Haleon SWOT Analysis

Your Strategic Toolkit Starts Here

Haleon shows strong global OTC brands and resilient cash flows but faces competitive pressure and regulatory risks that could affect growth. Our full SWOT unpacks market positioning, product pipeline, and strategic levers in actionable detail. Purchase the complete report for a professionally formatted Word and editable Excel analysis to plan and invest with confidence.

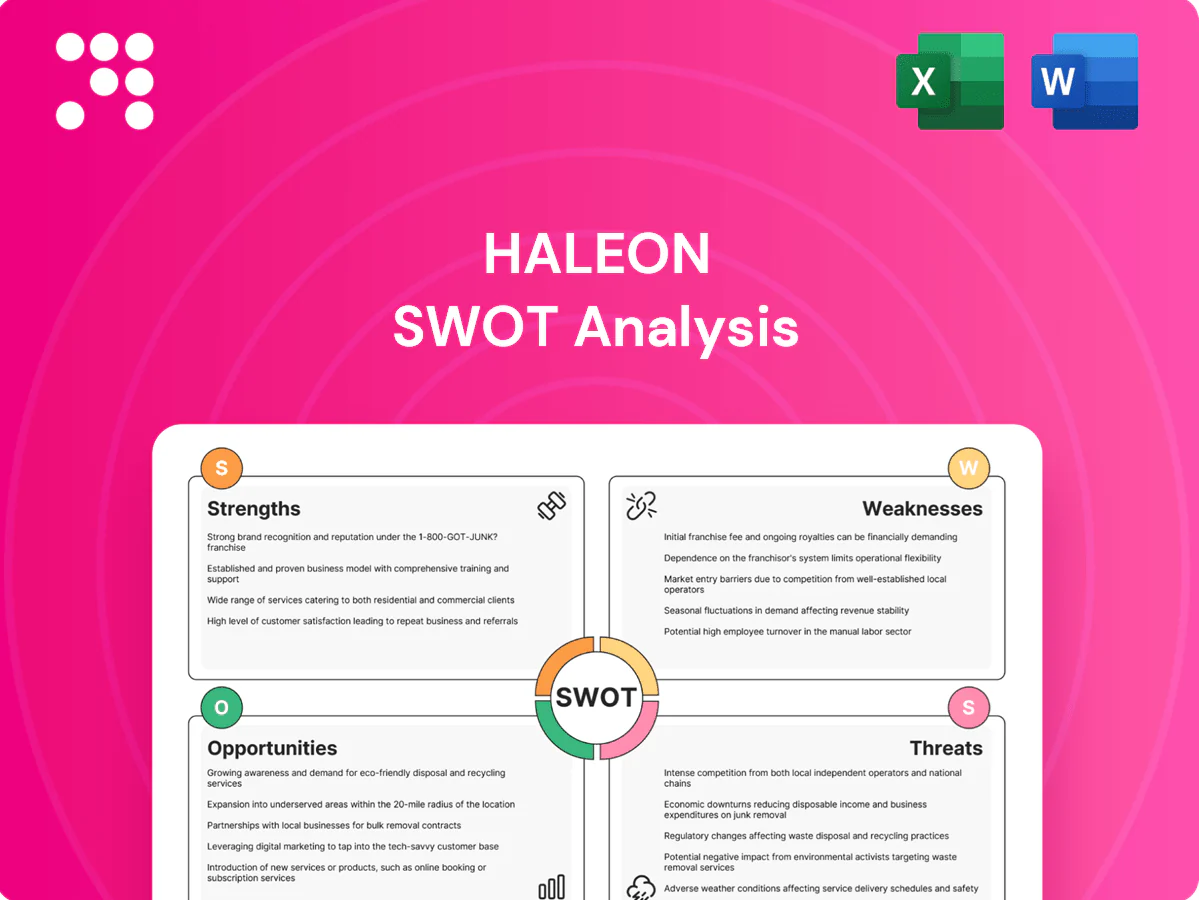

Strengths

Powerhouse brand portfolio

Haleon owns category-leading, science-backed brands such as Sensodyne, Voltaren, Centrum and Panadol that command premium pricing across oral care, pain relief, respiratory and VMS. Strong brand equity drives repeat purchase and pharmacist recommendation, supporting stable margins. Broad consumer awareness lowers incremental marketing spend and increases ROI. Brand stretch enables efficient line extensions across formats and need-states.

Global scale and distribution

Haleon, spun out of GSK in 2022, reaches 100+ markets and manages a portfolio of over 50 consumer-health brands including Sensodyne, Voltaren and Panadol. This wide geographic footprint and deep retail, pharmacy and e-commerce penetration boosts shelf presence and availability. Scale in procurement, manufacturing and media buying reduces unit costs, while omnichannel route-to-market expertise shortens launch timelines and cushions local disruptions.

Science-led R&D and regulatory expertise

Robust clinical substantiation (Haleon reported c.£7.9bn sales in 2023) underpins premium pricing and claims, supporting higher margins on brands like Sensodyne and Voltaren. In-house and partnered R&D accelerates incremental innovation and reformulation cycles. Strong quality/regulatory compliance reduces approval friction across 100+ markets, and trusted HCP engagement boosts recommendation rates.

Category leadership and focus

Haleon, spun out from GSK in 2022, concentrates on everyday health categories—oral care (Sensodyne, Parodontax) and pain relief (Panadol)—allowing deeper channel execution and consumer insight rather than broad diversification.

Category leadership drives shelf priority and proprietary POS and NPD data, while focused portfolios streamline capital allocation to high-ROI brands and scale in priority categories raises barriers for smaller challengers.

- Focused portfolio

- Oral care & pain leadership

- Superior shelf/data access

- Efficient capital allocation

- Scale deters challengers

Resilient, everyday demand

Haleons OTC and self-care products face relatively inelastic demand, supporting steady sales—Haleon reported approximately £7.9bn in FY 2024 revenue, driven by staples like Sensodyne, Voltaren and Centrum. Preventive and maintenance behaviors sustain consumption across cycles, while diversification across indications (oral care, pain, vitamins) reduces category-specific shocks. Seasonal lines (cold/flu, allergy) create predictable quarterly uplifts, aiding cashflow planning.

- Resilient staples: inelastic demand

- Behavioral tailwinds: preventive consumption

- Portfolio diversification: lowers shock risk

- Seasonality: predictable revenue cadence

Science-backed OTC portfolio, global scale and resilient demand driving c.£7.9bn FY2024

Category-leading, science-backed brands (Sensodyne, Voltaren, Panadol) support premium pricing and repeat purchase.

Scale across 100+ markets and 50+ brands delivers procurement, manufacturing and route-to-market efficiencies.

Resilient OTC demand underpinned FY2024 revenue of c.£7.9bn, aiding predictable cashflow and margin sustainability.

| Metric | Value |

|---|---|

| FY2024 revenue | c.£7.9bn |

| Markets | 100+ |

| Brands | 50+ |

What is included in the product

Provides a concise SWOT overview of Haleon, detailing its internal strengths and weaknesses and external opportunities and threats to assess competitive positioning and strategic priorities. Highlights core capabilities, market growth drivers, operational gaps, and risks shaping Haleon’s future performance.

Provides a focused SWOT assessment of Haleon to quickly surface strategic risks and growth levers, enabling faster, evidence-based decisions and streamlined stakeholder communication.

Weaknesses

Brand and market concentration

Haleon remains dependent on a handful of power brands—Sensodyne and Centrum notably—after reporting approximately £6.9bn revenue in 2023, concentrating sales risk if market share slips. Aggressive competitor promotions or supply disruptions could disproportionately dent quarterly results given this concentration. Heavy exposure to developed markets limits upside versus faster-growing EMs, and portfolio gaps constrain cross-selling across categories and channels.

Price sensitivity and private label pressure

Retailer brands and value players, with UK grocery private-label share near 47% in 2023 (NielsenIQ), compress prices in commoditizing subcategories and force promotional activity that erodes gross margins and brand equity. Consumers historically trade down in downturns (UK inflation peaked 11.1% in Oct 2022), weakening loyalty. Ongoing trade-term pressure squeezes net revenue realization for Haleon.

Incremental innovation cadence

OTC innovation at Haleon has skewed toward line extensions rather than step-change breakthroughs, a trend persistent since the GSK demerger in 2022. Regulatory claim constraints and guardrails limit bold differentiation, while rapid copycating in mass-market channels compresses advantage windows. Rising R&D input faces diminishing marginal returns as incremental tweaks dominate pipelines.

Supply chain complexity

Multi-plant, multi-country operations increase coordination risk and escalate logistics and overhead costs, stressing margins and responsiveness. Volatility in APIs and packaging inputs has repeatedly disrupted service levels across brands. Regulatory compliance and serialization requirements raise capital and operating expenses. Seasonal demand forces capacity rebalancing that strains planning and drives expedited-costs.

- Coordination risk: multi-plant/multi-country

- Input volatility: APIs & packaging

- Regulatory burden: compliance & serialization

- Seasonality: capacity rebalancing strains planning

Litigation and recall exposure

Product liability, labeling disputes and advertising challenges pose persistent risks for Haleon; any quality lapse can prompt recalls and reputational damage. Legal costs and settlements are unpredictable, and heightened regulatory scrutiny increases documentation and testing burdens. These exposures can strain margins and divert management focus.

- Product liability risk

- Recall/reputation impact

- Unpredictable legal costs

- Higher compliance burden

Concentrated portfolio and retail pressure heighten downside after £6.9bn sales

Haleon’s portfolio concentration around Sensodyne and Centrum leaves revenue exposure after £6.9bn sales in 2023, amplifying downside from market-share loss or supply shocks. Heavy developed‑market mix and 47% UK private‑label grocery share (NielsenIQ 2023) compress pricing power, while incremental R&D and regulatory constraints limit breakthrough innovation. Multi‑plant complexity, input volatility and product‑liability risks raise costs and operational strain.

| Metric | Value |

|---|---|

| Revenue (2023) | £6.9bn |

| UK private‑label share (2023) | 47% |

| UK inflation peak | 11.1% (Oct 2022) |

What You See Is What You Get

Haleon SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. The file shown is the real, editable SWOT analysis you'll download post-purchase.

Your Strategic Toolkit Starts Here

Haleon shows strong global OTC brands and resilient cash flows but faces competitive pressure and regulatory risks that could affect growth. Our full SWOT unpacks market positioning, product pipeline, and strategic levers in actionable detail. Purchase the complete report for a professionally formatted Word and editable Excel analysis to plan and invest with confidence.

Strengths

Powerhouse brand portfolio

Haleon owns category-leading, science-backed brands such as Sensodyne, Voltaren, Centrum and Panadol that command premium pricing across oral care, pain relief, respiratory and VMS. Strong brand equity drives repeat purchase and pharmacist recommendation, supporting stable margins. Broad consumer awareness lowers incremental marketing spend and increases ROI. Brand stretch enables efficient line extensions across formats and need-states.

Global scale and distribution

Haleon, spun out of GSK in 2022, reaches 100+ markets and manages a portfolio of over 50 consumer-health brands including Sensodyne, Voltaren and Panadol. This wide geographic footprint and deep retail, pharmacy and e-commerce penetration boosts shelf presence and availability. Scale in procurement, manufacturing and media buying reduces unit costs, while omnichannel route-to-market expertise shortens launch timelines and cushions local disruptions.

Science-led R&D and regulatory expertise

Robust clinical substantiation (Haleon reported c.£7.9bn sales in 2023) underpins premium pricing and claims, supporting higher margins on brands like Sensodyne and Voltaren. In-house and partnered R&D accelerates incremental innovation and reformulation cycles. Strong quality/regulatory compliance reduces approval friction across 100+ markets, and trusted HCP engagement boosts recommendation rates.

Category leadership and focus

Haleon, spun out from GSK in 2022, concentrates on everyday health categories—oral care (Sensodyne, Parodontax) and pain relief (Panadol)—allowing deeper channel execution and consumer insight rather than broad diversification.

Category leadership drives shelf priority and proprietary POS and NPD data, while focused portfolios streamline capital allocation to high-ROI brands and scale in priority categories raises barriers for smaller challengers.

- Focused portfolio

- Oral care & pain leadership

- Superior shelf/data access

- Efficient capital allocation

- Scale deters challengers

Resilient, everyday demand

Haleons OTC and self-care products face relatively inelastic demand, supporting steady sales—Haleon reported approximately £7.9bn in FY 2024 revenue, driven by staples like Sensodyne, Voltaren and Centrum. Preventive and maintenance behaviors sustain consumption across cycles, while diversification across indications (oral care, pain, vitamins) reduces category-specific shocks. Seasonal lines (cold/flu, allergy) create predictable quarterly uplifts, aiding cashflow planning.

- Resilient staples: inelastic demand

- Behavioral tailwinds: preventive consumption

- Portfolio diversification: lowers shock risk

- Seasonality: predictable revenue cadence

Science-backed OTC portfolio, global scale and resilient demand driving c.£7.9bn FY2024

Category-leading, science-backed brands (Sensodyne, Voltaren, Panadol) support premium pricing and repeat purchase.

Scale across 100+ markets and 50+ brands delivers procurement, manufacturing and route-to-market efficiencies.

Resilient OTC demand underpinned FY2024 revenue of c.£7.9bn, aiding predictable cashflow and margin sustainability.

| Metric | Value |

|---|---|

| FY2024 revenue | c.£7.9bn |

| Markets | 100+ |

| Brands | 50+ |

What is included in the product

Provides a concise SWOT overview of Haleon, detailing its internal strengths and weaknesses and external opportunities and threats to assess competitive positioning and strategic priorities. Highlights core capabilities, market growth drivers, operational gaps, and risks shaping Haleon’s future performance.

Provides a focused SWOT assessment of Haleon to quickly surface strategic risks and growth levers, enabling faster, evidence-based decisions and streamlined stakeholder communication.

Weaknesses

Brand and market concentration

Haleon remains dependent on a handful of power brands—Sensodyne and Centrum notably—after reporting approximately £6.9bn revenue in 2023, concentrating sales risk if market share slips. Aggressive competitor promotions or supply disruptions could disproportionately dent quarterly results given this concentration. Heavy exposure to developed markets limits upside versus faster-growing EMs, and portfolio gaps constrain cross-selling across categories and channels.

Price sensitivity and private label pressure

Retailer brands and value players, with UK grocery private-label share near 47% in 2023 (NielsenIQ), compress prices in commoditizing subcategories and force promotional activity that erodes gross margins and brand equity. Consumers historically trade down in downturns (UK inflation peaked 11.1% in Oct 2022), weakening loyalty. Ongoing trade-term pressure squeezes net revenue realization for Haleon.

Incremental innovation cadence

OTC innovation at Haleon has skewed toward line extensions rather than step-change breakthroughs, a trend persistent since the GSK demerger in 2022. Regulatory claim constraints and guardrails limit bold differentiation, while rapid copycating in mass-market channels compresses advantage windows. Rising R&D input faces diminishing marginal returns as incremental tweaks dominate pipelines.

Supply chain complexity

Multi-plant, multi-country operations increase coordination risk and escalate logistics and overhead costs, stressing margins and responsiveness. Volatility in APIs and packaging inputs has repeatedly disrupted service levels across brands. Regulatory compliance and serialization requirements raise capital and operating expenses. Seasonal demand forces capacity rebalancing that strains planning and drives expedited-costs.

- Coordination risk: multi-plant/multi-country

- Input volatility: APIs & packaging

- Regulatory burden: compliance & serialization

- Seasonality: capacity rebalancing strains planning

Litigation and recall exposure

Product liability, labeling disputes and advertising challenges pose persistent risks for Haleon; any quality lapse can prompt recalls and reputational damage. Legal costs and settlements are unpredictable, and heightened regulatory scrutiny increases documentation and testing burdens. These exposures can strain margins and divert management focus.

- Product liability risk

- Recall/reputation impact

- Unpredictable legal costs

- Higher compliance burden

Concentrated portfolio and retail pressure heighten downside after £6.9bn sales

Haleon’s portfolio concentration around Sensodyne and Centrum leaves revenue exposure after £6.9bn sales in 2023, amplifying downside from market-share loss or supply shocks. Heavy developed‑market mix and 47% UK private‑label grocery share (NielsenIQ 2023) compress pricing power, while incremental R&D and regulatory constraints limit breakthrough innovation. Multi‑plant complexity, input volatility and product‑liability risks raise costs and operational strain.

| Metric | Value |

|---|---|

| Revenue (2023) | £6.9bn |

| UK private‑label share (2023) | 47% |

| UK inflation peak | 11.1% (Oct 2022) |

What You See Is What You Get

Haleon SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. The file shown is the real, editable SWOT analysis you'll download post-purchase.

Description

Your Strategic Toolkit Starts Here

Haleon shows strong global OTC brands and resilient cash flows but faces competitive pressure and regulatory risks that could affect growth. Our full SWOT unpacks market positioning, product pipeline, and strategic levers in actionable detail. Purchase the complete report for a professionally formatted Word and editable Excel analysis to plan and invest with confidence.

Strengths

Powerhouse brand portfolio

Haleon owns category-leading, science-backed brands such as Sensodyne, Voltaren, Centrum and Panadol that command premium pricing across oral care, pain relief, respiratory and VMS. Strong brand equity drives repeat purchase and pharmacist recommendation, supporting stable margins. Broad consumer awareness lowers incremental marketing spend and increases ROI. Brand stretch enables efficient line extensions across formats and need-states.

Global scale and distribution

Haleon, spun out of GSK in 2022, reaches 100+ markets and manages a portfolio of over 50 consumer-health brands including Sensodyne, Voltaren and Panadol. This wide geographic footprint and deep retail, pharmacy and e-commerce penetration boosts shelf presence and availability. Scale in procurement, manufacturing and media buying reduces unit costs, while omnichannel route-to-market expertise shortens launch timelines and cushions local disruptions.

Science-led R&D and regulatory expertise

Robust clinical substantiation (Haleon reported c.£7.9bn sales in 2023) underpins premium pricing and claims, supporting higher margins on brands like Sensodyne and Voltaren. In-house and partnered R&D accelerates incremental innovation and reformulation cycles. Strong quality/regulatory compliance reduces approval friction across 100+ markets, and trusted HCP engagement boosts recommendation rates.

Category leadership and focus

Haleon, spun out from GSK in 2022, concentrates on everyday health categories—oral care (Sensodyne, Parodontax) and pain relief (Panadol)—allowing deeper channel execution and consumer insight rather than broad diversification.

Category leadership drives shelf priority and proprietary POS and NPD data, while focused portfolios streamline capital allocation to high-ROI brands and scale in priority categories raises barriers for smaller challengers.

- Focused portfolio

- Oral care & pain leadership

- Superior shelf/data access

- Efficient capital allocation

- Scale deters challengers

Resilient, everyday demand

Haleons OTC and self-care products face relatively inelastic demand, supporting steady sales—Haleon reported approximately £7.9bn in FY 2024 revenue, driven by staples like Sensodyne, Voltaren and Centrum. Preventive and maintenance behaviors sustain consumption across cycles, while diversification across indications (oral care, pain, vitamins) reduces category-specific shocks. Seasonal lines (cold/flu, allergy) create predictable quarterly uplifts, aiding cashflow planning.

- Resilient staples: inelastic demand

- Behavioral tailwinds: preventive consumption

- Portfolio diversification: lowers shock risk

- Seasonality: predictable revenue cadence

Science-backed OTC portfolio, global scale and resilient demand driving c.£7.9bn FY2024

Category-leading, science-backed brands (Sensodyne, Voltaren, Panadol) support premium pricing and repeat purchase.

Scale across 100+ markets and 50+ brands delivers procurement, manufacturing and route-to-market efficiencies.

Resilient OTC demand underpinned FY2024 revenue of c.£7.9bn, aiding predictable cashflow and margin sustainability.

| Metric | Value |

|---|---|

| FY2024 revenue | c.£7.9bn |

| Markets | 100+ |

| Brands | 50+ |

What is included in the product

Provides a concise SWOT overview of Haleon, detailing its internal strengths and weaknesses and external opportunities and threats to assess competitive positioning and strategic priorities. Highlights core capabilities, market growth drivers, operational gaps, and risks shaping Haleon’s future performance.

Provides a focused SWOT assessment of Haleon to quickly surface strategic risks and growth levers, enabling faster, evidence-based decisions and streamlined stakeholder communication.

Weaknesses

Brand and market concentration

Haleon remains dependent on a handful of power brands—Sensodyne and Centrum notably—after reporting approximately £6.9bn revenue in 2023, concentrating sales risk if market share slips. Aggressive competitor promotions or supply disruptions could disproportionately dent quarterly results given this concentration. Heavy exposure to developed markets limits upside versus faster-growing EMs, and portfolio gaps constrain cross-selling across categories and channels.

Price sensitivity and private label pressure

Retailer brands and value players, with UK grocery private-label share near 47% in 2023 (NielsenIQ), compress prices in commoditizing subcategories and force promotional activity that erodes gross margins and brand equity. Consumers historically trade down in downturns (UK inflation peaked 11.1% in Oct 2022), weakening loyalty. Ongoing trade-term pressure squeezes net revenue realization for Haleon.

Incremental innovation cadence

OTC innovation at Haleon has skewed toward line extensions rather than step-change breakthroughs, a trend persistent since the GSK demerger in 2022. Regulatory claim constraints and guardrails limit bold differentiation, while rapid copycating in mass-market channels compresses advantage windows. Rising R&D input faces diminishing marginal returns as incremental tweaks dominate pipelines.

Supply chain complexity

Multi-plant, multi-country operations increase coordination risk and escalate logistics and overhead costs, stressing margins and responsiveness. Volatility in APIs and packaging inputs has repeatedly disrupted service levels across brands. Regulatory compliance and serialization requirements raise capital and operating expenses. Seasonal demand forces capacity rebalancing that strains planning and drives expedited-costs.

- Coordination risk: multi-plant/multi-country

- Input volatility: APIs & packaging

- Regulatory burden: compliance & serialization

- Seasonality: capacity rebalancing strains planning

Litigation and recall exposure

Product liability, labeling disputes and advertising challenges pose persistent risks for Haleon; any quality lapse can prompt recalls and reputational damage. Legal costs and settlements are unpredictable, and heightened regulatory scrutiny increases documentation and testing burdens. These exposures can strain margins and divert management focus.

- Product liability risk

- Recall/reputation impact

- Unpredictable legal costs

- Higher compliance burden

Concentrated portfolio and retail pressure heighten downside after £6.9bn sales

Haleon’s portfolio concentration around Sensodyne and Centrum leaves revenue exposure after £6.9bn sales in 2023, amplifying downside from market-share loss or supply shocks. Heavy developed‑market mix and 47% UK private‑label grocery share (NielsenIQ 2023) compress pricing power, while incremental R&D and regulatory constraints limit breakthrough innovation. Multi‑plant complexity, input volatility and product‑liability risks raise costs and operational strain.

| Metric | Value |

|---|---|

| Revenue (2023) | £6.9bn |

| UK private‑label share (2023) | 47% |

| UK inflation peak | 11.1% (Oct 2022) |

What You See Is What You Get

Haleon SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. The file shown is the real, editable SWOT analysis you'll download post-purchase.