Kidswant Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kidswant’s competitive dynamics, market pressures, and strategic advantages in detail. The complete report quantifies force strength, provides visuals, and outlines implications for growth and risk. Get the consultant-grade breakdown ready for presentations and investment decisions.

Suppliers Bargaining Power

Concentrated marquee brands

Infant formula, diaper and baby-care categories are dominated by global and leading domestic brands—top five formula firms account for roughly 60% of the market and P&G/Kimberly‑Clark together control about 55% of global diapers—giving suppliers strong pricing and trade-term leverage. Kidswant counters with breadth, negotiated rebates and data-sharing partnerships, but reliance on must-have SKUs preserves supplier bargaining power.

Scale offsets via centralized buying

Kidswant’s national footprint in 2024 enables volume commitments, joint promotions, and extended payment terms with suppliers, driving lower acquisition costs and improved cash flow. Aggregated demand reduces per-store dependency on any single vendor, strengthening negotiation leverage and supply continuity. Scale-backed private label development mitigates price pressure, though specialty SKUs and niche brands still command premiums.

Regulatory and quality constraints

Strict safety and registration rules—for example FDA registration for infant formula facilities and EU Toy Safety Directive CE requirements—limit supplier churn and raise barriers to entry. Fewer compliant alternatives amplify leverage for certified suppliers while Kidswant’s QA filters and preferred-vendor lists further narrow the pool. Rigorous vendor audits and compliance programs partially rebalance bargaining dynamics by enforcing corrective actions and replacement timelines.

Service partners’ variable leverage

Early education and in-store activity providers remain highly fragmented in 2024, reducing supplier leverage and allowing Kidswant to curate partners and standardize service packages across stores. Localized providers face credible switching threats if KPIs slip, while branded edu-tainment partners exert stronger clout in select metropolitan markets, influencing pricing and scheduling.

- fragmentation lowers supplier power

- standardized packages increase Kidswant control

- local providers vulnerable to switching

- branded partners hold city-specific leverage

Digital data and exclusivity levers

Omnichannel data enables joint category planning, strengthening Kidswant’s leverage as retailers using omnichannel analytics saw retail e-commerce scale to roughly $6.3 trillion in 2024, improving promotional efficiency and supplier negotiation leverage. Exclusive launches and co-branded SKUs create mutual dependence, while performance-based media buys and traffic guarantees can be exchanged for better terms; suppliers still enforce channel parity to prevent conflict.

- Omnichannel data: stronger negotiating position

- Exclusive SKUs: mutual dependence

- Media/traffic guarantees: tradeable for price/promotions

- Channel parity: supplier safeguard

Scale weakens supplier leverage despite ~60% and ~55%

Supplier power is high in formula/diapers (top 5 formula ~60% share; P&G/KC ~55% diapers) but Kidswant’s 2024 national scale enables volume rebates, private label and data-driven negotiations. Regulatory compliance (FDA/EU CE) tightens supplier pool; fragmented local services lower power. Omnichannel data and exclusive SKUs create mutual dependence while channel-parity preserves supplier leverage.

| Category | 2024 Metric | Value |

|---|---|---|

| Formula top5 | Market share | ~60% |

| Diapers P&G/KC | Global share | ~55% |

| Retail e‑commerce | Global 2024 GMV | $6.3T |

What is included in the product

Tailored Porter's Five Forces analysis for Kidswant that uncovers key competitive drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, with actionable strategic insights for reports and decks.

A concise, one-sheet Porter's Five Forces tool that instantly visualizes competitive pressure with an editable spider chart and customizable force levels—perfect for quick strategic decisions. No macros, easy to copy into decks, and ready to swap in your own data for different market scenarios.

Customers Bargaining Power

High price transparency

Parents compare prices across Tmall, JD, Pinduoduo and pharmacies in real time, with platforms like Pinduoduo reporting roughly 788 million MAUs in 2024, driving deal-hunting that raises discount expectations and compresses margins. Kidswant must deploy dynamic promotions and selective price-matching to defend share, but persistent parity pressures increase buyer leverage and squeeze gross margins.

Low switching costs

With e-commerce capturing about 23% of global retail sales in 2024, alternatives for Kidswant are abundant both online and offline and often offer same- or next-day delivery. Basket items are standardized and easily reordered elsewhere, pushing price- and convenience-driven switching. Loyalty thus hinges on service quality, trust and seamless convenience; industry data show loyalty lifts lifetime value by 20–30%. Without clear differentiation, churn risk rises materially.

Trust and safety sensitivity

For infant products, authenticity and safety moderate pure price bargaining as parents prioritize verified sourcing and expert in-store guidance; the global infant products market topped $100 billion in 2024, underpinning willingness to pay for assurance. Kidswant can command a measurable premium through certified sourcing, demonstrable safety checks and after-sales support, which partially dampens buyer power in these sensitive categories.

Loyalty and membership programs

Loyalty and membership programs at Kidswant use CRM, parenting communities and events to raise stickiness; 2024 metrics show members deliver roughly 20–30% higher repeat purchase rates and 15% lower churn. Personalized lifecycle bundles and targeted offers raise switching costs, while points, subscriptions and scheduled replenishment lock purchase frequency and reduce unit-level price haggling.

- CRM-driven retention

- Community/events stickiness

- Personalized bundles lift switching

- Points/subscriptions lock frequency

- Less price haggling per unit

Segmented elasticity

Affluent urban families prioritize quality and convenience over price, supporting 15–25% higher ASPs in premium kids categories in 2024 while mass segments remain price-sensitive and elastic; category elasticity varies sharply (toys lower elasticity than infant formula). Kidswant uses tailored pricing, KVI management and channel segmentation to protect margins and reduce aggregate buyer power.

- Affluent urban: premium ASPs +15–25% (2024)

- Mass segment: high price elasticity

- Category gap: toys < formula elasticity

- Tools: KVI, dynamic pricing, channel segmentation

Transparency and big platforms shift leverage to buyers; infant premium enables higher ASPs

High price transparency and platforms like Pinduoduo (≈788M MAU in 2024) plus e‑commerce at ≈23% of retail (2024) increase buyer leverage, compressing margins; infant products ($100B market, 2024) and safety concerns allow some premium. Loyalty programs lift repeat by ~20–30% (2024), while premium segments command +15–25% ASPs.

| Metric | 2024 Value |

|---|---|

| Pinduoduo MAU | ≈788M |

| E‑commerce share | ≈23% global retail |

| Infant market | $100B |

| Member repeat lift | 20–30% |

| Premium ASP uplift | 15–25% |

Same Document Delivered

Kidswant Porter's Five Forces Analysis

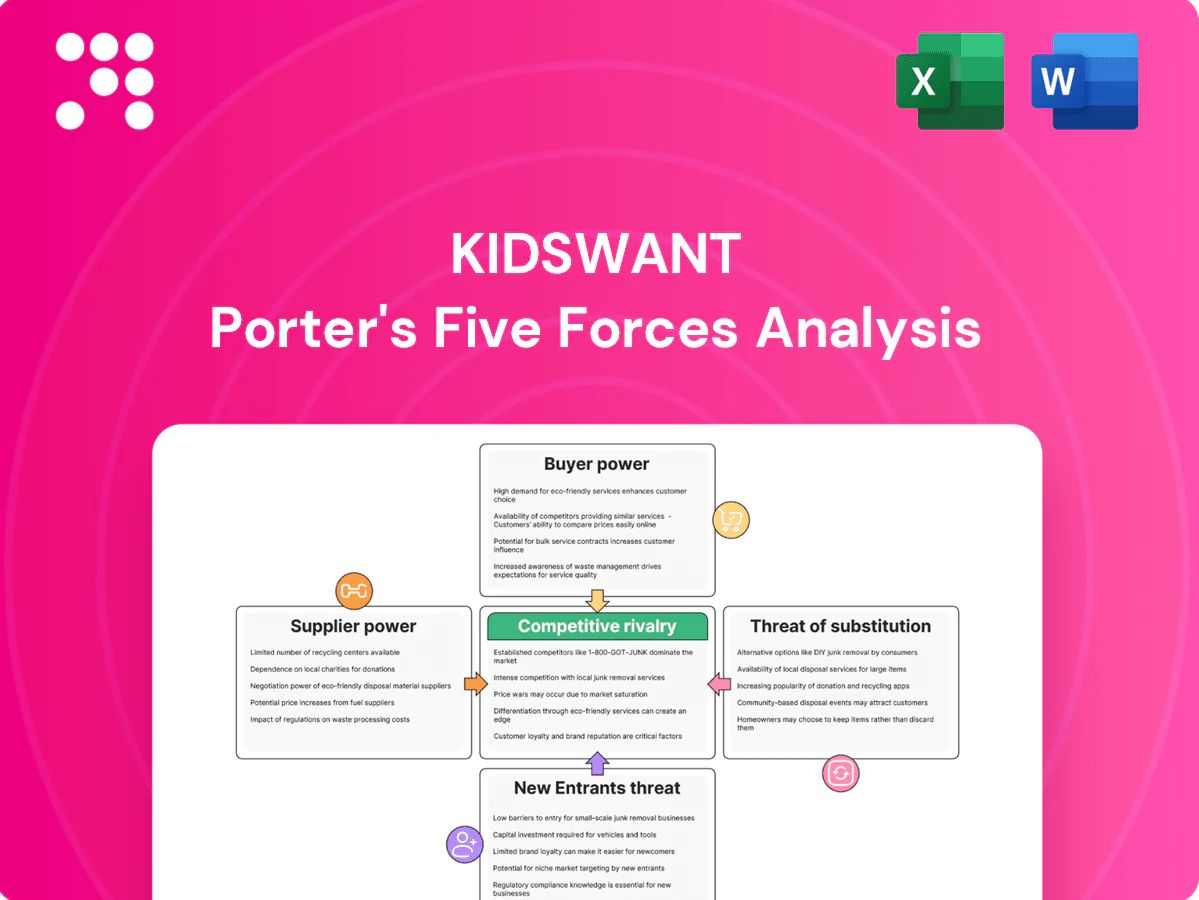

This preview is the exact Kidswant Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. It contains a full assessment of competitive rivalry, buyer and supplier power, threat of substitutes and new entrants. The file is fully formatted and ready for immediate download and use.

A Must-Have Tool for Decision-Makers

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kidswant’s competitive dynamics, market pressures, and strategic advantages in detail. The complete report quantifies force strength, provides visuals, and outlines implications for growth and risk. Get the consultant-grade breakdown ready for presentations and investment decisions.

Suppliers Bargaining Power

Concentrated marquee brands

Infant formula, diaper and baby-care categories are dominated by global and leading domestic brands—top five formula firms account for roughly 60% of the market and P&G/Kimberly‑Clark together control about 55% of global diapers—giving suppliers strong pricing and trade-term leverage. Kidswant counters with breadth, negotiated rebates and data-sharing partnerships, but reliance on must-have SKUs preserves supplier bargaining power.

Scale offsets via centralized buying

Kidswant’s national footprint in 2024 enables volume commitments, joint promotions, and extended payment terms with suppliers, driving lower acquisition costs and improved cash flow. Aggregated demand reduces per-store dependency on any single vendor, strengthening negotiation leverage and supply continuity. Scale-backed private label development mitigates price pressure, though specialty SKUs and niche brands still command premiums.

Regulatory and quality constraints

Strict safety and registration rules—for example FDA registration for infant formula facilities and EU Toy Safety Directive CE requirements—limit supplier churn and raise barriers to entry. Fewer compliant alternatives amplify leverage for certified suppliers while Kidswant’s QA filters and preferred-vendor lists further narrow the pool. Rigorous vendor audits and compliance programs partially rebalance bargaining dynamics by enforcing corrective actions and replacement timelines.

Service partners’ variable leverage

Early education and in-store activity providers remain highly fragmented in 2024, reducing supplier leverage and allowing Kidswant to curate partners and standardize service packages across stores. Localized providers face credible switching threats if KPIs slip, while branded edu-tainment partners exert stronger clout in select metropolitan markets, influencing pricing and scheduling.

- fragmentation lowers supplier power

- standardized packages increase Kidswant control

- local providers vulnerable to switching

- branded partners hold city-specific leverage

Digital data and exclusivity levers

Omnichannel data enables joint category planning, strengthening Kidswant’s leverage as retailers using omnichannel analytics saw retail e-commerce scale to roughly $6.3 trillion in 2024, improving promotional efficiency and supplier negotiation leverage. Exclusive launches and co-branded SKUs create mutual dependence, while performance-based media buys and traffic guarantees can be exchanged for better terms; suppliers still enforce channel parity to prevent conflict.

- Omnichannel data: stronger negotiating position

- Exclusive SKUs: mutual dependence

- Media/traffic guarantees: tradeable for price/promotions

- Channel parity: supplier safeguard

Scale weakens supplier leverage despite ~60% and ~55%

Supplier power is high in formula/diapers (top 5 formula ~60% share; P&G/KC ~55% diapers) but Kidswant’s 2024 national scale enables volume rebates, private label and data-driven negotiations. Regulatory compliance (FDA/EU CE) tightens supplier pool; fragmented local services lower power. Omnichannel data and exclusive SKUs create mutual dependence while channel-parity preserves supplier leverage.

| Category | 2024 Metric | Value |

|---|---|---|

| Formula top5 | Market share | ~60% |

| Diapers P&G/KC | Global share | ~55% |

| Retail e‑commerce | Global 2024 GMV | $6.3T |

What is included in the product

Tailored Porter's Five Forces analysis for Kidswant that uncovers key competitive drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, with actionable strategic insights for reports and decks.

A concise, one-sheet Porter's Five Forces tool that instantly visualizes competitive pressure with an editable spider chart and customizable force levels—perfect for quick strategic decisions. No macros, easy to copy into decks, and ready to swap in your own data for different market scenarios.

Customers Bargaining Power

High price transparency

Parents compare prices across Tmall, JD, Pinduoduo and pharmacies in real time, with platforms like Pinduoduo reporting roughly 788 million MAUs in 2024, driving deal-hunting that raises discount expectations and compresses margins. Kidswant must deploy dynamic promotions and selective price-matching to defend share, but persistent parity pressures increase buyer leverage and squeeze gross margins.

Low switching costs

With e-commerce capturing about 23% of global retail sales in 2024, alternatives for Kidswant are abundant both online and offline and often offer same- or next-day delivery. Basket items are standardized and easily reordered elsewhere, pushing price- and convenience-driven switching. Loyalty thus hinges on service quality, trust and seamless convenience; industry data show loyalty lifts lifetime value by 20–30%. Without clear differentiation, churn risk rises materially.

Trust and safety sensitivity

For infant products, authenticity and safety moderate pure price bargaining as parents prioritize verified sourcing and expert in-store guidance; the global infant products market topped $100 billion in 2024, underpinning willingness to pay for assurance. Kidswant can command a measurable premium through certified sourcing, demonstrable safety checks and after-sales support, which partially dampens buyer power in these sensitive categories.

Loyalty and membership programs

Loyalty and membership programs at Kidswant use CRM, parenting communities and events to raise stickiness; 2024 metrics show members deliver roughly 20–30% higher repeat purchase rates and 15% lower churn. Personalized lifecycle bundles and targeted offers raise switching costs, while points, subscriptions and scheduled replenishment lock purchase frequency and reduce unit-level price haggling.

- CRM-driven retention

- Community/events stickiness

- Personalized bundles lift switching

- Points/subscriptions lock frequency

- Less price haggling per unit

Segmented elasticity

Affluent urban families prioritize quality and convenience over price, supporting 15–25% higher ASPs in premium kids categories in 2024 while mass segments remain price-sensitive and elastic; category elasticity varies sharply (toys lower elasticity than infant formula). Kidswant uses tailored pricing, KVI management and channel segmentation to protect margins and reduce aggregate buyer power.

- Affluent urban: premium ASPs +15–25% (2024)

- Mass segment: high price elasticity

- Category gap: toys < formula elasticity

- Tools: KVI, dynamic pricing, channel segmentation

Transparency and big platforms shift leverage to buyers; infant premium enables higher ASPs

High price transparency and platforms like Pinduoduo (≈788M MAU in 2024) plus e‑commerce at ≈23% of retail (2024) increase buyer leverage, compressing margins; infant products ($100B market, 2024) and safety concerns allow some premium. Loyalty programs lift repeat by ~20–30% (2024), while premium segments command +15–25% ASPs.

| Metric | 2024 Value |

|---|---|

| Pinduoduo MAU | ≈788M |

| E‑commerce share | ≈23% global retail |

| Infant market | $100B |

| Member repeat lift | 20–30% |

| Premium ASP uplift | 15–25% |

Same Document Delivered

Kidswant Porter's Five Forces Analysis

This preview is the exact Kidswant Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. It contains a full assessment of competitive rivalry, buyer and supplier power, threat of substitutes and new entrants. The file is fully formatted and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kidswant’s competitive dynamics, market pressures, and strategic advantages in detail. The complete report quantifies force strength, provides visuals, and outlines implications for growth and risk. Get the consultant-grade breakdown ready for presentations and investment decisions.

Suppliers Bargaining Power

Concentrated marquee brands

Infant formula, diaper and baby-care categories are dominated by global and leading domestic brands—top five formula firms account for roughly 60% of the market and P&G/Kimberly‑Clark together control about 55% of global diapers—giving suppliers strong pricing and trade-term leverage. Kidswant counters with breadth, negotiated rebates and data-sharing partnerships, but reliance on must-have SKUs preserves supplier bargaining power.

Scale offsets via centralized buying

Kidswant’s national footprint in 2024 enables volume commitments, joint promotions, and extended payment terms with suppliers, driving lower acquisition costs and improved cash flow. Aggregated demand reduces per-store dependency on any single vendor, strengthening negotiation leverage and supply continuity. Scale-backed private label development mitigates price pressure, though specialty SKUs and niche brands still command premiums.

Regulatory and quality constraints

Strict safety and registration rules—for example FDA registration for infant formula facilities and EU Toy Safety Directive CE requirements—limit supplier churn and raise barriers to entry. Fewer compliant alternatives amplify leverage for certified suppliers while Kidswant’s QA filters and preferred-vendor lists further narrow the pool. Rigorous vendor audits and compliance programs partially rebalance bargaining dynamics by enforcing corrective actions and replacement timelines.

Service partners’ variable leverage

Early education and in-store activity providers remain highly fragmented in 2024, reducing supplier leverage and allowing Kidswant to curate partners and standardize service packages across stores. Localized providers face credible switching threats if KPIs slip, while branded edu-tainment partners exert stronger clout in select metropolitan markets, influencing pricing and scheduling.

- fragmentation lowers supplier power

- standardized packages increase Kidswant control

- local providers vulnerable to switching

- branded partners hold city-specific leverage

Digital data and exclusivity levers

Omnichannel data enables joint category planning, strengthening Kidswant’s leverage as retailers using omnichannel analytics saw retail e-commerce scale to roughly $6.3 trillion in 2024, improving promotional efficiency and supplier negotiation leverage. Exclusive launches and co-branded SKUs create mutual dependence, while performance-based media buys and traffic guarantees can be exchanged for better terms; suppliers still enforce channel parity to prevent conflict.

- Omnichannel data: stronger negotiating position

- Exclusive SKUs: mutual dependence

- Media/traffic guarantees: tradeable for price/promotions

- Channel parity: supplier safeguard

Scale weakens supplier leverage despite ~60% and ~55%

Supplier power is high in formula/diapers (top 5 formula ~60% share; P&G/KC ~55% diapers) but Kidswant’s 2024 national scale enables volume rebates, private label and data-driven negotiations. Regulatory compliance (FDA/EU CE) tightens supplier pool; fragmented local services lower power. Omnichannel data and exclusive SKUs create mutual dependence while channel-parity preserves supplier leverage.

| Category | 2024 Metric | Value |

|---|---|---|

| Formula top5 | Market share | ~60% |

| Diapers P&G/KC | Global share | ~55% |

| Retail e‑commerce | Global 2024 GMV | $6.3T |

What is included in the product

Tailored Porter's Five Forces analysis for Kidswant that uncovers key competitive drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, with actionable strategic insights for reports and decks.

A concise, one-sheet Porter's Five Forces tool that instantly visualizes competitive pressure with an editable spider chart and customizable force levels—perfect for quick strategic decisions. No macros, easy to copy into decks, and ready to swap in your own data for different market scenarios.

Customers Bargaining Power

High price transparency

Parents compare prices across Tmall, JD, Pinduoduo and pharmacies in real time, with platforms like Pinduoduo reporting roughly 788 million MAUs in 2024, driving deal-hunting that raises discount expectations and compresses margins. Kidswant must deploy dynamic promotions and selective price-matching to defend share, but persistent parity pressures increase buyer leverage and squeeze gross margins.

Low switching costs

With e-commerce capturing about 23% of global retail sales in 2024, alternatives for Kidswant are abundant both online and offline and often offer same- or next-day delivery. Basket items are standardized and easily reordered elsewhere, pushing price- and convenience-driven switching. Loyalty thus hinges on service quality, trust and seamless convenience; industry data show loyalty lifts lifetime value by 20–30%. Without clear differentiation, churn risk rises materially.

Trust and safety sensitivity

For infant products, authenticity and safety moderate pure price bargaining as parents prioritize verified sourcing and expert in-store guidance; the global infant products market topped $100 billion in 2024, underpinning willingness to pay for assurance. Kidswant can command a measurable premium through certified sourcing, demonstrable safety checks and after-sales support, which partially dampens buyer power in these sensitive categories.

Loyalty and membership programs

Loyalty and membership programs at Kidswant use CRM, parenting communities and events to raise stickiness; 2024 metrics show members deliver roughly 20–30% higher repeat purchase rates and 15% lower churn. Personalized lifecycle bundles and targeted offers raise switching costs, while points, subscriptions and scheduled replenishment lock purchase frequency and reduce unit-level price haggling.

- CRM-driven retention

- Community/events stickiness

- Personalized bundles lift switching

- Points/subscriptions lock frequency

- Less price haggling per unit

Segmented elasticity

Affluent urban families prioritize quality and convenience over price, supporting 15–25% higher ASPs in premium kids categories in 2024 while mass segments remain price-sensitive and elastic; category elasticity varies sharply (toys lower elasticity than infant formula). Kidswant uses tailored pricing, KVI management and channel segmentation to protect margins and reduce aggregate buyer power.

- Affluent urban: premium ASPs +15–25% (2024)

- Mass segment: high price elasticity

- Category gap: toys < formula elasticity

- Tools: KVI, dynamic pricing, channel segmentation

Transparency and big platforms shift leverage to buyers; infant premium enables higher ASPs

High price transparency and platforms like Pinduoduo (≈788M MAU in 2024) plus e‑commerce at ≈23% of retail (2024) increase buyer leverage, compressing margins; infant products ($100B market, 2024) and safety concerns allow some premium. Loyalty programs lift repeat by ~20–30% (2024), while premium segments command +15–25% ASPs.

| Metric | 2024 Value |

|---|---|

| Pinduoduo MAU | ≈788M |

| E‑commerce share | ≈23% global retail |

| Infant market | $100B |

| Member repeat lift | 20–30% |

| Premium ASP uplift | 15–25% |

Same Document Delivered

Kidswant Porter's Five Forces Analysis

This preview is the exact Kidswant Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. It contains a full assessment of competitive rivalry, buyer and supplier power, threat of substitutes and new entrants. The file is fully formatted and ready for immediate download and use.