Great Wall Motor PESTLE Analysis

Your Competitive Advantage Starts with This Report

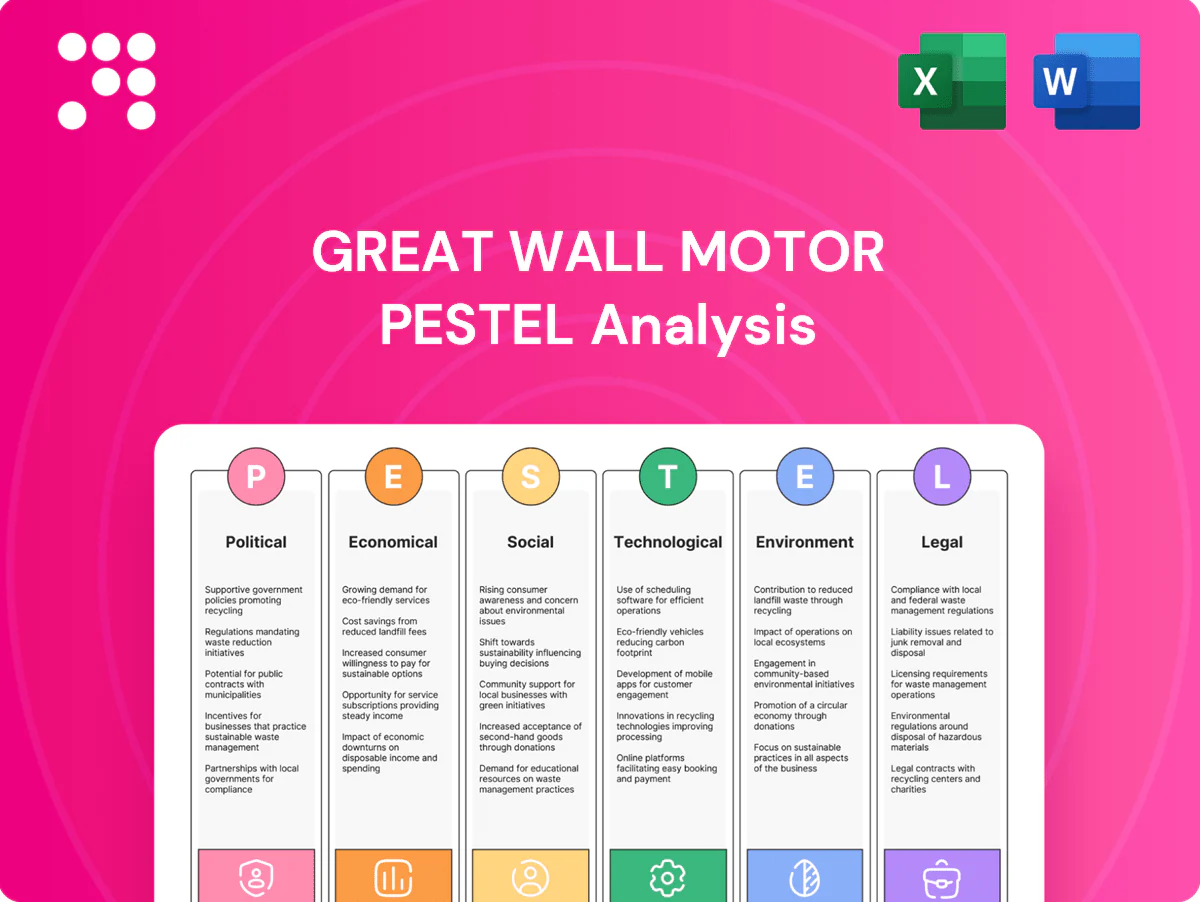

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures are reshaping Great Wall Motor’s competitive landscape in our concise PESTLE snapshot. Designed for investors, strategists, and analysts, this briefing highlights key external risks and opportunities you can act on quickly. Purchase the full PESTLE analysis to access deep-dive insights, data tables, and ready-to-use recommendations.

Political factors

China industrial policy and EV incentives

China's strong industrial policy — central and local subsidies, purchase‑tax breaks and preferential green plates — shapes Great Wall Motor’s Ora roadmap; China recorded about 10.6 million NEV sales in 2023, underpinning demand. Access to pilot zones and green‑plate policies accelerates Ora uptake, while any sudden rollback of incentives would force GWM to cut prices or absorb margin pressure.

Geopolitical tensions and export barriers

Trade frictions can trigger tariffs, anti-subsidy probes or quotas on Chinese autos, as seen when the EU opened an anti-subsidy investigation into Chinese electric cars in June 2023. This threatens pricing power for Haval, Tank and Poer in Europe, Australia and emerging markets. Diplomatic ties now materially affect homologation timelines and market access. Diversifying export destinations and localizing assembly in over 60 markets mitigates tariff and quota risk.

Localization and content rules in target markets

Host countries often impose local content or joint venture rules, with content thresholds commonly ranging from 30% to 60%, and meeting them can unlock tax incentives, tariff relief and preferential access to public procurement. GWM’s in-house component manufacturing and modular EV platforms help satisfy local content tests and shorten qualification timelines. Active local supplier development also lowers political pushback and strengthens bids for government fleet contracts.

Government procurement and fleet policies

Public-sector EV mandates—China's procurement push and rising NEV adoption (NEV share ~34% in 2024)—open fleet sales for Great Wall's pickups and SUVs, provided models meet mandatory safety and emissions standards.

Preferential treatment for domestic producers in China and some emerging markets can be leveraged; transparent bidding and adherence to procurement rules reduce political exposure and disqualification risk.

- NEV share ~34% (China, 2024)

- Compliance: safety & emissions mandatory

- Preferential procurement in China/emerging markets

- Transparent bidding lowers political risk

Infrastructure and energy strategy

National charging and grid plans directly pace EV adoption; IEA reports electric cars were 14% of global car sales in 2023, with China accounting for roughly 60% of that demand, shaping Great Wall Motor’s rollout timing.

- Charging rollout pace influences model launch timing

- Hydrogen/alt-fuel policy can redirect R&D budgets

- Regional infrastructure gaps change provincial model mix

- Utility partnerships raise rollout certainty

China NEV surge and EU probe push tariff-risk localization in 60+ markets

China's industrial policy (10.6M NEVs in 2023; NEV share ~34% in China 2024) supports Ora but incentive rollback would compress margins. EU anti‑subsidy probe (June 2023) and tariff risk threaten export pricing, so localization across 60+ markets is strategic. Local content rules (30–60%) and national charging plans directly dictate launch timing and procurement access.

| Metric | Value |

|---|---|

| China NEV sales 2023 | 10.6M |

| China NEV share 2024 | ~34% |

| EU probe | Anti‑subsidy Jun 2023 |

| Markets with local presence | 60+ |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely shape Great Wall Motor’s strategy and operations, using current market, regulatory and EV-transition data to identify risks and opportunities. Designed for executives and investors, it offers actionable, forward‑looking insights for scenario planning.

A concise PESTLE summary of Great Wall Motor that relieves research pain by distilling regulatory, economic, social, technological, environmental, and legal risks into a single-page reference—ready to drop into presentations, share across teams, and annotate for local market actions.

Economic factors

Cyclical demand and consumer confidence

Auto sales closely follow GDP and employment; China’s GDP grew 5.2% in 2023, linking macro swings to vehicle demand and consumer confidence. Slowdowns typically compress volumes for discretionary SUVs, pressuring margins on higher-end models. Great Wall Motor’s multi-brand pricing ladder helps buffer mix risk across segments. Targeted incentives and flexible financing offers have historically smoothed cyclical dips in volume.

Currency volatility and export competitiveness

FX swings (USD/CNY moved roughly between 6.2–7.4 since 2020) affect GWM overseas pricing and repatriated profits; RMB weakness boosts export price competitiveness but raises imported component costs. GWM mitigates with hedging programs and local sourcing — overseas procurement rose notably in recent years — while price‑indexed contracts help stabilize margins.

Commodity prices: steel, lithium, nickel

Rising input prices—steel ~USD 600/ton, lithium carbonate ~USD 25,000/ton, nickel ~USD 20,000/ton—directly lift COGS across GWM’s ICE and EV lines. Volatility in battery metals hits Ora and hybrid margins through battery pack costs and warranty exposures. Long-term supply contracts and vertical partnerships with battery/mining firms improve cost predictability. Design-to-cost and flexible battery chemistry choices preserve margin resilience.

Interest rates and auto financing

Higher policy rates raise borrowing costs and dampen affordability and lease penetration; China LPR stood at 3.45% (1yr) and 3.95% (5yr) mid‑2024, making subvention schemes costlier and squeezing margins for GWM. Captive or partner financing becomes strategic to preserve sales; weaker credit screening elevates default risk and resale-value pressure.

- Interest rates: China LPR 1yr 3.45%, 5yr 3.95%

- Effect: lower affordability, reduced lease penetration

- Strategy: captive/partner finance to support demand

- Risk: higher subvention costs, credit quality drives defaults

Scale economies and manufacturing utilization

High plant utilization across Haval, Tank and Wey lowers per-unit manufacturing costs by spreading fixed expenses over larger volumes, supported by platform sharing and common components that standardize supply chains and reduce BOM complexity.

Export volumes help absorb fixed costs and smooth seasonality, while flexible production lines let GWM switch models quickly to mitigate regional demand shocks and optimize capacity use.

- Scale benefits: platform sharing across brands

- Utilization: higher output cuts unit costs

- Exports: absorb fixed costs and seasonality

- Flexible lines: rapid model switches reduce risk

China NEV surge and EU probe push tariff-risk localization in 60+ markets

China GDP 5.2% (2023) ties auto demand to macro cycles; FX (USD/CNY 6.2–7.4 since 2020) shifts export competitiveness vs input costs; steel ~USD600/t, lithium ~USD25,000/t, nickel ~USD20,000/t lift COGS; China LPR 1yr 3.45% / 5yr 3.95% raises financing costs and subvention pressure.

| Metric | Value |

|---|---|

| China GDP (2023) | 5.2% |

| USD/CNY (2020–) | 6.2–7.4 |

| Steel | ~USD600/ton |

| Lithium carbonate | ~USD25,000/ton |

| Nickel | ~USD20,000/ton |

| China LPR (mid‑2024) | 1yr 3.45% / 5yr 3.95% |

Preview the Actual Deliverable

Great Wall Motor PESTLE Analysis

This Great Wall Motor PESTLE Analysis preview is the exact document you’ll receive after purchase — fully formatted, professionally structured, and ready to use. It contains complete political, economic, social, technological, legal, and environmental insights as shown. No placeholders or surprises; download the same file immediately after checkout.

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures are reshaping Great Wall Motor’s competitive landscape in our concise PESTLE snapshot. Designed for investors, strategists, and analysts, this briefing highlights key external risks and opportunities you can act on quickly. Purchase the full PESTLE analysis to access deep-dive insights, data tables, and ready-to-use recommendations.

Political factors

China industrial policy and EV incentives

China's strong industrial policy — central and local subsidies, purchase‑tax breaks and preferential green plates — shapes Great Wall Motor’s Ora roadmap; China recorded about 10.6 million NEV sales in 2023, underpinning demand. Access to pilot zones and green‑plate policies accelerates Ora uptake, while any sudden rollback of incentives would force GWM to cut prices or absorb margin pressure.

Geopolitical tensions and export barriers

Trade frictions can trigger tariffs, anti-subsidy probes or quotas on Chinese autos, as seen when the EU opened an anti-subsidy investigation into Chinese electric cars in June 2023. This threatens pricing power for Haval, Tank and Poer in Europe, Australia and emerging markets. Diplomatic ties now materially affect homologation timelines and market access. Diversifying export destinations and localizing assembly in over 60 markets mitigates tariff and quota risk.

Localization and content rules in target markets

Host countries often impose local content or joint venture rules, with content thresholds commonly ranging from 30% to 60%, and meeting them can unlock tax incentives, tariff relief and preferential access to public procurement. GWM’s in-house component manufacturing and modular EV platforms help satisfy local content tests and shorten qualification timelines. Active local supplier development also lowers political pushback and strengthens bids for government fleet contracts.

Government procurement and fleet policies

Public-sector EV mandates—China's procurement push and rising NEV adoption (NEV share ~34% in 2024)—open fleet sales for Great Wall's pickups and SUVs, provided models meet mandatory safety and emissions standards.

Preferential treatment for domestic producers in China and some emerging markets can be leveraged; transparent bidding and adherence to procurement rules reduce political exposure and disqualification risk.

- NEV share ~34% (China, 2024)

- Compliance: safety & emissions mandatory

- Preferential procurement in China/emerging markets

- Transparent bidding lowers political risk

Infrastructure and energy strategy

National charging and grid plans directly pace EV adoption; IEA reports electric cars were 14% of global car sales in 2023, with China accounting for roughly 60% of that demand, shaping Great Wall Motor’s rollout timing.

- Charging rollout pace influences model launch timing

- Hydrogen/alt-fuel policy can redirect R&D budgets

- Regional infrastructure gaps change provincial model mix

- Utility partnerships raise rollout certainty

China NEV surge and EU probe push tariff-risk localization in 60+ markets

China's industrial policy (10.6M NEVs in 2023; NEV share ~34% in China 2024) supports Ora but incentive rollback would compress margins. EU anti‑subsidy probe (June 2023) and tariff risk threaten export pricing, so localization across 60+ markets is strategic. Local content rules (30–60%) and national charging plans directly dictate launch timing and procurement access.

| Metric | Value |

|---|---|

| China NEV sales 2023 | 10.6M |

| China NEV share 2024 | ~34% |

| EU probe | Anti‑subsidy Jun 2023 |

| Markets with local presence | 60+ |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely shape Great Wall Motor’s strategy and operations, using current market, regulatory and EV-transition data to identify risks and opportunities. Designed for executives and investors, it offers actionable, forward‑looking insights for scenario planning.

A concise PESTLE summary of Great Wall Motor that relieves research pain by distilling regulatory, economic, social, technological, environmental, and legal risks into a single-page reference—ready to drop into presentations, share across teams, and annotate for local market actions.

Economic factors

Cyclical demand and consumer confidence

Auto sales closely follow GDP and employment; China’s GDP grew 5.2% in 2023, linking macro swings to vehicle demand and consumer confidence. Slowdowns typically compress volumes for discretionary SUVs, pressuring margins on higher-end models. Great Wall Motor’s multi-brand pricing ladder helps buffer mix risk across segments. Targeted incentives and flexible financing offers have historically smoothed cyclical dips in volume.

Currency volatility and export competitiveness

FX swings (USD/CNY moved roughly between 6.2–7.4 since 2020) affect GWM overseas pricing and repatriated profits; RMB weakness boosts export price competitiveness but raises imported component costs. GWM mitigates with hedging programs and local sourcing — overseas procurement rose notably in recent years — while price‑indexed contracts help stabilize margins.

Commodity prices: steel, lithium, nickel

Rising input prices—steel ~USD 600/ton, lithium carbonate ~USD 25,000/ton, nickel ~USD 20,000/ton—directly lift COGS across GWM’s ICE and EV lines. Volatility in battery metals hits Ora and hybrid margins through battery pack costs and warranty exposures. Long-term supply contracts and vertical partnerships with battery/mining firms improve cost predictability. Design-to-cost and flexible battery chemistry choices preserve margin resilience.

Interest rates and auto financing

Higher policy rates raise borrowing costs and dampen affordability and lease penetration; China LPR stood at 3.45% (1yr) and 3.95% (5yr) mid‑2024, making subvention schemes costlier and squeezing margins for GWM. Captive or partner financing becomes strategic to preserve sales; weaker credit screening elevates default risk and resale-value pressure.

- Interest rates: China LPR 1yr 3.45%, 5yr 3.95%

- Effect: lower affordability, reduced lease penetration

- Strategy: captive/partner finance to support demand

- Risk: higher subvention costs, credit quality drives defaults

Scale economies and manufacturing utilization

High plant utilization across Haval, Tank and Wey lowers per-unit manufacturing costs by spreading fixed expenses over larger volumes, supported by platform sharing and common components that standardize supply chains and reduce BOM complexity.

Export volumes help absorb fixed costs and smooth seasonality, while flexible production lines let GWM switch models quickly to mitigate regional demand shocks and optimize capacity use.

- Scale benefits: platform sharing across brands

- Utilization: higher output cuts unit costs

- Exports: absorb fixed costs and seasonality

- Flexible lines: rapid model switches reduce risk

China NEV surge and EU probe push tariff-risk localization in 60+ markets

China GDP 5.2% (2023) ties auto demand to macro cycles; FX (USD/CNY 6.2–7.4 since 2020) shifts export competitiveness vs input costs; steel ~USD600/t, lithium ~USD25,000/t, nickel ~USD20,000/t lift COGS; China LPR 1yr 3.45% / 5yr 3.95% raises financing costs and subvention pressure.

| Metric | Value |

|---|---|

| China GDP (2023) | 5.2% |

| USD/CNY (2020–) | 6.2–7.4 |

| Steel | ~USD600/ton |

| Lithium carbonate | ~USD25,000/ton |

| Nickel | ~USD20,000/ton |

| China LPR (mid‑2024) | 1yr 3.45% / 5yr 3.95% |

Preview the Actual Deliverable

Great Wall Motor PESTLE Analysis

This Great Wall Motor PESTLE Analysis preview is the exact document you’ll receive after purchase — fully formatted, professionally structured, and ready to use. It contains complete political, economic, social, technological, legal, and environmental insights as shown. No placeholders or surprises; download the same file immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures are reshaping Great Wall Motor’s competitive landscape in our concise PESTLE snapshot. Designed for investors, strategists, and analysts, this briefing highlights key external risks and opportunities you can act on quickly. Purchase the full PESTLE analysis to access deep-dive insights, data tables, and ready-to-use recommendations.

Political factors

China industrial policy and EV incentives

China's strong industrial policy — central and local subsidies, purchase‑tax breaks and preferential green plates — shapes Great Wall Motor’s Ora roadmap; China recorded about 10.6 million NEV sales in 2023, underpinning demand. Access to pilot zones and green‑plate policies accelerates Ora uptake, while any sudden rollback of incentives would force GWM to cut prices or absorb margin pressure.

Geopolitical tensions and export barriers

Trade frictions can trigger tariffs, anti-subsidy probes or quotas on Chinese autos, as seen when the EU opened an anti-subsidy investigation into Chinese electric cars in June 2023. This threatens pricing power for Haval, Tank and Poer in Europe, Australia and emerging markets. Diplomatic ties now materially affect homologation timelines and market access. Diversifying export destinations and localizing assembly in over 60 markets mitigates tariff and quota risk.

Localization and content rules in target markets

Host countries often impose local content or joint venture rules, with content thresholds commonly ranging from 30% to 60%, and meeting them can unlock tax incentives, tariff relief and preferential access to public procurement. GWM’s in-house component manufacturing and modular EV platforms help satisfy local content tests and shorten qualification timelines. Active local supplier development also lowers political pushback and strengthens bids for government fleet contracts.

Government procurement and fleet policies

Public-sector EV mandates—China's procurement push and rising NEV adoption (NEV share ~34% in 2024)—open fleet sales for Great Wall's pickups and SUVs, provided models meet mandatory safety and emissions standards.

Preferential treatment for domestic producers in China and some emerging markets can be leveraged; transparent bidding and adherence to procurement rules reduce political exposure and disqualification risk.

- NEV share ~34% (China, 2024)

- Compliance: safety & emissions mandatory

- Preferential procurement in China/emerging markets

- Transparent bidding lowers political risk

Infrastructure and energy strategy

National charging and grid plans directly pace EV adoption; IEA reports electric cars were 14% of global car sales in 2023, with China accounting for roughly 60% of that demand, shaping Great Wall Motor’s rollout timing.

- Charging rollout pace influences model launch timing

- Hydrogen/alt-fuel policy can redirect R&D budgets

- Regional infrastructure gaps change provincial model mix

- Utility partnerships raise rollout certainty

China NEV surge and EU probe push tariff-risk localization in 60+ markets

China's industrial policy (10.6M NEVs in 2023; NEV share ~34% in China 2024) supports Ora but incentive rollback would compress margins. EU anti‑subsidy probe (June 2023) and tariff risk threaten export pricing, so localization across 60+ markets is strategic. Local content rules (30–60%) and national charging plans directly dictate launch timing and procurement access.

| Metric | Value |

|---|---|

| China NEV sales 2023 | 10.6M |

| China NEV share 2024 | ~34% |

| EU probe | Anti‑subsidy Jun 2023 |

| Markets with local presence | 60+ |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely shape Great Wall Motor’s strategy and operations, using current market, regulatory and EV-transition data to identify risks and opportunities. Designed for executives and investors, it offers actionable, forward‑looking insights for scenario planning.

A concise PESTLE summary of Great Wall Motor that relieves research pain by distilling regulatory, economic, social, technological, environmental, and legal risks into a single-page reference—ready to drop into presentations, share across teams, and annotate for local market actions.

Economic factors

Cyclical demand and consumer confidence

Auto sales closely follow GDP and employment; China’s GDP grew 5.2% in 2023, linking macro swings to vehicle demand and consumer confidence. Slowdowns typically compress volumes for discretionary SUVs, pressuring margins on higher-end models. Great Wall Motor’s multi-brand pricing ladder helps buffer mix risk across segments. Targeted incentives and flexible financing offers have historically smoothed cyclical dips in volume.

Currency volatility and export competitiveness

FX swings (USD/CNY moved roughly between 6.2–7.4 since 2020) affect GWM overseas pricing and repatriated profits; RMB weakness boosts export price competitiveness but raises imported component costs. GWM mitigates with hedging programs and local sourcing — overseas procurement rose notably in recent years — while price‑indexed contracts help stabilize margins.

Commodity prices: steel, lithium, nickel

Rising input prices—steel ~USD 600/ton, lithium carbonate ~USD 25,000/ton, nickel ~USD 20,000/ton—directly lift COGS across GWM’s ICE and EV lines. Volatility in battery metals hits Ora and hybrid margins through battery pack costs and warranty exposures. Long-term supply contracts and vertical partnerships with battery/mining firms improve cost predictability. Design-to-cost and flexible battery chemistry choices preserve margin resilience.

Interest rates and auto financing

Higher policy rates raise borrowing costs and dampen affordability and lease penetration; China LPR stood at 3.45% (1yr) and 3.95% (5yr) mid‑2024, making subvention schemes costlier and squeezing margins for GWM. Captive or partner financing becomes strategic to preserve sales; weaker credit screening elevates default risk and resale-value pressure.

- Interest rates: China LPR 1yr 3.45%, 5yr 3.95%

- Effect: lower affordability, reduced lease penetration

- Strategy: captive/partner finance to support demand

- Risk: higher subvention costs, credit quality drives defaults

Scale economies and manufacturing utilization

High plant utilization across Haval, Tank and Wey lowers per-unit manufacturing costs by spreading fixed expenses over larger volumes, supported by platform sharing and common components that standardize supply chains and reduce BOM complexity.

Export volumes help absorb fixed costs and smooth seasonality, while flexible production lines let GWM switch models quickly to mitigate regional demand shocks and optimize capacity use.

- Scale benefits: platform sharing across brands

- Utilization: higher output cuts unit costs

- Exports: absorb fixed costs and seasonality

- Flexible lines: rapid model switches reduce risk

China NEV surge and EU probe push tariff-risk localization in 60+ markets

China GDP 5.2% (2023) ties auto demand to macro cycles; FX (USD/CNY 6.2–7.4 since 2020) shifts export competitiveness vs input costs; steel ~USD600/t, lithium ~USD25,000/t, nickel ~USD20,000/t lift COGS; China LPR 1yr 3.45% / 5yr 3.95% raises financing costs and subvention pressure.

| Metric | Value |

|---|---|

| China GDP (2023) | 5.2% |

| USD/CNY (2020–) | 6.2–7.4 |

| Steel | ~USD600/ton |

| Lithium carbonate | ~USD25,000/ton |

| Nickel | ~USD20,000/ton |

| China LPR (mid‑2024) | 1yr 3.45% / 5yr 3.95% |

Preview the Actual Deliverable

Great Wall Motor PESTLE Analysis

This Great Wall Motor PESTLE Analysis preview is the exact document you’ll receive after purchase — fully formatted, professionally structured, and ready to use. It contains complete political, economic, social, technological, legal, and environmental insights as shown. No placeholders or surprises; download the same file immediately after checkout.