GS Holdings Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

GS Holdings faces moderate supplier power and evolving buyer demands, while barriers to entry and substitute threats vary across its energy and retail segments; competitive rivalry is intensifying with regional peers. This snapshot highlights key pressures but omits force-level ratings, visuals, and tactical implications. Unlock the full Porter's Five Forces Analysis to access detailed ratings, charts, and strategic recommendations tailored to GS Holdings.

Suppliers Bargaining Power

Scale-driven sourcing

As of 2024 GS Holdings leverages scale across three core sectors—energy, retail and construction—to enable consolidated procurement that dilutes individual supplier leverage. Cross-affiliate category management standardizes specs and prices, driving volume discounts and tighter contract terms. Heterogeneous inputs (fuel, retail MRO, EPC parts) limit full aggregation, so supplier power ranges from low for commoditized MRO to high for specialized EPC components.

Commodity input exposure

Energy affiliates rely on crude, LNG and petrochemical feedstocks where OPEC+ production policy keeps supplier leverage high; Brent averaged ~$86/bbl in 2024 and JKM LNG spot near $12/MMBtu, lifting input costs. Price volatility can quickly compress downstream margins. Hedging programs and multi-year supply contracts have partially offset swings. Diversifying sources and price pass-through clauses remain critical to preserve margins.

Specialized equipment and tech

Construction and energy projects for GS Holdings rely on OEM equipment and licensed technologies, creating supplier pockets of dominance where specialized items and IP drive procurement decisions. Lead times for major equipment in 2024 commonly run 12–24 months, raising switching costs and long qualification timelines. Multi-vendor qualification and lifecycle service agreements (typically 10–25 year terms) lower single-supplier exposure and maintenance risk. Local content strategies in procurement can shift bargaining leverage toward GS by developing domestic supplier capacity.

Retail FMCG brands

- CPG shelf power: high promotional share

- Private label: ~18% global grocery share (2024)

- Data-sharing: placement for improved terms

- Fragmented suppliers: reduced aggregate strength

Labor and subcontractors

Skilled labor and subcontractor capacity for GS Holdings tightened in the 2024 upcycle, with construction wages rising about 5% year-on-year and compliance-related costs lifting input rigidity; long-term contractor frameworks and performance-based pay drove steadier availability and reduced turnover.

- 2024 wage growth ~5%

- Performance pay lowers churn

- Long-term contracts cap price volatility

- Workforce development improves negotiation leverage

Scale lowers commodity supplier power; energy prices and construction bottlenecks raise input risk

GS Holdings' scale and cross-affiliate procurement reduce supplier power for commoditized inputs, while specialized EPC/OEM suppliers retain high leverage; Brent ~$86/bbl and JKM ~$12/MMBtu in 2024 raised energy input pressure. Private label ~18% (2024) shifts CPG bargaining; construction wages +5% YoY and equipment lead times 12–24 months increase supplier hold.

| Category | 2024 metric | Impact |

|---|---|---|

| Crude/LNG | Brent ~$86/bbl; JKM ~$12/MMBtu | High supplier leverage |

| CPG | Private label ~18% | Retail negotiation shift |

| Construction | Wages +5%; lead times 12–24m | Higher switching costs |

What is included in the product

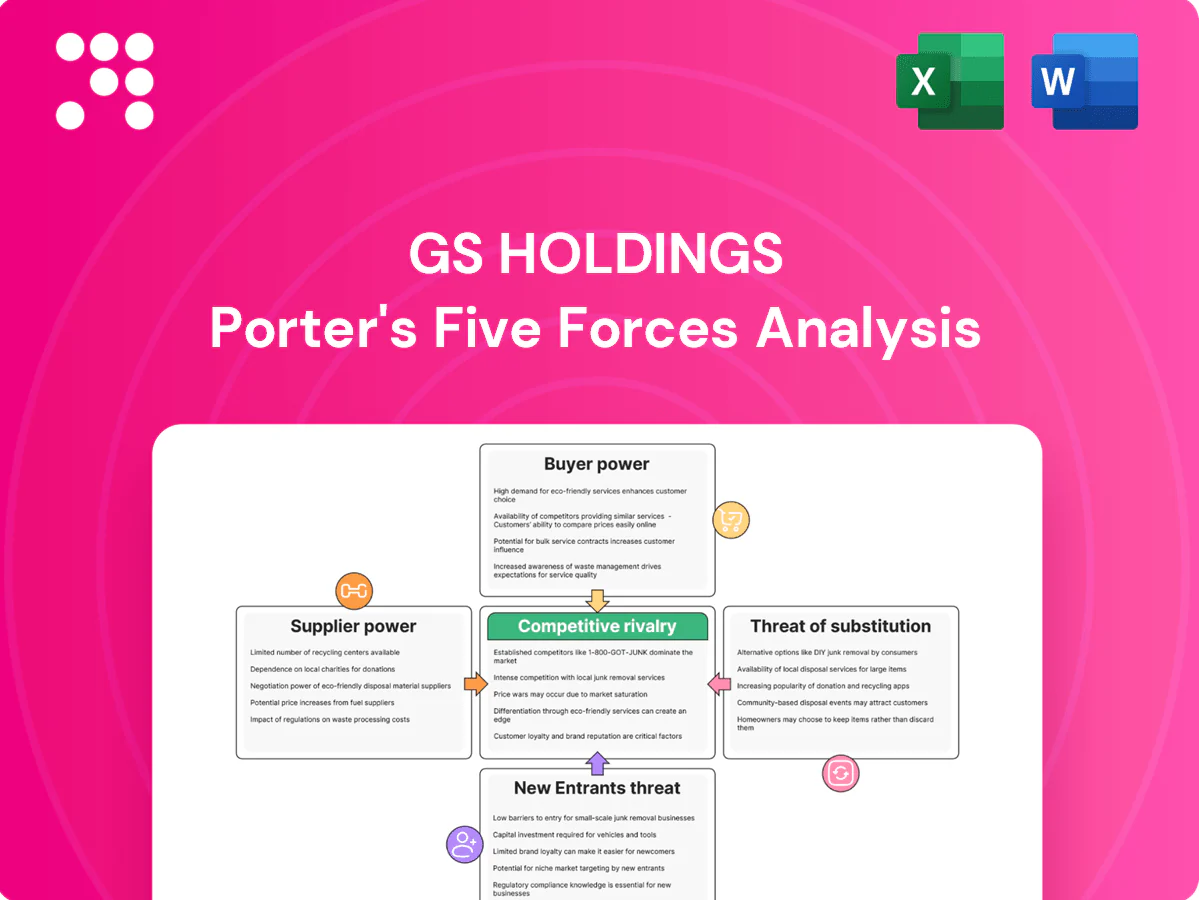

Comprehensive Porter's Five Forces analysis tailored for GS Holdings, assessing competitive rivalry, buyer and supplier power, threat of entrants and substitutes, and highlighting strategic risks and opportunities shaping its market position.

One-sheet Porter’s Five Forces for GS Holdings—quickly spot competitive pressures, customize force levels with current data, and export a clear spider chart for decks or board meetings.

Customers Bargaining Power

End-consumer sensitivity

Retail customers face low switching costs and near-perfect price transparency, increasing buyer power; South Korea’s ~98% smartphone penetration and online price tools amplify this. GS Holdings’ convenience arm GS25’s ~15,000 stores and dense locations, plus omnichannel fulfillment, partially offset price pressure. Loyalty programs and promotions (members often drive >50% of transactions) are essential to retain traffic. Data-driven personalization reduces churn and raises basket size.

B2B and public clients

B2B and public offtakers run competitive tenders, amplifying buyer leverage; OECD data shows public procurement averages about 12% of GDP in 2024, concentrating purchasing power. Large contracts hinge on specs, price and risk-sharing, intensifying price pressure on suppliers. Differentiation in safety, schedule reliability and ESG commands premiums, while long-term service and O&M bundling deepens client stickiness.

Wholesale fuel customers

Wholesale fuel customers, especially commercial buyers in 2024, leverage volume and logistics scale to extract discounts and flexible delivery terms. Regional supply-demand balances and inventory swings in 2024 routinely dictated contract cadence and spot exposure. Index-linked pricing clauses in many contracts limited downside risk for suppliers. Value-added services such as fleet cards and data analytics shifted negotiations away from pure price competition.

Digital channel expectations

Buyers now demand seamless e-commerce, fast delivery and easy returns, raising service benchmarks; failing UX or speed increases their bargaining power and churn risk (2024 retail trend data shows accelerated shift to digital channels).

GS Holdings' investments in last-mile, dark stores and app ecosystems reduce this power, while membership tiers and loyalty programs lock in repeat purchase behavior and raise switching costs.

- Digital expectations: higher bargaining power if unmet

- Operational response: last-mile, dark stores, apps

- Retention: membership tiers increase repeat buys

ESG-conscious purchasers

- 2024: global sustainable investment ~41 trillion USD, raising buyer leverage

- Corporate net-zero targets shift demand toward low-carbon offerings

- Certified reporting (ISO, SASB) improves pricing power and access to green premiums

Smartphone power, loyalty and green capital reshape retail sourcing and customer churn

Customers wield high bargaining power due to ~98% smartphone penetration and near-perfect price transparency; GS25’s ~15,000 stores and omnichannel reach partially mitigate this. Loyalty programs drive >50% of transactions and raise switching costs. Public tenders (≈12% of GDP) and 2024 sustainable investment (~41tn USD) shift volume toward certified, low-carbon suppliers.

| Metric | 2024 |

|---|---|

| Smartphone penetration | 98% |

| GS25 stores | ~15,000 |

| Transactions via members | >50% |

| Public procurement | ~12% GDP |

| Sustainable assets | 41tn USD |

Same Document Delivered

GS Holdings Porter's Five Forces Analysis

This preview is the GS Holdings Porter's Five Forces Analysis and contains the full, professionally formatted assessment you'll receive immediately after purchase. It includes competitive dynamics, supplier and buyer power, threat of entry and substitutes, and strategic implications. No mockups or placeholders—this is the exact downloadable file ready for use.

A Must-Have Tool for Decision-Makers

GS Holdings faces moderate supplier power and evolving buyer demands, while barriers to entry and substitute threats vary across its energy and retail segments; competitive rivalry is intensifying with regional peers. This snapshot highlights key pressures but omits force-level ratings, visuals, and tactical implications. Unlock the full Porter's Five Forces Analysis to access detailed ratings, charts, and strategic recommendations tailored to GS Holdings.

Suppliers Bargaining Power

Scale-driven sourcing

As of 2024 GS Holdings leverages scale across three core sectors—energy, retail and construction—to enable consolidated procurement that dilutes individual supplier leverage. Cross-affiliate category management standardizes specs and prices, driving volume discounts and tighter contract terms. Heterogeneous inputs (fuel, retail MRO, EPC parts) limit full aggregation, so supplier power ranges from low for commoditized MRO to high for specialized EPC components.

Commodity input exposure

Energy affiliates rely on crude, LNG and petrochemical feedstocks where OPEC+ production policy keeps supplier leverage high; Brent averaged ~$86/bbl in 2024 and JKM LNG spot near $12/MMBtu, lifting input costs. Price volatility can quickly compress downstream margins. Hedging programs and multi-year supply contracts have partially offset swings. Diversifying sources and price pass-through clauses remain critical to preserve margins.

Specialized equipment and tech

Construction and energy projects for GS Holdings rely on OEM equipment and licensed technologies, creating supplier pockets of dominance where specialized items and IP drive procurement decisions. Lead times for major equipment in 2024 commonly run 12–24 months, raising switching costs and long qualification timelines. Multi-vendor qualification and lifecycle service agreements (typically 10–25 year terms) lower single-supplier exposure and maintenance risk. Local content strategies in procurement can shift bargaining leverage toward GS by developing domestic supplier capacity.

Retail FMCG brands

- CPG shelf power: high promotional share

- Private label: ~18% global grocery share (2024)

- Data-sharing: placement for improved terms

- Fragmented suppliers: reduced aggregate strength

Labor and subcontractors

Skilled labor and subcontractor capacity for GS Holdings tightened in the 2024 upcycle, with construction wages rising about 5% year-on-year and compliance-related costs lifting input rigidity; long-term contractor frameworks and performance-based pay drove steadier availability and reduced turnover.

- 2024 wage growth ~5%

- Performance pay lowers churn

- Long-term contracts cap price volatility

- Workforce development improves negotiation leverage

Scale lowers commodity supplier power; energy prices and construction bottlenecks raise input risk

GS Holdings' scale and cross-affiliate procurement reduce supplier power for commoditized inputs, while specialized EPC/OEM suppliers retain high leverage; Brent ~$86/bbl and JKM ~$12/MMBtu in 2024 raised energy input pressure. Private label ~18% (2024) shifts CPG bargaining; construction wages +5% YoY and equipment lead times 12–24 months increase supplier hold.

| Category | 2024 metric | Impact |

|---|---|---|

| Crude/LNG | Brent ~$86/bbl; JKM ~$12/MMBtu | High supplier leverage |

| CPG | Private label ~18% | Retail negotiation shift |

| Construction | Wages +5%; lead times 12–24m | Higher switching costs |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for GS Holdings, assessing competitive rivalry, buyer and supplier power, threat of entrants and substitutes, and highlighting strategic risks and opportunities shaping its market position.

One-sheet Porter’s Five Forces for GS Holdings—quickly spot competitive pressures, customize force levels with current data, and export a clear spider chart for decks or board meetings.

Customers Bargaining Power

End-consumer sensitivity

Retail customers face low switching costs and near-perfect price transparency, increasing buyer power; South Korea’s ~98% smartphone penetration and online price tools amplify this. GS Holdings’ convenience arm GS25’s ~15,000 stores and dense locations, plus omnichannel fulfillment, partially offset price pressure. Loyalty programs and promotions (members often drive >50% of transactions) are essential to retain traffic. Data-driven personalization reduces churn and raises basket size.

B2B and public clients

B2B and public offtakers run competitive tenders, amplifying buyer leverage; OECD data shows public procurement averages about 12% of GDP in 2024, concentrating purchasing power. Large contracts hinge on specs, price and risk-sharing, intensifying price pressure on suppliers. Differentiation in safety, schedule reliability and ESG commands premiums, while long-term service and O&M bundling deepens client stickiness.

Wholesale fuel customers

Wholesale fuel customers, especially commercial buyers in 2024, leverage volume and logistics scale to extract discounts and flexible delivery terms. Regional supply-demand balances and inventory swings in 2024 routinely dictated contract cadence and spot exposure. Index-linked pricing clauses in many contracts limited downside risk for suppliers. Value-added services such as fleet cards and data analytics shifted negotiations away from pure price competition.

Digital channel expectations

Buyers now demand seamless e-commerce, fast delivery and easy returns, raising service benchmarks; failing UX or speed increases their bargaining power and churn risk (2024 retail trend data shows accelerated shift to digital channels).

GS Holdings' investments in last-mile, dark stores and app ecosystems reduce this power, while membership tiers and loyalty programs lock in repeat purchase behavior and raise switching costs.

- Digital expectations: higher bargaining power if unmet

- Operational response: last-mile, dark stores, apps

- Retention: membership tiers increase repeat buys

ESG-conscious purchasers

- 2024: global sustainable investment ~41 trillion USD, raising buyer leverage

- Corporate net-zero targets shift demand toward low-carbon offerings

- Certified reporting (ISO, SASB) improves pricing power and access to green premiums

Smartphone power, loyalty and green capital reshape retail sourcing and customer churn

Customers wield high bargaining power due to ~98% smartphone penetration and near-perfect price transparency; GS25’s ~15,000 stores and omnichannel reach partially mitigate this. Loyalty programs drive >50% of transactions and raise switching costs. Public tenders (≈12% of GDP) and 2024 sustainable investment (~41tn USD) shift volume toward certified, low-carbon suppliers.

| Metric | 2024 |

|---|---|

| Smartphone penetration | 98% |

| GS25 stores | ~15,000 |

| Transactions via members | >50% |

| Public procurement | ~12% GDP |

| Sustainable assets | 41tn USD |

Same Document Delivered

GS Holdings Porter's Five Forces Analysis

This preview is the GS Holdings Porter's Five Forces Analysis and contains the full, professionally formatted assessment you'll receive immediately after purchase. It includes competitive dynamics, supplier and buyer power, threat of entry and substitutes, and strategic implications. No mockups or placeholders—this is the exact downloadable file ready for use.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

GS Holdings faces moderate supplier power and evolving buyer demands, while barriers to entry and substitute threats vary across its energy and retail segments; competitive rivalry is intensifying with regional peers. This snapshot highlights key pressures but omits force-level ratings, visuals, and tactical implications. Unlock the full Porter's Five Forces Analysis to access detailed ratings, charts, and strategic recommendations tailored to GS Holdings.

Suppliers Bargaining Power

Scale-driven sourcing

As of 2024 GS Holdings leverages scale across three core sectors—energy, retail and construction—to enable consolidated procurement that dilutes individual supplier leverage. Cross-affiliate category management standardizes specs and prices, driving volume discounts and tighter contract terms. Heterogeneous inputs (fuel, retail MRO, EPC parts) limit full aggregation, so supplier power ranges from low for commoditized MRO to high for specialized EPC components.

Commodity input exposure

Energy affiliates rely on crude, LNG and petrochemical feedstocks where OPEC+ production policy keeps supplier leverage high; Brent averaged ~$86/bbl in 2024 and JKM LNG spot near $12/MMBtu, lifting input costs. Price volatility can quickly compress downstream margins. Hedging programs and multi-year supply contracts have partially offset swings. Diversifying sources and price pass-through clauses remain critical to preserve margins.

Specialized equipment and tech

Construction and energy projects for GS Holdings rely on OEM equipment and licensed technologies, creating supplier pockets of dominance where specialized items and IP drive procurement decisions. Lead times for major equipment in 2024 commonly run 12–24 months, raising switching costs and long qualification timelines. Multi-vendor qualification and lifecycle service agreements (typically 10–25 year terms) lower single-supplier exposure and maintenance risk. Local content strategies in procurement can shift bargaining leverage toward GS by developing domestic supplier capacity.

Retail FMCG brands

- CPG shelf power: high promotional share

- Private label: ~18% global grocery share (2024)

- Data-sharing: placement for improved terms

- Fragmented suppliers: reduced aggregate strength

Labor and subcontractors

Skilled labor and subcontractor capacity for GS Holdings tightened in the 2024 upcycle, with construction wages rising about 5% year-on-year and compliance-related costs lifting input rigidity; long-term contractor frameworks and performance-based pay drove steadier availability and reduced turnover.

- 2024 wage growth ~5%

- Performance pay lowers churn

- Long-term contracts cap price volatility

- Workforce development improves negotiation leverage

Scale lowers commodity supplier power; energy prices and construction bottlenecks raise input risk

GS Holdings' scale and cross-affiliate procurement reduce supplier power for commoditized inputs, while specialized EPC/OEM suppliers retain high leverage; Brent ~$86/bbl and JKM ~$12/MMBtu in 2024 raised energy input pressure. Private label ~18% (2024) shifts CPG bargaining; construction wages +5% YoY and equipment lead times 12–24 months increase supplier hold.

| Category | 2024 metric | Impact |

|---|---|---|

| Crude/LNG | Brent ~$86/bbl; JKM ~$12/MMBtu | High supplier leverage |

| CPG | Private label ~18% | Retail negotiation shift |

| Construction | Wages +5%; lead times 12–24m | Higher switching costs |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for GS Holdings, assessing competitive rivalry, buyer and supplier power, threat of entrants and substitutes, and highlighting strategic risks and opportunities shaping its market position.

One-sheet Porter’s Five Forces for GS Holdings—quickly spot competitive pressures, customize force levels with current data, and export a clear spider chart for decks or board meetings.

Customers Bargaining Power

End-consumer sensitivity

Retail customers face low switching costs and near-perfect price transparency, increasing buyer power; South Korea’s ~98% smartphone penetration and online price tools amplify this. GS Holdings’ convenience arm GS25’s ~15,000 stores and dense locations, plus omnichannel fulfillment, partially offset price pressure. Loyalty programs and promotions (members often drive >50% of transactions) are essential to retain traffic. Data-driven personalization reduces churn and raises basket size.

B2B and public clients

B2B and public offtakers run competitive tenders, amplifying buyer leverage; OECD data shows public procurement averages about 12% of GDP in 2024, concentrating purchasing power. Large contracts hinge on specs, price and risk-sharing, intensifying price pressure on suppliers. Differentiation in safety, schedule reliability and ESG commands premiums, while long-term service and O&M bundling deepens client stickiness.

Wholesale fuel customers

Wholesale fuel customers, especially commercial buyers in 2024, leverage volume and logistics scale to extract discounts and flexible delivery terms. Regional supply-demand balances and inventory swings in 2024 routinely dictated contract cadence and spot exposure. Index-linked pricing clauses in many contracts limited downside risk for suppliers. Value-added services such as fleet cards and data analytics shifted negotiations away from pure price competition.

Digital channel expectations

Buyers now demand seamless e-commerce, fast delivery and easy returns, raising service benchmarks; failing UX or speed increases their bargaining power and churn risk (2024 retail trend data shows accelerated shift to digital channels).

GS Holdings' investments in last-mile, dark stores and app ecosystems reduce this power, while membership tiers and loyalty programs lock in repeat purchase behavior and raise switching costs.

- Digital expectations: higher bargaining power if unmet

- Operational response: last-mile, dark stores, apps

- Retention: membership tiers increase repeat buys

ESG-conscious purchasers

- 2024: global sustainable investment ~41 trillion USD, raising buyer leverage

- Corporate net-zero targets shift demand toward low-carbon offerings

- Certified reporting (ISO, SASB) improves pricing power and access to green premiums

Smartphone power, loyalty and green capital reshape retail sourcing and customer churn

Customers wield high bargaining power due to ~98% smartphone penetration and near-perfect price transparency; GS25’s ~15,000 stores and omnichannel reach partially mitigate this. Loyalty programs drive >50% of transactions and raise switching costs. Public tenders (≈12% of GDP) and 2024 sustainable investment (~41tn USD) shift volume toward certified, low-carbon suppliers.

| Metric | 2024 |

|---|---|

| Smartphone penetration | 98% |

| GS25 stores | ~15,000 |

| Transactions via members | >50% |

| Public procurement | ~12% GDP |

| Sustainable assets | 41tn USD |

Same Document Delivered

GS Holdings Porter's Five Forces Analysis

This preview is the GS Holdings Porter's Five Forces Analysis and contains the full, professionally formatted assessment you'll receive immediately after purchase. It includes competitive dynamics, supplier and buyer power, threat of entry and substitutes, and strategic implications. No mockups or placeholders—this is the exact downloadable file ready for use.