Great Wall Motor Porter's Five Forces Analysis

From Overview to Strategy Blueprint

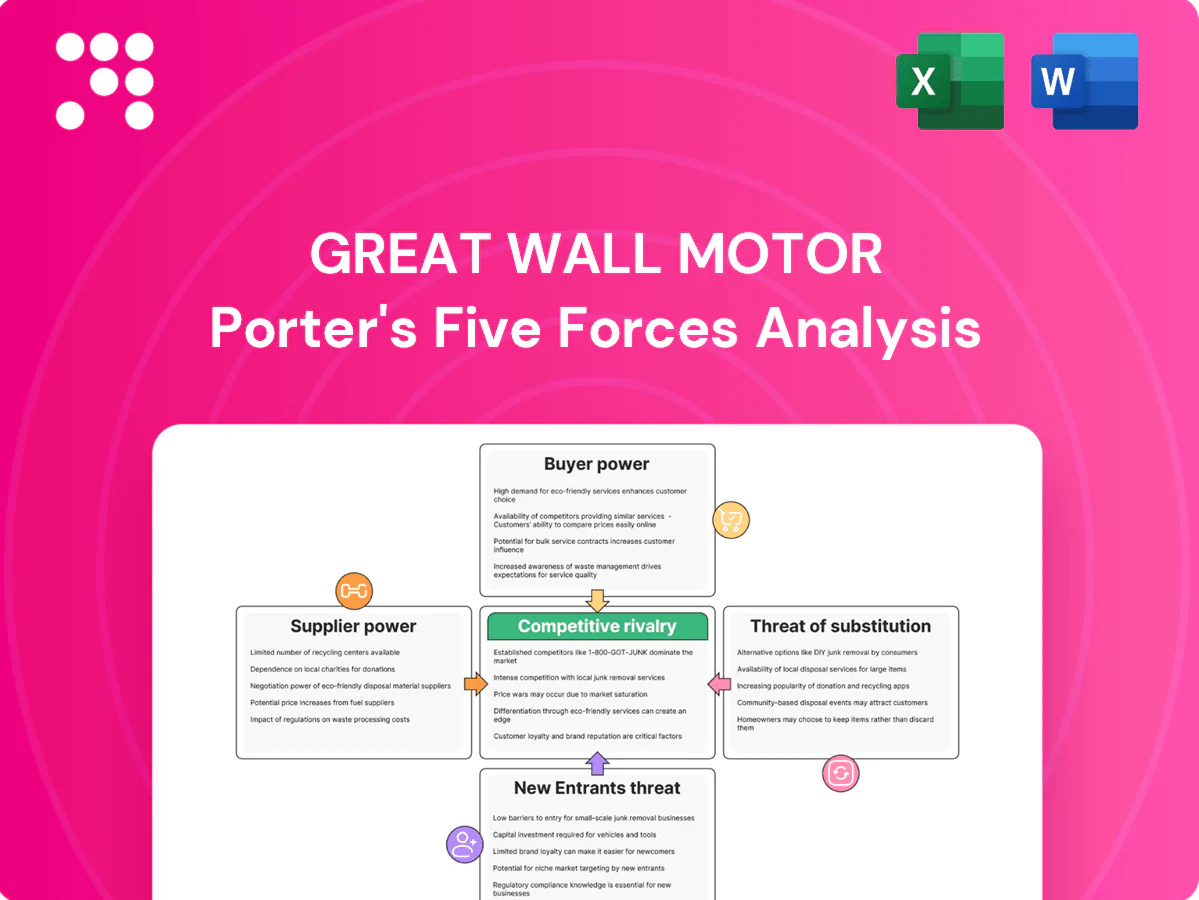

Great Wall Motor faces intense rivalry, rising buyer power in EV markets, moderate supplier influence, growing substitute threats from mobility services, and regulatory/new-entrant pressures. This snapshot highlights key competitive tensions shaping GWM’s strategy. Unlock the full Porter's Five Forces Analysis to explore force-by-force implications and visuals for informed decisions.

Suppliers Bargaining Power

Vertical integration moderates dependency

GWM designs and manufactures core components like engines and transmissions in-house, which reduces dependency and supplier pricing power, but in 2024 its EV battery cells and some power electronics remain largely sourced from suppliers (notably CATL on several models), so supplier leverage rises in domains where vertical integration is incomplete.

Battery and semiconductor suppliers hold leverage

Battery cells and cathode/anode feedstocks remain concentrated: SNE Research 2024 shows CATL and LG Energy Solution account for roughly half of global EV cell capacity, while automotive-grade chips are dominated by NXP, Infineon and Renesas. Long qualification, safety/regulatory tests and software integration make switching slow; shortages or design lock-ins therefore boost supplier leverage, and long-term contracts or dual-sourcing only partially mitigate risk.

Commodity volatility impacts terms

Steel, aluminum and lithium price swings in 2024 (steel HRC ~4,200 RMB/ton, LME aluminum ~2,300 USD/ton, battery-grade lithium carbonate ~25,000 USD/ton) shift bargaining toward upstream producers during tight markets. Hedging reduces volatility exposure but does not eliminate cost pass-through to OEMs. Suppliers increasingly push surcharges or shorten pricing windows. GWM’s scale secures some concessions, but material exposure remains significant.

Tooling, molds, and specialized parts create switching costs

Platform-specific tooling, Tier-1 ADAS sensors and infotainment modules require lengthy requalification and regulatory validation, increasing switching costs and locking Great Wall Motor into niche suppliers; in 2024 requalification timelines and homologation demands intensified this lock-in. Co-development can rebalance bargaining power but deepens dependence.

- Platform tooling: high requalification burden

- ADAS/infotainment: niche supplier leverage

- Regulatory validation: increases lock-in

- Co-development: mitigates cost but raises dependence

Logistics and geopolitical risks lift supplier influence

Trade frictions, export controls—notably US restrictions on advanced semiconductors and some battery materials in 2023–2024—and shipping disruptions have narrowed Great Wall Motor's supplier options. Suppliers assuring continuity command better terms and allocation. Localizing key inputs boosts resilience but requires multi-year capital; diversified sourcing mitigates risk but is imperfect.

- Export controls 2023–24: higher supplier leverage

- Localizing: multi-year, capital-intensive

- Diversified sourcing: reduces but does not eliminate shocks

Powertrain integration limits supplier power; batteries, chips and materials raise upstream risk

GWM's vertical integration in engines/transmissions limits supplier power, but 2024 reliance on external battery cells (CATL+LGES ~50% global EV cell capacity) and key semiconductors raises supplier leverage. Long qualification cycles for ADAS/infotainment and platform tooling increase switching costs. 2024 prices—HRC steel ~4,200 RMB/t, LME Al ~2,300 USD/t, Li2CO3 ~25,000 USD/t—shift power upstream; trade controls 2023–24 further constrain options; GWM scale offsets but does not eliminate risk.

| Item | 2024 metric | Impact |

|---|---|---|

| Battery concentration | CATL+LGES ~50% | High |

| Chips | NXP/Infineon/Renesas dominant | High |

| Materials | Steel 4,200 RMB/t; Al 2,300 USD/t; Li2CO3 25,000 USD/t | Medium-High |

| Tooling/ADAS | Long requalification | High |

What is included in the product

Provides a concise Porter’s Five Forces assessment of Great Wall Motor, revealing competitive intensity, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect margins and market share.

One-sheet Porter’s Five Forces for Great Wall Motor—quickly visualize supplier/buyer power, rivalry, substitutes, and entrants to ease strategic decisions and update pressure levels as market data evolves.

Customers Bargaining Power

Price-sensitive mass-market segments

Great Wall Motor faces strong buyer power in price-sensitive SUV and pickup segments where consumers compare price-performance and can switch brands with low switching costs, increasing price pressure. Discounts and competitive financing—frequently used in 2024 sales campaigns—materially sway purchase decisions. This dynamic amplifies bargaining power, forcing GWM to protect margins through scale, model differentiation and targeted incentives.

Abundant alternatives heighten choice

Domestic rivals and international brands offer overlapping models across segments, and in 2024 China remained the world’s largest auto market, intensifying choice pressure on Great Wall Motor. Feature parity in ADAS and connectivity has narrowed technical differentiation, shifting competition to design, price and aftersales. Easy cross-shopping via online platforms increases buyer leverage, forcing faster product cycles. GWM must continuously refresh models to defend share.

Information transparency compresses margins

Online reviews, social media and dealer price disclosures have substantially improved buyer knowledge, compressing dealer margins; IEA reports 14 million electric cars sold globally in 2023, fueling broader TCO comparisons. Widely available ICE vs EV total cost of ownership calculators reduce information asymmetry and raise customer negotiating power. As a result, short-term promotions quickly become table stakes.

Fleet and government tenders negotiate hard

Fleet and government tenders negotiate hard: large-volume buyers extract bulk discounts and service guarantees, push specs, delivery windows and tougher warranty terms, and can sway bids given GWM’s 2024 global deliveries of about 1.5 million vehicles. Losing a single major tender can reduce plant utilization and raise per-unit costs; GWM’s broad product lineup helps win bids but compresses margins.

- Volume leverage: bulk discounts demanded

- Contract terms: stricter specs, delivery, warranties

- Capacity risk: single tender loss hits utilization

- Competitive bids: breadth aids wins but trims margins

After-sales ecosystem shapes switching costs

After-sales ecosystem — service coverage, parts availability and timely software updates — directly shapes loyalty for Great Wall Motor by raising or lowering switching frictions; strong dealer and service networks reduce buyer power by increasing retention, while gaps in after-sales or weak residual values amplify it. Warranty terms and trade-in programs act as key levers to mitigate customer bargaining power.

- Service coverage: affects loyalty

- Parts availability: reduces switching

- Software updates: sustain value

- Warranty/trade-in: strategic levers

Buyers wield pricing power as heavy 2024 discounts and EV TCO comparisons squeeze SUV/pickup margins

Buyers hold strong price leverage in GWM’s SUV/pickup segments, with low switching costs and heavy 2024 discounting pressuring margins. China remained the world’s largest auto market in 2024, intensifying cross-shop pressure; GWM reported ~1.5 million global deliveries in 2024. Improved buyer information and 2023 global EV sales of 14 million raise TCO comparisons and negotiation power.

| Metric | Value |

|---|---|

| GWM deliveries (2024) | ~1.5 million |

| China market (2024) | World’s largest |

| Global EV sales (2023) | 14 million |

Preview the Actual Deliverable

Great Wall Motor Porter's Five Forces Analysis

This preview shows the exact Great Wall Motor Porter’s Five Forces analysis you'll receive—no placeholders or samples. The document is fully formatted, professionally written, and ready for download immediately after purchase. What you see here is the deliverable you’ll get, complete and usable for decision-making.

From Overview to Strategy Blueprint

Great Wall Motor faces intense rivalry, rising buyer power in EV markets, moderate supplier influence, growing substitute threats from mobility services, and regulatory/new-entrant pressures. This snapshot highlights key competitive tensions shaping GWM’s strategy. Unlock the full Porter's Five Forces Analysis to explore force-by-force implications and visuals for informed decisions.

Suppliers Bargaining Power

Vertical integration moderates dependency

GWM designs and manufactures core components like engines and transmissions in-house, which reduces dependency and supplier pricing power, but in 2024 its EV battery cells and some power electronics remain largely sourced from suppliers (notably CATL on several models), so supplier leverage rises in domains where vertical integration is incomplete.

Battery and semiconductor suppliers hold leverage

Battery cells and cathode/anode feedstocks remain concentrated: SNE Research 2024 shows CATL and LG Energy Solution account for roughly half of global EV cell capacity, while automotive-grade chips are dominated by NXP, Infineon and Renesas. Long qualification, safety/regulatory tests and software integration make switching slow; shortages or design lock-ins therefore boost supplier leverage, and long-term contracts or dual-sourcing only partially mitigate risk.

Commodity volatility impacts terms

Steel, aluminum and lithium price swings in 2024 (steel HRC ~4,200 RMB/ton, LME aluminum ~2,300 USD/ton, battery-grade lithium carbonate ~25,000 USD/ton) shift bargaining toward upstream producers during tight markets. Hedging reduces volatility exposure but does not eliminate cost pass-through to OEMs. Suppliers increasingly push surcharges or shorten pricing windows. GWM’s scale secures some concessions, but material exposure remains significant.

Tooling, molds, and specialized parts create switching costs

Platform-specific tooling, Tier-1 ADAS sensors and infotainment modules require lengthy requalification and regulatory validation, increasing switching costs and locking Great Wall Motor into niche suppliers; in 2024 requalification timelines and homologation demands intensified this lock-in. Co-development can rebalance bargaining power but deepens dependence.

- Platform tooling: high requalification burden

- ADAS/infotainment: niche supplier leverage

- Regulatory validation: increases lock-in

- Co-development: mitigates cost but raises dependence

Logistics and geopolitical risks lift supplier influence

Trade frictions, export controls—notably US restrictions on advanced semiconductors and some battery materials in 2023–2024—and shipping disruptions have narrowed Great Wall Motor's supplier options. Suppliers assuring continuity command better terms and allocation. Localizing key inputs boosts resilience but requires multi-year capital; diversified sourcing mitigates risk but is imperfect.

- Export controls 2023–24: higher supplier leverage

- Localizing: multi-year, capital-intensive

- Diversified sourcing: reduces but does not eliminate shocks

Powertrain integration limits supplier power; batteries, chips and materials raise upstream risk

GWM's vertical integration in engines/transmissions limits supplier power, but 2024 reliance on external battery cells (CATL+LGES ~50% global EV cell capacity) and key semiconductors raises supplier leverage. Long qualification cycles for ADAS/infotainment and platform tooling increase switching costs. 2024 prices—HRC steel ~4,200 RMB/t, LME Al ~2,300 USD/t, Li2CO3 ~25,000 USD/t—shift power upstream; trade controls 2023–24 further constrain options; GWM scale offsets but does not eliminate risk.

| Item | 2024 metric | Impact |

|---|---|---|

| Battery concentration | CATL+LGES ~50% | High |

| Chips | NXP/Infineon/Renesas dominant | High |

| Materials | Steel 4,200 RMB/t; Al 2,300 USD/t; Li2CO3 25,000 USD/t | Medium-High |

| Tooling/ADAS | Long requalification | High |

What is included in the product

Provides a concise Porter’s Five Forces assessment of Great Wall Motor, revealing competitive intensity, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect margins and market share.

One-sheet Porter’s Five Forces for Great Wall Motor—quickly visualize supplier/buyer power, rivalry, substitutes, and entrants to ease strategic decisions and update pressure levels as market data evolves.

Customers Bargaining Power

Price-sensitive mass-market segments

Great Wall Motor faces strong buyer power in price-sensitive SUV and pickup segments where consumers compare price-performance and can switch brands with low switching costs, increasing price pressure. Discounts and competitive financing—frequently used in 2024 sales campaigns—materially sway purchase decisions. This dynamic amplifies bargaining power, forcing GWM to protect margins through scale, model differentiation and targeted incentives.

Abundant alternatives heighten choice

Domestic rivals and international brands offer overlapping models across segments, and in 2024 China remained the world’s largest auto market, intensifying choice pressure on Great Wall Motor. Feature parity in ADAS and connectivity has narrowed technical differentiation, shifting competition to design, price and aftersales. Easy cross-shopping via online platforms increases buyer leverage, forcing faster product cycles. GWM must continuously refresh models to defend share.

Information transparency compresses margins

Online reviews, social media and dealer price disclosures have substantially improved buyer knowledge, compressing dealer margins; IEA reports 14 million electric cars sold globally in 2023, fueling broader TCO comparisons. Widely available ICE vs EV total cost of ownership calculators reduce information asymmetry and raise customer negotiating power. As a result, short-term promotions quickly become table stakes.

Fleet and government tenders negotiate hard

Fleet and government tenders negotiate hard: large-volume buyers extract bulk discounts and service guarantees, push specs, delivery windows and tougher warranty terms, and can sway bids given GWM’s 2024 global deliveries of about 1.5 million vehicles. Losing a single major tender can reduce plant utilization and raise per-unit costs; GWM’s broad product lineup helps win bids but compresses margins.

- Volume leverage: bulk discounts demanded

- Contract terms: stricter specs, delivery, warranties

- Capacity risk: single tender loss hits utilization

- Competitive bids: breadth aids wins but trims margins

After-sales ecosystem shapes switching costs

After-sales ecosystem — service coverage, parts availability and timely software updates — directly shapes loyalty for Great Wall Motor by raising or lowering switching frictions; strong dealer and service networks reduce buyer power by increasing retention, while gaps in after-sales or weak residual values amplify it. Warranty terms and trade-in programs act as key levers to mitigate customer bargaining power.

- Service coverage: affects loyalty

- Parts availability: reduces switching

- Software updates: sustain value

- Warranty/trade-in: strategic levers

Buyers wield pricing power as heavy 2024 discounts and EV TCO comparisons squeeze SUV/pickup margins

Buyers hold strong price leverage in GWM’s SUV/pickup segments, with low switching costs and heavy 2024 discounting pressuring margins. China remained the world’s largest auto market in 2024, intensifying cross-shop pressure; GWM reported ~1.5 million global deliveries in 2024. Improved buyer information and 2023 global EV sales of 14 million raise TCO comparisons and negotiation power.

| Metric | Value |

|---|---|

| GWM deliveries (2024) | ~1.5 million |

| China market (2024) | World’s largest |

| Global EV sales (2023) | 14 million |

Preview the Actual Deliverable

Great Wall Motor Porter's Five Forces Analysis

This preview shows the exact Great Wall Motor Porter’s Five Forces analysis you'll receive—no placeholders or samples. The document is fully formatted, professionally written, and ready for download immediately after purchase. What you see here is the deliverable you’ll get, complete and usable for decision-making.

Description

From Overview to Strategy Blueprint

Great Wall Motor faces intense rivalry, rising buyer power in EV markets, moderate supplier influence, growing substitute threats from mobility services, and regulatory/new-entrant pressures. This snapshot highlights key competitive tensions shaping GWM’s strategy. Unlock the full Porter's Five Forces Analysis to explore force-by-force implications and visuals for informed decisions.

Suppliers Bargaining Power

Vertical integration moderates dependency

GWM designs and manufactures core components like engines and transmissions in-house, which reduces dependency and supplier pricing power, but in 2024 its EV battery cells and some power electronics remain largely sourced from suppliers (notably CATL on several models), so supplier leverage rises in domains where vertical integration is incomplete.

Battery and semiconductor suppliers hold leverage

Battery cells and cathode/anode feedstocks remain concentrated: SNE Research 2024 shows CATL and LG Energy Solution account for roughly half of global EV cell capacity, while automotive-grade chips are dominated by NXP, Infineon and Renesas. Long qualification, safety/regulatory tests and software integration make switching slow; shortages or design lock-ins therefore boost supplier leverage, and long-term contracts or dual-sourcing only partially mitigate risk.

Commodity volatility impacts terms

Steel, aluminum and lithium price swings in 2024 (steel HRC ~4,200 RMB/ton, LME aluminum ~2,300 USD/ton, battery-grade lithium carbonate ~25,000 USD/ton) shift bargaining toward upstream producers during tight markets. Hedging reduces volatility exposure but does not eliminate cost pass-through to OEMs. Suppliers increasingly push surcharges or shorten pricing windows. GWM’s scale secures some concessions, but material exposure remains significant.

Tooling, molds, and specialized parts create switching costs

Platform-specific tooling, Tier-1 ADAS sensors and infotainment modules require lengthy requalification and regulatory validation, increasing switching costs and locking Great Wall Motor into niche suppliers; in 2024 requalification timelines and homologation demands intensified this lock-in. Co-development can rebalance bargaining power but deepens dependence.

- Platform tooling: high requalification burden

- ADAS/infotainment: niche supplier leverage

- Regulatory validation: increases lock-in

- Co-development: mitigates cost but raises dependence

Logistics and geopolitical risks lift supplier influence

Trade frictions, export controls—notably US restrictions on advanced semiconductors and some battery materials in 2023–2024—and shipping disruptions have narrowed Great Wall Motor's supplier options. Suppliers assuring continuity command better terms and allocation. Localizing key inputs boosts resilience but requires multi-year capital; diversified sourcing mitigates risk but is imperfect.

- Export controls 2023–24: higher supplier leverage

- Localizing: multi-year, capital-intensive

- Diversified sourcing: reduces but does not eliminate shocks

Powertrain integration limits supplier power; batteries, chips and materials raise upstream risk

GWM's vertical integration in engines/transmissions limits supplier power, but 2024 reliance on external battery cells (CATL+LGES ~50% global EV cell capacity) and key semiconductors raises supplier leverage. Long qualification cycles for ADAS/infotainment and platform tooling increase switching costs. 2024 prices—HRC steel ~4,200 RMB/t, LME Al ~2,300 USD/t, Li2CO3 ~25,000 USD/t—shift power upstream; trade controls 2023–24 further constrain options; GWM scale offsets but does not eliminate risk.

| Item | 2024 metric | Impact |

|---|---|---|

| Battery concentration | CATL+LGES ~50% | High |

| Chips | NXP/Infineon/Renesas dominant | High |

| Materials | Steel 4,200 RMB/t; Al 2,300 USD/t; Li2CO3 25,000 USD/t | Medium-High |

| Tooling/ADAS | Long requalification | High |

What is included in the product

Provides a concise Porter’s Five Forces assessment of Great Wall Motor, revealing competitive intensity, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect margins and market share.

One-sheet Porter’s Five Forces for Great Wall Motor—quickly visualize supplier/buyer power, rivalry, substitutes, and entrants to ease strategic decisions and update pressure levels as market data evolves.

Customers Bargaining Power

Price-sensitive mass-market segments

Great Wall Motor faces strong buyer power in price-sensitive SUV and pickup segments where consumers compare price-performance and can switch brands with low switching costs, increasing price pressure. Discounts and competitive financing—frequently used in 2024 sales campaigns—materially sway purchase decisions. This dynamic amplifies bargaining power, forcing GWM to protect margins through scale, model differentiation and targeted incentives.

Abundant alternatives heighten choice

Domestic rivals and international brands offer overlapping models across segments, and in 2024 China remained the world’s largest auto market, intensifying choice pressure on Great Wall Motor. Feature parity in ADAS and connectivity has narrowed technical differentiation, shifting competition to design, price and aftersales. Easy cross-shopping via online platforms increases buyer leverage, forcing faster product cycles. GWM must continuously refresh models to defend share.

Information transparency compresses margins

Online reviews, social media and dealer price disclosures have substantially improved buyer knowledge, compressing dealer margins; IEA reports 14 million electric cars sold globally in 2023, fueling broader TCO comparisons. Widely available ICE vs EV total cost of ownership calculators reduce information asymmetry and raise customer negotiating power. As a result, short-term promotions quickly become table stakes.

Fleet and government tenders negotiate hard

Fleet and government tenders negotiate hard: large-volume buyers extract bulk discounts and service guarantees, push specs, delivery windows and tougher warranty terms, and can sway bids given GWM’s 2024 global deliveries of about 1.5 million vehicles. Losing a single major tender can reduce plant utilization and raise per-unit costs; GWM’s broad product lineup helps win bids but compresses margins.

- Volume leverage: bulk discounts demanded

- Contract terms: stricter specs, delivery, warranties

- Capacity risk: single tender loss hits utilization

- Competitive bids: breadth aids wins but trims margins

After-sales ecosystem shapes switching costs

After-sales ecosystem — service coverage, parts availability and timely software updates — directly shapes loyalty for Great Wall Motor by raising or lowering switching frictions; strong dealer and service networks reduce buyer power by increasing retention, while gaps in after-sales or weak residual values amplify it. Warranty terms and trade-in programs act as key levers to mitigate customer bargaining power.

- Service coverage: affects loyalty

- Parts availability: reduces switching

- Software updates: sustain value

- Warranty/trade-in: strategic levers

Buyers wield pricing power as heavy 2024 discounts and EV TCO comparisons squeeze SUV/pickup margins

Buyers hold strong price leverage in GWM’s SUV/pickup segments, with low switching costs and heavy 2024 discounting pressuring margins. China remained the world’s largest auto market in 2024, intensifying cross-shop pressure; GWM reported ~1.5 million global deliveries in 2024. Improved buyer information and 2023 global EV sales of 14 million raise TCO comparisons and negotiation power.

| Metric | Value |

|---|---|

| GWM deliveries (2024) | ~1.5 million |

| China market (2024) | World’s largest |

| Global EV sales (2023) | 14 million |

Preview the Actual Deliverable

Great Wall Motor Porter's Five Forces Analysis

This preview shows the exact Great Wall Motor Porter’s Five Forces analysis you'll receive—no placeholders or samples. The document is fully formatted, professionally written, and ready for download immediately after purchase. What you see here is the deliverable you’ll get, complete and usable for decision-making.