Guardian Capital Porter's Five Forces Analysis

Don't Miss the Bigger Picture

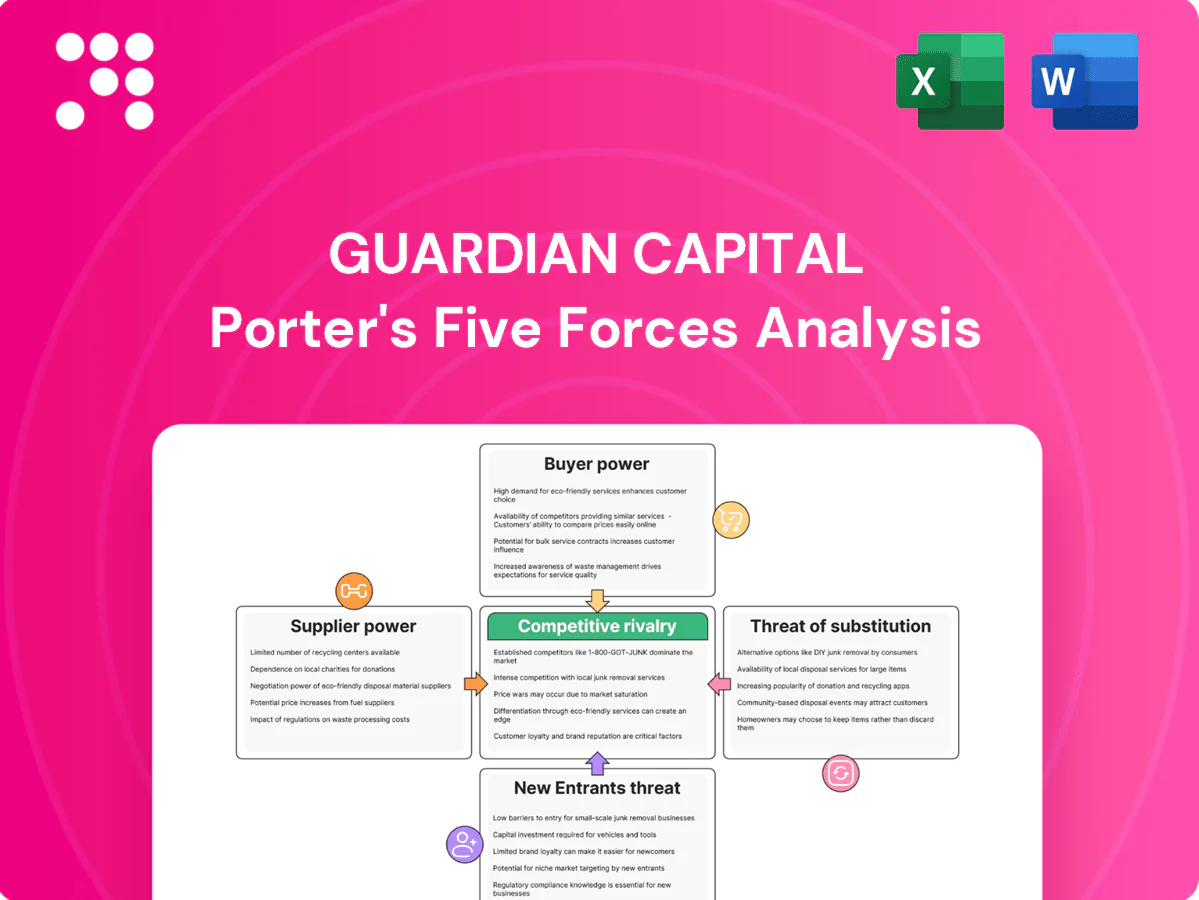

Guardian Capital’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, substitute threats, and barriers to entry, revealing where strategic pressure points lie. This concise overview signals key risks and opportunities across the firm’s market position. Ready to move beyond the basics? Get the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Talent scarcity

In 2024 Guardian faces acute scarcity of experienced portfolio managers, quants and advisors who are highly mobile and drive up wages and retention costs. Star hires increasingly secure revenue-sharing or bespoke bonus deals, shifting leverage toward talent. Weakening non-compete enforcement in some US states in 2024 further raises mobility risk. Guardian counters with culture, equity incentives and structured training pipelines.

Data and indices

Dependence on benchmark licensors such as MSCI and S&P and market data vendors raises switching costs and pricing exposure, especially as passive vehicles now reference over $12 trillion of global ETF AUM in 2024. Price hikes or licensing changes can compress margins or force product redesigns, limiting go-to-market agility. Multi-vendor strategies reduce single-vendor risk but add integration complexity and operational overhead, while proprietary research and factor models can partially offset reliance.

Custody and brokerage

Custodians, prime brokers and execution venues form critical infrastructure with few top-tier providers; global assets under custody exceeded $100 trillion in 2024, concentrating market power. Volume-based pricing and best-execution rules cap price leverage, but service-quality gaps drive switching costs and impact performance. Ongoing consolidation among custodians can raise fees or force bundled services, so Guardian uses strategic partnerships and regular RFPs to preserve competitive terms.

Technology platforms

Reliance on OMS/EMS, risk and client-reporting systems ties Guardian Capital to vendors with high changeover costs; integrations and data reconciliation often generate six-figure migration expenses and months of downtime risk. Cloud services and APIs improved portability—public cloud grew about 20% in 2024—but do not eliminate switching friction. Vendor outages remain material operational and reputational risks. Co-development and modular architectures can rebalance vendor leverage.

- High switching cost: six-figure integrations

- Cloud growth 2024: ~20%

- Outages = operational + reputational risk

- Mitigation: co-development, modular APIs

Distribution partners

Third-party platforms, consultants and intermediaries remain gatekeepers to client access in 2024, with preferred lists and due-diligence gates often forcing fee concessions or marketing support; platform concentration increases listing and shelf-space costs, while expanding direct channels and brand recognition reduces dependency.

- Gatekeepers: platforms/consultants

- Concessions: fees & marketing

- Cost: concentrated platforms

- Mitigation: direct channels & branding

Tight talent, custodial concentration squeeze margins; ETFs $12T, AUC >$100T

Supplier power is high: talent scarcity drove revenue-share deals and raises in 2024, forcing higher retention spend. Licensing and data vendors risk margin pressure as passive vehicles reference ~$12 trillion ETF AUM in 2024. Custodial concentration (global AUC >$100 trillion in 2024) and OMS/EMS migration costs create switching barriers. Guardian mitigates via equity, co-development, multi-vendor and direct channels.

| Metric | 2024 |

|---|---|

| ETF AUM referenced | $12 trillion |

| Global assets under custody | $100 trillion+ |

| Public cloud growth | ~20% |

| Typical migration cost | Six-figure |

What is included in the product

Tailored Porter's Five Forces analysis for Guardian Capital that uncovers key competitive drivers, buyer/supplier power, barriers to entry, substitution threats, and emerging disruptors—with strategic commentary to inform pricing, profitability, and defensive positioning.

A clear, one-sheet Guardian Capital Porter's Five Forces summary—instantly visualize competitive pressure with a spider chart and swap in your own data for quick, board-ready insights.

Customers Bargaining Power

Institutional leverage

Pensions, endowments and insurers run competitive RFPs and mandate sizable allocations, enabling strong fee negotiations; institutional investors held over 60% of global AUM in 2024, magnifying their leverage. They set guidelines, require transparency and can terminate managers quickly for underperformance. Consultants such as Mercer and Aon standardize comparisons, and multi-manager structures make replacement easier and faster.

Retail price sensitivity

Individual investors increasingly compare fees vs ETFs and robo-advisors as ETFs surpassed roughly $12 trillion in global AUM in 2024 and automated platforms charge about 0.20–0.35% on average. Wealth clients demand holistic planning and digital UX, raising service expectations without proportional fee growth; breakpoints and bundled pricing requests rose in 2024. Education and outcomes-based narratives (ROI, goal success rates) defend advisory value.

Switching costs

For liquid equity and ETF strategies switching managers is operationally straightforward — reallocations can occur in days, keeping customer bargaining power high. In alternatives and bespoke mandates lockups typically range from 1 to 7 years and tax-triggered realized gains can create meaningful frictions, moderating that power. Performance drawdowns and risk events prompt rapid outflows, with institutional reallocations often completed within weeks. Strong client service and customization materially increase client stickiness.

Information transparency

- Regulatory reports: standardized comparability

- Real-time portals: higher reporting/ESG expectations

- Buyer power: leverage to push fees/terms

- Pricing defense: attribution and unique insights

Channel concentration

Gatekeepers such as wirehouses and platforms aggregate retail demand and negotiate fees at scale; BlackRock remained the largest manager with over 10 trillion USD AUM in 2024 while custodians like Schwab, Fidelity and Vanguard each held trillions in client assets, concentrating distribution power. Institutional consultants (Mercer, Aon, Willis Towers Watson) shape shortlists and direct flows into approved managers, intensifying buyer bargaining power. Diversifying channels—direct wholesaling, boutique platforms, and institutional mandates—reduces exposure to any single gatekeeper.

- Gatekeepers: platforms & wirehouses concentrate retail flows

- Scale: BlackRock >10T AUM in 2024

- Consultants: concentrate institutional allocations

- Mitigation: diversify distribution channels

Institutional pressure as >60% of AUM; ETFs ~12T; robo fees 0.20–0.35%

Institutional clients (over 60% of global AUM in 2024) and gatekeepers exert strong fee/term pressure, often replacing managers rapidly. Retail/wealth clients compare fees vs ETFs (~12T USD global AUM in 2024) and robo fees (~0.20–0.35%), raising service demands. Alternatives' lockups (1–7 years) and proprietary attribution can preserve manager pricing power.

| Metric | 2024 |

|---|---|

| Institutional share of AUM | >60% |

| Global ETF AUM | ~12T USD |

| BlackRock AUM | >10T USD |

| Robo-advisor avg fee | 0.20–0.35% |

| Alternatives lockup | 1–7 yrs |

Preview the Actual Deliverable

Guardian Capital Porter's Five Forces Analysis

This preview shows the Guardian Capital Porter's Five Forces Analysis exactly as delivered—no placeholders or samples. The full document is fully formatted, professionally written and ready for immediate download after purchase. You’ll receive this identical file instantly, ready to use.

Don't Miss the Bigger Picture

Guardian Capital’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, substitute threats, and barriers to entry, revealing where strategic pressure points lie. This concise overview signals key risks and opportunities across the firm’s market position. Ready to move beyond the basics? Get the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Talent scarcity

In 2024 Guardian faces acute scarcity of experienced portfolio managers, quants and advisors who are highly mobile and drive up wages and retention costs. Star hires increasingly secure revenue-sharing or bespoke bonus deals, shifting leverage toward talent. Weakening non-compete enforcement in some US states in 2024 further raises mobility risk. Guardian counters with culture, equity incentives and structured training pipelines.

Data and indices

Dependence on benchmark licensors such as MSCI and S&P and market data vendors raises switching costs and pricing exposure, especially as passive vehicles now reference over $12 trillion of global ETF AUM in 2024. Price hikes or licensing changes can compress margins or force product redesigns, limiting go-to-market agility. Multi-vendor strategies reduce single-vendor risk but add integration complexity and operational overhead, while proprietary research and factor models can partially offset reliance.

Custody and brokerage

Custodians, prime brokers and execution venues form critical infrastructure with few top-tier providers; global assets under custody exceeded $100 trillion in 2024, concentrating market power. Volume-based pricing and best-execution rules cap price leverage, but service-quality gaps drive switching costs and impact performance. Ongoing consolidation among custodians can raise fees or force bundled services, so Guardian uses strategic partnerships and regular RFPs to preserve competitive terms.

Technology platforms

Reliance on OMS/EMS, risk and client-reporting systems ties Guardian Capital to vendors with high changeover costs; integrations and data reconciliation often generate six-figure migration expenses and months of downtime risk. Cloud services and APIs improved portability—public cloud grew about 20% in 2024—but do not eliminate switching friction. Vendor outages remain material operational and reputational risks. Co-development and modular architectures can rebalance vendor leverage.

- High switching cost: six-figure integrations

- Cloud growth 2024: ~20%

- Outages = operational + reputational risk

- Mitigation: co-development, modular APIs

Distribution partners

Third-party platforms, consultants and intermediaries remain gatekeepers to client access in 2024, with preferred lists and due-diligence gates often forcing fee concessions or marketing support; platform concentration increases listing and shelf-space costs, while expanding direct channels and brand recognition reduces dependency.

- Gatekeepers: platforms/consultants

- Concessions: fees & marketing

- Cost: concentrated platforms

- Mitigation: direct channels & branding

Tight talent, custodial concentration squeeze margins; ETFs $12T, AUC >$100T

Supplier power is high: talent scarcity drove revenue-share deals and raises in 2024, forcing higher retention spend. Licensing and data vendors risk margin pressure as passive vehicles reference ~$12 trillion ETF AUM in 2024. Custodial concentration (global AUC >$100 trillion in 2024) and OMS/EMS migration costs create switching barriers. Guardian mitigates via equity, co-development, multi-vendor and direct channels.

| Metric | 2024 |

|---|---|

| ETF AUM referenced | $12 trillion |

| Global assets under custody | $100 trillion+ |

| Public cloud growth | ~20% |

| Typical migration cost | Six-figure |

What is included in the product

Tailored Porter's Five Forces analysis for Guardian Capital that uncovers key competitive drivers, buyer/supplier power, barriers to entry, substitution threats, and emerging disruptors—with strategic commentary to inform pricing, profitability, and defensive positioning.

A clear, one-sheet Guardian Capital Porter's Five Forces summary—instantly visualize competitive pressure with a spider chart and swap in your own data for quick, board-ready insights.

Customers Bargaining Power

Institutional leverage

Pensions, endowments and insurers run competitive RFPs and mandate sizable allocations, enabling strong fee negotiations; institutional investors held over 60% of global AUM in 2024, magnifying their leverage. They set guidelines, require transparency and can terminate managers quickly for underperformance. Consultants such as Mercer and Aon standardize comparisons, and multi-manager structures make replacement easier and faster.

Retail price sensitivity

Individual investors increasingly compare fees vs ETFs and robo-advisors as ETFs surpassed roughly $12 trillion in global AUM in 2024 and automated platforms charge about 0.20–0.35% on average. Wealth clients demand holistic planning and digital UX, raising service expectations without proportional fee growth; breakpoints and bundled pricing requests rose in 2024. Education and outcomes-based narratives (ROI, goal success rates) defend advisory value.

Switching costs

For liquid equity and ETF strategies switching managers is operationally straightforward — reallocations can occur in days, keeping customer bargaining power high. In alternatives and bespoke mandates lockups typically range from 1 to 7 years and tax-triggered realized gains can create meaningful frictions, moderating that power. Performance drawdowns and risk events prompt rapid outflows, with institutional reallocations often completed within weeks. Strong client service and customization materially increase client stickiness.

Information transparency

- Regulatory reports: standardized comparability

- Real-time portals: higher reporting/ESG expectations

- Buyer power: leverage to push fees/terms

- Pricing defense: attribution and unique insights

Channel concentration

Gatekeepers such as wirehouses and platforms aggregate retail demand and negotiate fees at scale; BlackRock remained the largest manager with over 10 trillion USD AUM in 2024 while custodians like Schwab, Fidelity and Vanguard each held trillions in client assets, concentrating distribution power. Institutional consultants (Mercer, Aon, Willis Towers Watson) shape shortlists and direct flows into approved managers, intensifying buyer bargaining power. Diversifying channels—direct wholesaling, boutique platforms, and institutional mandates—reduces exposure to any single gatekeeper.

- Gatekeepers: platforms & wirehouses concentrate retail flows

- Scale: BlackRock >10T AUM in 2024

- Consultants: concentrate institutional allocations

- Mitigation: diversify distribution channels

Institutional pressure as >60% of AUM; ETFs ~12T; robo fees 0.20–0.35%

Institutional clients (over 60% of global AUM in 2024) and gatekeepers exert strong fee/term pressure, often replacing managers rapidly. Retail/wealth clients compare fees vs ETFs (~12T USD global AUM in 2024) and robo fees (~0.20–0.35%), raising service demands. Alternatives' lockups (1–7 years) and proprietary attribution can preserve manager pricing power.

| Metric | 2024 |

|---|---|

| Institutional share of AUM | >60% |

| Global ETF AUM | ~12T USD |

| BlackRock AUM | >10T USD |

| Robo-advisor avg fee | 0.20–0.35% |

| Alternatives lockup | 1–7 yrs |

Preview the Actual Deliverable

Guardian Capital Porter's Five Forces Analysis

This preview shows the Guardian Capital Porter's Five Forces Analysis exactly as delivered—no placeholders or samples. The full document is fully formatted, professionally written and ready for immediate download after purchase. You’ll receive this identical file instantly, ready to use.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Guardian Capital’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, substitute threats, and barriers to entry, revealing where strategic pressure points lie. This concise overview signals key risks and opportunities across the firm’s market position. Ready to move beyond the basics? Get the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Talent scarcity

In 2024 Guardian faces acute scarcity of experienced portfolio managers, quants and advisors who are highly mobile and drive up wages and retention costs. Star hires increasingly secure revenue-sharing or bespoke bonus deals, shifting leverage toward talent. Weakening non-compete enforcement in some US states in 2024 further raises mobility risk. Guardian counters with culture, equity incentives and structured training pipelines.

Data and indices

Dependence on benchmark licensors such as MSCI and S&P and market data vendors raises switching costs and pricing exposure, especially as passive vehicles now reference over $12 trillion of global ETF AUM in 2024. Price hikes or licensing changes can compress margins or force product redesigns, limiting go-to-market agility. Multi-vendor strategies reduce single-vendor risk but add integration complexity and operational overhead, while proprietary research and factor models can partially offset reliance.

Custody and brokerage

Custodians, prime brokers and execution venues form critical infrastructure with few top-tier providers; global assets under custody exceeded $100 trillion in 2024, concentrating market power. Volume-based pricing and best-execution rules cap price leverage, but service-quality gaps drive switching costs and impact performance. Ongoing consolidation among custodians can raise fees or force bundled services, so Guardian uses strategic partnerships and regular RFPs to preserve competitive terms.

Technology platforms

Reliance on OMS/EMS, risk and client-reporting systems ties Guardian Capital to vendors with high changeover costs; integrations and data reconciliation often generate six-figure migration expenses and months of downtime risk. Cloud services and APIs improved portability—public cloud grew about 20% in 2024—but do not eliminate switching friction. Vendor outages remain material operational and reputational risks. Co-development and modular architectures can rebalance vendor leverage.

- High switching cost: six-figure integrations

- Cloud growth 2024: ~20%

- Outages = operational + reputational risk

- Mitigation: co-development, modular APIs

Distribution partners

Third-party platforms, consultants and intermediaries remain gatekeepers to client access in 2024, with preferred lists and due-diligence gates often forcing fee concessions or marketing support; platform concentration increases listing and shelf-space costs, while expanding direct channels and brand recognition reduces dependency.

- Gatekeepers: platforms/consultants

- Concessions: fees & marketing

- Cost: concentrated platforms

- Mitigation: direct channels & branding

Tight talent, custodial concentration squeeze margins; ETFs $12T, AUC >$100T

Supplier power is high: talent scarcity drove revenue-share deals and raises in 2024, forcing higher retention spend. Licensing and data vendors risk margin pressure as passive vehicles reference ~$12 trillion ETF AUM in 2024. Custodial concentration (global AUC >$100 trillion in 2024) and OMS/EMS migration costs create switching barriers. Guardian mitigates via equity, co-development, multi-vendor and direct channels.

| Metric | 2024 |

|---|---|

| ETF AUM referenced | $12 trillion |

| Global assets under custody | $100 trillion+ |

| Public cloud growth | ~20% |

| Typical migration cost | Six-figure |

What is included in the product

Tailored Porter's Five Forces analysis for Guardian Capital that uncovers key competitive drivers, buyer/supplier power, barriers to entry, substitution threats, and emerging disruptors—with strategic commentary to inform pricing, profitability, and defensive positioning.

A clear, one-sheet Guardian Capital Porter's Five Forces summary—instantly visualize competitive pressure with a spider chart and swap in your own data for quick, board-ready insights.

Customers Bargaining Power

Institutional leverage

Pensions, endowments and insurers run competitive RFPs and mandate sizable allocations, enabling strong fee negotiations; institutional investors held over 60% of global AUM in 2024, magnifying their leverage. They set guidelines, require transparency and can terminate managers quickly for underperformance. Consultants such as Mercer and Aon standardize comparisons, and multi-manager structures make replacement easier and faster.

Retail price sensitivity

Individual investors increasingly compare fees vs ETFs and robo-advisors as ETFs surpassed roughly $12 trillion in global AUM in 2024 and automated platforms charge about 0.20–0.35% on average. Wealth clients demand holistic planning and digital UX, raising service expectations without proportional fee growth; breakpoints and bundled pricing requests rose in 2024. Education and outcomes-based narratives (ROI, goal success rates) defend advisory value.

Switching costs

For liquid equity and ETF strategies switching managers is operationally straightforward — reallocations can occur in days, keeping customer bargaining power high. In alternatives and bespoke mandates lockups typically range from 1 to 7 years and tax-triggered realized gains can create meaningful frictions, moderating that power. Performance drawdowns and risk events prompt rapid outflows, with institutional reallocations often completed within weeks. Strong client service and customization materially increase client stickiness.

Information transparency

- Regulatory reports: standardized comparability

- Real-time portals: higher reporting/ESG expectations

- Buyer power: leverage to push fees/terms

- Pricing defense: attribution and unique insights

Channel concentration

Gatekeepers such as wirehouses and platforms aggregate retail demand and negotiate fees at scale; BlackRock remained the largest manager with over 10 trillion USD AUM in 2024 while custodians like Schwab, Fidelity and Vanguard each held trillions in client assets, concentrating distribution power. Institutional consultants (Mercer, Aon, Willis Towers Watson) shape shortlists and direct flows into approved managers, intensifying buyer bargaining power. Diversifying channels—direct wholesaling, boutique platforms, and institutional mandates—reduces exposure to any single gatekeeper.

- Gatekeepers: platforms & wirehouses concentrate retail flows

- Scale: BlackRock >10T AUM in 2024

- Consultants: concentrate institutional allocations

- Mitigation: diversify distribution channels

Institutional pressure as >60% of AUM; ETFs ~12T; robo fees 0.20–0.35%

Institutional clients (over 60% of global AUM in 2024) and gatekeepers exert strong fee/term pressure, often replacing managers rapidly. Retail/wealth clients compare fees vs ETFs (~12T USD global AUM in 2024) and robo fees (~0.20–0.35%), raising service demands. Alternatives' lockups (1–7 years) and proprietary attribution can preserve manager pricing power.

| Metric | 2024 |

|---|---|

| Institutional share of AUM | >60% |

| Global ETF AUM | ~12T USD |

| BlackRock AUM | >10T USD |

| Robo-advisor avg fee | 0.20–0.35% |

| Alternatives lockup | 1–7 yrs |

Preview the Actual Deliverable

Guardian Capital Porter's Five Forces Analysis

This preview shows the Guardian Capital Porter's Five Forces Analysis exactly as delivered—no placeholders or samples. The full document is fully formatted, professionally written and ready for immediate download after purchase. You’ll receive this identical file instantly, ready to use.