Gala Television Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

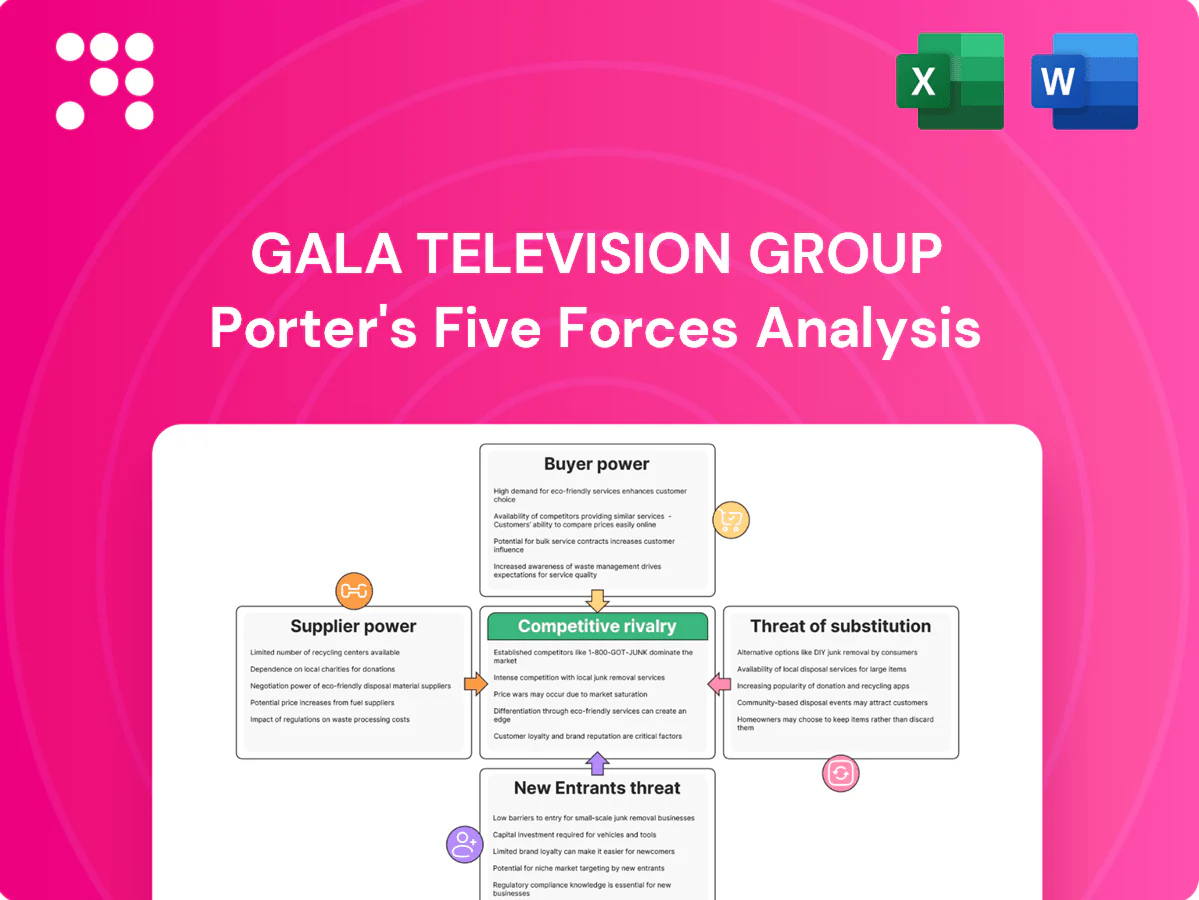

Gala Television Group faces intense rivalry from streaming platforms and regional broadcasters, while content suppliers and production costs exert moderate supplier power; subscriber bargaining is growing as alternatives multiply, and new entrants find barriers in content licensing but can exploit digital distribution. This snapshot highlights key competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategy.

Suppliers Bargaining Power

Star talent and creators command premiums

High-profile actors, showrunners, and variety hosts command premiums because they directly drive ratings and ad RPMs; in 2024 top-tier talent deals have been linked to viewership lifts of 20–40% on comparable formats. Scarcity in genres like idol dramas and variety amplifies this leverage, making talent a concentrated supplier market. Long-term exclusivity can cap bidding but raises fixed costs by an estimated 15–25%, so GTV must balance marquee signings with scalable in-house talent development.

Content rights holders control popular IP

Studios and overseas distributors control must-have formats and series rights, and in 2024 platform exclusivity and windowing tightened availability, pushing licence premiums higher. Currency swings and geo-licensing terms introduced further cost volatility for cross-border buys. GTV's mix of commissioned and acquired shows diversifies exposure and limits supplier concentration risk.

Production houses and post facilities

Capacity constraints during peak seasons drive up rates and create scheduling risk for Gala, concentrating supplier leverage over production timelines and budgets.

Specialized post services such as VFX, subtitling and 4K/HDR narrow vendor choices, increasing switching costs and supplier bargaining power.

Bundled service contracts can lower unit costs but lock Gala into providers and reduce flexibility; building in-house capabilities offers a gradual shift in bargaining power back to the firm.

Distribution tech and playout vendors

Music, format, and sports licensing

Music cues, formats and sports rights often come on take‑it‑or‑leave‑it terms, and renewals can spike if ratings climb; major US league deals run to multiple billions annually, driving seller leverage. Competing OTT bidders (Netflix, Amazon, Disney+) intensify auctions. Early pipeline planning and co‑productions help moderate fee spikes.

- Take‑it‑or‑leave‑it terms

- Renewal price risk with strong ratings

- OTT bidders intensify auctions

- Pipeline planning/co‑productions mitigate spikes

Supplier power: talent lifts 20–40%; CDN ~$26B

Supplier power is high: top talent drives 20–40% ratings lifts and exclusivity raises fixed costs 15–25% in 2024, concentrating leverage. CDN/infra remains concentrated (global CDN market ~26 billion USD in 2024), raising switching costs and escalators. Rights for sports/music sell on take‑it‑or‑leave‑it terms and spike with ratings; co‑productions and in‑house build mitigate exposure.

| Supplier | 2024 metric |

|---|---|

| Top talent | 20–40% viewership lift; +15–25% fixed cost |

| CDN/infra | $26B market; high switching cost |

What is included in the product

Concise Porter's Five Forces analysis revealing key competitive drivers, buyer/supplier leverage, threat of substitutes, and entry barriers specific to Gala Television Group. It identifies emerging disruptors and strategic levers the company can use to protect market share and optimize pricing and profitability.

A one-sheet Porter's Five Forces for Gala Television Group that instantly visualizes competitive pressures with a radar chart, is fully customizable for scenario or post-regulation comparisons, requires no macros, and is ready to copy into pitch decks or integrate into broader dashboards for fast strategic decisions.

Customers Bargaining Power

Cable MSOs and platform aggregators

Cable MSOs and platform aggregators in Taiwan hold strong leverage over Gala Television by controlling carriage, pricing tiers and EPG placement, enabling negotiations for lower affiliate fees or mandatory bundling that compress channel margins. Threat of blackouts can shift audiences and ad spend rapidly, pressuring retransmission revenue and CPMs. Growing multi-platform distribution and regulatory must-carry/content quotas, however, reduce single-channel dependence and mitigate MSO bargaining power.

Advertisers and media agencies

Large advertisers and media agencies leverage scale to negotiate CPMs and network-wide integrations, pressuring rates as digital accounted for about 66% of global ad spend in 2024. Cross-platform measurement adoption forces hard ROI demands and performance clauses. Shift of budgets to programmatic and social increases discount pressure. Gala can protect yield via branded content and sponsorship packages commanding premium CPMs.

End viewers with abundant choice

End viewers can switch channels or apps instantly, and with global SVOD subscriptions topping 1 billion in 2024 (Statista), low switching costs force constant fresh content. Ratings sensitivity yields rapid ad and subscription revenue swings after viewership shifts. Personalization features and marquee event programming remain critical levers to retain audiences and stabilize monetization.

OTT platforms as wholesale buyers

OTT platforms buying catch-up and simulcast rights demand exclusivity and revenue shares, leveraging their first-party data; global SVOD subscriptions reached about 1.1 billion in 2023, strengthening streamers' negotiating position into 2024.

Windowing conflicts between OTT and linear have eroded linear CPMs, while hybrid AVOD/SVOD deals in 2024 broaden monetization and help protect linear schedules.

- Negotiation leverage: exclusivity + data

- Impact: windowing cuts linear value

- 2023 stat: ~1.1B SVOD subs

- Strategy: AVOD/SVOD hybrid preserves linear

Government and regulators influencing carriage

Regulatory guidelines shape channel lineups and content standards, with 2024 local-content quotas (commonly around 30% in several markets) and advertising limits directly constraining carriage options. Compliance costs and mandated content edits reduce scheduling flexibility and can raise operating costs, often shifting 1–3% of broadcaster budgets to regulatory compliance. Policy shifts (licensing, must-offer rules) can quickly change bargaining leverage vis-à-vis MSOs. Proactive compliance and investing in local content maintain regulator goodwill and protect carriage negotiating positions.

- Regulatory quotas: ~30% local/European content in many markets (2024)

- Compliance burden: reallocates ~1–3% of budgets

- Policy risk: alters MSO bargaining power

- Mitigation: proactive compliance + local-content investment

MSO carriage and bundling squeeze CPMs as digital hits 66%

Cable MSOs and aggregators exert high leverage over Gala via carriage, EPG placement and bundling, risking fee cuts and blackouts that depress CPMs. Large advertisers/agencies and digital channels (digital ~66% global ad spend in 2024) push performance pricing; SVOD scale (≈1.1B subs) strengthens OTT negotiating power. Regulatory local-content quotas (~30%) and compliance (≈1–3% budgets) moderate bargaining dynamics.

| Factor | 2024 metric | Impact |

|---|---|---|

| Digital ad share | 66% | CPM pressure |

| SVOD subs | ~1.1B | OTT leverage |

| Local-content quota | ~30% | Scheduling constraints |

| Compliance cost | 1–3% budgets | Reduced flexibility |

Full Version Awaits

Gala Television Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Gala Television Group you’ll receive after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for immediate download and use. What you see here is precisely the deliverable available to you upon payment.

From Overview to Strategy Blueprint

Gala Television Group faces intense rivalry from streaming platforms and regional broadcasters, while content suppliers and production costs exert moderate supplier power; subscriber bargaining is growing as alternatives multiply, and new entrants find barriers in content licensing but can exploit digital distribution. This snapshot highlights key competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategy.

Suppliers Bargaining Power

Star talent and creators command premiums

High-profile actors, showrunners, and variety hosts command premiums because they directly drive ratings and ad RPMs; in 2024 top-tier talent deals have been linked to viewership lifts of 20–40% on comparable formats. Scarcity in genres like idol dramas and variety amplifies this leverage, making talent a concentrated supplier market. Long-term exclusivity can cap bidding but raises fixed costs by an estimated 15–25%, so GTV must balance marquee signings with scalable in-house talent development.

Content rights holders control popular IP

Studios and overseas distributors control must-have formats and series rights, and in 2024 platform exclusivity and windowing tightened availability, pushing licence premiums higher. Currency swings and geo-licensing terms introduced further cost volatility for cross-border buys. GTV's mix of commissioned and acquired shows diversifies exposure and limits supplier concentration risk.

Production houses and post facilities

Capacity constraints during peak seasons drive up rates and create scheduling risk for Gala, concentrating supplier leverage over production timelines and budgets.

Specialized post services such as VFX, subtitling and 4K/HDR narrow vendor choices, increasing switching costs and supplier bargaining power.

Bundled service contracts can lower unit costs but lock Gala into providers and reduce flexibility; building in-house capabilities offers a gradual shift in bargaining power back to the firm.

Distribution tech and playout vendors

Music, format, and sports licensing

Music cues, formats and sports rights often come on take‑it‑or‑leave‑it terms, and renewals can spike if ratings climb; major US league deals run to multiple billions annually, driving seller leverage. Competing OTT bidders (Netflix, Amazon, Disney+) intensify auctions. Early pipeline planning and co‑productions help moderate fee spikes.

- Take‑it‑or‑leave‑it terms

- Renewal price risk with strong ratings

- OTT bidders intensify auctions

- Pipeline planning/co‑productions mitigate spikes

Supplier power: talent lifts 20–40%; CDN ~$26B

Supplier power is high: top talent drives 20–40% ratings lifts and exclusivity raises fixed costs 15–25% in 2024, concentrating leverage. CDN/infra remains concentrated (global CDN market ~26 billion USD in 2024), raising switching costs and escalators. Rights for sports/music sell on take‑it‑or‑leave‑it terms and spike with ratings; co‑productions and in‑house build mitigate exposure.

| Supplier | 2024 metric |

|---|---|

| Top talent | 20–40% viewership lift; +15–25% fixed cost |

| CDN/infra | $26B market; high switching cost |

What is included in the product

Concise Porter's Five Forces analysis revealing key competitive drivers, buyer/supplier leverage, threat of substitutes, and entry barriers specific to Gala Television Group. It identifies emerging disruptors and strategic levers the company can use to protect market share and optimize pricing and profitability.

A one-sheet Porter's Five Forces for Gala Television Group that instantly visualizes competitive pressures with a radar chart, is fully customizable for scenario or post-regulation comparisons, requires no macros, and is ready to copy into pitch decks or integrate into broader dashboards for fast strategic decisions.

Customers Bargaining Power

Cable MSOs and platform aggregators

Cable MSOs and platform aggregators in Taiwan hold strong leverage over Gala Television by controlling carriage, pricing tiers and EPG placement, enabling negotiations for lower affiliate fees or mandatory bundling that compress channel margins. Threat of blackouts can shift audiences and ad spend rapidly, pressuring retransmission revenue and CPMs. Growing multi-platform distribution and regulatory must-carry/content quotas, however, reduce single-channel dependence and mitigate MSO bargaining power.

Advertisers and media agencies

Large advertisers and media agencies leverage scale to negotiate CPMs and network-wide integrations, pressuring rates as digital accounted for about 66% of global ad spend in 2024. Cross-platform measurement adoption forces hard ROI demands and performance clauses. Shift of budgets to programmatic and social increases discount pressure. Gala can protect yield via branded content and sponsorship packages commanding premium CPMs.

End viewers with abundant choice

End viewers can switch channels or apps instantly, and with global SVOD subscriptions topping 1 billion in 2024 (Statista), low switching costs force constant fresh content. Ratings sensitivity yields rapid ad and subscription revenue swings after viewership shifts. Personalization features and marquee event programming remain critical levers to retain audiences and stabilize monetization.

OTT platforms as wholesale buyers

OTT platforms buying catch-up and simulcast rights demand exclusivity and revenue shares, leveraging their first-party data; global SVOD subscriptions reached about 1.1 billion in 2023, strengthening streamers' negotiating position into 2024.

Windowing conflicts between OTT and linear have eroded linear CPMs, while hybrid AVOD/SVOD deals in 2024 broaden monetization and help protect linear schedules.

- Negotiation leverage: exclusivity + data

- Impact: windowing cuts linear value

- 2023 stat: ~1.1B SVOD subs

- Strategy: AVOD/SVOD hybrid preserves linear

Government and regulators influencing carriage

Regulatory guidelines shape channel lineups and content standards, with 2024 local-content quotas (commonly around 30% in several markets) and advertising limits directly constraining carriage options. Compliance costs and mandated content edits reduce scheduling flexibility and can raise operating costs, often shifting 1–3% of broadcaster budgets to regulatory compliance. Policy shifts (licensing, must-offer rules) can quickly change bargaining leverage vis-à-vis MSOs. Proactive compliance and investing in local content maintain regulator goodwill and protect carriage negotiating positions.

- Regulatory quotas: ~30% local/European content in many markets (2024)

- Compliance burden: reallocates ~1–3% of budgets

- Policy risk: alters MSO bargaining power

- Mitigation: proactive compliance + local-content investment

MSO carriage and bundling squeeze CPMs as digital hits 66%

Cable MSOs and aggregators exert high leverage over Gala via carriage, EPG placement and bundling, risking fee cuts and blackouts that depress CPMs. Large advertisers/agencies and digital channels (digital ~66% global ad spend in 2024) push performance pricing; SVOD scale (≈1.1B subs) strengthens OTT negotiating power. Regulatory local-content quotas (~30%) and compliance (≈1–3% budgets) moderate bargaining dynamics.

| Factor | 2024 metric | Impact |

|---|---|---|

| Digital ad share | 66% | CPM pressure |

| SVOD subs | ~1.1B | OTT leverage |

| Local-content quota | ~30% | Scheduling constraints |

| Compliance cost | 1–3% budgets | Reduced flexibility |

Full Version Awaits

Gala Television Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Gala Television Group you’ll receive after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for immediate download and use. What you see here is precisely the deliverable available to you upon payment.

Description

From Overview to Strategy Blueprint

Gala Television Group faces intense rivalry from streaming platforms and regional broadcasters, while content suppliers and production costs exert moderate supplier power; subscriber bargaining is growing as alternatives multiply, and new entrants find barriers in content licensing but can exploit digital distribution. This snapshot highlights key competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategy.

Suppliers Bargaining Power

Star talent and creators command premiums

High-profile actors, showrunners, and variety hosts command premiums because they directly drive ratings and ad RPMs; in 2024 top-tier talent deals have been linked to viewership lifts of 20–40% on comparable formats. Scarcity in genres like idol dramas and variety amplifies this leverage, making talent a concentrated supplier market. Long-term exclusivity can cap bidding but raises fixed costs by an estimated 15–25%, so GTV must balance marquee signings with scalable in-house talent development.

Content rights holders control popular IP

Studios and overseas distributors control must-have formats and series rights, and in 2024 platform exclusivity and windowing tightened availability, pushing licence premiums higher. Currency swings and geo-licensing terms introduced further cost volatility for cross-border buys. GTV's mix of commissioned and acquired shows diversifies exposure and limits supplier concentration risk.

Production houses and post facilities

Capacity constraints during peak seasons drive up rates and create scheduling risk for Gala, concentrating supplier leverage over production timelines and budgets.

Specialized post services such as VFX, subtitling and 4K/HDR narrow vendor choices, increasing switching costs and supplier bargaining power.

Bundled service contracts can lower unit costs but lock Gala into providers and reduce flexibility; building in-house capabilities offers a gradual shift in bargaining power back to the firm.

Distribution tech and playout vendors

Music, format, and sports licensing

Music cues, formats and sports rights often come on take‑it‑or‑leave‑it terms, and renewals can spike if ratings climb; major US league deals run to multiple billions annually, driving seller leverage. Competing OTT bidders (Netflix, Amazon, Disney+) intensify auctions. Early pipeline planning and co‑productions help moderate fee spikes.

- Take‑it‑or‑leave‑it terms

- Renewal price risk with strong ratings

- OTT bidders intensify auctions

- Pipeline planning/co‑productions mitigate spikes

Supplier power: talent lifts 20–40%; CDN ~$26B

Supplier power is high: top talent drives 20–40% ratings lifts and exclusivity raises fixed costs 15–25% in 2024, concentrating leverage. CDN/infra remains concentrated (global CDN market ~26 billion USD in 2024), raising switching costs and escalators. Rights for sports/music sell on take‑it‑or‑leave‑it terms and spike with ratings; co‑productions and in‑house build mitigate exposure.

| Supplier | 2024 metric |

|---|---|

| Top talent | 20–40% viewership lift; +15–25% fixed cost |

| CDN/infra | $26B market; high switching cost |

What is included in the product

Concise Porter's Five Forces analysis revealing key competitive drivers, buyer/supplier leverage, threat of substitutes, and entry barriers specific to Gala Television Group. It identifies emerging disruptors and strategic levers the company can use to protect market share and optimize pricing and profitability.

A one-sheet Porter's Five Forces for Gala Television Group that instantly visualizes competitive pressures with a radar chart, is fully customizable for scenario or post-regulation comparisons, requires no macros, and is ready to copy into pitch decks or integrate into broader dashboards for fast strategic decisions.

Customers Bargaining Power

Cable MSOs and platform aggregators

Cable MSOs and platform aggregators in Taiwan hold strong leverage over Gala Television by controlling carriage, pricing tiers and EPG placement, enabling negotiations for lower affiliate fees or mandatory bundling that compress channel margins. Threat of blackouts can shift audiences and ad spend rapidly, pressuring retransmission revenue and CPMs. Growing multi-platform distribution and regulatory must-carry/content quotas, however, reduce single-channel dependence and mitigate MSO bargaining power.

Advertisers and media agencies

Large advertisers and media agencies leverage scale to negotiate CPMs and network-wide integrations, pressuring rates as digital accounted for about 66% of global ad spend in 2024. Cross-platform measurement adoption forces hard ROI demands and performance clauses. Shift of budgets to programmatic and social increases discount pressure. Gala can protect yield via branded content and sponsorship packages commanding premium CPMs.

End viewers with abundant choice

End viewers can switch channels or apps instantly, and with global SVOD subscriptions topping 1 billion in 2024 (Statista), low switching costs force constant fresh content. Ratings sensitivity yields rapid ad and subscription revenue swings after viewership shifts. Personalization features and marquee event programming remain critical levers to retain audiences and stabilize monetization.

OTT platforms as wholesale buyers

OTT platforms buying catch-up and simulcast rights demand exclusivity and revenue shares, leveraging their first-party data; global SVOD subscriptions reached about 1.1 billion in 2023, strengthening streamers' negotiating position into 2024.

Windowing conflicts between OTT and linear have eroded linear CPMs, while hybrid AVOD/SVOD deals in 2024 broaden monetization and help protect linear schedules.

- Negotiation leverage: exclusivity + data

- Impact: windowing cuts linear value

- 2023 stat: ~1.1B SVOD subs

- Strategy: AVOD/SVOD hybrid preserves linear

Government and regulators influencing carriage

Regulatory guidelines shape channel lineups and content standards, with 2024 local-content quotas (commonly around 30% in several markets) and advertising limits directly constraining carriage options. Compliance costs and mandated content edits reduce scheduling flexibility and can raise operating costs, often shifting 1–3% of broadcaster budgets to regulatory compliance. Policy shifts (licensing, must-offer rules) can quickly change bargaining leverage vis-à-vis MSOs. Proactive compliance and investing in local content maintain regulator goodwill and protect carriage negotiating positions.

- Regulatory quotas: ~30% local/European content in many markets (2024)

- Compliance burden: reallocates ~1–3% of budgets

- Policy risk: alters MSO bargaining power

- Mitigation: proactive compliance + local-content investment

MSO carriage and bundling squeeze CPMs as digital hits 66%

Cable MSOs and aggregators exert high leverage over Gala via carriage, EPG placement and bundling, risking fee cuts and blackouts that depress CPMs. Large advertisers/agencies and digital channels (digital ~66% global ad spend in 2024) push performance pricing; SVOD scale (≈1.1B subs) strengthens OTT negotiating power. Regulatory local-content quotas (~30%) and compliance (≈1–3% budgets) moderate bargaining dynamics.

| Factor | 2024 metric | Impact |

|---|---|---|

| Digital ad share | 66% | CPM pressure |

| SVOD subs | ~1.1B | OTT leverage |

| Local-content quota | ~30% | Scheduling constraints |

| Compliance cost | 1–3% budgets | Reduced flexibility |

Full Version Awaits

Gala Television Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Gala Television Group you’ll receive after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for immediate download and use. What you see here is precisely the deliverable available to you upon payment.