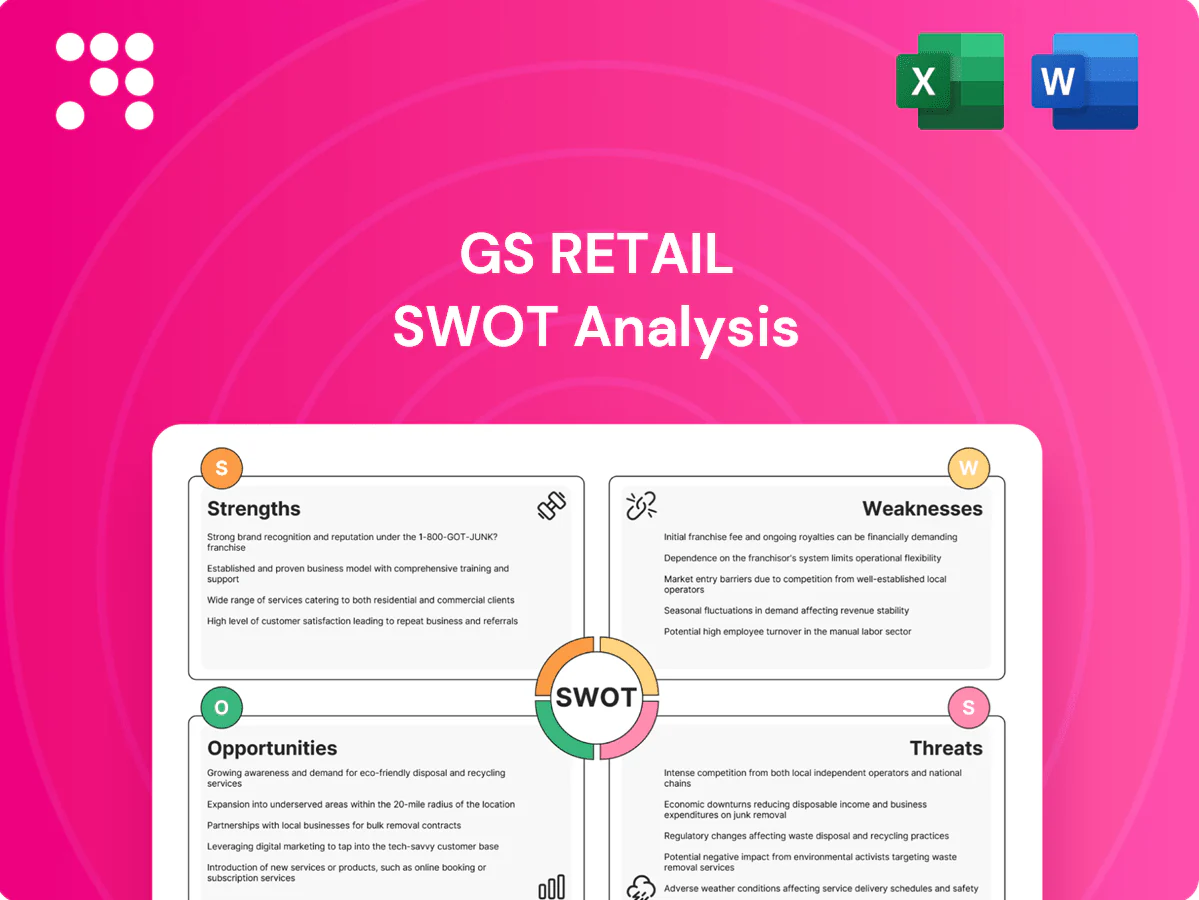

GS Retail SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

GS Retail's SWOT reveals strong market reach and omnichannel capability, counterbalanced by margin pressures and intense competition. Our full analysis dissects financial implications, strategic risks, and growth levers to inform investors and managers. Purchase the complete, editable SWOT (Word + Excel) for ready-to-use strategic insights.

Strengths

Nationwide GS25 footprint

GS Retail operates one of Korea’s largest convenience networks with over 14,000 GS25 stores nationwide as of 2024, driving high daily traffic and purchase frequency. Dense urban and transit placements create habitual purchases and sustained brand visibility, supporting same-store sales resilience. Scale delivers strong negotiating leverage with suppliers and logistics partners, and the resulting network effects raise barriers to entry for smaller rivals.

Strong brand and loyalty

GS25 and GS THE FRESH enjoy high recognition—GS Retail operates over 14,000 GS25 stores nationwide—with active loyalty programs and co-branded promotions driving engagement. Earn-and-burn mechanics boost basket size and repeat visits, while partnerships with KakaoPay and Naver Pay deepen payment engagement and data capture. Strong brand equity enables premium pricing on select categories, supporting higher category margins.

Omnichannel and delivery

Integrated online platforms extend convenience beyond stores via on-demand delivery and pickup, leveraging GS Retail's network of over 14,000 GS25 stores to act as fulfillment nodes. Last-mile partnerships shorten lead times and improve inventory turns through localized replenishment. Omnichannel reduces friction and broadens catchment areas, and supports targeted promotions based on real-time demand signals from POS and app data.

Private label and sourcing scale

GS Retail leverages scale—over 13,000 stores (2024)—to secure competitive procurement and create differentiated private-label assortments that lift margins and reduce direct price comparisons. Data-driven micro-location assortment optimizes SKU productivity, while deep supplier ties accelerate innovation cycles and shortened time-to-shelf.

- Scale: 13,000+ stores (2024)

- Margin uplift: private brands drive exclusivity

- Assortment: micro-location SKU optimization

- Speed: faster innovation via supplier partnerships

Diversified retail portfolio

GS Retail’s diversified mix across convenience, supermarkets, online and hotels spreads revenue risk; its GS25 network exceeds 16,000 stores (2024), enabling scale in procurement, logistics and marketing. Hospitality assets provide upsell and brand-extension channels that help smooth seasonal volatility and market shocks.

- Scale: GS25 >16,000 stores (2024)

- Synergies: procurement, logistics, marketing

- Upsell: hotels → brand extensions

- Risk: smoother seasonality

14,000+ stores, dense urban reach, strong payment partners and omnichannel fulfillment

GS Retail commands scale with over 14,000 GS25 stores (2024), driving high foot traffic, frequent purchases and strong supplier leverage. Recognized brands, loyalty programs and partnerships with KakaoPay and Naver Pay boost repeat sales and payment/data capture. Dense urban store network enables rapid last‑mile delivery and omnichannel fulfillment, supporting premium pricing on select categories and private‑label margin uplift.

| Metric | Value (2024) |

|---|---|

| GS25 stores | 14,000+ nationwide |

| Payment partners | KakaoPay, Naver Pay |

| Omnichannel | Delivery & pickup via GS25 network |

| Competitive edge | Procurement & supplier leverage |

What is included in the product

Provides a concise strategic overview of GS Retail’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decision-making.

Provides a clear SWOT matrix tailored to GS Retail for rapid identification of competitive gaps and growth levers, enabling fast alignment across teams and quicker decision-making.

Weaknesses

Thin retail margins

Convenience and grocery formats yield structurally low net margins—typically around 1–3% in the convenience channel—making GS Retail highly sensitive to cost inflation and small price changes that can sharply compress profits. Heavy promotional activity entrenches price-sensitive shoppers, while high fixed costs and operating leverage exacerbate earnings declines in downturns.

Domestic market concentration

Revenue remains overwhelmingly tied to South Korea—over 90% of sales and roughly 13,000 convenience and retail outlets operate domestically—so GS Retail is exposed to Korean GDP swings, policy changes and competition. Limited geographic diversification amplifies local market risk, while demographic shifts (South Korea’s 65+ cohort rising toward ~20% by 2025) and urban saturation constrain organic growth and limit currency-diversification benefits.

Operational complexity

Running over 13,000 convenience stores alongside supermarkets, online channels and hospitality businesses increases management complexity and overhead for GS Retail. Integrating systems and processes across these formats has proven challenging, leading to slower decision-making and reduced innovation speed in 2023–24 transformation efforts. That complexity raises execution risk during restructurings and technology rollouts, increasing operational costs and implementation timelines.

Franchisee dependence

- ~15,000+ stores (GS25)

- Over 90% franchised

- Inconsistent execution hurts NPS

- Fee disputes drive churn; support costs climb

Digital capability gap risk

Competing with tech-led players forces GS Retail to sustain heavy IT and data investments; South Korea's online retail penetration was about 33% in 2024, raising stakes for UX and agility. Legacy systems can slow personalization and fulfillment speed, risking share loss to pure-play e-commerce if digital UX lags. Hiring data engineers and ML talent is competitive and costly.

- Investment pressure: sustained IT spend

- Operational drag: legacy systems reduce speed

- Market risk: ~33% online retail penetration (2024)

- Talent gap: competitive data/engineering hiring

Tight margins, franchise concentration and rising tech costs squeeze convenience retail

Low net margins (~1–3% in convenience) make profits highly sensitive to cost inflation and promotions.

Over 90% of revenue is domestic; GS25 ~15,000 stores with >90% franchised increases execution and churn risk.

Legacy IT and rising digital spend vs ~33% online retail penetration (2024) raise tech/talent costs and competitive pressure.

| Metric | Value |

|---|---|

| Net margin (convenience) | 1–3% |

| Store count (GS25) | ~15,000 |

| Franchised | >90% |

| Domestic revenue | >90% |

| Online penetration (2024) | ~33% |

| Population 65+ (2025) | ~20% |

Preview the Actual Deliverable

GS Retail SWOT Analysis

This is the actual SWOT analysis document for GS Retail you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, actionable insights. Purchase unlocks the complete, editable file for immediate download and use.

Elevate Your Analysis with the Complete SWOT Report

GS Retail's SWOT reveals strong market reach and omnichannel capability, counterbalanced by margin pressures and intense competition. Our full analysis dissects financial implications, strategic risks, and growth levers to inform investors and managers. Purchase the complete, editable SWOT (Word + Excel) for ready-to-use strategic insights.

Strengths

Nationwide GS25 footprint

GS Retail operates one of Korea’s largest convenience networks with over 14,000 GS25 stores nationwide as of 2024, driving high daily traffic and purchase frequency. Dense urban and transit placements create habitual purchases and sustained brand visibility, supporting same-store sales resilience. Scale delivers strong negotiating leverage with suppliers and logistics partners, and the resulting network effects raise barriers to entry for smaller rivals.

Strong brand and loyalty

GS25 and GS THE FRESH enjoy high recognition—GS Retail operates over 14,000 GS25 stores nationwide—with active loyalty programs and co-branded promotions driving engagement. Earn-and-burn mechanics boost basket size and repeat visits, while partnerships with KakaoPay and Naver Pay deepen payment engagement and data capture. Strong brand equity enables premium pricing on select categories, supporting higher category margins.

Omnichannel and delivery

Integrated online platforms extend convenience beyond stores via on-demand delivery and pickup, leveraging GS Retail's network of over 14,000 GS25 stores to act as fulfillment nodes. Last-mile partnerships shorten lead times and improve inventory turns through localized replenishment. Omnichannel reduces friction and broadens catchment areas, and supports targeted promotions based on real-time demand signals from POS and app data.

Private label and sourcing scale

GS Retail leverages scale—over 13,000 stores (2024)—to secure competitive procurement and create differentiated private-label assortments that lift margins and reduce direct price comparisons. Data-driven micro-location assortment optimizes SKU productivity, while deep supplier ties accelerate innovation cycles and shortened time-to-shelf.

- Scale: 13,000+ stores (2024)

- Margin uplift: private brands drive exclusivity

- Assortment: micro-location SKU optimization

- Speed: faster innovation via supplier partnerships

Diversified retail portfolio

GS Retail’s diversified mix across convenience, supermarkets, online and hotels spreads revenue risk; its GS25 network exceeds 16,000 stores (2024), enabling scale in procurement, logistics and marketing. Hospitality assets provide upsell and brand-extension channels that help smooth seasonal volatility and market shocks.

- Scale: GS25 >16,000 stores (2024)

- Synergies: procurement, logistics, marketing

- Upsell: hotels → brand extensions

- Risk: smoother seasonality

14,000+ stores, dense urban reach, strong payment partners and omnichannel fulfillment

GS Retail commands scale with over 14,000 GS25 stores (2024), driving high foot traffic, frequent purchases and strong supplier leverage. Recognized brands, loyalty programs and partnerships with KakaoPay and Naver Pay boost repeat sales and payment/data capture. Dense urban store network enables rapid last‑mile delivery and omnichannel fulfillment, supporting premium pricing on select categories and private‑label margin uplift.

| Metric | Value (2024) |

|---|---|

| GS25 stores | 14,000+ nationwide |

| Payment partners | KakaoPay, Naver Pay |

| Omnichannel | Delivery & pickup via GS25 network |

| Competitive edge | Procurement & supplier leverage |

What is included in the product

Provides a concise strategic overview of GS Retail’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decision-making.

Provides a clear SWOT matrix tailored to GS Retail for rapid identification of competitive gaps and growth levers, enabling fast alignment across teams and quicker decision-making.

Weaknesses

Thin retail margins

Convenience and grocery formats yield structurally low net margins—typically around 1–3% in the convenience channel—making GS Retail highly sensitive to cost inflation and small price changes that can sharply compress profits. Heavy promotional activity entrenches price-sensitive shoppers, while high fixed costs and operating leverage exacerbate earnings declines in downturns.

Domestic market concentration

Revenue remains overwhelmingly tied to South Korea—over 90% of sales and roughly 13,000 convenience and retail outlets operate domestically—so GS Retail is exposed to Korean GDP swings, policy changes and competition. Limited geographic diversification amplifies local market risk, while demographic shifts (South Korea’s 65+ cohort rising toward ~20% by 2025) and urban saturation constrain organic growth and limit currency-diversification benefits.

Operational complexity

Running over 13,000 convenience stores alongside supermarkets, online channels and hospitality businesses increases management complexity and overhead for GS Retail. Integrating systems and processes across these formats has proven challenging, leading to slower decision-making and reduced innovation speed in 2023–24 transformation efforts. That complexity raises execution risk during restructurings and technology rollouts, increasing operational costs and implementation timelines.

Franchisee dependence

- ~15,000+ stores (GS25)

- Over 90% franchised

- Inconsistent execution hurts NPS

- Fee disputes drive churn; support costs climb

Digital capability gap risk

Competing with tech-led players forces GS Retail to sustain heavy IT and data investments; South Korea's online retail penetration was about 33% in 2024, raising stakes for UX and agility. Legacy systems can slow personalization and fulfillment speed, risking share loss to pure-play e-commerce if digital UX lags. Hiring data engineers and ML talent is competitive and costly.

- Investment pressure: sustained IT spend

- Operational drag: legacy systems reduce speed

- Market risk: ~33% online retail penetration (2024)

- Talent gap: competitive data/engineering hiring

Tight margins, franchise concentration and rising tech costs squeeze convenience retail

Low net margins (~1–3% in convenience) make profits highly sensitive to cost inflation and promotions.

Over 90% of revenue is domestic; GS25 ~15,000 stores with >90% franchised increases execution and churn risk.

Legacy IT and rising digital spend vs ~33% online retail penetration (2024) raise tech/talent costs and competitive pressure.

| Metric | Value |

|---|---|

| Net margin (convenience) | 1–3% |

| Store count (GS25) | ~15,000 |

| Franchised | >90% |

| Domestic revenue | >90% |

| Online penetration (2024) | ~33% |

| Population 65+ (2025) | ~20% |

Preview the Actual Deliverable

GS Retail SWOT Analysis

This is the actual SWOT analysis document for GS Retail you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, actionable insights. Purchase unlocks the complete, editable file for immediate download and use.

Description

Elevate Your Analysis with the Complete SWOT Report

GS Retail's SWOT reveals strong market reach and omnichannel capability, counterbalanced by margin pressures and intense competition. Our full analysis dissects financial implications, strategic risks, and growth levers to inform investors and managers. Purchase the complete, editable SWOT (Word + Excel) for ready-to-use strategic insights.

Strengths

Nationwide GS25 footprint

GS Retail operates one of Korea’s largest convenience networks with over 14,000 GS25 stores nationwide as of 2024, driving high daily traffic and purchase frequency. Dense urban and transit placements create habitual purchases and sustained brand visibility, supporting same-store sales resilience. Scale delivers strong negotiating leverage with suppliers and logistics partners, and the resulting network effects raise barriers to entry for smaller rivals.

Strong brand and loyalty

GS25 and GS THE FRESH enjoy high recognition—GS Retail operates over 14,000 GS25 stores nationwide—with active loyalty programs and co-branded promotions driving engagement. Earn-and-burn mechanics boost basket size and repeat visits, while partnerships with KakaoPay and Naver Pay deepen payment engagement and data capture. Strong brand equity enables premium pricing on select categories, supporting higher category margins.

Omnichannel and delivery

Integrated online platforms extend convenience beyond stores via on-demand delivery and pickup, leveraging GS Retail's network of over 14,000 GS25 stores to act as fulfillment nodes. Last-mile partnerships shorten lead times and improve inventory turns through localized replenishment. Omnichannel reduces friction and broadens catchment areas, and supports targeted promotions based on real-time demand signals from POS and app data.

Private label and sourcing scale

GS Retail leverages scale—over 13,000 stores (2024)—to secure competitive procurement and create differentiated private-label assortments that lift margins and reduce direct price comparisons. Data-driven micro-location assortment optimizes SKU productivity, while deep supplier ties accelerate innovation cycles and shortened time-to-shelf.

- Scale: 13,000+ stores (2024)

- Margin uplift: private brands drive exclusivity

- Assortment: micro-location SKU optimization

- Speed: faster innovation via supplier partnerships

Diversified retail portfolio

GS Retail’s diversified mix across convenience, supermarkets, online and hotels spreads revenue risk; its GS25 network exceeds 16,000 stores (2024), enabling scale in procurement, logistics and marketing. Hospitality assets provide upsell and brand-extension channels that help smooth seasonal volatility and market shocks.

- Scale: GS25 >16,000 stores (2024)

- Synergies: procurement, logistics, marketing

- Upsell: hotels → brand extensions

- Risk: smoother seasonality

14,000+ stores, dense urban reach, strong payment partners and omnichannel fulfillment

GS Retail commands scale with over 14,000 GS25 stores (2024), driving high foot traffic, frequent purchases and strong supplier leverage. Recognized brands, loyalty programs and partnerships with KakaoPay and Naver Pay boost repeat sales and payment/data capture. Dense urban store network enables rapid last‑mile delivery and omnichannel fulfillment, supporting premium pricing on select categories and private‑label margin uplift.

| Metric | Value (2024) |

|---|---|

| GS25 stores | 14,000+ nationwide |

| Payment partners | KakaoPay, Naver Pay |

| Omnichannel | Delivery & pickup via GS25 network |

| Competitive edge | Procurement & supplier leverage |

What is included in the product

Provides a concise strategic overview of GS Retail’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decision-making.

Provides a clear SWOT matrix tailored to GS Retail for rapid identification of competitive gaps and growth levers, enabling fast alignment across teams and quicker decision-making.

Weaknesses

Thin retail margins

Convenience and grocery formats yield structurally low net margins—typically around 1–3% in the convenience channel—making GS Retail highly sensitive to cost inflation and small price changes that can sharply compress profits. Heavy promotional activity entrenches price-sensitive shoppers, while high fixed costs and operating leverage exacerbate earnings declines in downturns.

Domestic market concentration

Revenue remains overwhelmingly tied to South Korea—over 90% of sales and roughly 13,000 convenience and retail outlets operate domestically—so GS Retail is exposed to Korean GDP swings, policy changes and competition. Limited geographic diversification amplifies local market risk, while demographic shifts (South Korea’s 65+ cohort rising toward ~20% by 2025) and urban saturation constrain organic growth and limit currency-diversification benefits.

Operational complexity

Running over 13,000 convenience stores alongside supermarkets, online channels and hospitality businesses increases management complexity and overhead for GS Retail. Integrating systems and processes across these formats has proven challenging, leading to slower decision-making and reduced innovation speed in 2023–24 transformation efforts. That complexity raises execution risk during restructurings and technology rollouts, increasing operational costs and implementation timelines.

Franchisee dependence

- ~15,000+ stores (GS25)

- Over 90% franchised

- Inconsistent execution hurts NPS

- Fee disputes drive churn; support costs climb

Digital capability gap risk

Competing with tech-led players forces GS Retail to sustain heavy IT and data investments; South Korea's online retail penetration was about 33% in 2024, raising stakes for UX and agility. Legacy systems can slow personalization and fulfillment speed, risking share loss to pure-play e-commerce if digital UX lags. Hiring data engineers and ML talent is competitive and costly.

- Investment pressure: sustained IT spend

- Operational drag: legacy systems reduce speed

- Market risk: ~33% online retail penetration (2024)

- Talent gap: competitive data/engineering hiring

Tight margins, franchise concentration and rising tech costs squeeze convenience retail

Low net margins (~1–3% in convenience) make profits highly sensitive to cost inflation and promotions.

Over 90% of revenue is domestic; GS25 ~15,000 stores with >90% franchised increases execution and churn risk.

Legacy IT and rising digital spend vs ~33% online retail penetration (2024) raise tech/talent costs and competitive pressure.

| Metric | Value |

|---|---|

| Net margin (convenience) | 1–3% |

| Store count (GS25) | ~15,000 |

| Franchised | >90% |

| Domestic revenue | >90% |

| Online penetration (2024) | ~33% |

| Population 65+ (2025) | ~20% |

Preview the Actual Deliverable

GS Retail SWOT Analysis

This is the actual SWOT analysis document for GS Retail you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, actionable insights. Purchase unlocks the complete, editable file for immediate download and use.