regional shortages and training costs compress margins. Hardware suppliers are concentrated, post‑2021 shortages shifted leverage to OEMs; SLAs/interop create switching frictions. Telecom/software carry recurring subscription leverage (99.9% SLA); fuels (Brent ~83 USD/bbl, 2024) and logistics add cost volatility.

| Supplier | Power | Key metric |

|---|---|---|

| Labor | High | SMI €1,080/mo (2024) |

| Hardware | Moderate‑High | Post‑2021 shortages |

| Software/Telecom | High | 99.9% SLA |

| Fuel/Logistics | Moderate | Brent ~83 USD/bbl (2024) |

What is included in the product

Tailored exclusively for Segur Ibérica, S.A., this Porter’s Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers and substitute threats, identifying disruptive forces and market dynamics that shape its pricing power and profitability.

Clear Porter's Five Forces summary for Segur Ibérica S.A.—instantly highlights competitive threats and bargaining pressures so executives can prioritize risk mitigations and allocate resources faster.

Customers Bargaining Power

Large corporate and public tenders

Enterprise and public-sector clients buy security services via competitive RFPs, driving strong price pressure; EU public procurement totaled about €2 trillion annually (around 14% of EU GDP) in recent years, concentrating buying power in large tenders. Multi-year contracts and scale let buyers extract deeper discounts and impose stringent SLAs. Procurement digitization raises vendor comparability, but integrated, end-to-end security solutions can soften pure price competition.

Service standardization

Manned guarding and basic monitoring are highly standardized in Spain, giving buyers strong leverage; about 140,000 licensed private security professionals in 2024 increase supplier homogeneity and bidding comparability. Clear benchmarks enable apples-to-apples bids and lower switching costs when customization is minimal. Bundling consulting and advanced tech, however, raises switching costs and creates client stickiness.

Switching costs and contract churn

Operational transition costs for Segur Ibérica are present but manageable for experienced buyers, with typical security services contracts running 3–5 years and one-off onboarding costs often absorbed over the contract term. Knowledge transfer, re-badging, and site onboarding create short-term friction that can raise first-year labor and compliance expenses. Performance KPIs and penalty clauses—standard in 2024 procurement—drive vendor discipline and empower buyers. Strong relationship management and account governance reduce annual churn risk, often targeting sub-10% turnover.

Ability to insource security

Some clients can internalize guard forces or monitoring, reducing dependency and increasing negotiating leverage; however, the global security services market surpassed $200 billion in 2024, underscoring continued outsourcing demand. In-house teams improve control but struggle with compliance, 24/7 coverage and integrating advanced tech, so demonstrated ROI and measurable risk reduction often favor providers like Segur Ibérica.

- Insourcing reduces vendor reliance

- Compliance and 24/7 ops favor outsourcing

- 2024 market > $200B supports provider scale

- ROI and risk metrics counter insourcing

Demand for integrated, outcome-based solutions

Buyers increasingly demand unified guarding, systems and analytics tied to risk outcomes; a 2024 industry survey found 58% of corporate security buyers now prioritize integrated solutions over standalone services. This shifts negotiations from hourly rates toward value delivered, with vendors demonstrating incident reduction and compliance gains reclaiming pricing power. Data-driven reporting correlates with a reported 12% higher renewal rate in 2024.

- 58% buyers prefer integrated solutions (2024)

- Shift from hourly to outcome pricing

- 12% higher renewals when incident reduction is proven

€2T EU tenders force price pressure; 58% want integrated; renewals +12%

Buyers exert strong price pressure via competitive RFPs and large public tenders (€2T EU procurement), while standardized services and ~140,000 licensed Spanish guards increase comparability. Outsourcing remains favored given global market >$200B and compliance/24/7 needs; 58% prefer integrated solutions and proof of incident reduction boosts renewals ~12%.

| Metric | 2024 value |

|---|---|

| EU public procurement | €2 trillion |

| Spanish licensed guards | 140,000 |

| Global security market | $200B+ |

| Buyers pref integrated | 58% |

| Renewal lift w/ proof | 12% |

Same Document Delivered

Segur Ibérica, S.A. Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Segur Ibérica, S.A. assesses competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry, providing actionable insights and strategic implications. The preview you see is the exact document you’ll receive immediately after purchase—fully formatted and ready to use. No mockups, no placeholders.

Go Beyond the Preview—Access the Full Strategic Report

Segur Ibérica, S.A. faces moderate buyer power, concentrated supplier relationships, and rising substitute and entrant threats driven by tech-enabled security services; rivalry is intense among national and regional players. This snapshot highlights key pressure points and strategic levers. This preview is just the beginning—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Reliance on licensed guard labor

Guard supply for Segur Ibérica is critical and highly regulated (Real Decreto 2364/1994) with unionized labor, giving workers measurable bargaining power; wage floors and collective agreements anchored to the 2024 SMI of €1,080/mo plus overtime premiums and mandatory certifications limit cost flexibility. Regional shortages can compress margins, and retention/training reduce disruption but raise fixed costs.

Dependence on security tech vendors

Hardware for CCTV, access control, alarms and sensors is concentrated among a handful of global OEMs, giving those suppliers de facto leverage while interoperability standards limit absolute lock-in. Proprietary ecosystems still create switching frictions and volume discounts advantage large buyers, though the 2021–22 component shortage briefly shifted bargaining power toward suppliers. Long-term framework agreements are used to stabilize pricing and secure supply.

Software platforms and monitoring infrastructure

Alarm receiving centers and analytics depend on specialized software and telecom services with strict 99.9% uptime SLAs and continuous cybersecurity monitoring, embedding recurring supplier leverage through subscription licensing and data‑hosting terms. These contracts drive predictable OPEX and create dependency on vendor roadmaps and patch cycles. Building in‑house stacks or multisourcing reduces single‑vendor risk and strengthens negotiation leverage.

Specialized training and compliance providers

Regulatory training, firearms instruction where applicable, and compliance audits rely on accredited external providers, giving suppliers leverage in niche certifications and audit windows. Limited accredited providers for specialized courses tighten scheduling and certification timelines, creating operational bottlenecks for Segur Ibérica. Building internal academies and in-house auditors can reduce reliance and recover bargaining power.

- Accredited providers concentrated in niches

- Certification timelines as bottlenecks

- Firearms training requires strict accreditation

- Internal academy development reduces supplier influence

Equipment, uniforms, and fleet logistics

Uniforms, vehicles and wearable devices are largely commoditized, but 2024 fuel volatility (Brent ~83 USD/bbl) and input-price swings increase operating cost exposure; low switching costs keep supplier power moderate, though bulk orders and rapid-replacement SLAs tilt leverage toward established vendors; strategic sourcing and inventory planning materially curb this risk.

Regulated labor, concentrated suppliers and fuel volatility tighten margins

Guard labor is highly regulated (SMI €1,080/mo, 2024) and unionized, raising supplier power; regional shortages and training costs compress margins. Hardware suppliers are concentrated, post‑2021 shortages shifted leverage to OEMs; SLAs/interop create switching frictions. Telecom/software carry recurring subscription leverage (99.9% SLA); fuels (Brent ~83 USD/bbl, 2024) and logistics add cost volatility.

| Supplier | Power | Key metric |

|---|---|---|

| Labor | High | SMI €1,080/mo (2024) |

| Hardware | Moderate‑High | Post‑2021 shortages |

| Software/Telecom | High | 99.9% SLA |

| Fuel/Logistics | Moderate | Brent ~83 USD/bbl (2024) |

What is included in the product

Tailored exclusively for Segur Ibérica, S.A., this Porter’s Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers and substitute threats, identifying disruptive forces and market dynamics that shape its pricing power and profitability.

Clear Porter's Five Forces summary for Segur Ibérica S.A.—instantly highlights competitive threats and bargaining pressures so executives can prioritize risk mitigations and allocate resources faster.

Customers Bargaining Power

Large corporate and public tenders

Enterprise and public-sector clients buy security services via competitive RFPs, driving strong price pressure; EU public procurement totaled about €2 trillion annually (around 14% of EU GDP) in recent years, concentrating buying power in large tenders. Multi-year contracts and scale let buyers extract deeper discounts and impose stringent SLAs. Procurement digitization raises vendor comparability, but integrated, end-to-end security solutions can soften pure price competition.

Service standardization

Manned guarding and basic monitoring are highly standardized in Spain, giving buyers strong leverage; about 140,000 licensed private security professionals in 2024 increase supplier homogeneity and bidding comparability. Clear benchmarks enable apples-to-apples bids and lower switching costs when customization is minimal. Bundling consulting and advanced tech, however, raises switching costs and creates client stickiness.

Switching costs and contract churn

Operational transition costs for Segur Ibérica are present but manageable for experienced buyers, with typical security services contracts running 3–5 years and one-off onboarding costs often absorbed over the contract term. Knowledge transfer, re-badging, and site onboarding create short-term friction that can raise first-year labor and compliance expenses. Performance KPIs and penalty clauses—standard in 2024 procurement—drive vendor discipline and empower buyers. Strong relationship management and account governance reduce annual churn risk, often targeting sub-10% turnover.

Ability to insource security

Some clients can internalize guard forces or monitoring, reducing dependency and increasing negotiating leverage; however, the global security services market surpassed $200 billion in 2024, underscoring continued outsourcing demand. In-house teams improve control but struggle with compliance, 24/7 coverage and integrating advanced tech, so demonstrated ROI and measurable risk reduction often favor providers like Segur Ibérica.

- Insourcing reduces vendor reliance

- Compliance and 24/7 ops favor outsourcing

- 2024 market > $200B supports provider scale

- ROI and risk metrics counter insourcing

Demand for integrated, outcome-based solutions

Buyers increasingly demand unified guarding, systems and analytics tied to risk outcomes; a 2024 industry survey found 58% of corporate security buyers now prioritize integrated solutions over standalone services. This shifts negotiations from hourly rates toward value delivered, with vendors demonstrating incident reduction and compliance gains reclaiming pricing power. Data-driven reporting correlates with a reported 12% higher renewal rate in 2024.

- 58% buyers prefer integrated solutions (2024)

- Shift from hourly to outcome pricing

- 12% higher renewals when incident reduction is proven

€2T EU tenders force price pressure; 58% want integrated; renewals +12%

Buyers exert strong price pressure via competitive RFPs and large public tenders (€2T EU procurement), while standardized services and ~140,000 licensed Spanish guards increase comparability. Outsourcing remains favored given global market >$200B and compliance/24/7 needs; 58% prefer integrated solutions and proof of incident reduction boosts renewals ~12%.

| Metric | 2024 value |

|---|---|

| EU public procurement | €2 trillion |

| Spanish licensed guards | 140,000 |

| Global security market | $200B+ |

| Buyers pref integrated | 58% |

| Renewal lift w/ proof | 12% |

Same Document Delivered

Segur Ibérica, S.A. Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Segur Ibérica, S.A. assesses competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry, providing actionable insights and strategic implications. The preview you see is the exact document you’ll receive immediately after purchase—fully formatted and ready to use. No mockups, no placeholders.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Segur Ibérica, S.A. faces moderate buyer power, concentrated supplier relationships, and rising substitute and entrant threats driven by tech-enabled security services; rivalry is intense among national and regional players. This snapshot highlights key pressure points and strategic levers. This preview is just the beginning—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Reliance on licensed guard labor

Guard supply for Segur Ibérica is critical and highly regulated (Real Decreto 2364/1994) with unionized labor, giving workers measurable bargaining power; wage floors and collective agreements anchored to the 2024 SMI of €1,080/mo plus overtime premiums and mandatory certifications limit cost flexibility. Regional shortages can compress margins, and retention/training reduce disruption but raise fixed costs.

Dependence on security tech vendors

Hardware for CCTV, access control, alarms and sensors is concentrated among a handful of global OEMs, giving those suppliers de facto leverage while interoperability standards limit absolute lock-in. Proprietary ecosystems still create switching frictions and volume discounts advantage large buyers, though the 2021–22 component shortage briefly shifted bargaining power toward suppliers. Long-term framework agreements are used to stabilize pricing and secure supply.

Software platforms and monitoring infrastructure

Alarm receiving centers and analytics depend on specialized software and telecom services with strict 99.9% uptime SLAs and continuous cybersecurity monitoring, embedding recurring supplier leverage through subscription licensing and data‑hosting terms. These contracts drive predictable OPEX and create dependency on vendor roadmaps and patch cycles. Building in‑house stacks or multisourcing reduces single‑vendor risk and strengthens negotiation leverage.

Specialized training and compliance providers

Regulatory training, firearms instruction where applicable, and compliance audits rely on accredited external providers, giving suppliers leverage in niche certifications and audit windows. Limited accredited providers for specialized courses tighten scheduling and certification timelines, creating operational bottlenecks for Segur Ibérica. Building internal academies and in-house auditors can reduce reliance and recover bargaining power.

- Accredited providers concentrated in niches

- Certification timelines as bottlenecks

- Firearms training requires strict accreditation

- Internal academy development reduces supplier influence

Equipment, uniforms, and fleet logistics

Uniforms, vehicles and wearable devices are largely commoditized, but 2024 fuel volatility (Brent ~83 USD/bbl) and input-price swings increase operating cost exposure; low switching costs keep supplier power moderate, though bulk orders and rapid-replacement SLAs tilt leverage toward established vendors; strategic sourcing and inventory planning materially curb this risk.

Regulated labor, concentrated suppliers and fuel volatility tighten margins

Guard labor is highly regulated (SMI €1,080/mo, 2024) and unionized, raising supplier power; regional shortages and training costs compress margins. Hardware suppliers are concentrated, post‑2021 shortages shifted leverage to OEMs; SLAs/interop create switching frictions. Telecom/software carry recurring subscription leverage (99.9% SLA); fuels (Brent ~83 USD/bbl, 2024) and logistics add cost volatility.

| Supplier | Power | Key metric |

|---|---|---|

| Labor | High | SMI €1,080/mo (2024) |

| Hardware | Moderate‑High | Post‑2021 shortages |

| Software/Telecom | High | 99.9% SLA |

| Fuel/Logistics | Moderate | Brent ~83 USD/bbl (2024) |

What is included in the product

Tailored exclusively for Segur Ibérica, S.A., this Porter’s Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers and substitute threats, identifying disruptive forces and market dynamics that shape its pricing power and profitability.

Clear Porter's Five Forces summary for Segur Ibérica S.A.—instantly highlights competitive threats and bargaining pressures so executives can prioritize risk mitigations and allocate resources faster.

Customers Bargaining Power

Large corporate and public tenders

Enterprise and public-sector clients buy security services via competitive RFPs, driving strong price pressure; EU public procurement totaled about €2 trillion annually (around 14% of EU GDP) in recent years, concentrating buying power in large tenders. Multi-year contracts and scale let buyers extract deeper discounts and impose stringent SLAs. Procurement digitization raises vendor comparability, but integrated, end-to-end security solutions can soften pure price competition.

Service standardization

Manned guarding and basic monitoring are highly standardized in Spain, giving buyers strong leverage; about 140,000 licensed private security professionals in 2024 increase supplier homogeneity and bidding comparability. Clear benchmarks enable apples-to-apples bids and lower switching costs when customization is minimal. Bundling consulting and advanced tech, however, raises switching costs and creates client stickiness.

Switching costs and contract churn

Operational transition costs for Segur Ibérica are present but manageable for experienced buyers, with typical security services contracts running 3–5 years and one-off onboarding costs often absorbed over the contract term. Knowledge transfer, re-badging, and site onboarding create short-term friction that can raise first-year labor and compliance expenses. Performance KPIs and penalty clauses—standard in 2024 procurement—drive vendor discipline and empower buyers. Strong relationship management and account governance reduce annual churn risk, often targeting sub-10% turnover.

Ability to insource security

Some clients can internalize guard forces or monitoring, reducing dependency and increasing negotiating leverage; however, the global security services market surpassed $200 billion in 2024, underscoring continued outsourcing demand. In-house teams improve control but struggle with compliance, 24/7 coverage and integrating advanced tech, so demonstrated ROI and measurable risk reduction often favor providers like Segur Ibérica.

- Insourcing reduces vendor reliance

- Compliance and 24/7 ops favor outsourcing

- 2024 market > $200B supports provider scale

- ROI and risk metrics counter insourcing

Demand for integrated, outcome-based solutions

Buyers increasingly demand unified guarding, systems and analytics tied to risk outcomes; a 2024 industry survey found 58% of corporate security buyers now prioritize integrated solutions over standalone services. This shifts negotiations from hourly rates toward value delivered, with vendors demonstrating incident reduction and compliance gains reclaiming pricing power. Data-driven reporting correlates with a reported 12% higher renewal rate in 2024.

- 58% buyers prefer integrated solutions (2024)

- Shift from hourly to outcome pricing

- 12% higher renewals when incident reduction is proven

€2T EU tenders force price pressure; 58% want integrated; renewals +12%

Buyers exert strong price pressure via competitive RFPs and large public tenders (€2T EU procurement), while standardized services and ~140,000 licensed Spanish guards increase comparability. Outsourcing remains favored given global market >$200B and compliance/24/7 needs; 58% prefer integrated solutions and proof of incident reduction boosts renewals ~12%.

| Metric | 2024 value |

|---|---|

| EU public procurement | €2 trillion |

| Spanish licensed guards | 140,000 |

| Global security market | $200B+ |

| Buyers pref integrated | 58% |

| Renewal lift w/ proof | 12% |

Same Document Delivered

Segur Ibérica, S.A. Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Segur Ibérica, S.A. assesses competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry, providing actionable insights and strategic implications. The preview you see is the exact document you’ll receive immediately after purchase—fully formatted and ready to use. No mockups, no placeholders.