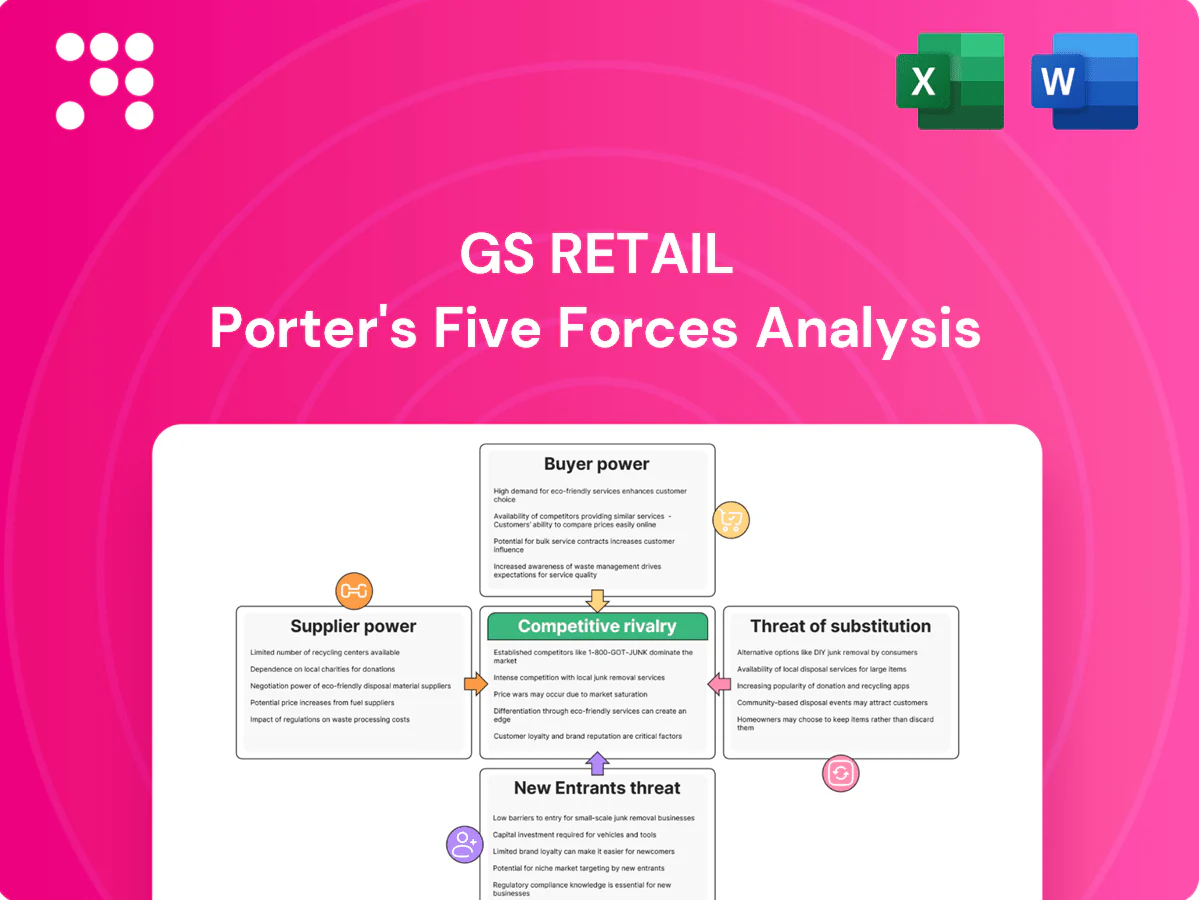

GS Retail Porter's Five Forces Analysis

From Overview to Strategy Blueprint

GS Retail faces intense local competition, shifting buyer preferences, and moderate supplier leverage that together shape slim margins and strategic urgency; new entrants and substitutes raise long-term risk. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy recommendations.

Suppliers Bargaining Power

Fragmented FMCG and fresh suppliers

GS Retail sources from hundreds of CPG brands and thousands of wholesalers and farmers, diluting single-supplier leverage; as of 2024 GS25’s ~13,500-store network and GS THE FRESH’s wide assortments support SKU substitution (10,000+ SKUs across formats). Perishables and seasonal produce can tighten supply short-term, while strategic vendor consolidation and growing private-label penetration mitigate supplier power spikes.

Global brands with pull power

Multinational beverage, tobacco and snack brands wield strong consumer pull, enabling leverage on pricing and shelf placement; the global soft drinks market was estimated at about US$520 billion in 2024, concentrating power among a few players. Limited exclusivity and brand loyalty raise switching costs for GS Retail, but the retailer mitigates this through category management and data-driven shelf optimization. Joint promotions and volume commitments help GS negotiate more balanced terms and protect margins.

Cold-chain and logistics dependencies

Perishable categories force reliance on capable cold-chain providers, concentrating bargaining power among few specialized logistics firms. Service quality and on-time delivery directly drive shrink and sales performance, making logistics KPIs critical. GS Retail’s in-house logistics network and scale—supporting about 16,000 stores in 2024—reduce dependence on external carriers. Multi-sourcing and strict performance SLAs further constrain supplier leverage.

Real estate and landlords

Prime convenience-store locations are scarce in dense Korean cities and landlords can push rents, raising negotiation pressure at lease renewals for high-traffic GS Retail sites. GS Retail’s scale — about 14,000 stores (2024) — and willingness to relocate within micro-trade areas provide counterbalance, while long-term leases and dense network coverage reduce overall exposure.

Private label and direct sourcing

Own-brand development shifts margin upstream and reduces reliance on branded suppliers; GS Retail leverages private labels across its network of over 14,000 GS25 stores in 2024 to capture higher gross margins. Direct sourcing for staples and ready-to-eat SKUs cuts intermediary power, while real-time POS and supply-chain data enable faster iteration and vendor replacement; quality-assurance investments preserve consumer trust.

- Private-label margin capture: upstream shift

- Direct sourcing: lowers intermediary leverage

- Data-driven vendor replacement: faster cycle times

- QA investment: maintains private-label acceptance

Extensive SKU range and in-house logistics reduce supplier leverage and protect margins

GS Retail’s broad supplier base and 10,000+ SKU assortments across ~13,500 GS25 stores (2024) limit single-supplier leverage. Multinational beverage/snack firms (global soft drinks market ~US$520bn in 2024) retain pricing and shelf power, managed via volume commitments and joint promotions. In-house logistics and private-label expansion reduce supplier dependence and protect margins.

| Metric | 2024 |

|---|---|

| GS25 stores | ~13,500 |

| Total stores | ~14,000 |

| SKUs across formats | 10,000+ |

| Soft drinks market | ~US$520bn |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored exclusively for GS Retail, uncovering competitive intensity, buyer and supplier power, entry barriers, substitutes, and disruptive threats shaping its market position. Fully editable in Word for use in investor decks, strategy plans, or academic projects with data-driven insights and strategic implications.

A concise, one-sheet Porter’s Five Forces for GS Retail—ready for quick boardroom decisions and pitch decks; customize pressure levels or swap in your data to reflect new competitors, regulations, or market shifts.

Customers Bargaining Power

Low switching costs for shoppers

Consumers can switch easily among GS25, CU, 7-Eleven, Emart24 and online channels, and with South Korea's e-commerce share near 30% of retail sales in 2024 substitution is swift. Proximity and price drive quick switching, keeping pricing and availability pressure high on margins. Differentiated assortments, private-labels and services like delivery and click‑and‑collect help GS Retail soften buyer power.

Price sensitivity and promotion intensity

Frequent promotions in snacks, beverages and meal kits have amplified deal-seeking, with promo-driven SKUs representing roughly 20–30% of in-store volume in Korea convenience channels; this raises customer price sensitivity and churn. App coupons and payment wallet tie-ins now account for about 25–35% of digital redemptions, increasing elasticity. GS Retail must calibrate promo depth to protect margins while using personalized offers and basket-building to raise average ticket and improve economics.

Loyalty programs and ecosystem effects

GS Retail leverages memberships, apps and GS&POINT to reward repeat purchases and reduce switching; its GS25 network of around 14,000 stores in Korea (2024) amplifies reach. Cross-channel integration with online GS Shop deepens stickiness, but rival chains like CU run comparable programs, capping defensibility. Exclusive brand partnerships and limited SKUs offer differentiation.

Delivery and quick-commerce expectations

Consumers expect rapid, reliable delivery for convenience items, and service failures prompt quick churn to platforms such as Coupang or Baemin; GS Retail’s network of about 15,000 GS25 stores in 2024 supports micro-fulfillment, reducing buyer leverage by improving speed and SKU availability.

- Faster delivery lowers customer bargaining power

- Service lapses drive platform switching

- ~15,000 stores enable networked micro-fulfillment

- Higher availability diminishes price/terms pressure

Corporate and franchise customer influence

B2B accounts and franchisees can negotiate assortment, pricing, and services, with GS Retail's nationwide GS25 network exceeding 13,000 stores in 2024, amplifying cluster bargaining clout in key regions. Transparent economics and franchise support programs published by GS Retail reduce conflicts and align incentives. Standardized contracts plus analytics-driven category guidance limit ad hoc concessions.

- Franchise scale: >13,000 stores (2024)

- Negotiation areas: assortment, pricing, services

- Alignment tools: transparent economics, support services

- Control levers: standardized contracts, analytics guidance

Shoppers switch fast among convenience chains and online; e‑commerce ≈30%, promos drive sensitivity

Customers switch quickly among GS25, CU, 7‑Eleven, Emart24 and online (e‑commerce ≈30% of retail sales in 2024), keeping price and availability pressure high. Promotions (≈20–30% of in‑store volume) and app coupons (≈25–35% redemptions) raise price sensitivity, while GS Retail’s memberships, private labels and ~15,000 GS25 stores reduce churn. Franchise negotiation power exists but is constrained by standardized contracts and analytics.

| Metric | 2024 value |

|---|---|

| E‑commerce share | ≈30% |

| GS25 stores | ≈15,000 |

| Promo-driven volume | 20–30% |

| App coupon redemptions | 25–35% |

| Franchise stores | >13,000 |

What You See Is What You Get

GS Retail Porter's Five Forces Analysis

This preview shows the exact GS Retail Porter’s Five Forces analysis you’ll receive—no mockups or placeholders. The document is fully formatted, professionally written, and ready for immediate download upon purchase. It delivers the complete competitive assessment, actionable insights, and implications for strategy and valuation as presented here.

From Overview to Strategy Blueprint

GS Retail faces intense local competition, shifting buyer preferences, and moderate supplier leverage that together shape slim margins and strategic urgency; new entrants and substitutes raise long-term risk. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy recommendations.

Suppliers Bargaining Power

Fragmented FMCG and fresh suppliers

GS Retail sources from hundreds of CPG brands and thousands of wholesalers and farmers, diluting single-supplier leverage; as of 2024 GS25’s ~13,500-store network and GS THE FRESH’s wide assortments support SKU substitution (10,000+ SKUs across formats). Perishables and seasonal produce can tighten supply short-term, while strategic vendor consolidation and growing private-label penetration mitigate supplier power spikes.

Global brands with pull power

Multinational beverage, tobacco and snack brands wield strong consumer pull, enabling leverage on pricing and shelf placement; the global soft drinks market was estimated at about US$520 billion in 2024, concentrating power among a few players. Limited exclusivity and brand loyalty raise switching costs for GS Retail, but the retailer mitigates this through category management and data-driven shelf optimization. Joint promotions and volume commitments help GS negotiate more balanced terms and protect margins.

Cold-chain and logistics dependencies

Perishable categories force reliance on capable cold-chain providers, concentrating bargaining power among few specialized logistics firms. Service quality and on-time delivery directly drive shrink and sales performance, making logistics KPIs critical. GS Retail’s in-house logistics network and scale—supporting about 16,000 stores in 2024—reduce dependence on external carriers. Multi-sourcing and strict performance SLAs further constrain supplier leverage.

Real estate and landlords

Prime convenience-store locations are scarce in dense Korean cities and landlords can push rents, raising negotiation pressure at lease renewals for high-traffic GS Retail sites. GS Retail’s scale — about 14,000 stores (2024) — and willingness to relocate within micro-trade areas provide counterbalance, while long-term leases and dense network coverage reduce overall exposure.

Private label and direct sourcing

Own-brand development shifts margin upstream and reduces reliance on branded suppliers; GS Retail leverages private labels across its network of over 14,000 GS25 stores in 2024 to capture higher gross margins. Direct sourcing for staples and ready-to-eat SKUs cuts intermediary power, while real-time POS and supply-chain data enable faster iteration and vendor replacement; quality-assurance investments preserve consumer trust.

- Private-label margin capture: upstream shift

- Direct sourcing: lowers intermediary leverage

- Data-driven vendor replacement: faster cycle times

- QA investment: maintains private-label acceptance

Extensive SKU range and in-house logistics reduce supplier leverage and protect margins

GS Retail’s broad supplier base and 10,000+ SKU assortments across ~13,500 GS25 stores (2024) limit single-supplier leverage. Multinational beverage/snack firms (global soft drinks market ~US$520bn in 2024) retain pricing and shelf power, managed via volume commitments and joint promotions. In-house logistics and private-label expansion reduce supplier dependence and protect margins.

| Metric | 2024 |

|---|---|

| GS25 stores | ~13,500 |

| Total stores | ~14,000 |

| SKUs across formats | 10,000+ |

| Soft drinks market | ~US$520bn |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored exclusively for GS Retail, uncovering competitive intensity, buyer and supplier power, entry barriers, substitutes, and disruptive threats shaping its market position. Fully editable in Word for use in investor decks, strategy plans, or academic projects with data-driven insights and strategic implications.

A concise, one-sheet Porter’s Five Forces for GS Retail—ready for quick boardroom decisions and pitch decks; customize pressure levels or swap in your data to reflect new competitors, regulations, or market shifts.

Customers Bargaining Power

Low switching costs for shoppers

Consumers can switch easily among GS25, CU, 7-Eleven, Emart24 and online channels, and with South Korea's e-commerce share near 30% of retail sales in 2024 substitution is swift. Proximity and price drive quick switching, keeping pricing and availability pressure high on margins. Differentiated assortments, private-labels and services like delivery and click‑and‑collect help GS Retail soften buyer power.

Price sensitivity and promotion intensity

Frequent promotions in snacks, beverages and meal kits have amplified deal-seeking, with promo-driven SKUs representing roughly 20–30% of in-store volume in Korea convenience channels; this raises customer price sensitivity and churn. App coupons and payment wallet tie-ins now account for about 25–35% of digital redemptions, increasing elasticity. GS Retail must calibrate promo depth to protect margins while using personalized offers and basket-building to raise average ticket and improve economics.

Loyalty programs and ecosystem effects

GS Retail leverages memberships, apps and GS&POINT to reward repeat purchases and reduce switching; its GS25 network of around 14,000 stores in Korea (2024) amplifies reach. Cross-channel integration with online GS Shop deepens stickiness, but rival chains like CU run comparable programs, capping defensibility. Exclusive brand partnerships and limited SKUs offer differentiation.

Delivery and quick-commerce expectations

Consumers expect rapid, reliable delivery for convenience items, and service failures prompt quick churn to platforms such as Coupang or Baemin; GS Retail’s network of about 15,000 GS25 stores in 2024 supports micro-fulfillment, reducing buyer leverage by improving speed and SKU availability.

- Faster delivery lowers customer bargaining power

- Service lapses drive platform switching

- ~15,000 stores enable networked micro-fulfillment

- Higher availability diminishes price/terms pressure

Corporate and franchise customer influence

B2B accounts and franchisees can negotiate assortment, pricing, and services, with GS Retail's nationwide GS25 network exceeding 13,000 stores in 2024, amplifying cluster bargaining clout in key regions. Transparent economics and franchise support programs published by GS Retail reduce conflicts and align incentives. Standardized contracts plus analytics-driven category guidance limit ad hoc concessions.

- Franchise scale: >13,000 stores (2024)

- Negotiation areas: assortment, pricing, services

- Alignment tools: transparent economics, support services

- Control levers: standardized contracts, analytics guidance

Shoppers switch fast among convenience chains and online; e‑commerce ≈30%, promos drive sensitivity

Customers switch quickly among GS25, CU, 7‑Eleven, Emart24 and online (e‑commerce ≈30% of retail sales in 2024), keeping price and availability pressure high. Promotions (≈20–30% of in‑store volume) and app coupons (≈25–35% redemptions) raise price sensitivity, while GS Retail’s memberships, private labels and ~15,000 GS25 stores reduce churn. Franchise negotiation power exists but is constrained by standardized contracts and analytics.

| Metric | 2024 value |

|---|---|

| E‑commerce share | ≈30% |

| GS25 stores | ≈15,000 |

| Promo-driven volume | 20–30% |

| App coupon redemptions | 25–35% |

| Franchise stores | >13,000 |

What You See Is What You Get

GS Retail Porter's Five Forces Analysis

This preview shows the exact GS Retail Porter’s Five Forces analysis you’ll receive—no mockups or placeholders. The document is fully formatted, professionally written, and ready for immediate download upon purchase. It delivers the complete competitive assessment, actionable insights, and implications for strategy and valuation as presented here.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

GS Retail faces intense local competition, shifting buyer preferences, and moderate supplier leverage that together shape slim margins and strategic urgency; new entrants and substitutes raise long-term risk. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy recommendations.

Suppliers Bargaining Power

Fragmented FMCG and fresh suppliers

GS Retail sources from hundreds of CPG brands and thousands of wholesalers and farmers, diluting single-supplier leverage; as of 2024 GS25’s ~13,500-store network and GS THE FRESH’s wide assortments support SKU substitution (10,000+ SKUs across formats). Perishables and seasonal produce can tighten supply short-term, while strategic vendor consolidation and growing private-label penetration mitigate supplier power spikes.

Global brands with pull power

Multinational beverage, tobacco and snack brands wield strong consumer pull, enabling leverage on pricing and shelf placement; the global soft drinks market was estimated at about US$520 billion in 2024, concentrating power among a few players. Limited exclusivity and brand loyalty raise switching costs for GS Retail, but the retailer mitigates this through category management and data-driven shelf optimization. Joint promotions and volume commitments help GS negotiate more balanced terms and protect margins.

Cold-chain and logistics dependencies

Perishable categories force reliance on capable cold-chain providers, concentrating bargaining power among few specialized logistics firms. Service quality and on-time delivery directly drive shrink and sales performance, making logistics KPIs critical. GS Retail’s in-house logistics network and scale—supporting about 16,000 stores in 2024—reduce dependence on external carriers. Multi-sourcing and strict performance SLAs further constrain supplier leverage.

Real estate and landlords

Prime convenience-store locations are scarce in dense Korean cities and landlords can push rents, raising negotiation pressure at lease renewals for high-traffic GS Retail sites. GS Retail’s scale — about 14,000 stores (2024) — and willingness to relocate within micro-trade areas provide counterbalance, while long-term leases and dense network coverage reduce overall exposure.

Private label and direct sourcing

Own-brand development shifts margin upstream and reduces reliance on branded suppliers; GS Retail leverages private labels across its network of over 14,000 GS25 stores in 2024 to capture higher gross margins. Direct sourcing for staples and ready-to-eat SKUs cuts intermediary power, while real-time POS and supply-chain data enable faster iteration and vendor replacement; quality-assurance investments preserve consumer trust.

- Private-label margin capture: upstream shift

- Direct sourcing: lowers intermediary leverage

- Data-driven vendor replacement: faster cycle times

- QA investment: maintains private-label acceptance

Extensive SKU range and in-house logistics reduce supplier leverage and protect margins

GS Retail’s broad supplier base and 10,000+ SKU assortments across ~13,500 GS25 stores (2024) limit single-supplier leverage. Multinational beverage/snack firms (global soft drinks market ~US$520bn in 2024) retain pricing and shelf power, managed via volume commitments and joint promotions. In-house logistics and private-label expansion reduce supplier dependence and protect margins.

| Metric | 2024 |

|---|---|

| GS25 stores | ~13,500 |

| Total stores | ~14,000 |

| SKUs across formats | 10,000+ |

| Soft drinks market | ~US$520bn |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored exclusively for GS Retail, uncovering competitive intensity, buyer and supplier power, entry barriers, substitutes, and disruptive threats shaping its market position. Fully editable in Word for use in investor decks, strategy plans, or academic projects with data-driven insights and strategic implications.

A concise, one-sheet Porter’s Five Forces for GS Retail—ready for quick boardroom decisions and pitch decks; customize pressure levels or swap in your data to reflect new competitors, regulations, or market shifts.

Customers Bargaining Power

Low switching costs for shoppers

Consumers can switch easily among GS25, CU, 7-Eleven, Emart24 and online channels, and with South Korea's e-commerce share near 30% of retail sales in 2024 substitution is swift. Proximity and price drive quick switching, keeping pricing and availability pressure high on margins. Differentiated assortments, private-labels and services like delivery and click‑and‑collect help GS Retail soften buyer power.

Price sensitivity and promotion intensity

Frequent promotions in snacks, beverages and meal kits have amplified deal-seeking, with promo-driven SKUs representing roughly 20–30% of in-store volume in Korea convenience channels; this raises customer price sensitivity and churn. App coupons and payment wallet tie-ins now account for about 25–35% of digital redemptions, increasing elasticity. GS Retail must calibrate promo depth to protect margins while using personalized offers and basket-building to raise average ticket and improve economics.

Loyalty programs and ecosystem effects

GS Retail leverages memberships, apps and GS&POINT to reward repeat purchases and reduce switching; its GS25 network of around 14,000 stores in Korea (2024) amplifies reach. Cross-channel integration with online GS Shop deepens stickiness, but rival chains like CU run comparable programs, capping defensibility. Exclusive brand partnerships and limited SKUs offer differentiation.

Delivery and quick-commerce expectations

Consumers expect rapid, reliable delivery for convenience items, and service failures prompt quick churn to platforms such as Coupang or Baemin; GS Retail’s network of about 15,000 GS25 stores in 2024 supports micro-fulfillment, reducing buyer leverage by improving speed and SKU availability.

- Faster delivery lowers customer bargaining power

- Service lapses drive platform switching

- ~15,000 stores enable networked micro-fulfillment

- Higher availability diminishes price/terms pressure

Corporate and franchise customer influence

B2B accounts and franchisees can negotiate assortment, pricing, and services, with GS Retail's nationwide GS25 network exceeding 13,000 stores in 2024, amplifying cluster bargaining clout in key regions. Transparent economics and franchise support programs published by GS Retail reduce conflicts and align incentives. Standardized contracts plus analytics-driven category guidance limit ad hoc concessions.

- Franchise scale: >13,000 stores (2024)

- Negotiation areas: assortment, pricing, services

- Alignment tools: transparent economics, support services

- Control levers: standardized contracts, analytics guidance

Shoppers switch fast among convenience chains and online; e‑commerce ≈30%, promos drive sensitivity

Customers switch quickly among GS25, CU, 7‑Eleven, Emart24 and online (e‑commerce ≈30% of retail sales in 2024), keeping price and availability pressure high. Promotions (≈20–30% of in‑store volume) and app coupons (≈25–35% redemptions) raise price sensitivity, while GS Retail’s memberships, private labels and ~15,000 GS25 stores reduce churn. Franchise negotiation power exists but is constrained by standardized contracts and analytics.

| Metric | 2024 value |

|---|---|

| E‑commerce share | ≈30% |

| GS25 stores | ≈15,000 |

| Promo-driven volume | 20–30% |

| App coupon redemptions | 25–35% |

| Franchise stores | >13,000 |

What You See Is What You Get

GS Retail Porter's Five Forces Analysis

This preview shows the exact GS Retail Porter’s Five Forces analysis you’ll receive—no mockups or placeholders. The document is fully formatted, professionally written, and ready for immediate download upon purchase. It delivers the complete competitive assessment, actionable insights, and implications for strategy and valuation as presented here.