Great Wall Motor Business Model Canvas

Strategic Business Model Canvas for automotive growth and investment insights

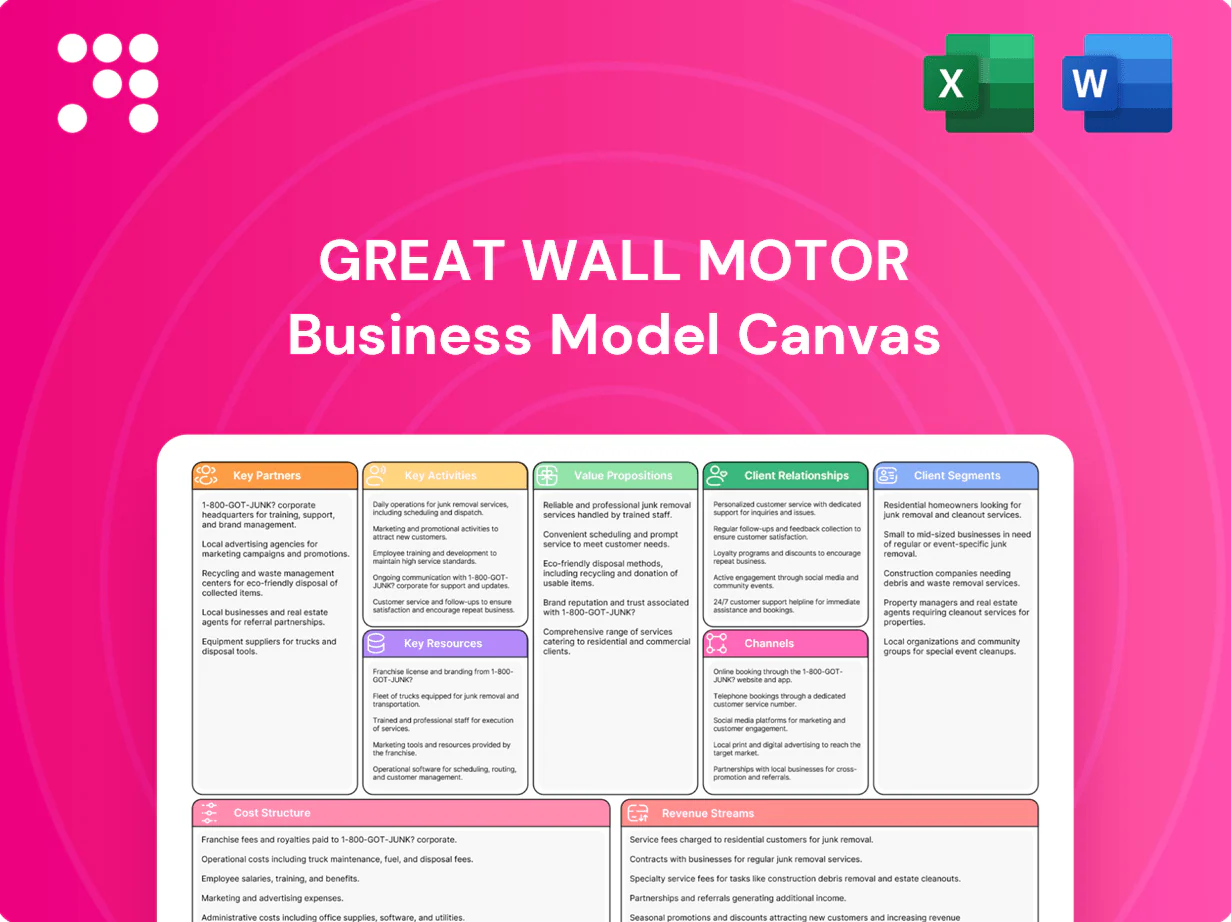

Unlock the full strategic blueprint behind Great Wall Motor with our Business Model Canvas. This concise, actionable analysis reveals how GWM creates value, scales operations, and captures market share across segments. Download the complete Word and Excel canvases to benchmark strategy, inform investments, and accelerate decision-making.

Partnerships

Global component suppliers

Strategic relationships with battery, semiconductor, electronics and drivetrain suppliers secure quality and volume through long-term agreements that stabilize pricing and mitigate shortages; co-development with tier‑1s accelerates EV/HEV innovation and safety features, while supplier localization in key markets reduces tariffs and logistics risk.

Dealers and import/distribution networks

Authorized dealer groups deliver sales, servicing and brand experience across domestic and export markets, while 2024 saw dealers intensify role in aftersales to protect residual values. Importers handle homologation and regulatory compliance for new geographies, enabling faster market entry in 2024. Performance-based partnerships tie incentives to retail throughput and CSI, lifting showroom conversion and satisfaction. Shared marketing and inventory planning improved sell-through and stabilised residuals in 2024.

Technology and software partners

Technology and software partnerships for ADAS, connectivity, infotainment and OTA systems raised vehicle intelligence across Great Wall Motor 2024 models, shortening digital feature rollouts and enabling modular upgrades across model cycles. Collaboration with cybersecurity and data-platform vendors enforces compliance and reliability while joint roadmaps reduce integration lead times.

Manufacturing and localization partners

CKD/SKD assemblers and local suppliers enable cost-effective entry, supporting GWM’s 2024 push to scale production toward ~1.2M units by leveraging reduced tariffs and lower local labor costs. Government and industrial park partnerships unlock capex incentives and land access, accelerating plant setup. Logistics partners synchronize inbound parts and outbound vehicle flows to match production cadence, while local engineering firms handle homologation and adapt vehicles to regional preferences.

- CKD/SKD assemblers: lower entry costs

- Government parks: capex & land incentives

- Logistics: production-aligned flow

- Local engineering: homologation & localization

Financial and mobility services

Banking and captive finance alliances expand retail and fleet financing, supporting GWM as China's auto finance penetration reached about 55% in 2024, boosting sales of pickups and SUVs.

Insurance partners bundle coverage at point-of-sale, reducing buyer drop-off and claim friction.

Fleet, ride-hailing, subscription and leasing intermediaries drive volume and retention.

- finance: captive & banks

- insurance: bundled POS

- fleet: ride-hailing volumes

- leasing: subscriptions improve affordability

Supplier and CKD/SKD partnerships accelerate EV/ADAS rollouts and stabilise costs

Strategic supplier and co-development ties secure battery, semiconductor and drivetrain supply, accelerating EV/ADAS rollouts and stabilising costs. Dealer, CKD/SKD and logistics partners scale market entry and aftersales; CKD/SKD support helped GWM target ~1.2M units in 2024. Tech, cybersecurity and OTA partners speed digital feature delivery. Captive finance and banks benefit from China auto finance penetration ~55% in 2024.

| Partnership | Role | 2024 metric |

|---|---|---|

| CKD/SKD assemblers | Local production entry | Supports ~1.2M unit scale |

| Captive finance & banks | Retail financing | China finance penetration ~55% |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Great Wall Motor outlining customer segments, channels, nine BMC blocks, core value propositions (ICE and EV vehicles), key partners, revenue streams and cost structure, plus SWOT-linked insights for investor presentations and strategic planning.

High-level one-page Business Model Canvas for Great Wall Motor that condenses strategy into editable cells, saving hours of formatting and clarifying core components for quick decision-making. Shareable and ready for boardrooms, it's perfect for comparing models, brainstorming, or creating fast executive summaries.

Activities

Vehicle R&D and platform engineering

Development of ICE, HEV, PHEV and BEV architectures underpins GWM’s four core brands — Haval, Tank, Ora and Wey — enabling shared modules across segments; modular platforms accelerate model refreshes and variant launches. In-house testing at R&D centers in China, the UK and Australia validates safety, durability and efficiency targets. Software integration prioritizes ADAS, connectivity and energy management to support electrified portfolios; GWM sold ~1.45M vehicles in 2023.

Manufacturing and quality operations

End-to-end production at Great Wall Motor covers stamping, body, paint, assembly and powertrain, supporting a scale of over 1 million vehicles annually; integrated lines enable faster takt times and throughput. Lean practices and factory automation cut cycle times and can reduce defects by up to 30%, improving yield and unit cost. Localization of parts (local content often exceeding 50%) lowers procurement costs and mitigates tariffs, while continuous quality monitoring has reduced warranty claims and strengthened brand reputation.

Supply chain and procurement management

Strategic sourcing secures batteries, chips and critical materials from key partners such as CATL while locking multi-year purchase agreements; dual-sourcing plus 45–60 day inventory buffers reduce disruption risk; global logistics coordinate inbound components and outbound vehicles across 20+ markets; supplier development programs lifted supplier audit pass rates to 92% in 2024.

Branding and go-to-market execution

- Segmented brands: Haval, Tank, Wey, Ora, Poer

- Channels: TV, digital, dealer activation

- Pricing: elasticity‑aligned incentives & finance

- After-sales: warranties, service networks, loyalty programs

International expansion and compliance

Market entry prioritizes demand potential, regulatory barriers and cost-to-serve, steering GWM toward high-growth ASEAN, Latin America and MENA corridors; homologation and safety certifications adapt powertrains and crash standards to local regimes; targeted assembly and local-content plans capture fiscal incentives and supply resilience; distributor onboarding ensures service readiness and parts availability; as of 2024 GWM is present in 60+ markets.

- Market selection: demand, regulation, cost-to-serve

- Compliance: homologation, safety certifications

- Local assembly: incentives, resilience

- Distributor onboarding: service, spare parts

Modular ICE/HEV/PHEV/BEV R&D, RMB 12.4bn spend, 1.6M vehicles (2024)

R&D: modular ICE/HEV/PHEV/BEV platforms, R&D centers CN/UK/AU, 2024 R&D spend ~RMB 12.4bn, 1.6M vehicles sold (2024).

Manufacturing: end‑to‑end lines, >1M annual capacity, local content >50%, automation cut defects ~30%.

Supply & markets: multi‑year contracts with CATL, supplier audit pass 92% (2024), presence in 60+ markets.

| Metric | 2024 |

|---|---|

| Global sales | 1.6M |

| R&D spend | RMB 12.4bn |

| Markets | 60+ |

Preview Before You Purchase

Business Model Canvas

The document previewed here is the actual Great Wall Motor Business Model Canvas, not a mockup. When you purchase, you’ll receive this exact file—complete, formatted and ready to edit—in Word and Excel. No placeholders, no surprises, instant download.

Strategic Business Model Canvas for automotive growth and investment insights

Unlock the full strategic blueprint behind Great Wall Motor with our Business Model Canvas. This concise, actionable analysis reveals how GWM creates value, scales operations, and captures market share across segments. Download the complete Word and Excel canvases to benchmark strategy, inform investments, and accelerate decision-making.

Partnerships

Global component suppliers

Strategic relationships with battery, semiconductor, electronics and drivetrain suppliers secure quality and volume through long-term agreements that stabilize pricing and mitigate shortages; co-development with tier‑1s accelerates EV/HEV innovation and safety features, while supplier localization in key markets reduces tariffs and logistics risk.

Dealers and import/distribution networks

Authorized dealer groups deliver sales, servicing and brand experience across domestic and export markets, while 2024 saw dealers intensify role in aftersales to protect residual values. Importers handle homologation and regulatory compliance for new geographies, enabling faster market entry in 2024. Performance-based partnerships tie incentives to retail throughput and CSI, lifting showroom conversion and satisfaction. Shared marketing and inventory planning improved sell-through and stabilised residuals in 2024.

Technology and software partners

Technology and software partnerships for ADAS, connectivity, infotainment and OTA systems raised vehicle intelligence across Great Wall Motor 2024 models, shortening digital feature rollouts and enabling modular upgrades across model cycles. Collaboration with cybersecurity and data-platform vendors enforces compliance and reliability while joint roadmaps reduce integration lead times.

Manufacturing and localization partners

CKD/SKD assemblers and local suppliers enable cost-effective entry, supporting GWM’s 2024 push to scale production toward ~1.2M units by leveraging reduced tariffs and lower local labor costs. Government and industrial park partnerships unlock capex incentives and land access, accelerating plant setup. Logistics partners synchronize inbound parts and outbound vehicle flows to match production cadence, while local engineering firms handle homologation and adapt vehicles to regional preferences.

- CKD/SKD assemblers: lower entry costs

- Government parks: capex & land incentives

- Logistics: production-aligned flow

- Local engineering: homologation & localization

Financial and mobility services

Banking and captive finance alliances expand retail and fleet financing, supporting GWM as China's auto finance penetration reached about 55% in 2024, boosting sales of pickups and SUVs.

Insurance partners bundle coverage at point-of-sale, reducing buyer drop-off and claim friction.

Fleet, ride-hailing, subscription and leasing intermediaries drive volume and retention.

- finance: captive & banks

- insurance: bundled POS

- fleet: ride-hailing volumes

- leasing: subscriptions improve affordability

Supplier and CKD/SKD partnerships accelerate EV/ADAS rollouts and stabilise costs

Strategic supplier and co-development ties secure battery, semiconductor and drivetrain supply, accelerating EV/ADAS rollouts and stabilising costs. Dealer, CKD/SKD and logistics partners scale market entry and aftersales; CKD/SKD support helped GWM target ~1.2M units in 2024. Tech, cybersecurity and OTA partners speed digital feature delivery. Captive finance and banks benefit from China auto finance penetration ~55% in 2024.

| Partnership | Role | 2024 metric |

|---|---|---|

| CKD/SKD assemblers | Local production entry | Supports ~1.2M unit scale |

| Captive finance & banks | Retail financing | China finance penetration ~55% |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Great Wall Motor outlining customer segments, channels, nine BMC blocks, core value propositions (ICE and EV vehicles), key partners, revenue streams and cost structure, plus SWOT-linked insights for investor presentations and strategic planning.

High-level one-page Business Model Canvas for Great Wall Motor that condenses strategy into editable cells, saving hours of formatting and clarifying core components for quick decision-making. Shareable and ready for boardrooms, it's perfect for comparing models, brainstorming, or creating fast executive summaries.

Activities

Vehicle R&D and platform engineering

Development of ICE, HEV, PHEV and BEV architectures underpins GWM’s four core brands — Haval, Tank, Ora and Wey — enabling shared modules across segments; modular platforms accelerate model refreshes and variant launches. In-house testing at R&D centers in China, the UK and Australia validates safety, durability and efficiency targets. Software integration prioritizes ADAS, connectivity and energy management to support electrified portfolios; GWM sold ~1.45M vehicles in 2023.

Manufacturing and quality operations

End-to-end production at Great Wall Motor covers stamping, body, paint, assembly and powertrain, supporting a scale of over 1 million vehicles annually; integrated lines enable faster takt times and throughput. Lean practices and factory automation cut cycle times and can reduce defects by up to 30%, improving yield and unit cost. Localization of parts (local content often exceeding 50%) lowers procurement costs and mitigates tariffs, while continuous quality monitoring has reduced warranty claims and strengthened brand reputation.

Supply chain and procurement management

Strategic sourcing secures batteries, chips and critical materials from key partners such as CATL while locking multi-year purchase agreements; dual-sourcing plus 45–60 day inventory buffers reduce disruption risk; global logistics coordinate inbound components and outbound vehicles across 20+ markets; supplier development programs lifted supplier audit pass rates to 92% in 2024.

Branding and go-to-market execution

- Segmented brands: Haval, Tank, Wey, Ora, Poer

- Channels: TV, digital, dealer activation

- Pricing: elasticity‑aligned incentives & finance

- After-sales: warranties, service networks, loyalty programs

International expansion and compliance

Market entry prioritizes demand potential, regulatory barriers and cost-to-serve, steering GWM toward high-growth ASEAN, Latin America and MENA corridors; homologation and safety certifications adapt powertrains and crash standards to local regimes; targeted assembly and local-content plans capture fiscal incentives and supply resilience; distributor onboarding ensures service readiness and parts availability; as of 2024 GWM is present in 60+ markets.

- Market selection: demand, regulation, cost-to-serve

- Compliance: homologation, safety certifications

- Local assembly: incentives, resilience

- Distributor onboarding: service, spare parts

Modular ICE/HEV/PHEV/BEV R&D, RMB 12.4bn spend, 1.6M vehicles (2024)

R&D: modular ICE/HEV/PHEV/BEV platforms, R&D centers CN/UK/AU, 2024 R&D spend ~RMB 12.4bn, 1.6M vehicles sold (2024).

Manufacturing: end‑to‑end lines, >1M annual capacity, local content >50%, automation cut defects ~30%.

Supply & markets: multi‑year contracts with CATL, supplier audit pass 92% (2024), presence in 60+ markets.

| Metric | 2024 |

|---|---|

| Global sales | 1.6M |

| R&D spend | RMB 12.4bn |

| Markets | 60+ |

Preview Before You Purchase

Business Model Canvas

The document previewed here is the actual Great Wall Motor Business Model Canvas, not a mockup. When you purchase, you’ll receive this exact file—complete, formatted and ready to edit—in Word and Excel. No placeholders, no surprises, instant download.

Description

Strategic Business Model Canvas for automotive growth and investment insights

Unlock the full strategic blueprint behind Great Wall Motor with our Business Model Canvas. This concise, actionable analysis reveals how GWM creates value, scales operations, and captures market share across segments. Download the complete Word and Excel canvases to benchmark strategy, inform investments, and accelerate decision-making.

Partnerships

Global component suppliers

Strategic relationships with battery, semiconductor, electronics and drivetrain suppliers secure quality and volume through long-term agreements that stabilize pricing and mitigate shortages; co-development with tier‑1s accelerates EV/HEV innovation and safety features, while supplier localization in key markets reduces tariffs and logistics risk.

Dealers and import/distribution networks

Authorized dealer groups deliver sales, servicing and brand experience across domestic and export markets, while 2024 saw dealers intensify role in aftersales to protect residual values. Importers handle homologation and regulatory compliance for new geographies, enabling faster market entry in 2024. Performance-based partnerships tie incentives to retail throughput and CSI, lifting showroom conversion and satisfaction. Shared marketing and inventory planning improved sell-through and stabilised residuals in 2024.

Technology and software partners

Technology and software partnerships for ADAS, connectivity, infotainment and OTA systems raised vehicle intelligence across Great Wall Motor 2024 models, shortening digital feature rollouts and enabling modular upgrades across model cycles. Collaboration with cybersecurity and data-platform vendors enforces compliance and reliability while joint roadmaps reduce integration lead times.

Manufacturing and localization partners

CKD/SKD assemblers and local suppliers enable cost-effective entry, supporting GWM’s 2024 push to scale production toward ~1.2M units by leveraging reduced tariffs and lower local labor costs. Government and industrial park partnerships unlock capex incentives and land access, accelerating plant setup. Logistics partners synchronize inbound parts and outbound vehicle flows to match production cadence, while local engineering firms handle homologation and adapt vehicles to regional preferences.

- CKD/SKD assemblers: lower entry costs

- Government parks: capex & land incentives

- Logistics: production-aligned flow

- Local engineering: homologation & localization

Financial and mobility services

Banking and captive finance alliances expand retail and fleet financing, supporting GWM as China's auto finance penetration reached about 55% in 2024, boosting sales of pickups and SUVs.

Insurance partners bundle coverage at point-of-sale, reducing buyer drop-off and claim friction.

Fleet, ride-hailing, subscription and leasing intermediaries drive volume and retention.

- finance: captive & banks

- insurance: bundled POS

- fleet: ride-hailing volumes

- leasing: subscriptions improve affordability

Supplier and CKD/SKD partnerships accelerate EV/ADAS rollouts and stabilise costs

Strategic supplier and co-development ties secure battery, semiconductor and drivetrain supply, accelerating EV/ADAS rollouts and stabilising costs. Dealer, CKD/SKD and logistics partners scale market entry and aftersales; CKD/SKD support helped GWM target ~1.2M units in 2024. Tech, cybersecurity and OTA partners speed digital feature delivery. Captive finance and banks benefit from China auto finance penetration ~55% in 2024.

| Partnership | Role | 2024 metric |

|---|---|---|

| CKD/SKD assemblers | Local production entry | Supports ~1.2M unit scale |

| Captive finance & banks | Retail financing | China finance penetration ~55% |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Great Wall Motor outlining customer segments, channels, nine BMC blocks, core value propositions (ICE and EV vehicles), key partners, revenue streams and cost structure, plus SWOT-linked insights for investor presentations and strategic planning.

High-level one-page Business Model Canvas for Great Wall Motor that condenses strategy into editable cells, saving hours of formatting and clarifying core components for quick decision-making. Shareable and ready for boardrooms, it's perfect for comparing models, brainstorming, or creating fast executive summaries.

Activities

Vehicle R&D and platform engineering

Development of ICE, HEV, PHEV and BEV architectures underpins GWM’s four core brands — Haval, Tank, Ora and Wey — enabling shared modules across segments; modular platforms accelerate model refreshes and variant launches. In-house testing at R&D centers in China, the UK and Australia validates safety, durability and efficiency targets. Software integration prioritizes ADAS, connectivity and energy management to support electrified portfolios; GWM sold ~1.45M vehicles in 2023.

Manufacturing and quality operations

End-to-end production at Great Wall Motor covers stamping, body, paint, assembly and powertrain, supporting a scale of over 1 million vehicles annually; integrated lines enable faster takt times and throughput. Lean practices and factory automation cut cycle times and can reduce defects by up to 30%, improving yield and unit cost. Localization of parts (local content often exceeding 50%) lowers procurement costs and mitigates tariffs, while continuous quality monitoring has reduced warranty claims and strengthened brand reputation.

Supply chain and procurement management

Strategic sourcing secures batteries, chips and critical materials from key partners such as CATL while locking multi-year purchase agreements; dual-sourcing plus 45–60 day inventory buffers reduce disruption risk; global logistics coordinate inbound components and outbound vehicles across 20+ markets; supplier development programs lifted supplier audit pass rates to 92% in 2024.

Branding and go-to-market execution

- Segmented brands: Haval, Tank, Wey, Ora, Poer

- Channels: TV, digital, dealer activation

- Pricing: elasticity‑aligned incentives & finance

- After-sales: warranties, service networks, loyalty programs

International expansion and compliance

Market entry prioritizes demand potential, regulatory barriers and cost-to-serve, steering GWM toward high-growth ASEAN, Latin America and MENA corridors; homologation and safety certifications adapt powertrains and crash standards to local regimes; targeted assembly and local-content plans capture fiscal incentives and supply resilience; distributor onboarding ensures service readiness and parts availability; as of 2024 GWM is present in 60+ markets.

- Market selection: demand, regulation, cost-to-serve

- Compliance: homologation, safety certifications

- Local assembly: incentives, resilience

- Distributor onboarding: service, spare parts

Modular ICE/HEV/PHEV/BEV R&D, RMB 12.4bn spend, 1.6M vehicles (2024)

R&D: modular ICE/HEV/PHEV/BEV platforms, R&D centers CN/UK/AU, 2024 R&D spend ~RMB 12.4bn, 1.6M vehicles sold (2024).

Manufacturing: end‑to‑end lines, >1M annual capacity, local content >50%, automation cut defects ~30%.

Supply & markets: multi‑year contracts with CATL, supplier audit pass 92% (2024), presence in 60+ markets.

| Metric | 2024 |

|---|---|

| Global sales | 1.6M |

| R&D spend | RMB 12.4bn |

| Markets | 60+ |

Preview Before You Purchase

Business Model Canvas

The document previewed here is the actual Great Wall Motor Business Model Canvas, not a mockup. When you purchase, you’ll receive this exact file—complete, formatted and ready to edit—in Word and Excel. No placeholders, no surprises, instant download.