Foshan Haitian Flavouring and Food Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

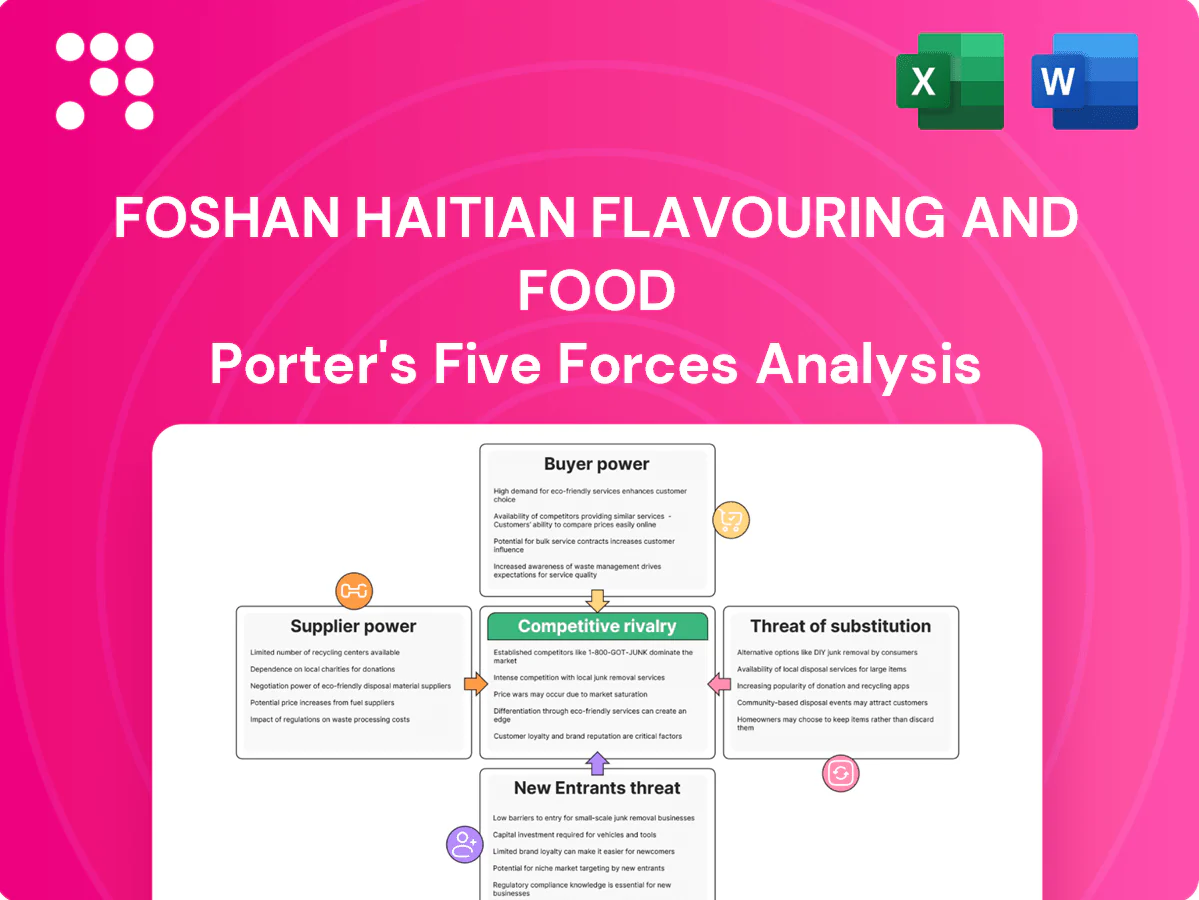

Foshan Haitian faces strong rivalry, concentrated suppliers for raw materials, rising buyer sophistication, moderate entrant barriers, and growing substitute pressures shaping margins and growth prospects. This preview is just the beginning—unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Commodity inputs mostly fungible

Core inputs like soybeans, wheat, salt and sugar are largely fungible and widely available, limiting individual supplier leverage over Foshan Haitian.

Haitian can multi-source domestically and globally to mitigate single‑supplier risk, but China imported about 100 million tonnes of soybeans in 2023, exposing costs to FX and trade policy swings.

Long‑term contracts and scale buying buffer price volatility and supply shocks but cannot fully eliminate import and policy risk.

Scale buying and vendor diversification

Haitian’s massive purchase volumes secure priority allocations, tiered rebates and extended payment terms, forcing suppliers to accept thinner margins; in 2024 the company leveraged this scale across a broad vendor panel to lower switching costs and extract better pricing. Continuous supplier performance benchmarking enforces quality and price discipline, materially compressing supplier margins and raising bar for smaller rivals.

Packaging and energy exposure

Packaging inputs—PET resin (~1,000 USD/tonne in Asia in 2024), glass, labels and caps—are supply-concentrated and tied to energy-linked feedstocks, elevating supplier power; brewing’s power and steam intensity (industrial tariffs in Guangdong around 0.6 RMB/kWh in 2024) raises sensitivity to outages and price spikes. Haitian mitigates via hedges and efficiency programs but remains exposed to short-term spikes; regional redundancy and ~60-day inventory buffers cut disruption risk.

Quality and compliance requirements

Food safety, traceability, and fermentation-grade input requirements raise qualification hurdles, shrinking the available supplier pool for specialty enzymes and raw materials and modestly increasing supplier leverage. Haitian’s centralized QA systems, supplier audits, and standardized specs reduce variability and push compliance costs onto suppliers, enabling Haitian to negotiate firmer terms. Strategic co-investments in supplier quality upgrades create switching costs and can lock in preferential pricing and supply continuity.

- food safety: tighter specs raise supplier thresholds

- traceability: fewer qualified vendors → modest supplier power

- QA & audits: standardize expectations, reduce risk

- co-investment: locks favorable terms, increases switching costs

Limited upstream integration

Haitian lacks full upstream integration into farming and petrochemicals, so it cannot fully use self-supply to constrain supplier bargaining; it relies on strategic stockpiles and futures hedges that mitigate but do not replace upstream control. Partnerships with major agricultural suppliers and packagers provide supply stability and quality assurance, keeping supply disruptions limited. Overall supplier power is moderate given limited vertical control balanced by hedging and long-term contracts.

- Integration: limited upstream ownership, reliance on external farms and petrochemical providers

- Mitigation: strategic stocks and futures hedging

- Stabilizers: long-term partnerships with large agris and packagers

- Net effect: supplier power – moderate

Supplier power moderate amid fungible feedstocks and import exposure

Core inputs (soybeans, wheat, salt, sugar) are fungible and multi‑sourcable, limiting supplier leverage; China imported ~100m t soybeans in 2023, exposing Haitian to FX and trade risk.

Haitian’s scale, long contracts and benchmarking compress supplier margins; in 2024 PET resin traded ~1,000 USD/t, aiding negotiation.

Packaging feedstock concentration and energy-linked costs (Guangdong industrial electricity ~0.6 RMB/kWh in 2024) raise supplier power for resins and glass.

Net: supplier power moderate—mitigated by hedges, ~60-day inventories and partnerships, but limited upstream integration keeps residual risk.

| Metric | Value | Impact |

|---|---|---|

| Soybean imports (2023) | ~100m t | Import exposure |

| PET resin (2024) | ~1,000 USD/t | Price leverage |

| Guangdong industrial power (2024) | ~0.6 RMB/kWh | Cost sensitivity |

| Inventory buffer | ~60 days | Disruption mitigation |

What is included in the product

Tailored exclusively for Foshan Haitian Flavouring and Food, this analysis uncovers key drivers of competition, evaluates supplier and buyer power, identifies disruptive substitutes and emerging threats, and examines barriers deterring new entrants to assess impacts on pricing, market share, and long‑term profitability.

A clear, one-sheet Porter's Five Forces summary for Foshan Haitian Flavouring and Food — perfect for quick strategic decisions and investor briefings; customize force levels as market data evolves.

Customers Bargaining Power

Fragmented consumers, concentrated retail

End-users are highly fragmented while modern trade, e-commerce and key distributors concentrate buying power; large chains push on price, placement and promos. Haitian holds roughly 30% share in the soy sauce segment, giving brand pull that tempers discounting. Broad omnichannel distribution—offline, online and distributor networks—reduces dependence on any single buyer and limits squeeze from a few large accounts.

Price sensitivity in mass segments

Price sensitivity in mass condiment segments drives frequent price comparisons and promotion cycles, with private labels and value brands anchoring shelf pricing and pressuring margins. Foshan Haitian leverages tiered portfolios—economy to premium—to segment willingness to pay and protect ASPs. Active mix management and trade promotions mitigate deep discounting pressure while preserving share in value tiers.

Foodservice and B2B contracts

Catering chains and OEM clients buy in bulk and demand consistent specs and service levels, often via 12–36 month supply contracts that concentrate purchasing power and compress margins. Contracted volumes enhance buyer leverage on price and payment terms, though Haitian’s broad SKU range and on-time fill rates secure preferred-supplier status with many chains. Switching costs rise sharply when menus and QA protocols are integrated across outlets.

Brand equity reduces switching

Foshan Haitian's strong national brand recognition and perceived quality create stickiness, with 2023 revenue reported at RMB 36.6 billion reinforcing scale and repeat purchase behavior. Its locked-in recipes and taste profiles embed Haitian into household routines; retailers favor traffic-driving brands, curbing aggressive demands, so loyalty offsets pure price bargaining.

- RMB 36.6 billion revenue (2023)

- Recipes/taste drive household repeat purchase

- Retailers limit margin pressure to keep traffic

- Loyalty reduces price-only bargaining

Data and category management

Retailers increasingly leverage POS and scanner data to demand shelf space and slotting fees; in China FMCG trade spend averaged about 12% of revenue in 2024 (Kantar), keeping buyer bargaining power high. Haitian’s category analytics and joint business planning improve share of shelf, while disciplined ROI tracking of trade spend tightens investments and protects margins.

- Retailers: POS-led negotiations

- Trade spend: ~12% of FMCG revenue (2024)

- Haitian: category insights + JBP

- ROI tracking: disciplines trade spend

Retail concentration sharpens buyer power; market leader scale and trade strategies protect margins

Buyers are fragmented but large retailers, e-commerce platforms and distributors concentrate power, driving price, placement and promo demands. Haitian’s ~30% soy sauce share and RMB 36.6 billion revenue (2023) give brand leverage and reduce pure price pressure. Trade spend in China FMCG ~12% of revenue (2024) sustains buyer bargaining; Haitian’s JBP, category analytics and SKU/mix management mitigate margin squeeze.

| Metric | Value |

|---|---|

| Haitian revenue (2023) | RMB 36.6 bn |

| Soy sauce share | ~30% |

| FMCG trade spend (China, 2024) | ~12% rev |

Preview the Actual Deliverable

Foshan Haitian Flavouring and Food Porter's Five Forces Analysis

This preview shows the exact Foshan Haitian Flavouring and Food Porter's Five Forces Analysis you'll receive. Immediately after purchase you'll get this fully formatted, ready-to-use document with no placeholders. No mockups or samples—what you see is the final deliverable available for instant download.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Foshan Haitian faces strong rivalry, concentrated suppliers for raw materials, rising buyer sophistication, moderate entrant barriers, and growing substitute pressures shaping margins and growth prospects. This preview is just the beginning—unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Commodity inputs mostly fungible

Core inputs like soybeans, wheat, salt and sugar are largely fungible and widely available, limiting individual supplier leverage over Foshan Haitian.

Haitian can multi-source domestically and globally to mitigate single‑supplier risk, but China imported about 100 million tonnes of soybeans in 2023, exposing costs to FX and trade policy swings.

Long‑term contracts and scale buying buffer price volatility and supply shocks but cannot fully eliminate import and policy risk.

Scale buying and vendor diversification

Haitian’s massive purchase volumes secure priority allocations, tiered rebates and extended payment terms, forcing suppliers to accept thinner margins; in 2024 the company leveraged this scale across a broad vendor panel to lower switching costs and extract better pricing. Continuous supplier performance benchmarking enforces quality and price discipline, materially compressing supplier margins and raising bar for smaller rivals.

Packaging and energy exposure

Packaging inputs—PET resin (~1,000 USD/tonne in Asia in 2024), glass, labels and caps—are supply-concentrated and tied to energy-linked feedstocks, elevating supplier power; brewing’s power and steam intensity (industrial tariffs in Guangdong around 0.6 RMB/kWh in 2024) raises sensitivity to outages and price spikes. Haitian mitigates via hedges and efficiency programs but remains exposed to short-term spikes; regional redundancy and ~60-day inventory buffers cut disruption risk.

Quality and compliance requirements

Food safety, traceability, and fermentation-grade input requirements raise qualification hurdles, shrinking the available supplier pool for specialty enzymes and raw materials and modestly increasing supplier leverage. Haitian’s centralized QA systems, supplier audits, and standardized specs reduce variability and push compliance costs onto suppliers, enabling Haitian to negotiate firmer terms. Strategic co-investments in supplier quality upgrades create switching costs and can lock in preferential pricing and supply continuity.

- food safety: tighter specs raise supplier thresholds

- traceability: fewer qualified vendors → modest supplier power

- QA & audits: standardize expectations, reduce risk

- co-investment: locks favorable terms, increases switching costs

Limited upstream integration

Haitian lacks full upstream integration into farming and petrochemicals, so it cannot fully use self-supply to constrain supplier bargaining; it relies on strategic stockpiles and futures hedges that mitigate but do not replace upstream control. Partnerships with major agricultural suppliers and packagers provide supply stability and quality assurance, keeping supply disruptions limited. Overall supplier power is moderate given limited vertical control balanced by hedging and long-term contracts.

- Integration: limited upstream ownership, reliance on external farms and petrochemical providers

- Mitigation: strategic stocks and futures hedging

- Stabilizers: long-term partnerships with large agris and packagers

- Net effect: supplier power – moderate

Supplier power moderate amid fungible feedstocks and import exposure

Core inputs (soybeans, wheat, salt, sugar) are fungible and multi‑sourcable, limiting supplier leverage; China imported ~100m t soybeans in 2023, exposing Haitian to FX and trade risk.

Haitian’s scale, long contracts and benchmarking compress supplier margins; in 2024 PET resin traded ~1,000 USD/t, aiding negotiation.

Packaging feedstock concentration and energy-linked costs (Guangdong industrial electricity ~0.6 RMB/kWh in 2024) raise supplier power for resins and glass.

Net: supplier power moderate—mitigated by hedges, ~60-day inventories and partnerships, but limited upstream integration keeps residual risk.

| Metric | Value | Impact |

|---|---|---|

| Soybean imports (2023) | ~100m t | Import exposure |

| PET resin (2024) | ~1,000 USD/t | Price leverage |

| Guangdong industrial power (2024) | ~0.6 RMB/kWh | Cost sensitivity |

| Inventory buffer | ~60 days | Disruption mitigation |

What is included in the product

Tailored exclusively for Foshan Haitian Flavouring and Food, this analysis uncovers key drivers of competition, evaluates supplier and buyer power, identifies disruptive substitutes and emerging threats, and examines barriers deterring new entrants to assess impacts on pricing, market share, and long‑term profitability.

A clear, one-sheet Porter's Five Forces summary for Foshan Haitian Flavouring and Food — perfect for quick strategic decisions and investor briefings; customize force levels as market data evolves.

Customers Bargaining Power

Fragmented consumers, concentrated retail

End-users are highly fragmented while modern trade, e-commerce and key distributors concentrate buying power; large chains push on price, placement and promos. Haitian holds roughly 30% share in the soy sauce segment, giving brand pull that tempers discounting. Broad omnichannel distribution—offline, online and distributor networks—reduces dependence on any single buyer and limits squeeze from a few large accounts.

Price sensitivity in mass segments

Price sensitivity in mass condiment segments drives frequent price comparisons and promotion cycles, with private labels and value brands anchoring shelf pricing and pressuring margins. Foshan Haitian leverages tiered portfolios—economy to premium—to segment willingness to pay and protect ASPs. Active mix management and trade promotions mitigate deep discounting pressure while preserving share in value tiers.

Foodservice and B2B contracts

Catering chains and OEM clients buy in bulk and demand consistent specs and service levels, often via 12–36 month supply contracts that concentrate purchasing power and compress margins. Contracted volumes enhance buyer leverage on price and payment terms, though Haitian’s broad SKU range and on-time fill rates secure preferred-supplier status with many chains. Switching costs rise sharply when menus and QA protocols are integrated across outlets.

Brand equity reduces switching

Foshan Haitian's strong national brand recognition and perceived quality create stickiness, with 2023 revenue reported at RMB 36.6 billion reinforcing scale and repeat purchase behavior. Its locked-in recipes and taste profiles embed Haitian into household routines; retailers favor traffic-driving brands, curbing aggressive demands, so loyalty offsets pure price bargaining.

- RMB 36.6 billion revenue (2023)

- Recipes/taste drive household repeat purchase

- Retailers limit margin pressure to keep traffic

- Loyalty reduces price-only bargaining

Data and category management

Retailers increasingly leverage POS and scanner data to demand shelf space and slotting fees; in China FMCG trade spend averaged about 12% of revenue in 2024 (Kantar), keeping buyer bargaining power high. Haitian’s category analytics and joint business planning improve share of shelf, while disciplined ROI tracking of trade spend tightens investments and protects margins.

- Retailers: POS-led negotiations

- Trade spend: ~12% of FMCG revenue (2024)

- Haitian: category insights + JBP

- ROI tracking: disciplines trade spend

Retail concentration sharpens buyer power; market leader scale and trade strategies protect margins

Buyers are fragmented but large retailers, e-commerce platforms and distributors concentrate power, driving price, placement and promo demands. Haitian’s ~30% soy sauce share and RMB 36.6 billion revenue (2023) give brand leverage and reduce pure price pressure. Trade spend in China FMCG ~12% of revenue (2024) sustains buyer bargaining; Haitian’s JBP, category analytics and SKU/mix management mitigate margin squeeze.

| Metric | Value |

|---|---|

| Haitian revenue (2023) | RMB 36.6 bn |

| Soy sauce share | ~30% |

| FMCG trade spend (China, 2024) | ~12% rev |

Preview the Actual Deliverable

Foshan Haitian Flavouring and Food Porter's Five Forces Analysis

This preview shows the exact Foshan Haitian Flavouring and Food Porter's Five Forces Analysis you'll receive. Immediately after purchase you'll get this fully formatted, ready-to-use document with no placeholders. No mockups or samples—what you see is the final deliverable available for instant download.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Foshan Haitian faces strong rivalry, concentrated suppliers for raw materials, rising buyer sophistication, moderate entrant barriers, and growing substitute pressures shaping margins and growth prospects. This preview is just the beginning—unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Commodity inputs mostly fungible

Core inputs like soybeans, wheat, salt and sugar are largely fungible and widely available, limiting individual supplier leverage over Foshan Haitian.

Haitian can multi-source domestically and globally to mitigate single‑supplier risk, but China imported about 100 million tonnes of soybeans in 2023, exposing costs to FX and trade policy swings.

Long‑term contracts and scale buying buffer price volatility and supply shocks but cannot fully eliminate import and policy risk.

Scale buying and vendor diversification

Haitian’s massive purchase volumes secure priority allocations, tiered rebates and extended payment terms, forcing suppliers to accept thinner margins; in 2024 the company leveraged this scale across a broad vendor panel to lower switching costs and extract better pricing. Continuous supplier performance benchmarking enforces quality and price discipline, materially compressing supplier margins and raising bar for smaller rivals.

Packaging and energy exposure

Packaging inputs—PET resin (~1,000 USD/tonne in Asia in 2024), glass, labels and caps—are supply-concentrated and tied to energy-linked feedstocks, elevating supplier power; brewing’s power and steam intensity (industrial tariffs in Guangdong around 0.6 RMB/kWh in 2024) raises sensitivity to outages and price spikes. Haitian mitigates via hedges and efficiency programs but remains exposed to short-term spikes; regional redundancy and ~60-day inventory buffers cut disruption risk.

Quality and compliance requirements

Food safety, traceability, and fermentation-grade input requirements raise qualification hurdles, shrinking the available supplier pool for specialty enzymes and raw materials and modestly increasing supplier leverage. Haitian’s centralized QA systems, supplier audits, and standardized specs reduce variability and push compliance costs onto suppliers, enabling Haitian to negotiate firmer terms. Strategic co-investments in supplier quality upgrades create switching costs and can lock in preferential pricing and supply continuity.

- food safety: tighter specs raise supplier thresholds

- traceability: fewer qualified vendors → modest supplier power

- QA & audits: standardize expectations, reduce risk

- co-investment: locks favorable terms, increases switching costs

Limited upstream integration

Haitian lacks full upstream integration into farming and petrochemicals, so it cannot fully use self-supply to constrain supplier bargaining; it relies on strategic stockpiles and futures hedges that mitigate but do not replace upstream control. Partnerships with major agricultural suppliers and packagers provide supply stability and quality assurance, keeping supply disruptions limited. Overall supplier power is moderate given limited vertical control balanced by hedging and long-term contracts.

- Integration: limited upstream ownership, reliance on external farms and petrochemical providers

- Mitigation: strategic stocks and futures hedging

- Stabilizers: long-term partnerships with large agris and packagers

- Net effect: supplier power – moderate

Supplier power moderate amid fungible feedstocks and import exposure

Core inputs (soybeans, wheat, salt, sugar) are fungible and multi‑sourcable, limiting supplier leverage; China imported ~100m t soybeans in 2023, exposing Haitian to FX and trade risk.

Haitian’s scale, long contracts and benchmarking compress supplier margins; in 2024 PET resin traded ~1,000 USD/t, aiding negotiation.

Packaging feedstock concentration and energy-linked costs (Guangdong industrial electricity ~0.6 RMB/kWh in 2024) raise supplier power for resins and glass.

Net: supplier power moderate—mitigated by hedges, ~60-day inventories and partnerships, but limited upstream integration keeps residual risk.

| Metric | Value | Impact |

|---|---|---|

| Soybean imports (2023) | ~100m t | Import exposure |

| PET resin (2024) | ~1,000 USD/t | Price leverage |

| Guangdong industrial power (2024) | ~0.6 RMB/kWh | Cost sensitivity |

| Inventory buffer | ~60 days | Disruption mitigation |

What is included in the product

Tailored exclusively for Foshan Haitian Flavouring and Food, this analysis uncovers key drivers of competition, evaluates supplier and buyer power, identifies disruptive substitutes and emerging threats, and examines barriers deterring new entrants to assess impacts on pricing, market share, and long‑term profitability.

A clear, one-sheet Porter's Five Forces summary for Foshan Haitian Flavouring and Food — perfect for quick strategic decisions and investor briefings; customize force levels as market data evolves.

Customers Bargaining Power

Fragmented consumers, concentrated retail

End-users are highly fragmented while modern trade, e-commerce and key distributors concentrate buying power; large chains push on price, placement and promos. Haitian holds roughly 30% share in the soy sauce segment, giving brand pull that tempers discounting. Broad omnichannel distribution—offline, online and distributor networks—reduces dependence on any single buyer and limits squeeze from a few large accounts.

Price sensitivity in mass segments

Price sensitivity in mass condiment segments drives frequent price comparisons and promotion cycles, with private labels and value brands anchoring shelf pricing and pressuring margins. Foshan Haitian leverages tiered portfolios—economy to premium—to segment willingness to pay and protect ASPs. Active mix management and trade promotions mitigate deep discounting pressure while preserving share in value tiers.

Foodservice and B2B contracts

Catering chains and OEM clients buy in bulk and demand consistent specs and service levels, often via 12–36 month supply contracts that concentrate purchasing power and compress margins. Contracted volumes enhance buyer leverage on price and payment terms, though Haitian’s broad SKU range and on-time fill rates secure preferred-supplier status with many chains. Switching costs rise sharply when menus and QA protocols are integrated across outlets.

Brand equity reduces switching

Foshan Haitian's strong national brand recognition and perceived quality create stickiness, with 2023 revenue reported at RMB 36.6 billion reinforcing scale and repeat purchase behavior. Its locked-in recipes and taste profiles embed Haitian into household routines; retailers favor traffic-driving brands, curbing aggressive demands, so loyalty offsets pure price bargaining.

- RMB 36.6 billion revenue (2023)

- Recipes/taste drive household repeat purchase

- Retailers limit margin pressure to keep traffic

- Loyalty reduces price-only bargaining

Data and category management

Retailers increasingly leverage POS and scanner data to demand shelf space and slotting fees; in China FMCG trade spend averaged about 12% of revenue in 2024 (Kantar), keeping buyer bargaining power high. Haitian’s category analytics and joint business planning improve share of shelf, while disciplined ROI tracking of trade spend tightens investments and protects margins.

- Retailers: POS-led negotiations

- Trade spend: ~12% of FMCG revenue (2024)

- Haitian: category insights + JBP

- ROI tracking: disciplines trade spend

Retail concentration sharpens buyer power; market leader scale and trade strategies protect margins

Buyers are fragmented but large retailers, e-commerce platforms and distributors concentrate power, driving price, placement and promo demands. Haitian’s ~30% soy sauce share and RMB 36.6 billion revenue (2023) give brand leverage and reduce pure price pressure. Trade spend in China FMCG ~12% of revenue (2024) sustains buyer bargaining; Haitian’s JBP, category analytics and SKU/mix management mitigate margin squeeze.

| Metric | Value |

|---|---|

| Haitian revenue (2023) | RMB 36.6 bn |

| Soy sauce share | ~30% |

| FMCG trade spend (China, 2024) | ~12% rev |

Preview the Actual Deliverable

Foshan Haitian Flavouring and Food Porter's Five Forces Analysis

This preview shows the exact Foshan Haitian Flavouring and Food Porter's Five Forces Analysis you'll receive. Immediately after purchase you'll get this fully formatted, ready-to-use document with no placeholders. No mockups or samples—what you see is the final deliverable available for instant download.