Hakuhodo Holdings Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Hakuhodo Holdings faces nuanced competitive pressures—from client bargaining power and digital disruption to agency consolidation and substitute communication channels—shaping its margin and growth outlook. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings and strategic implications in detail. Get a consultant-grade report with visuals and ready-to-use Word/Excel deliverables.

Suppliers Bargaining Power

Dominant media and tech platforms

Global walled gardens command inventory and data, raising supplier leverage: Google (~29% of global digital ad spend in 2024) and Meta (~21% in 2024 per Insider Intelligence) together capture roughly half the market, letting policy changes and price moves compress agency margins. Hakuhodo’s scale strengthens negotiation, but platform concentration keeps power elevated; multi-platform planning partially offsets dependency.

Premium content and rights holders

TV networks, streaming services and sports/entertainment rights owners control scarce premium inventory, concentrating leverage over agencies like Hakuhodo; peak events (eg Super Bowl 30s spots ~$7m in 2023–24) create rate rigidity. Major streamers (Netflix ~260m paid subs in 2024) compound demand for premium audiences. Bundling and long-term rights deals can soften price spikes but demand contractual commitments. Scarcity thus sustains supplier bargaining power in key seasons.

Data, adtech, and measurement vendors

Data, DMPs, CDPs, ID graphs and verification tools are now critical for targeting and measurement in a privacy-first environment. Interoperability constraints in adtech stacks raise switching costs and can lock in vendor fees, while Hakuhodo’s integrated stacks help mitigate single-vendor risk. The ongoing deprecation of third-party cookies has increased bargaining power for privacy-compliant data suppliers and measurement vendors.

Creative talent and production houses

Regulatory and platform compliance gatekeepers

Platforms 29%+21% ad share; streamers 260m; talent gap 68%

Global platforms (Google 29% and Meta 21% of global digital ad spend in 2024) plus premium broadcasters/streamers (Netflix 260m subs in 2024) sustain high supplier leverage; Hakuhodo scale and multi-platform buys partly offset. Data/verification vendors and compliance teams rose in power post-cookie deprecation; 68% of agencies reported talent shortages in 2024. In-house studios and multivendor stacks mitigate but do not remove supplier bargaining power.

| Supplier | 2024 stat | Impact |

|---|---|---|

| 29% digital ad spend | High pricing/policy leverage | |

| Meta | 21% digital ad spend | High leverage |

| Netflix | 260m subs | Premium inventory scarcity |

| Agencies | 68% talent shortage | Higher creator fees |

What is included in the product

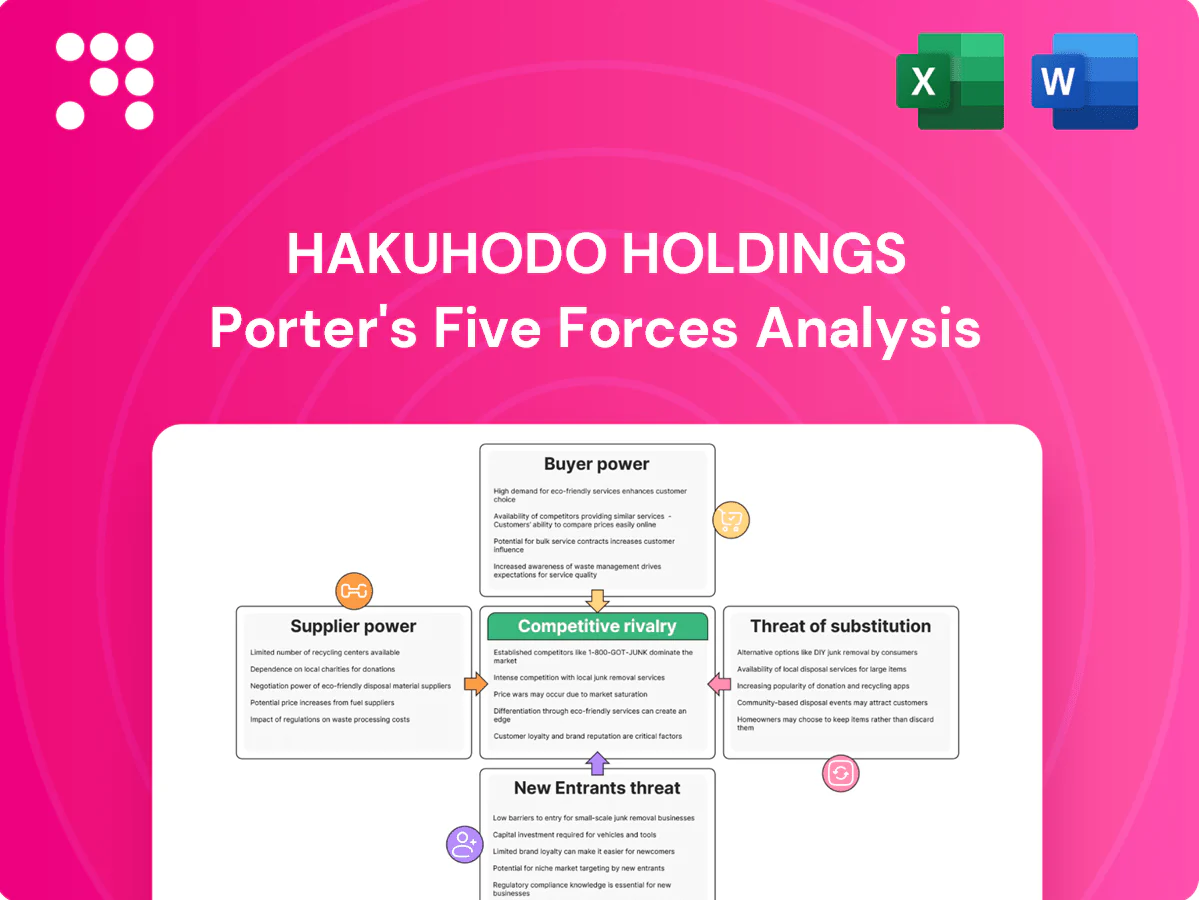

Tailored Porter's Five Forces analysis for Hakuhodo Holdings revealing competitive rivalry, buyer and supplier power, threat of entrants and substitutes, and identifies disruptive forces and market dynamics that shape pricing, profitability and barriers protecting incumbents.

Clear one-sheet Porter's Five Forces for Hakuhodo Holdings—instantly visualize competitive pressure with a customizable radar chart, swap in current data/labels, and copy clean slides into decks for rapid, boardroom-ready decisions.

Customers Bargaining Power

Large multinational advertisers

Large multinational advertisers run global RFPs and consolidate spend to extract fee discounts often in the 10–30% range, leveraging benchmarks and formal audit rights to enforce rate cards and performance; the top-tier global advertisers account for roughly 40% of industry spend, pressuring margins. Multi-year scopes commonly trade margin for volume stability, while Hakuhodo’s integrated creative+media+data offer helps defend value in negotiations by unifying billing and measurables.

Procurement-driven pricing pressure

Procurement-driven pricing pressure for Hakuhodo manifests as structured SLAs and standardized rate cards that compress fees and shorten negotiation cycles. Outcome-based models increasingly shift campaign risk to agencies, forcing tighter margin management. Sustaining premium pricing requires clear ROI attribution, especially as the global ad market exceeded $800bn in 2024. Process excellence and automation are essential to protect margins.

Switching and multi-agency rosters

Competitive pitches and project-based work in 2024 keep switching costs low as clients routinely split creative, media and digital across multi-agency rosters, creating persistent price tension; Hakuhodo’s deeper client relationships and proprietary tools raise stickiness, while demonstrable performance metrics—benchmarked against a Japan ad market of roughly ¥6.7 trillion in 2024—help reduce churn risk.

In-housing and self-serve tools

Clients increasingly build in-house media and creative teams for speed and control; self-serve and programmatic platforms accounted for over 50% of digital ad transactions in 2024, reducing agency dependency, so agencies must pivot to strategy, complex activation and analytics while offering hybrid models to retain wallet share.

- In-housing drives speed and control

- Self-serve >50% of digital ad transactions (2024)

- Agencies shift to strategy, analytics, complex activations

- Hybrid models help retain wallet share

Demand for integrated, measurable impact

- Omnichannel demand: 61% (Forrester 2024)

- Closed-loop = better terms

- Data-to-sales linkage = competitive moat

- Measurement gaps = fee compression

Clients consolidate spend, forcing agencies to prove ROI and integrate services

Major clients consolidate spend via global RFPs, extracting 10–30% fee discounts; top advertisers ≈40% of industry spend. In-housing and self-serve exceed 50% of digital transactions (2024), while omnichannel measurement demand is 61% (Forrester 2024), compressing agency margins unless ROI attribution and integrated offerings prove value.

| Metric | 2024 |

|---|---|

| Global ad market | >$800bn |

| Japan ad market | ¥6.7T |

| Top advertisers share | ~40% |

Preview the Actual Deliverable

Hakuhodo Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Hakuhodo Holdings that you'll receive after purchase—no placeholders or samples. The report covers supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry with data-driven insights and strategic implications. It's professionally formatted and ready for immediate download and use.

A Must-Have Tool for Decision-Makers

Hakuhodo Holdings faces nuanced competitive pressures—from client bargaining power and digital disruption to agency consolidation and substitute communication channels—shaping its margin and growth outlook. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings and strategic implications in detail. Get a consultant-grade report with visuals and ready-to-use Word/Excel deliverables.

Suppliers Bargaining Power

Dominant media and tech platforms

Global walled gardens command inventory and data, raising supplier leverage: Google (~29% of global digital ad spend in 2024) and Meta (~21% in 2024 per Insider Intelligence) together capture roughly half the market, letting policy changes and price moves compress agency margins. Hakuhodo’s scale strengthens negotiation, but platform concentration keeps power elevated; multi-platform planning partially offsets dependency.

Premium content and rights holders

TV networks, streaming services and sports/entertainment rights owners control scarce premium inventory, concentrating leverage over agencies like Hakuhodo; peak events (eg Super Bowl 30s spots ~$7m in 2023–24) create rate rigidity. Major streamers (Netflix ~260m paid subs in 2024) compound demand for premium audiences. Bundling and long-term rights deals can soften price spikes but demand contractual commitments. Scarcity thus sustains supplier bargaining power in key seasons.

Data, adtech, and measurement vendors

Data, DMPs, CDPs, ID graphs and verification tools are now critical for targeting and measurement in a privacy-first environment. Interoperability constraints in adtech stacks raise switching costs and can lock in vendor fees, while Hakuhodo’s integrated stacks help mitigate single-vendor risk. The ongoing deprecation of third-party cookies has increased bargaining power for privacy-compliant data suppliers and measurement vendors.

Creative talent and production houses

Regulatory and platform compliance gatekeepers

Platforms 29%+21% ad share; streamers 260m; talent gap 68%

Global platforms (Google 29% and Meta 21% of global digital ad spend in 2024) plus premium broadcasters/streamers (Netflix 260m subs in 2024) sustain high supplier leverage; Hakuhodo scale and multi-platform buys partly offset. Data/verification vendors and compliance teams rose in power post-cookie deprecation; 68% of agencies reported talent shortages in 2024. In-house studios and multivendor stacks mitigate but do not remove supplier bargaining power.

| Supplier | 2024 stat | Impact |

|---|---|---|

| 29% digital ad spend | High pricing/policy leverage | |

| Meta | 21% digital ad spend | High leverage |

| Netflix | 260m subs | Premium inventory scarcity |

| Agencies | 68% talent shortage | Higher creator fees |

What is included in the product

Tailored Porter's Five Forces analysis for Hakuhodo Holdings revealing competitive rivalry, buyer and supplier power, threat of entrants and substitutes, and identifies disruptive forces and market dynamics that shape pricing, profitability and barriers protecting incumbents.

Clear one-sheet Porter's Five Forces for Hakuhodo Holdings—instantly visualize competitive pressure with a customizable radar chart, swap in current data/labels, and copy clean slides into decks for rapid, boardroom-ready decisions.

Customers Bargaining Power

Large multinational advertisers

Large multinational advertisers run global RFPs and consolidate spend to extract fee discounts often in the 10–30% range, leveraging benchmarks and formal audit rights to enforce rate cards and performance; the top-tier global advertisers account for roughly 40% of industry spend, pressuring margins. Multi-year scopes commonly trade margin for volume stability, while Hakuhodo’s integrated creative+media+data offer helps defend value in negotiations by unifying billing and measurables.

Procurement-driven pricing pressure

Procurement-driven pricing pressure for Hakuhodo manifests as structured SLAs and standardized rate cards that compress fees and shorten negotiation cycles. Outcome-based models increasingly shift campaign risk to agencies, forcing tighter margin management. Sustaining premium pricing requires clear ROI attribution, especially as the global ad market exceeded $800bn in 2024. Process excellence and automation are essential to protect margins.

Switching and multi-agency rosters

Competitive pitches and project-based work in 2024 keep switching costs low as clients routinely split creative, media and digital across multi-agency rosters, creating persistent price tension; Hakuhodo’s deeper client relationships and proprietary tools raise stickiness, while demonstrable performance metrics—benchmarked against a Japan ad market of roughly ¥6.7 trillion in 2024—help reduce churn risk.

In-housing and self-serve tools

Clients increasingly build in-house media and creative teams for speed and control; self-serve and programmatic platforms accounted for over 50% of digital ad transactions in 2024, reducing agency dependency, so agencies must pivot to strategy, complex activation and analytics while offering hybrid models to retain wallet share.

- In-housing drives speed and control

- Self-serve >50% of digital ad transactions (2024)

- Agencies shift to strategy, analytics, complex activations

- Hybrid models help retain wallet share

Demand for integrated, measurable impact

- Omnichannel demand: 61% (Forrester 2024)

- Closed-loop = better terms

- Data-to-sales linkage = competitive moat

- Measurement gaps = fee compression

Clients consolidate spend, forcing agencies to prove ROI and integrate services

Major clients consolidate spend via global RFPs, extracting 10–30% fee discounts; top advertisers ≈40% of industry spend. In-housing and self-serve exceed 50% of digital transactions (2024), while omnichannel measurement demand is 61% (Forrester 2024), compressing agency margins unless ROI attribution and integrated offerings prove value.

| Metric | 2024 |

|---|---|

| Global ad market | >$800bn |

| Japan ad market | ¥6.7T |

| Top advertisers share | ~40% |

Preview the Actual Deliverable

Hakuhodo Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Hakuhodo Holdings that you'll receive after purchase—no placeholders or samples. The report covers supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry with data-driven insights and strategic implications. It's professionally formatted and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Hakuhodo Holdings faces nuanced competitive pressures—from client bargaining power and digital disruption to agency consolidation and substitute communication channels—shaping its margin and growth outlook. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings and strategic implications in detail. Get a consultant-grade report with visuals and ready-to-use Word/Excel deliverables.

Suppliers Bargaining Power

Dominant media and tech platforms

Global walled gardens command inventory and data, raising supplier leverage: Google (~29% of global digital ad spend in 2024) and Meta (~21% in 2024 per Insider Intelligence) together capture roughly half the market, letting policy changes and price moves compress agency margins. Hakuhodo’s scale strengthens negotiation, but platform concentration keeps power elevated; multi-platform planning partially offsets dependency.

Premium content and rights holders

TV networks, streaming services and sports/entertainment rights owners control scarce premium inventory, concentrating leverage over agencies like Hakuhodo; peak events (eg Super Bowl 30s spots ~$7m in 2023–24) create rate rigidity. Major streamers (Netflix ~260m paid subs in 2024) compound demand for premium audiences. Bundling and long-term rights deals can soften price spikes but demand contractual commitments. Scarcity thus sustains supplier bargaining power in key seasons.

Data, adtech, and measurement vendors

Data, DMPs, CDPs, ID graphs and verification tools are now critical for targeting and measurement in a privacy-first environment. Interoperability constraints in adtech stacks raise switching costs and can lock in vendor fees, while Hakuhodo’s integrated stacks help mitigate single-vendor risk. The ongoing deprecation of third-party cookies has increased bargaining power for privacy-compliant data suppliers and measurement vendors.

Creative talent and production houses

Regulatory and platform compliance gatekeepers

Platforms 29%+21% ad share; streamers 260m; talent gap 68%

Global platforms (Google 29% and Meta 21% of global digital ad spend in 2024) plus premium broadcasters/streamers (Netflix 260m subs in 2024) sustain high supplier leverage; Hakuhodo scale and multi-platform buys partly offset. Data/verification vendors and compliance teams rose in power post-cookie deprecation; 68% of agencies reported talent shortages in 2024. In-house studios and multivendor stacks mitigate but do not remove supplier bargaining power.

| Supplier | 2024 stat | Impact |

|---|---|---|

| 29% digital ad spend | High pricing/policy leverage | |

| Meta | 21% digital ad spend | High leverage |

| Netflix | 260m subs | Premium inventory scarcity |

| Agencies | 68% talent shortage | Higher creator fees |

What is included in the product

Tailored Porter's Five Forces analysis for Hakuhodo Holdings revealing competitive rivalry, buyer and supplier power, threat of entrants and substitutes, and identifies disruptive forces and market dynamics that shape pricing, profitability and barriers protecting incumbents.

Clear one-sheet Porter's Five Forces for Hakuhodo Holdings—instantly visualize competitive pressure with a customizable radar chart, swap in current data/labels, and copy clean slides into decks for rapid, boardroom-ready decisions.

Customers Bargaining Power

Large multinational advertisers

Large multinational advertisers run global RFPs and consolidate spend to extract fee discounts often in the 10–30% range, leveraging benchmarks and formal audit rights to enforce rate cards and performance; the top-tier global advertisers account for roughly 40% of industry spend, pressuring margins. Multi-year scopes commonly trade margin for volume stability, while Hakuhodo’s integrated creative+media+data offer helps defend value in negotiations by unifying billing and measurables.

Procurement-driven pricing pressure

Procurement-driven pricing pressure for Hakuhodo manifests as structured SLAs and standardized rate cards that compress fees and shorten negotiation cycles. Outcome-based models increasingly shift campaign risk to agencies, forcing tighter margin management. Sustaining premium pricing requires clear ROI attribution, especially as the global ad market exceeded $800bn in 2024. Process excellence and automation are essential to protect margins.

Switching and multi-agency rosters

Competitive pitches and project-based work in 2024 keep switching costs low as clients routinely split creative, media and digital across multi-agency rosters, creating persistent price tension; Hakuhodo’s deeper client relationships and proprietary tools raise stickiness, while demonstrable performance metrics—benchmarked against a Japan ad market of roughly ¥6.7 trillion in 2024—help reduce churn risk.

In-housing and self-serve tools

Clients increasingly build in-house media and creative teams for speed and control; self-serve and programmatic platforms accounted for over 50% of digital ad transactions in 2024, reducing agency dependency, so agencies must pivot to strategy, complex activation and analytics while offering hybrid models to retain wallet share.

- In-housing drives speed and control

- Self-serve >50% of digital ad transactions (2024)

- Agencies shift to strategy, analytics, complex activations

- Hybrid models help retain wallet share

Demand for integrated, measurable impact

- Omnichannel demand: 61% (Forrester 2024)

- Closed-loop = better terms

- Data-to-sales linkage = competitive moat

- Measurement gaps = fee compression

Clients consolidate spend, forcing agencies to prove ROI and integrate services

Major clients consolidate spend via global RFPs, extracting 10–30% fee discounts; top advertisers ≈40% of industry spend. In-housing and self-serve exceed 50% of digital transactions (2024), while omnichannel measurement demand is 61% (Forrester 2024), compressing agency margins unless ROI attribution and integrated offerings prove value.

| Metric | 2024 |

|---|---|

| Global ad market | >$800bn |

| Japan ad market | ¥6.7T |

| Top advertisers share | ~40% |

Preview the Actual Deliverable

Hakuhodo Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Hakuhodo Holdings that you'll receive after purchase—no placeholders or samples. The report covers supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry with data-driven insights and strategic implications. It's professionally formatted and ready for immediate download and use.