Hailiang Education Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

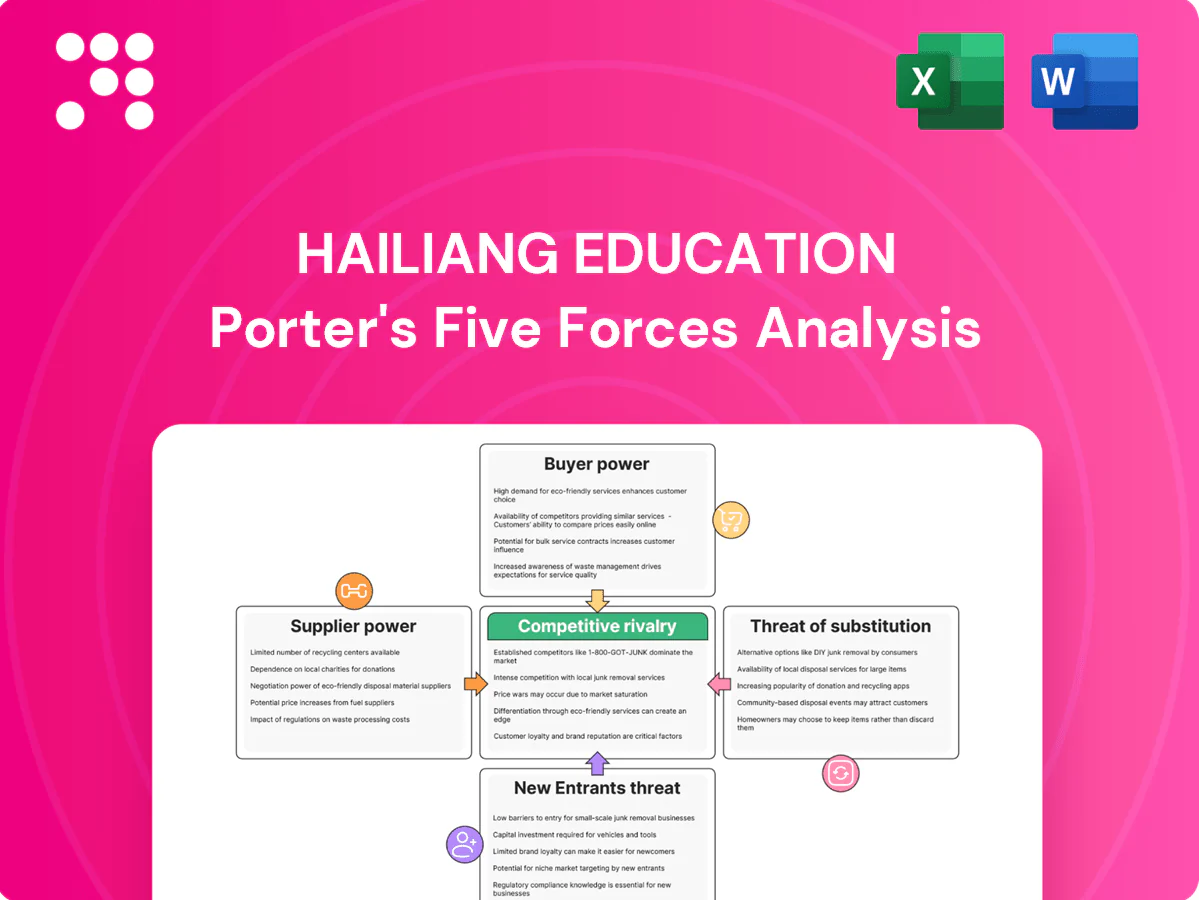

Hailiang Education faces moderate buyer power and rising competitive intensity as online and private tutors scale, while supplier influence and regulatory shifts shape margins; substitutes and new entrants exert uneven pressure across segments. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hailiang’s competitive dynamics in detail.

Suppliers Bargaining Power

Teacher talent scarcity

Experienced bilingual and STEM teachers are scarce in China’s private K–12 market, with a 2024 industry survey reporting 62% of schools facing shortages; scarcity pushes wage demands and retention bonuses up, often a 20–30% premium versus general teacher pay. Star faculty leverage reputations to negotiate better terms, amplifying cost pressure on margins. Hailiang must invest in training pipelines and recruitment to reduce supplier dependency.

Curriculum and content vendors

International curricula and exam-prep materials largely come from a handful of specialized providers—IB, Cambridge, Pearson, ETS and College Board—concentrating supply and giving differentiated content moderate pricing power. Multi-sourcing across these five major vendors plus growing internal content development reduces dependency and limits bargaining leverage. Regulatory alignment with provincial and national standards further narrows viable supplier options.

Edtech platforms and infrastructure

LMS, hardware and cloud services are concentrated among a few large vendors, with AWS, Azure and GCP holding about 64% of global cloud market share in 2024; this concentration raises supplier leverage as switching costs and integration complexity grow. Typical enterprise contracts span 3–5 years, locking in terms and reducing flexibility. Negotiating bundled pricing and open-standards integrations can materially reduce supplier risk.

Real estate and local services

Campus land, facilities and transport are highly location-constrained, concentrating supplier power in prime urban areas where municipal approvals and landlord leverage are strong; education leases commonly exceed 10 years and capex payback periods often span a decade or more, limiting exit flexibility, while regional diversification across tiers reduces single-market supplier dependency.

- Location constraint: prime sites command higher landlord leverage

- Regulatory power: municipal approvals raise switching costs

- Long-term exposure: leases often 10+ years, capex payback ~10 years

- Diversification: multi-region footprint rebalances bargaining

Regulatory approvals as quasi-supply

Licenses, quotas and policy permissions act as essential inputs for Hailiang Education; the July 2021 double reduction shift shows how regulatory changes can immediately curtail capacity and demand, with Chinas K-12 private tutoring market revenue falling roughly 50–60% versus 2019 levels and remaining depressed into 2024. This indirect supplier wields very high power in China; proactive compliance, licensing management and government relations are therefore critical to control sudden compliance costs and market access risk.

- Licenses = essential input, gatekeeping market access

- Policy shifts can cut supply/demand rapidly (double reduction, 2021)

- Market revenue down ~50–60% vs 2019 through 2024

- High supplier power → prioritize compliance & gov relations

Teacher shortages, long leases and cloud dominance create high supplier constraints

Supplier power is mixed: scarce bilingual/STEM teachers give high leverage (62% schools short; 20–30% wage premium), curricula vendors moderate power (IB/Cambridge/Pearson/ETS/College Board), cloud providers higher power (AWS/Azure/GCP ~64% share in 2024), land/leases and regulatory licenses exert very high, long-term constraint (leases 10+ yrs; market revenue down ~50–60% vs 2019).

| Supplier | Power | Key metrics (2024) |

|---|---|---|

| Teachers | High | 62% shortage; 20–30% premium |

| Curricula | Moderate | 5 major vendors |

| Cloud | Moderate-High | AWS/Azure/GCP 64% share |

| Land/Leases | High | Leases 10+ yrs |

| Regulation | Very High | Revenue -50–60% vs 2019 |

What is included in the product

Uncovers key drivers of competition, supplier and buyer influence, substitutes, entry barriers, and rivalry tailored exclusively for Hailiang Education, highlighting disruptive threats and strategic implications for market share and profitability; fully editable for investor materials, business plans, and internal strategy decks.

A clear, one-sheet summary of Hailiang Education’s Porter's Five Forces—instantly highlights competitive pressures and regulatory risks for quick, board-ready decisions.

Customers Bargaining Power

Price-sensitive parents

Parents weigh tuition strictlly against measurable outcomes like exam scores and university placements, driving sensitivity to price. Transparent online comparisons of admission rates and results bolster buyer power; China’s private K-12 market was estimated near US$100B in 2024, increasing leverage. Discounts, scholarships become negotiation levers, and economic cycles amplify price elasticity in discretionary segments.

Outcome-driven expectations

Parents prioritize Gaokao results, international admissions and safety; with about 12.98 million Gaokao candidates in 2024, measurable KPIs let buyers demand demonstrable improvements. Clear outcome targets mean underperformance risks immediate churn to rivals offering higher admission rates or safer campuses. Publishing campus-level outcomes both attracts families and empowers them to negotiate pricing and service levels.

Switching and relocation options

Urban families can shift among private, public and international schools, driven by China’s 2020 urbanization rate of 63.89% and a large mobile population (about 376 million internal migrants in 2020), making mid‑year transfers and city moves tangible exit options. Social ties, parental networks and curriculum continuity create switching frictions that limit churn. When these frictions fall, buyer bargaining power rises, pressuring tuition and retention.

Information transparency and reviews

Digital forums and parent communities deliver real-time feedback for Hailiang Education, with over 80% of parents reportedly consulting online reviews before enrolling children in 2024, amplifying collective buyer power and reputational sensitivity. Reputation spreads rapidly across platforms, so negative incidents can trigger swift withdrawals and enrollment declines within days. Active, transparent communication and prompt service recovery are essential to contain impact and restore trust.

- real-time feedback

- over 80% consult reviews (2024)

- rapid withdrawals possible

- need for active communication & recovery

Ancillary services bundling

Study tours, counseling and boarding are easily unbundled, letting buyers source each element separately to trim total cost and exert pressure on margins beyond core tuition; compelling bundles with demonstrable quality differentiation help defend pricing and reduce churn.

- Unbundling reduces bundled margin

- Separate shopping increases buyer leverage

- High-differentiation bundles protect pricing

Outcome-driven parents squeeze margins; China private K‑12 ~US$100B, Gaokao 12.98M

Parents tie tuition to measurable outcomes, raising price sensitivity; China private K‑12 market ~US$100B in 2024. With 12.98M Gaokao candidates (2024) and over 80% of parents consulting online reviews, buyer leverage and reputational risk are high. Service unbundling and urban mobility increase switching options, pressuring margins unless Hailiang offers high‑differentiation bundles.

| Metric | 2024 value |

|---|---|

| Private K-12 market | ~US$100B |

| Gaokao candidates | 12.98M |

| Parents consulting reviews | >80% |

Same Document Delivered

Hailiang Education Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Hailiang Education you'll receive after purchase—no placeholders, no edits. The document is fully formatted, actionable, and ready for immediate download and use. What you see here is the final deliverable.

Go Beyond the Preview—Access the Full Strategic Report

Hailiang Education faces moderate buyer power and rising competitive intensity as online and private tutors scale, while supplier influence and regulatory shifts shape margins; substitutes and new entrants exert uneven pressure across segments. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hailiang’s competitive dynamics in detail.

Suppliers Bargaining Power

Teacher talent scarcity

Experienced bilingual and STEM teachers are scarce in China’s private K–12 market, with a 2024 industry survey reporting 62% of schools facing shortages; scarcity pushes wage demands and retention bonuses up, often a 20–30% premium versus general teacher pay. Star faculty leverage reputations to negotiate better terms, amplifying cost pressure on margins. Hailiang must invest in training pipelines and recruitment to reduce supplier dependency.

Curriculum and content vendors

International curricula and exam-prep materials largely come from a handful of specialized providers—IB, Cambridge, Pearson, ETS and College Board—concentrating supply and giving differentiated content moderate pricing power. Multi-sourcing across these five major vendors plus growing internal content development reduces dependency and limits bargaining leverage. Regulatory alignment with provincial and national standards further narrows viable supplier options.

Edtech platforms and infrastructure

LMS, hardware and cloud services are concentrated among a few large vendors, with AWS, Azure and GCP holding about 64% of global cloud market share in 2024; this concentration raises supplier leverage as switching costs and integration complexity grow. Typical enterprise contracts span 3–5 years, locking in terms and reducing flexibility. Negotiating bundled pricing and open-standards integrations can materially reduce supplier risk.

Real estate and local services

Campus land, facilities and transport are highly location-constrained, concentrating supplier power in prime urban areas where municipal approvals and landlord leverage are strong; education leases commonly exceed 10 years and capex payback periods often span a decade or more, limiting exit flexibility, while regional diversification across tiers reduces single-market supplier dependency.

- Location constraint: prime sites command higher landlord leverage

- Regulatory power: municipal approvals raise switching costs

- Long-term exposure: leases often 10+ years, capex payback ~10 years

- Diversification: multi-region footprint rebalances bargaining

Regulatory approvals as quasi-supply

Licenses, quotas and policy permissions act as essential inputs for Hailiang Education; the July 2021 double reduction shift shows how regulatory changes can immediately curtail capacity and demand, with Chinas K-12 private tutoring market revenue falling roughly 50–60% versus 2019 levels and remaining depressed into 2024. This indirect supplier wields very high power in China; proactive compliance, licensing management and government relations are therefore critical to control sudden compliance costs and market access risk.

- Licenses = essential input, gatekeeping market access

- Policy shifts can cut supply/demand rapidly (double reduction, 2021)

- Market revenue down ~50–60% vs 2019 through 2024

- High supplier power → prioritize compliance & gov relations

Teacher shortages, long leases and cloud dominance create high supplier constraints

Supplier power is mixed: scarce bilingual/STEM teachers give high leverage (62% schools short; 20–30% wage premium), curricula vendors moderate power (IB/Cambridge/Pearson/ETS/College Board), cloud providers higher power (AWS/Azure/GCP ~64% share in 2024), land/leases and regulatory licenses exert very high, long-term constraint (leases 10+ yrs; market revenue down ~50–60% vs 2019).

| Supplier | Power | Key metrics (2024) |

|---|---|---|

| Teachers | High | 62% shortage; 20–30% premium |

| Curricula | Moderate | 5 major vendors |

| Cloud | Moderate-High | AWS/Azure/GCP 64% share |

| Land/Leases | High | Leases 10+ yrs |

| Regulation | Very High | Revenue -50–60% vs 2019 |

What is included in the product

Uncovers key drivers of competition, supplier and buyer influence, substitutes, entry barriers, and rivalry tailored exclusively for Hailiang Education, highlighting disruptive threats and strategic implications for market share and profitability; fully editable for investor materials, business plans, and internal strategy decks.

A clear, one-sheet summary of Hailiang Education’s Porter's Five Forces—instantly highlights competitive pressures and regulatory risks for quick, board-ready decisions.

Customers Bargaining Power

Price-sensitive parents

Parents weigh tuition strictlly against measurable outcomes like exam scores and university placements, driving sensitivity to price. Transparent online comparisons of admission rates and results bolster buyer power; China’s private K-12 market was estimated near US$100B in 2024, increasing leverage. Discounts, scholarships become negotiation levers, and economic cycles amplify price elasticity in discretionary segments.

Outcome-driven expectations

Parents prioritize Gaokao results, international admissions and safety; with about 12.98 million Gaokao candidates in 2024, measurable KPIs let buyers demand demonstrable improvements. Clear outcome targets mean underperformance risks immediate churn to rivals offering higher admission rates or safer campuses. Publishing campus-level outcomes both attracts families and empowers them to negotiate pricing and service levels.

Switching and relocation options

Urban families can shift among private, public and international schools, driven by China’s 2020 urbanization rate of 63.89% and a large mobile population (about 376 million internal migrants in 2020), making mid‑year transfers and city moves tangible exit options. Social ties, parental networks and curriculum continuity create switching frictions that limit churn. When these frictions fall, buyer bargaining power rises, pressuring tuition and retention.

Information transparency and reviews

Digital forums and parent communities deliver real-time feedback for Hailiang Education, with over 80% of parents reportedly consulting online reviews before enrolling children in 2024, amplifying collective buyer power and reputational sensitivity. Reputation spreads rapidly across platforms, so negative incidents can trigger swift withdrawals and enrollment declines within days. Active, transparent communication and prompt service recovery are essential to contain impact and restore trust.

- real-time feedback

- over 80% consult reviews (2024)

- rapid withdrawals possible

- need for active communication & recovery

Ancillary services bundling

Study tours, counseling and boarding are easily unbundled, letting buyers source each element separately to trim total cost and exert pressure on margins beyond core tuition; compelling bundles with demonstrable quality differentiation help defend pricing and reduce churn.

- Unbundling reduces bundled margin

- Separate shopping increases buyer leverage

- High-differentiation bundles protect pricing

Outcome-driven parents squeeze margins; China private K‑12 ~US$100B, Gaokao 12.98M

Parents tie tuition to measurable outcomes, raising price sensitivity; China private K‑12 market ~US$100B in 2024. With 12.98M Gaokao candidates (2024) and over 80% of parents consulting online reviews, buyer leverage and reputational risk are high. Service unbundling and urban mobility increase switching options, pressuring margins unless Hailiang offers high‑differentiation bundles.

| Metric | 2024 value |

|---|---|

| Private K-12 market | ~US$100B |

| Gaokao candidates | 12.98M |

| Parents consulting reviews | >80% |

Same Document Delivered

Hailiang Education Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Hailiang Education you'll receive after purchase—no placeholders, no edits. The document is fully formatted, actionable, and ready for immediate download and use. What you see here is the final deliverable.

Description

Go Beyond the Preview—Access the Full Strategic Report

Hailiang Education faces moderate buyer power and rising competitive intensity as online and private tutors scale, while supplier influence and regulatory shifts shape margins; substitutes and new entrants exert uneven pressure across segments. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hailiang’s competitive dynamics in detail.

Suppliers Bargaining Power

Teacher talent scarcity

Experienced bilingual and STEM teachers are scarce in China’s private K–12 market, with a 2024 industry survey reporting 62% of schools facing shortages; scarcity pushes wage demands and retention bonuses up, often a 20–30% premium versus general teacher pay. Star faculty leverage reputations to negotiate better terms, amplifying cost pressure on margins. Hailiang must invest in training pipelines and recruitment to reduce supplier dependency.

Curriculum and content vendors

International curricula and exam-prep materials largely come from a handful of specialized providers—IB, Cambridge, Pearson, ETS and College Board—concentrating supply and giving differentiated content moderate pricing power. Multi-sourcing across these five major vendors plus growing internal content development reduces dependency and limits bargaining leverage. Regulatory alignment with provincial and national standards further narrows viable supplier options.

Edtech platforms and infrastructure

LMS, hardware and cloud services are concentrated among a few large vendors, with AWS, Azure and GCP holding about 64% of global cloud market share in 2024; this concentration raises supplier leverage as switching costs and integration complexity grow. Typical enterprise contracts span 3–5 years, locking in terms and reducing flexibility. Negotiating bundled pricing and open-standards integrations can materially reduce supplier risk.

Real estate and local services

Campus land, facilities and transport are highly location-constrained, concentrating supplier power in prime urban areas where municipal approvals and landlord leverage are strong; education leases commonly exceed 10 years and capex payback periods often span a decade or more, limiting exit flexibility, while regional diversification across tiers reduces single-market supplier dependency.

- Location constraint: prime sites command higher landlord leverage

- Regulatory power: municipal approvals raise switching costs

- Long-term exposure: leases often 10+ years, capex payback ~10 years

- Diversification: multi-region footprint rebalances bargaining

Regulatory approvals as quasi-supply

Licenses, quotas and policy permissions act as essential inputs for Hailiang Education; the July 2021 double reduction shift shows how regulatory changes can immediately curtail capacity and demand, with Chinas K-12 private tutoring market revenue falling roughly 50–60% versus 2019 levels and remaining depressed into 2024. This indirect supplier wields very high power in China; proactive compliance, licensing management and government relations are therefore critical to control sudden compliance costs and market access risk.

- Licenses = essential input, gatekeeping market access

- Policy shifts can cut supply/demand rapidly (double reduction, 2021)

- Market revenue down ~50–60% vs 2019 through 2024

- High supplier power → prioritize compliance & gov relations

Teacher shortages, long leases and cloud dominance create high supplier constraints

Supplier power is mixed: scarce bilingual/STEM teachers give high leverage (62% schools short; 20–30% wage premium), curricula vendors moderate power (IB/Cambridge/Pearson/ETS/College Board), cloud providers higher power (AWS/Azure/GCP ~64% share in 2024), land/leases and regulatory licenses exert very high, long-term constraint (leases 10+ yrs; market revenue down ~50–60% vs 2019).

| Supplier | Power | Key metrics (2024) |

|---|---|---|

| Teachers | High | 62% shortage; 20–30% premium |

| Curricula | Moderate | 5 major vendors |

| Cloud | Moderate-High | AWS/Azure/GCP 64% share |

| Land/Leases | High | Leases 10+ yrs |

| Regulation | Very High | Revenue -50–60% vs 2019 |

What is included in the product

Uncovers key drivers of competition, supplier and buyer influence, substitutes, entry barriers, and rivalry tailored exclusively for Hailiang Education, highlighting disruptive threats and strategic implications for market share and profitability; fully editable for investor materials, business plans, and internal strategy decks.

A clear, one-sheet summary of Hailiang Education’s Porter's Five Forces—instantly highlights competitive pressures and regulatory risks for quick, board-ready decisions.

Customers Bargaining Power

Price-sensitive parents

Parents weigh tuition strictlly against measurable outcomes like exam scores and university placements, driving sensitivity to price. Transparent online comparisons of admission rates and results bolster buyer power; China’s private K-12 market was estimated near US$100B in 2024, increasing leverage. Discounts, scholarships become negotiation levers, and economic cycles amplify price elasticity in discretionary segments.

Outcome-driven expectations

Parents prioritize Gaokao results, international admissions and safety; with about 12.98 million Gaokao candidates in 2024, measurable KPIs let buyers demand demonstrable improvements. Clear outcome targets mean underperformance risks immediate churn to rivals offering higher admission rates or safer campuses. Publishing campus-level outcomes both attracts families and empowers them to negotiate pricing and service levels.

Switching and relocation options

Urban families can shift among private, public and international schools, driven by China’s 2020 urbanization rate of 63.89% and a large mobile population (about 376 million internal migrants in 2020), making mid‑year transfers and city moves tangible exit options. Social ties, parental networks and curriculum continuity create switching frictions that limit churn. When these frictions fall, buyer bargaining power rises, pressuring tuition and retention.

Information transparency and reviews

Digital forums and parent communities deliver real-time feedback for Hailiang Education, with over 80% of parents reportedly consulting online reviews before enrolling children in 2024, amplifying collective buyer power and reputational sensitivity. Reputation spreads rapidly across platforms, so negative incidents can trigger swift withdrawals and enrollment declines within days. Active, transparent communication and prompt service recovery are essential to contain impact and restore trust.

- real-time feedback

- over 80% consult reviews (2024)

- rapid withdrawals possible

- need for active communication & recovery

Ancillary services bundling

Study tours, counseling and boarding are easily unbundled, letting buyers source each element separately to trim total cost and exert pressure on margins beyond core tuition; compelling bundles with demonstrable quality differentiation help defend pricing and reduce churn.

- Unbundling reduces bundled margin

- Separate shopping increases buyer leverage

- High-differentiation bundles protect pricing

Outcome-driven parents squeeze margins; China private K‑12 ~US$100B, Gaokao 12.98M

Parents tie tuition to measurable outcomes, raising price sensitivity; China private K‑12 market ~US$100B in 2024. With 12.98M Gaokao candidates (2024) and over 80% of parents consulting online reviews, buyer leverage and reputational risk are high. Service unbundling and urban mobility increase switching options, pressuring margins unless Hailiang offers high‑differentiation bundles.

| Metric | 2024 value |

|---|---|

| Private K-12 market | ~US$100B |

| Gaokao candidates | 12.98M |

| Parents consulting reviews | >80% |

Same Document Delivered

Hailiang Education Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Hailiang Education you'll receive after purchase—no placeholders, no edits. The document is fully formatted, actionable, and ready for immediate download and use. What you see here is the final deliverable.