Dr. Haas GmbH PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive edge with our PESTLE Analysis of Dr. Haas GmbH—concise, expertly researched, and focused on the external forces shaping the company's future. Understand regulatory, economic, social, and technological risks and opportunities that matter. Ideal for investors, strategists, and consultants. Purchase the full report to access the complete, actionable breakdown instantly.

Political factors

EU policy on digital single market

EU digital single market rules, led by the Digital Markets Act and Digital Services Act (in force since 2022), push cross-border access and interoperability, expanding addressable markets to ~447 million EU consumers. Harmonized rules can open pan‑EU distribution for professional publications but compliance often requires format and metadata upgrades. The DMA designated ~22 gatekeepers, shifting platform bargaining power and revenue shares.

Public sector demand for fiscal/legal updates

Government reforms in taxation, audit oversight and justice—exemplified by 140+ jurisdictions committing to the OECD Pillar Two minimum tax and Germany’s ~30–33% combined corporate tax burden—drive steady demand for authoritative commentary. Frequent policy revisions create clear spikes in practitioner information needs as lawmakers update rules. Timely, live coverage strengthens brand relevance; delays risk obsolescence and lost renewals.

Funding and support for SME digitization

National and EU programs such as the EU Digital Europe Programme (budget €7.5 billion 2021–2027) and NextGenerationEU recovery funds (approx €750 billion) provide grants and tax-backed incentives that can lower capex for platforms, AI and cybersecurity for publishers. Complex application procedures and compliance requirements often deter SMEs without dedicated resources. Competitors that secure subsidies can accelerate digital capabilities and market positioning.

Geopolitical stability and paper supply

Political tensions drive energy costs and pulp imports, squeezing print margins: European TTF gas plunged from peaks near €330/MWh in 2022 to around €60/MWh in 2024 but remains volatility-prone, while NBSK pulp fell from ~$1,100/t in 2022 to ~ $700/t in 2024, affecting input costs and lead times. Sanctions or trade barriers can halt shipments, so contingency sourcing and local printing reduce exposure, and policy energy relief (subsidies/tax breaks) has capped some spikes.

- Energy volatility — TTF swing €330→€60/MWh (2022→2024)

- Pulp price shift — NBSK ~$1,100→~$700/t (2022→2024)

- Mitigation — contingency sourcing, nearshoring, local print

- Policy cushion — subsidies/tax relief limit cost spikes

Regulatory lobbying and professional bodies

Regulatory lobbying by bar associations and chambers shapes legal publishing standards and acceptance; the German Bar Association (DAV) represents about 160,000 lawyers (2024), making alignment key for credibility and adoption. Political debates over self-regulation shift citation preferences, so partnerships with these bodies can secure official distribution channels and revenue streams.

- Align with DAV and chambers

- Target citation influence

- Secure official distribution

DMA/DSA open ~447m market; ~22 gatekeepers boost compliance

EU DMA/DSA expand a ~447m cross‑border market and name ~22 gatekeepers, raising compliance costs but opening pan‑EU reach. Tax/audit reforms (OECD Pillar Two; DE combined tax ~30–33%) keep demand for authoritative legal content high. Energy/pulp volatility (TTF ~€60/MWh; NBSK ~$700/t) and DAV (~160,000 lawyers) shape distribution and credibility strategies.

| Item | 2024/25 |

|---|---|

| EU consumers | ~447m |

| Gatekeepers | ~22 |

| Digital Europe | €7.5bn |

| NextGenEU | €750bn |

| Germany tax | 30–33% |

| DAV lawyers | ~160,000 |

| TTF gas | ~€60/MWh |

| NBSK pulp | ~$700/t |

What is included in the product

Explores how macro-environmental factors uniquely affect Dr. Haas GmbH across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants and investors identify risks, opportunities and strategic responses aligned to regional market and regulatory dynamics.

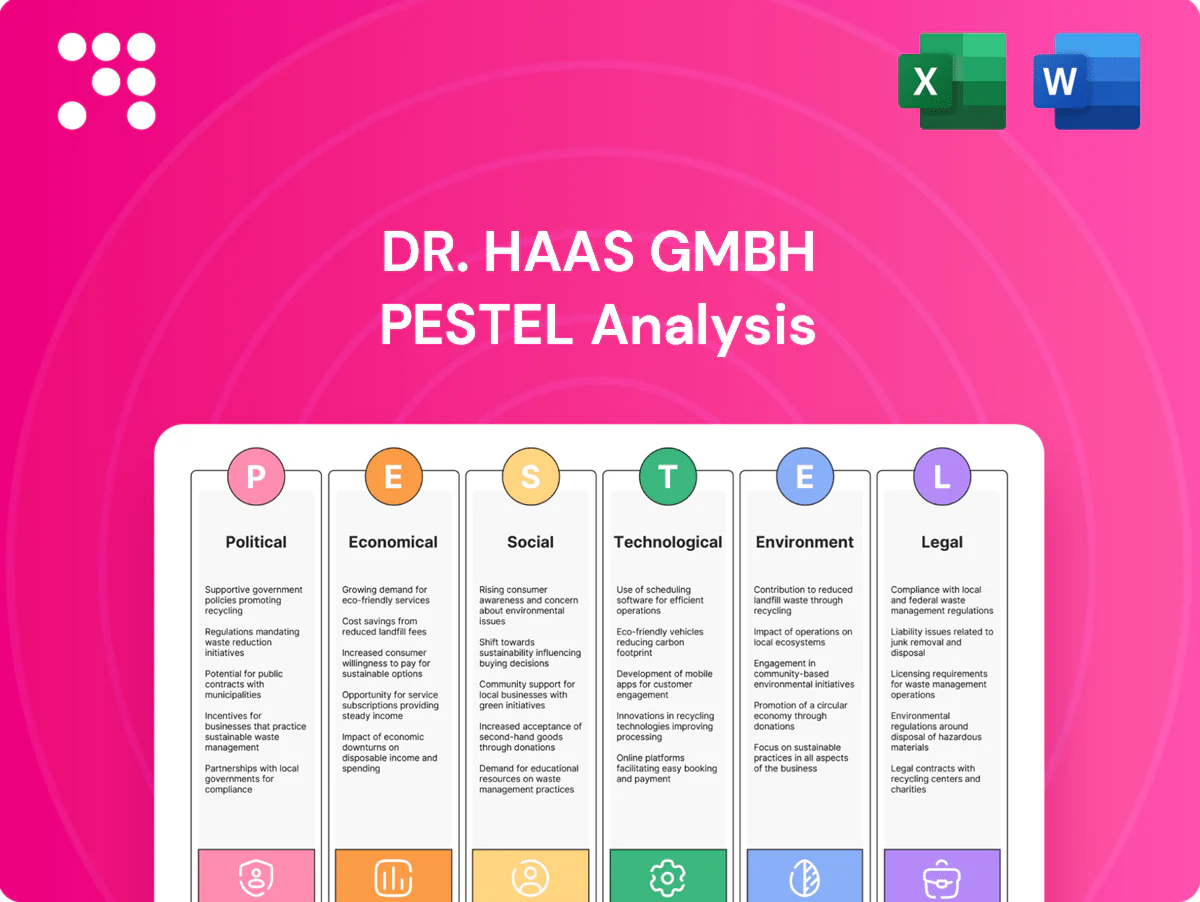

Visually segmented by PESTEL categories, the Dr. Haas GmbH PESTLE Analysis delivers a clean, shareable summary that’s easy to drop into presentations, edit with region- or business-specific notes, and use in planning sessions to streamline external risk discussion and team alignment.

Economic factors

Subscription budgets of professional firms

Economic cycles shape subscription budgets for law and tax firms: IMF projected global GDP growth of 3.1% in 2024, but sectoral volatility persists, and Thomson Reuters reported global legal demand growth of just 2.7% in 2023, prompting firms to consolidate vendors, favor tiered pricing and bundles, and require demonstrable productivity gains to defend renewals.

Inflation and input cost pressures

Rising costs in printing, logistics and tech talent squeezed Dr. Haas GmbH margins as euro area HICP eased to about 2.4% in 2024 but sector-specific inputs remained elevated, with paper/ink up roughly 8–12% versus 2019 and freight rates above pre‑pandemic norms. Price indexation clauses enable partial pass‑through, yet customers resist hikes without added value. Automation and RPA implementations can lower unit costs by an estimated 10–20%, offsetting some pressure.

Digital adoption and recurring revenue mix

Shift from print to digital raises gross margins (SaaS-style gross margins typically 70–90%) and makes cash flow more predictable as recurring revenue rises; firms with >50% recurring mix report materially lower revenue volatility. Transition risk includes churn if digital feature parity lags, with typical churn benchmarks 5–10% annually. Cross-selling databases, workflows and updates boosts ARPU. Phased 12–36 month migration plans smooth revenue volatility.

Consolidation among professional services

Consolidation in legal and tax advisory concentrates purchasing power, forcing vendors to add enterprise features and steeper volume discounts as the legaltech market is projected to reach USD 25.17 billion by 2026. Large accounts increasingly demand integrated licensing and SLAs, while smaller practitioners require low‑cost self‑serve options to remain viable. Dr. Haas GmbH should run dual go‑to‑market tracks to balance volume and margin.

- Concentration: fewer buyers, higher negotiation leverage

- Enterprise demand: integrated features + discounting pressure

- SME need: affordable self‑serve products

- Strategy: dual GTM for volume (self‑serve) and margin (enterprise)

Currency exposure on content licensing

International rights, data feeds and software tools are often invoiced in USD, EUR or GBP, and 2024 saw EUR/USD average about 1.08, producing low-single-digit percentage swings in content COGS that compressed margins for media licensors. Matching foreign-currency revenues provides natural hedging to offset these cost moves. Using forward contracts and FX swaps is common to stabilize budgeting and protect margins.

- FX invoicing: USD/EUR/GBP exposure

- 2024 EUR/USD avg ~1.08 — low-single-digit COGS variability

- Natural hedging: match revenues to costs

- Forward contracts: budget stability

DMA/DSA open ~447m market; ~22 gatekeepers boost compliance

Economic cycles capped law/tax subscription growth (IMF 2024 GDP 3.1%; legal demand +2.7% in 2023), pressuring renewals and favoring tiered pricing. Input inflation hit margins (EA HICP ~2.4% 2024; paper/ink +8–12% vs 2019; freight elevated); automation can cut unit costs 10–20%. Digital mix raises gross margins (SaaS 70–90%); churn 5–10% risks during migration. FX (EUR/USD ~1.08 in 2024) causes low‑single‑digit COGS swings.

| Metric | Value |

|---|---|

| IMF global GDP 2024 | 3.1% |

| Legal demand 2023 | +2.7% |

| EA HICP 2024 | ~2.4% |

| Paper/ink vs 2019 | +8–12% |

| Automation cost save | 10–20% |

| EUR/USD 2024 avg | ~1.08 |

Same Document Delivered

Dr. Haas GmbH PESTLE Analysis

The preview shown here is the exact Dr. Haas GmbH PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It includes political, economic, social, technological, legal and environmental assessments plus actionable insights. No placeholders, no surprises; download the final file immediately after checkout.

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive edge with our PESTLE Analysis of Dr. Haas GmbH—concise, expertly researched, and focused on the external forces shaping the company's future. Understand regulatory, economic, social, and technological risks and opportunities that matter. Ideal for investors, strategists, and consultants. Purchase the full report to access the complete, actionable breakdown instantly.

Political factors

EU policy on digital single market

EU digital single market rules, led by the Digital Markets Act and Digital Services Act (in force since 2022), push cross-border access and interoperability, expanding addressable markets to ~447 million EU consumers. Harmonized rules can open pan‑EU distribution for professional publications but compliance often requires format and metadata upgrades. The DMA designated ~22 gatekeepers, shifting platform bargaining power and revenue shares.

Public sector demand for fiscal/legal updates

Government reforms in taxation, audit oversight and justice—exemplified by 140+ jurisdictions committing to the OECD Pillar Two minimum tax and Germany’s ~30–33% combined corporate tax burden—drive steady demand for authoritative commentary. Frequent policy revisions create clear spikes in practitioner information needs as lawmakers update rules. Timely, live coverage strengthens brand relevance; delays risk obsolescence and lost renewals.

Funding and support for SME digitization

National and EU programs such as the EU Digital Europe Programme (budget €7.5 billion 2021–2027) and NextGenerationEU recovery funds (approx €750 billion) provide grants and tax-backed incentives that can lower capex for platforms, AI and cybersecurity for publishers. Complex application procedures and compliance requirements often deter SMEs without dedicated resources. Competitors that secure subsidies can accelerate digital capabilities and market positioning.

Geopolitical stability and paper supply

Political tensions drive energy costs and pulp imports, squeezing print margins: European TTF gas plunged from peaks near €330/MWh in 2022 to around €60/MWh in 2024 but remains volatility-prone, while NBSK pulp fell from ~$1,100/t in 2022 to ~ $700/t in 2024, affecting input costs and lead times. Sanctions or trade barriers can halt shipments, so contingency sourcing and local printing reduce exposure, and policy energy relief (subsidies/tax breaks) has capped some spikes.

- Energy volatility — TTF swing €330→€60/MWh (2022→2024)

- Pulp price shift — NBSK ~$1,100→~$700/t (2022→2024)

- Mitigation — contingency sourcing, nearshoring, local print

- Policy cushion — subsidies/tax relief limit cost spikes

Regulatory lobbying and professional bodies

Regulatory lobbying by bar associations and chambers shapes legal publishing standards and acceptance; the German Bar Association (DAV) represents about 160,000 lawyers (2024), making alignment key for credibility and adoption. Political debates over self-regulation shift citation preferences, so partnerships with these bodies can secure official distribution channels and revenue streams.

- Align with DAV and chambers

- Target citation influence

- Secure official distribution

DMA/DSA open ~447m market; ~22 gatekeepers boost compliance

EU DMA/DSA expand a ~447m cross‑border market and name ~22 gatekeepers, raising compliance costs but opening pan‑EU reach. Tax/audit reforms (OECD Pillar Two; DE combined tax ~30–33%) keep demand for authoritative legal content high. Energy/pulp volatility (TTF ~€60/MWh; NBSK ~$700/t) and DAV (~160,000 lawyers) shape distribution and credibility strategies.

| Item | 2024/25 |

|---|---|

| EU consumers | ~447m |

| Gatekeepers | ~22 |

| Digital Europe | €7.5bn |

| NextGenEU | €750bn |

| Germany tax | 30–33% |

| DAV lawyers | ~160,000 |

| TTF gas | ~€60/MWh |

| NBSK pulp | ~$700/t |

What is included in the product

Explores how macro-environmental factors uniquely affect Dr. Haas GmbH across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants and investors identify risks, opportunities and strategic responses aligned to regional market and regulatory dynamics.

Visually segmented by PESTEL categories, the Dr. Haas GmbH PESTLE Analysis delivers a clean, shareable summary that’s easy to drop into presentations, edit with region- or business-specific notes, and use in planning sessions to streamline external risk discussion and team alignment.

Economic factors

Subscription budgets of professional firms

Economic cycles shape subscription budgets for law and tax firms: IMF projected global GDP growth of 3.1% in 2024, but sectoral volatility persists, and Thomson Reuters reported global legal demand growth of just 2.7% in 2023, prompting firms to consolidate vendors, favor tiered pricing and bundles, and require demonstrable productivity gains to defend renewals.

Inflation and input cost pressures

Rising costs in printing, logistics and tech talent squeezed Dr. Haas GmbH margins as euro area HICP eased to about 2.4% in 2024 but sector-specific inputs remained elevated, with paper/ink up roughly 8–12% versus 2019 and freight rates above pre‑pandemic norms. Price indexation clauses enable partial pass‑through, yet customers resist hikes without added value. Automation and RPA implementations can lower unit costs by an estimated 10–20%, offsetting some pressure.

Digital adoption and recurring revenue mix

Shift from print to digital raises gross margins (SaaS-style gross margins typically 70–90%) and makes cash flow more predictable as recurring revenue rises; firms with >50% recurring mix report materially lower revenue volatility. Transition risk includes churn if digital feature parity lags, with typical churn benchmarks 5–10% annually. Cross-selling databases, workflows and updates boosts ARPU. Phased 12–36 month migration plans smooth revenue volatility.

Consolidation among professional services

Consolidation in legal and tax advisory concentrates purchasing power, forcing vendors to add enterprise features and steeper volume discounts as the legaltech market is projected to reach USD 25.17 billion by 2026. Large accounts increasingly demand integrated licensing and SLAs, while smaller practitioners require low‑cost self‑serve options to remain viable. Dr. Haas GmbH should run dual go‑to‑market tracks to balance volume and margin.

- Concentration: fewer buyers, higher negotiation leverage

- Enterprise demand: integrated features + discounting pressure

- SME need: affordable self‑serve products

- Strategy: dual GTM for volume (self‑serve) and margin (enterprise)

Currency exposure on content licensing

International rights, data feeds and software tools are often invoiced in USD, EUR or GBP, and 2024 saw EUR/USD average about 1.08, producing low-single-digit percentage swings in content COGS that compressed margins for media licensors. Matching foreign-currency revenues provides natural hedging to offset these cost moves. Using forward contracts and FX swaps is common to stabilize budgeting and protect margins.

- FX invoicing: USD/EUR/GBP exposure

- 2024 EUR/USD avg ~1.08 — low-single-digit COGS variability

- Natural hedging: match revenues to costs

- Forward contracts: budget stability

DMA/DSA open ~447m market; ~22 gatekeepers boost compliance

Economic cycles capped law/tax subscription growth (IMF 2024 GDP 3.1%; legal demand +2.7% in 2023), pressuring renewals and favoring tiered pricing. Input inflation hit margins (EA HICP ~2.4% 2024; paper/ink +8–12% vs 2019; freight elevated); automation can cut unit costs 10–20%. Digital mix raises gross margins (SaaS 70–90%); churn 5–10% risks during migration. FX (EUR/USD ~1.08 in 2024) causes low‑single‑digit COGS swings.

| Metric | Value |

|---|---|

| IMF global GDP 2024 | 3.1% |

| Legal demand 2023 | +2.7% |

| EA HICP 2024 | ~2.4% |

| Paper/ink vs 2019 | +8–12% |

| Automation cost save | 10–20% |

| EUR/USD 2024 avg | ~1.08 |

Same Document Delivered

Dr. Haas GmbH PESTLE Analysis

The preview shown here is the exact Dr. Haas GmbH PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It includes political, economic, social, technological, legal and environmental assessments plus actionable insights. No placeholders, no surprises; download the final file immediately after checkout.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive edge with our PESTLE Analysis of Dr. Haas GmbH—concise, expertly researched, and focused on the external forces shaping the company's future. Understand regulatory, economic, social, and technological risks and opportunities that matter. Ideal for investors, strategists, and consultants. Purchase the full report to access the complete, actionable breakdown instantly.

Political factors

EU policy on digital single market

EU digital single market rules, led by the Digital Markets Act and Digital Services Act (in force since 2022), push cross-border access and interoperability, expanding addressable markets to ~447 million EU consumers. Harmonized rules can open pan‑EU distribution for professional publications but compliance often requires format and metadata upgrades. The DMA designated ~22 gatekeepers, shifting platform bargaining power and revenue shares.

Public sector demand for fiscal/legal updates

Government reforms in taxation, audit oversight and justice—exemplified by 140+ jurisdictions committing to the OECD Pillar Two minimum tax and Germany’s ~30–33% combined corporate tax burden—drive steady demand for authoritative commentary. Frequent policy revisions create clear spikes in practitioner information needs as lawmakers update rules. Timely, live coverage strengthens brand relevance; delays risk obsolescence and lost renewals.

Funding and support for SME digitization

National and EU programs such as the EU Digital Europe Programme (budget €7.5 billion 2021–2027) and NextGenerationEU recovery funds (approx €750 billion) provide grants and tax-backed incentives that can lower capex for platforms, AI and cybersecurity for publishers. Complex application procedures and compliance requirements often deter SMEs without dedicated resources. Competitors that secure subsidies can accelerate digital capabilities and market positioning.

Geopolitical stability and paper supply

Political tensions drive energy costs and pulp imports, squeezing print margins: European TTF gas plunged from peaks near €330/MWh in 2022 to around €60/MWh in 2024 but remains volatility-prone, while NBSK pulp fell from ~$1,100/t in 2022 to ~ $700/t in 2024, affecting input costs and lead times. Sanctions or trade barriers can halt shipments, so contingency sourcing and local printing reduce exposure, and policy energy relief (subsidies/tax breaks) has capped some spikes.

- Energy volatility — TTF swing €330→€60/MWh (2022→2024)

- Pulp price shift — NBSK ~$1,100→~$700/t (2022→2024)

- Mitigation — contingency sourcing, nearshoring, local print

- Policy cushion — subsidies/tax relief limit cost spikes

Regulatory lobbying and professional bodies

Regulatory lobbying by bar associations and chambers shapes legal publishing standards and acceptance; the German Bar Association (DAV) represents about 160,000 lawyers (2024), making alignment key for credibility and adoption. Political debates over self-regulation shift citation preferences, so partnerships with these bodies can secure official distribution channels and revenue streams.

- Align with DAV and chambers

- Target citation influence

- Secure official distribution

DMA/DSA open ~447m market; ~22 gatekeepers boost compliance

EU DMA/DSA expand a ~447m cross‑border market and name ~22 gatekeepers, raising compliance costs but opening pan‑EU reach. Tax/audit reforms (OECD Pillar Two; DE combined tax ~30–33%) keep demand for authoritative legal content high. Energy/pulp volatility (TTF ~€60/MWh; NBSK ~$700/t) and DAV (~160,000 lawyers) shape distribution and credibility strategies.

| Item | 2024/25 |

|---|---|

| EU consumers | ~447m |

| Gatekeepers | ~22 |

| Digital Europe | €7.5bn |

| NextGenEU | €750bn |

| Germany tax | 30–33% |

| DAV lawyers | ~160,000 |

| TTF gas | ~€60/MWh |

| NBSK pulp | ~$700/t |

What is included in the product

Explores how macro-environmental factors uniquely affect Dr. Haas GmbH across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants and investors identify risks, opportunities and strategic responses aligned to regional market and regulatory dynamics.

Visually segmented by PESTEL categories, the Dr. Haas GmbH PESTLE Analysis delivers a clean, shareable summary that’s easy to drop into presentations, edit with region- or business-specific notes, and use in planning sessions to streamline external risk discussion and team alignment.

Economic factors

Subscription budgets of professional firms

Economic cycles shape subscription budgets for law and tax firms: IMF projected global GDP growth of 3.1% in 2024, but sectoral volatility persists, and Thomson Reuters reported global legal demand growth of just 2.7% in 2023, prompting firms to consolidate vendors, favor tiered pricing and bundles, and require demonstrable productivity gains to defend renewals.

Inflation and input cost pressures

Rising costs in printing, logistics and tech talent squeezed Dr. Haas GmbH margins as euro area HICP eased to about 2.4% in 2024 but sector-specific inputs remained elevated, with paper/ink up roughly 8–12% versus 2019 and freight rates above pre‑pandemic norms. Price indexation clauses enable partial pass‑through, yet customers resist hikes without added value. Automation and RPA implementations can lower unit costs by an estimated 10–20%, offsetting some pressure.

Digital adoption and recurring revenue mix

Shift from print to digital raises gross margins (SaaS-style gross margins typically 70–90%) and makes cash flow more predictable as recurring revenue rises; firms with >50% recurring mix report materially lower revenue volatility. Transition risk includes churn if digital feature parity lags, with typical churn benchmarks 5–10% annually. Cross-selling databases, workflows and updates boosts ARPU. Phased 12–36 month migration plans smooth revenue volatility.

Consolidation among professional services

Consolidation in legal and tax advisory concentrates purchasing power, forcing vendors to add enterprise features and steeper volume discounts as the legaltech market is projected to reach USD 25.17 billion by 2026. Large accounts increasingly demand integrated licensing and SLAs, while smaller practitioners require low‑cost self‑serve options to remain viable. Dr. Haas GmbH should run dual go‑to‑market tracks to balance volume and margin.

- Concentration: fewer buyers, higher negotiation leverage

- Enterprise demand: integrated features + discounting pressure

- SME need: affordable self‑serve products

- Strategy: dual GTM for volume (self‑serve) and margin (enterprise)

Currency exposure on content licensing

International rights, data feeds and software tools are often invoiced in USD, EUR or GBP, and 2024 saw EUR/USD average about 1.08, producing low-single-digit percentage swings in content COGS that compressed margins for media licensors. Matching foreign-currency revenues provides natural hedging to offset these cost moves. Using forward contracts and FX swaps is common to stabilize budgeting and protect margins.

- FX invoicing: USD/EUR/GBP exposure

- 2024 EUR/USD avg ~1.08 — low-single-digit COGS variability

- Natural hedging: match revenues to costs

- Forward contracts: budget stability

DMA/DSA open ~447m market; ~22 gatekeepers boost compliance

Economic cycles capped law/tax subscription growth (IMF 2024 GDP 3.1%; legal demand +2.7% in 2023), pressuring renewals and favoring tiered pricing. Input inflation hit margins (EA HICP ~2.4% 2024; paper/ink +8–12% vs 2019; freight elevated); automation can cut unit costs 10–20%. Digital mix raises gross margins (SaaS 70–90%); churn 5–10% risks during migration. FX (EUR/USD ~1.08 in 2024) causes low‑single‑digit COGS swings.

| Metric | Value |

|---|---|

| IMF global GDP 2024 | 3.1% |

| Legal demand 2023 | +2.7% |

| EA HICP 2024 | ~2.4% |

| Paper/ink vs 2019 | +8–12% |

| Automation cost save | 10–20% |

| EUR/USD 2024 avg | ~1.08 |

Same Document Delivered

Dr. Haas GmbH PESTLE Analysis

The preview shown here is the exact Dr. Haas GmbH PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It includes political, economic, social, technological, legal and environmental assessments plus actionable insights. No placeholders, no surprises; download the final file immediately after checkout.