Hagiwara Electric SWOT Analysis

Your Strategic Toolkit Starts Here

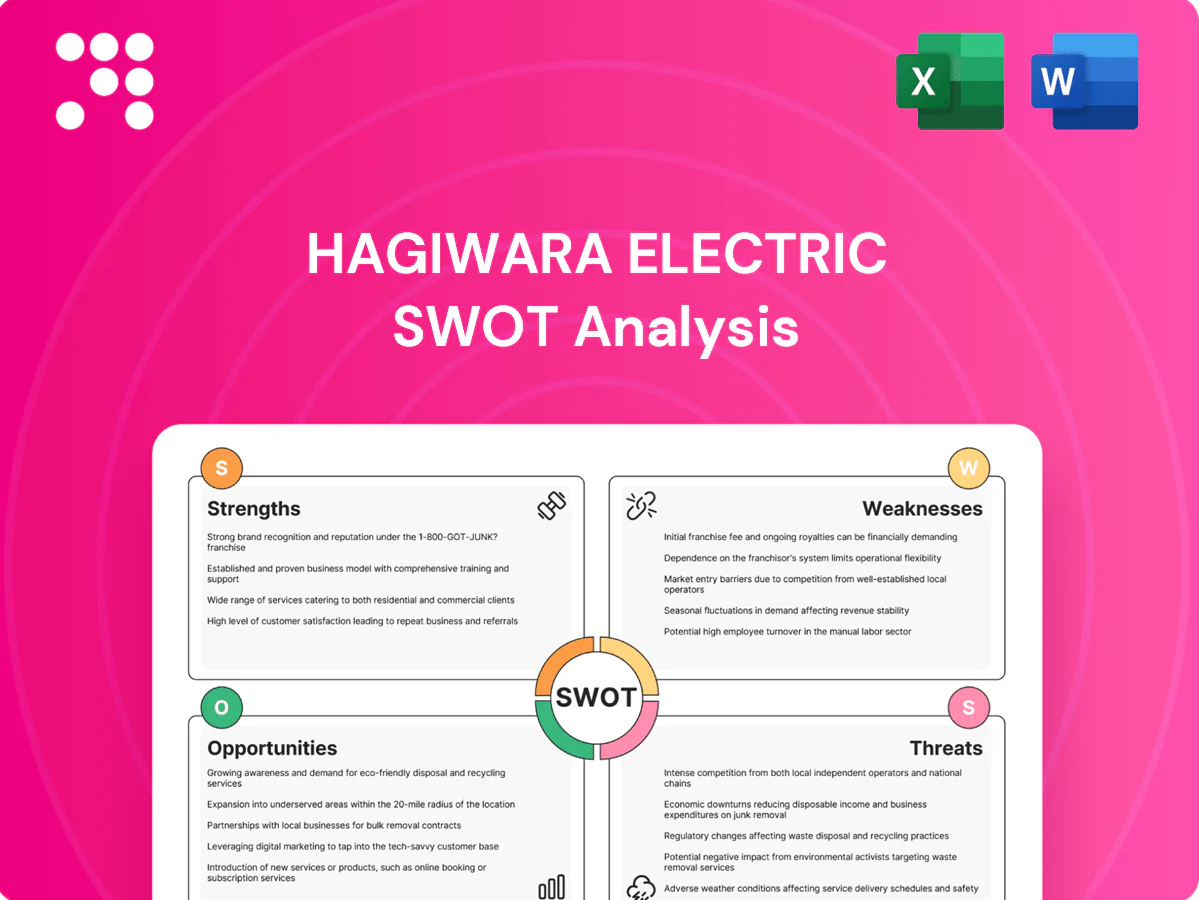

Hagiwara Electric's SWOT snapshot highlights robust manufacturing expertise, niche product lines, and export potential, balanced by supply-chain exposure and competitive pressures. Want the full strategic picture and data-driven recommendations? Purchase the complete SWOT analysis for a professional, editable Word and Excel package to plan, pitch, or invest with confidence.

Strengths

Deep industrial computing specialization

Hagiwara Electric's deep focus on embedded and industrial PCs aligns with the surge in automation and OT demand—IDC forecasts about 41.6 billion connected IoT devices by 2025, increasing need for edge/industrial compute. This specialization enables precise product fit and faster solutioning for mission-critical applications, raising customer trust. Strong domain knowledge increases switching costs in long-lifecycle industrial deployments.

Broad multi-vendor portfolio

Broad multi-vendor portfolio gives access to diverse embedded computers, industrial networking gear, and software, widening solution options for varied industry needs. Multi-sourcing balances cost, performance, and lead times, helping clients mitigate procurement bottlenecks. It reduces single-vendor risk and enhances reliability of supply chains. Bundling multi-vendor offerings increases deal size and customer stickiness.

Technical support and system integration

Integration services elevate Hagiwara Electric from trader to solution partner, enabling end-to-end pre-configuration, testing and lifecycle support that reduce customer operational complexity. These services generate higher-margin recurring revenue beyond one-time hardware sales. Embedding Hagiwara in customers’ workflows increases stickiness and upsell potential across project lifecycles.

Entrenched in manufacturing, infrastructure, transportation

- 10+ year lifecycles

- Use-case driven repeat business

- Installed base fuels upgrades

- Shorter sales cycles

Reliability and industrial standards know-how

Hagiwara Electric's deep ruggedization expertise, broad certifications and commitment to long-term availability reduce OT downtime risk and support equipment lifecycles of roughly 10–25 years, speeding customer ROI. Thorough documentation and validation shorten approval cycles and regulatory acceptance, differentiating Hagiwara from general IT resellers and lowering integration risk.

- Ruggedization expertise

- Certifications & compliance

- 10–25 year lifecycle support

- Accelerated approvals via documentation

Rugged edge PCs seize 41.6B IoT wave, raising switching costs and recurring services

Hagiwara Electric's specialization in rugged embedded/industrial PCs aligns with an IoT surge (41.6 billion connected devices by 2025, IDC), driving edge compute demand and higher switching costs in 10–25 year OT lifecycles. Broad multi-vendor portfolio and integration services create recurring, higher-margin ties and shorten proof-of-concept timelines.

| Strength | Evidence | Metric |

|---|---|---|

| Market fit | IDC IoT forecast | 41.6B devices by 2025 |

| Lifecycle support | Ruggedization & compliance | 10–25 years |

| Business model | Services + multi-vendor | Recurring/higher-margin revenue |

What is included in the product

Delivers a strategic overview of Hagiwara Electric’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position, growth drivers, operational gaps, and future risks.

Provides a concise SWOT matrix for Hagiwara Electric that quickly highlights strategic blind spots and growth levers, enabling fast alignment and actionable decisions to relieve planning pain points.

Weaknesses

Dependence on supplier roadmaps

Dependence on OEM roadmaps constrains Hagiwara Electric’s control over product features, pricing, and availability, exposing the company to sudden design or sourcing shifts. End-of-life changes by suppliers can abruptly disrupt customer deployments and require costly redesigns or inventory write-offs. Limited negotiating leverage versus larger distributors complicates securing favorable terms and long-term maintenance commitments.

Distributor margin compression

Hardware distribution typically carries low gross margins, commonly in the 5–15% range, leaving limited room for profit; price competition can push margins toward the low single digits. Currency swings and component-cost volatility, highlighted during 2021–24 supply-chain disruptions, amplify margin pressure. Scaling higher-margin services is therefore essential to offset distributor margin compression.

Limited differentiation risk

Competitors can access similar products, narrowing Hagiwara Electric’s product-based moat as the global connector market, valued at about USD 62.8 billion in 2023, sees rapid OEM sourcing and commoditization.

Without proprietary IP, Hagiwara must rely on systems integration and after-sales support to extract margin, where service replication by EMS and distributors is increasingly common.

Replication of service offerings by contract manufacturers and global distributors erodes pricing power and forces reinvestment in quality controls; brand separation depends on consistently high execution across channels.

Exposure to cyclical capex

Exposure to cyclical capex makes Hagiwara Electric vulnerable as manufacturing and infrastructure spending ebb with macro cycles, causing order intake and inventory turns to swing and revenue visibility to become lumpy. Project deferrals during downturns compress margins and force tighter cash flow management to sustain operations and supplier relationships.

- Order intake volatility

- Inventory turn pressure

- Lumpy revenue visibility

- Heightened cash-flow risk in downturns

Potential scale constraints

Hagiwara Electric risks being outcompeted by larger global distributors that in 2024 accounted for roughly 60% of electronic components distribution revenue, enabling them to undercut on pricing and offer deeper inventory and logistics muscle. Limited geographic reach constrains revenue diversification and caps growth potential. Vendor attention often skews to bigger channels, slowing Hagiwara’s entry into new verticals and regions.

- Larger distributors ~60% market share (2024)

- Weaker pricing/inventory/logistics

- Limited geographic footprint limits growth

- Lower vendor priority slows market entry

OEM reliance, low margins 5–15%, ~60% distributor dominance

Dependence on OEM roadmaps limits control over features, pricing and availability, raising redesign and write-off risk. Low distributor gross margins (5–15%, often drifting to low single digits) and 2021–24 supply-chain volatility compress profitability. Larger global distributors held ~60% of market share in 2024, restricting pricing, inventory and geographic reach.

| Metric | Value |

|---|---|

| Distributor gross margin | 5–15% (often low single digits) |

| Global distributor share (2024) | ~60% |

| Supply-chain shocks | 2021–24 highlighted volatility |

Same Document Delivered

Hagiwara Electric SWOT Analysis

This is the actual Hagiwara Electric SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth, editable version.

Your Strategic Toolkit Starts Here

Hagiwara Electric's SWOT snapshot highlights robust manufacturing expertise, niche product lines, and export potential, balanced by supply-chain exposure and competitive pressures. Want the full strategic picture and data-driven recommendations? Purchase the complete SWOT analysis for a professional, editable Word and Excel package to plan, pitch, or invest with confidence.

Strengths

Deep industrial computing specialization

Hagiwara Electric's deep focus on embedded and industrial PCs aligns with the surge in automation and OT demand—IDC forecasts about 41.6 billion connected IoT devices by 2025, increasing need for edge/industrial compute. This specialization enables precise product fit and faster solutioning for mission-critical applications, raising customer trust. Strong domain knowledge increases switching costs in long-lifecycle industrial deployments.

Broad multi-vendor portfolio

Broad multi-vendor portfolio gives access to diverse embedded computers, industrial networking gear, and software, widening solution options for varied industry needs. Multi-sourcing balances cost, performance, and lead times, helping clients mitigate procurement bottlenecks. It reduces single-vendor risk and enhances reliability of supply chains. Bundling multi-vendor offerings increases deal size and customer stickiness.

Technical support and system integration

Integration services elevate Hagiwara Electric from trader to solution partner, enabling end-to-end pre-configuration, testing and lifecycle support that reduce customer operational complexity. These services generate higher-margin recurring revenue beyond one-time hardware sales. Embedding Hagiwara in customers’ workflows increases stickiness and upsell potential across project lifecycles.

Entrenched in manufacturing, infrastructure, transportation

- 10+ year lifecycles

- Use-case driven repeat business

- Installed base fuels upgrades

- Shorter sales cycles

Reliability and industrial standards know-how

Hagiwara Electric's deep ruggedization expertise, broad certifications and commitment to long-term availability reduce OT downtime risk and support equipment lifecycles of roughly 10–25 years, speeding customer ROI. Thorough documentation and validation shorten approval cycles and regulatory acceptance, differentiating Hagiwara from general IT resellers and lowering integration risk.

- Ruggedization expertise

- Certifications & compliance

- 10–25 year lifecycle support

- Accelerated approvals via documentation

Rugged edge PCs seize 41.6B IoT wave, raising switching costs and recurring services

Hagiwara Electric's specialization in rugged embedded/industrial PCs aligns with an IoT surge (41.6 billion connected devices by 2025, IDC), driving edge compute demand and higher switching costs in 10–25 year OT lifecycles. Broad multi-vendor portfolio and integration services create recurring, higher-margin ties and shorten proof-of-concept timelines.

| Strength | Evidence | Metric |

|---|---|---|

| Market fit | IDC IoT forecast | 41.6B devices by 2025 |

| Lifecycle support | Ruggedization & compliance | 10–25 years |

| Business model | Services + multi-vendor | Recurring/higher-margin revenue |

What is included in the product

Delivers a strategic overview of Hagiwara Electric’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position, growth drivers, operational gaps, and future risks.

Provides a concise SWOT matrix for Hagiwara Electric that quickly highlights strategic blind spots and growth levers, enabling fast alignment and actionable decisions to relieve planning pain points.

Weaknesses

Dependence on supplier roadmaps

Dependence on OEM roadmaps constrains Hagiwara Electric’s control over product features, pricing, and availability, exposing the company to sudden design or sourcing shifts. End-of-life changes by suppliers can abruptly disrupt customer deployments and require costly redesigns or inventory write-offs. Limited negotiating leverage versus larger distributors complicates securing favorable terms and long-term maintenance commitments.

Distributor margin compression

Hardware distribution typically carries low gross margins, commonly in the 5–15% range, leaving limited room for profit; price competition can push margins toward the low single digits. Currency swings and component-cost volatility, highlighted during 2021–24 supply-chain disruptions, amplify margin pressure. Scaling higher-margin services is therefore essential to offset distributor margin compression.

Limited differentiation risk

Competitors can access similar products, narrowing Hagiwara Electric’s product-based moat as the global connector market, valued at about USD 62.8 billion in 2023, sees rapid OEM sourcing and commoditization.

Without proprietary IP, Hagiwara must rely on systems integration and after-sales support to extract margin, where service replication by EMS and distributors is increasingly common.

Replication of service offerings by contract manufacturers and global distributors erodes pricing power and forces reinvestment in quality controls; brand separation depends on consistently high execution across channels.

Exposure to cyclical capex

Exposure to cyclical capex makes Hagiwara Electric vulnerable as manufacturing and infrastructure spending ebb with macro cycles, causing order intake and inventory turns to swing and revenue visibility to become lumpy. Project deferrals during downturns compress margins and force tighter cash flow management to sustain operations and supplier relationships.

- Order intake volatility

- Inventory turn pressure

- Lumpy revenue visibility

- Heightened cash-flow risk in downturns

Potential scale constraints

Hagiwara Electric risks being outcompeted by larger global distributors that in 2024 accounted for roughly 60% of electronic components distribution revenue, enabling them to undercut on pricing and offer deeper inventory and logistics muscle. Limited geographic reach constrains revenue diversification and caps growth potential. Vendor attention often skews to bigger channels, slowing Hagiwara’s entry into new verticals and regions.

- Larger distributors ~60% market share (2024)

- Weaker pricing/inventory/logistics

- Limited geographic footprint limits growth

- Lower vendor priority slows market entry

OEM reliance, low margins 5–15%, ~60% distributor dominance

Dependence on OEM roadmaps limits control over features, pricing and availability, raising redesign and write-off risk. Low distributor gross margins (5–15%, often drifting to low single digits) and 2021–24 supply-chain volatility compress profitability. Larger global distributors held ~60% of market share in 2024, restricting pricing, inventory and geographic reach.

| Metric | Value |

|---|---|

| Distributor gross margin | 5–15% (often low single digits) |

| Global distributor share (2024) | ~60% |

| Supply-chain shocks | 2021–24 highlighted volatility |

Same Document Delivered

Hagiwara Electric SWOT Analysis

This is the actual Hagiwara Electric SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth, editable version.

Description

Your Strategic Toolkit Starts Here

Hagiwara Electric's SWOT snapshot highlights robust manufacturing expertise, niche product lines, and export potential, balanced by supply-chain exposure and competitive pressures. Want the full strategic picture and data-driven recommendations? Purchase the complete SWOT analysis for a professional, editable Word and Excel package to plan, pitch, or invest with confidence.

Strengths

Deep industrial computing specialization

Hagiwara Electric's deep focus on embedded and industrial PCs aligns with the surge in automation and OT demand—IDC forecasts about 41.6 billion connected IoT devices by 2025, increasing need for edge/industrial compute. This specialization enables precise product fit and faster solutioning for mission-critical applications, raising customer trust. Strong domain knowledge increases switching costs in long-lifecycle industrial deployments.

Broad multi-vendor portfolio

Broad multi-vendor portfolio gives access to diverse embedded computers, industrial networking gear, and software, widening solution options for varied industry needs. Multi-sourcing balances cost, performance, and lead times, helping clients mitigate procurement bottlenecks. It reduces single-vendor risk and enhances reliability of supply chains. Bundling multi-vendor offerings increases deal size and customer stickiness.

Technical support and system integration

Integration services elevate Hagiwara Electric from trader to solution partner, enabling end-to-end pre-configuration, testing and lifecycle support that reduce customer operational complexity. These services generate higher-margin recurring revenue beyond one-time hardware sales. Embedding Hagiwara in customers’ workflows increases stickiness and upsell potential across project lifecycles.

Entrenched in manufacturing, infrastructure, transportation

- 10+ year lifecycles

- Use-case driven repeat business

- Installed base fuels upgrades

- Shorter sales cycles

Reliability and industrial standards know-how

Hagiwara Electric's deep ruggedization expertise, broad certifications and commitment to long-term availability reduce OT downtime risk and support equipment lifecycles of roughly 10–25 years, speeding customer ROI. Thorough documentation and validation shorten approval cycles and regulatory acceptance, differentiating Hagiwara from general IT resellers and lowering integration risk.

- Ruggedization expertise

- Certifications & compliance

- 10–25 year lifecycle support

- Accelerated approvals via documentation

Rugged edge PCs seize 41.6B IoT wave, raising switching costs and recurring services

Hagiwara Electric's specialization in rugged embedded/industrial PCs aligns with an IoT surge (41.6 billion connected devices by 2025, IDC), driving edge compute demand and higher switching costs in 10–25 year OT lifecycles. Broad multi-vendor portfolio and integration services create recurring, higher-margin ties and shorten proof-of-concept timelines.

| Strength | Evidence | Metric |

|---|---|---|

| Market fit | IDC IoT forecast | 41.6B devices by 2025 |

| Lifecycle support | Ruggedization & compliance | 10–25 years |

| Business model | Services + multi-vendor | Recurring/higher-margin revenue |

What is included in the product

Delivers a strategic overview of Hagiwara Electric’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position, growth drivers, operational gaps, and future risks.

Provides a concise SWOT matrix for Hagiwara Electric that quickly highlights strategic blind spots and growth levers, enabling fast alignment and actionable decisions to relieve planning pain points.

Weaknesses

Dependence on supplier roadmaps

Dependence on OEM roadmaps constrains Hagiwara Electric’s control over product features, pricing, and availability, exposing the company to sudden design or sourcing shifts. End-of-life changes by suppliers can abruptly disrupt customer deployments and require costly redesigns or inventory write-offs. Limited negotiating leverage versus larger distributors complicates securing favorable terms and long-term maintenance commitments.

Distributor margin compression

Hardware distribution typically carries low gross margins, commonly in the 5–15% range, leaving limited room for profit; price competition can push margins toward the low single digits. Currency swings and component-cost volatility, highlighted during 2021–24 supply-chain disruptions, amplify margin pressure. Scaling higher-margin services is therefore essential to offset distributor margin compression.

Limited differentiation risk

Competitors can access similar products, narrowing Hagiwara Electric’s product-based moat as the global connector market, valued at about USD 62.8 billion in 2023, sees rapid OEM sourcing and commoditization.

Without proprietary IP, Hagiwara must rely on systems integration and after-sales support to extract margin, where service replication by EMS and distributors is increasingly common.

Replication of service offerings by contract manufacturers and global distributors erodes pricing power and forces reinvestment in quality controls; brand separation depends on consistently high execution across channels.

Exposure to cyclical capex

Exposure to cyclical capex makes Hagiwara Electric vulnerable as manufacturing and infrastructure spending ebb with macro cycles, causing order intake and inventory turns to swing and revenue visibility to become lumpy. Project deferrals during downturns compress margins and force tighter cash flow management to sustain operations and supplier relationships.

- Order intake volatility

- Inventory turn pressure

- Lumpy revenue visibility

- Heightened cash-flow risk in downturns

Potential scale constraints

Hagiwara Electric risks being outcompeted by larger global distributors that in 2024 accounted for roughly 60% of electronic components distribution revenue, enabling them to undercut on pricing and offer deeper inventory and logistics muscle. Limited geographic reach constrains revenue diversification and caps growth potential. Vendor attention often skews to bigger channels, slowing Hagiwara’s entry into new verticals and regions.

- Larger distributors ~60% market share (2024)

- Weaker pricing/inventory/logistics

- Limited geographic footprint limits growth

- Lower vendor priority slows market entry

OEM reliance, low margins 5–15%, ~60% distributor dominance

Dependence on OEM roadmaps limits control over features, pricing and availability, raising redesign and write-off risk. Low distributor gross margins (5–15%, often drifting to low single digits) and 2021–24 supply-chain volatility compress profitability. Larger global distributors held ~60% of market share in 2024, restricting pricing, inventory and geographic reach.

| Metric | Value |

|---|---|

| Distributor gross margin | 5–15% (often low single digits) |

| Global distributor share (2024) | ~60% |

| Supply-chain shocks | 2021–24 highlighted volatility |

Same Document Delivered

Hagiwara Electric SWOT Analysis

This is the actual Hagiwara Electric SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth, editable version.