Halkbank Business Model Canvas

Unlock a leading bank's Business Model Canvas for retail & SME value creation

Unlock the full strategic blueprint behind Halkbank's business model. This concise Business Model Canvas exposes how Halkbank creates value across retail and SME segments, leverages partnerships, and monetizes services while managing risks. Purchase the complete, editable Word & Excel canvas for detailed, section-by-section insights and actionable recommendations.

Partnerships

Turkish government and public institutions

Collaboration with the Treasury and ministries aligns Halkbank lending to national development priorities, supporting credit to sectors where SMEs — over 99% of Turkish firms — are concentrated. Access to Treasury-backed guarantee schemes and subsidized programs lowers counterparty risk and pricing for priority loans. Public infrastructure projects supply stable corporate and project finance pipelines, while policy coordination enables counter-cyclical credit expansion.

Central Bank of Türkiye and regulators

Monetary operations and CBRT reserve facilities underpin Halkbank liquidity management by providing short-term funding and reserve instruments. Regulatory guidance from BDDK and Basel III standards (minimum CET1 4.5% and total capital 8%) shapes capital, risk and consumer protection rules. Participation in national clearing infrastructures (Takasbank, BKM) ensures transaction reliability. Prudential supervision strengthens market confidence.

International development banks and DFIs

Partnerships with EBRD, IFC and similar DFIs provide Halkbank with long-tenor funding (typically 5–15 years), enabling SME, green and inclusive finance growth. Technical assistance programs from these partners strengthen credit frameworks and digital lending for SMEs. Co-financing structures diversify funding, lowering single-lender concentration and currency exposure. Access to DFI best practices enhances the bank’s sustainability and ESG frameworks.

Correspondent banks and payment networks

Halkbank leverages correspondent banks and payment networks to enable trade finance and cross-border payments. SWIFT (11,000+ institutions in 200+ countries) and card schemes Visa/Mastercard (operations in 200+ countries, 160+ currencies) expand transactional reach. Multicurrency settlement supports exporters/importers while network partnerships enhance speed, security and acceptance.

- Correspondent reach: SWIFT 11,000+ nodes

- Card schemes: 200+ countries, 160+ currencies

- Benefits: faster settlement, stronger security, wider acceptance

Fintechs and technology vendors

Fintech and technology vendors enable Halkbank to accelerate digital onboarding, KYC and payments via API partnerships, cutting onboarding times and supporting a 2024 digital payments volume exceeding 500 million transactions.

Core banking, cybersecurity and cloud providers boost scalability and resilience, underpinning Halkbank’s push to increase transaction capacity and regulatory compliance in 2024.

Data analytics vendors improve credit underwriting and personalization, feeding models that reduced default prediction errors and powered targeted product offers in 2024; co-innovation with partners shortens time-to-market for new products.

- API partners: faster onboarding, KYC, payments

- Core banking & cloud: scalability, compliance

- Cybersecurity: resilience against threats

- Data analytics: better underwriting, personalization

- Co-innovation: quicker product launches

Public-DFI-fintech tie-ups enable subsidized SME loans, long-term funding and 500M+ digital payments

Halkbank’s key partnerships with Treasury, DFIs (EBRD/IFC), correspondent banks and fintechs enable subsidized SME credit, long-tenor funding (DFI loans 5–15y), cross-border services (SWIFT 11,000+ nodes) and 2024 digital payments >500M tx. Regulatory and central bank links secure liquidity and compliance; tech vendors shorten onboarding and improve underwriting accuracy.

| Partner | Key metric |

|---|---|

| Treasury | SME focus; guarantee schemes |

| DFIs | 5–15y funding |

| SWIFT/cards | 11,000+/200+ countries |

| Fintechs | 2024: >500M payments |

What is included in the product

A comprehensive pre-written Business Model Canvas for Halkbank covering customer segments, value propositions, channels, revenue streams, key activities, resources, partners, cost structure and relationships, reflecting real-world operations and competitive advantages; includes SWOT-linked insights and a polished design ideal for presentations, investor discussions and strategic decision-making.

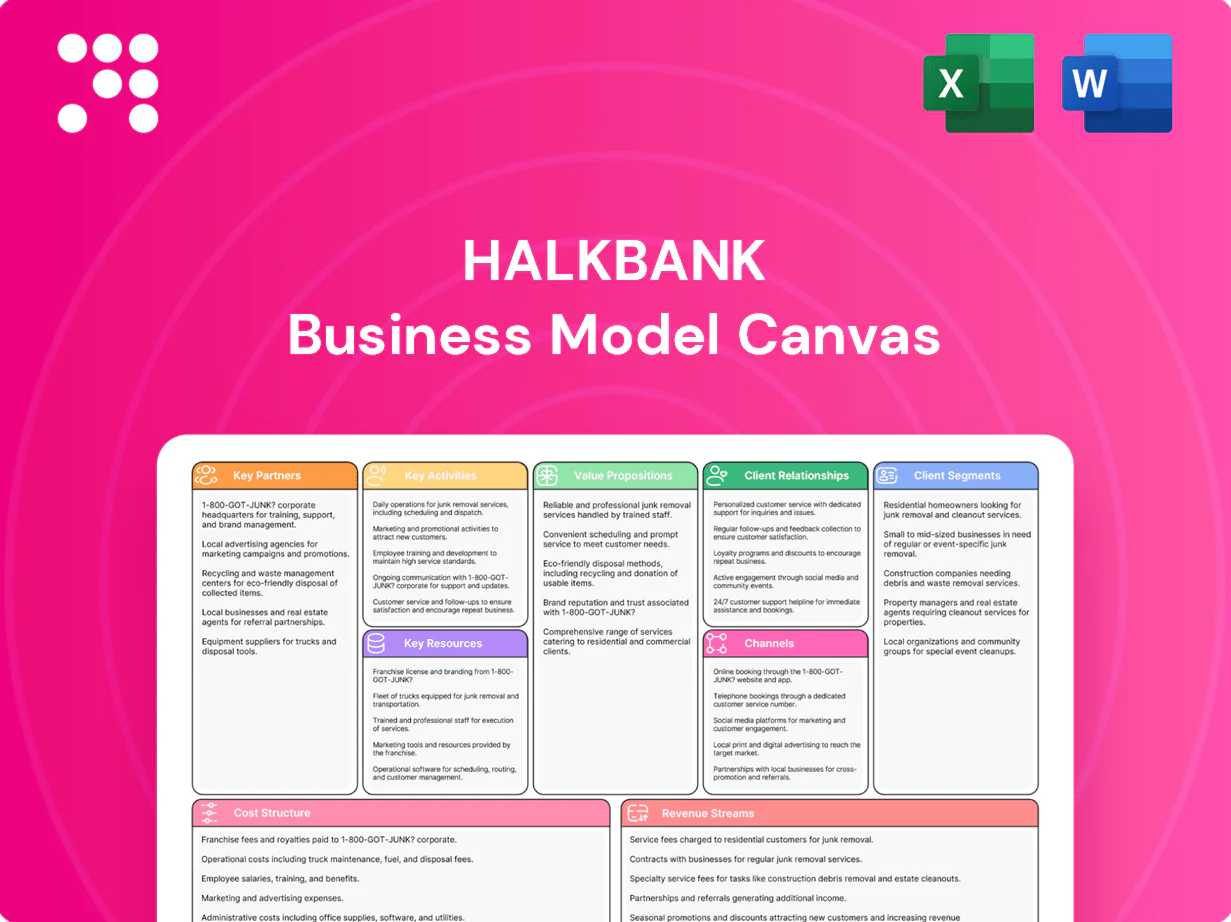

High-level view of Halkbank’s business model with editable cells, condensing its retail, SME and corporate banking strategies into a one-page snapshot for quick review and boardroom-ready discussion.

Activities

Deposit mobilization and liquidity management

Acquire retail and corporate deposits through competitive rates, enhanced digital and branch service, and trust built on Halkbank’s state-backed reputation to deepen stable funding. Optimize funding mix and maturities to lower cost of funds by shifting toward low-cost current accounts and term retail deposits. Manage liquidity buffers within BRSA limits and execute money market and repo operations as needed to meet short-term needs.

Lending and credit underwriting

Halkbank extends tailored loans to individuals, SMEs and corporates, structuring tenor, pricing and repayment to client cash flows and sector needs; in 2024 it served over 10 million customers with a broad retail and commercial product mix. The bank applies quantitative risk scoring, collateral valuation and covenant frameworks to underwrite exposures and price risk. Portfolios are actively monitored with early-warning indicators to preserve asset quality and nonperforming loan ratios. Halkbank channels targeted credit lines to priority sectors such as SMEs, exporters and construction to support growth and employment.

Risk, compliance, and governance

Operate robust credit, market and operational risk controls with regular portfolio limits, credit scoring and loss forecasting; maintain Basel III capital standards including a common equity tier 1 minimum of 4.5% plus a 2.5% conservation buffer. Enforce AML/CFT, sanctions and KYC processes compliant with Turkish and international rules, monitor suspicious activity and report to authorities. Align provisioning and reporting with IFRS 9 and local BRSA requirements, and conduct periodic stress tests and forward-looking provisioning to safeguard capital.

Trade finance and international banking

Halkbank issues letters of credit, performance and bid guarantees and manages collections to support exporters and importers, while providing FX, hedging and cross-border settlement services. It structures supply chain and export finance with correspondent partner banks and facilitates state-backed trade support programs to de-risk transactions. Core focus is ensuring liquidity and payment certainty across Turkish foreign trade corridors.

- Issue LCs and guarantees

- FX, hedging, settlements

- Supply chain & export finance with partners

- Facilitate state-backed trade support

Digital delivery and customer service

Halkbank develops mobile, internet and API-based services to expand digital delivery, streamlines onboarding and payments for speed and convenience, operates contact centers alongside RM-led service for complex needs, and leverages customer data to personalize offers and reduce churn.

- mobile, internet, API services

- fast onboarding & payments

- contact centers + RM-led support

- data-driven personalization & churn reduction

Low-cost deposits drive lending to 10M customers

Acquire deposits via state-backed trust, optimize funding mix toward low-cost current accounts, manage liquidity per BRSA; extend tailored retail/SME/corporate loans (served over 10 million customers in 2024) with quantitative underwriting and active monitoring; enforce credit/market/operational risk, IFRS 9 provisioning and Basel III CET1 minimum 4.5% plus 2.5% buffer; operate trade finance, FX hedging and digital channels.

| Metric | 2024 |

|---|---|

| Customers | over 10 million |

| CET1 minimum | 4.5% + 2.5% buffer |

Delivered as Displayed

Business Model Canvas

The document previewed here is the actual Halkbank Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this identical file with all content included. Files are delivered ready-to-edit in Word and Excel formats for immediate use and presentation.

Unlock a leading bank's Business Model Canvas for retail & SME value creation

Unlock the full strategic blueprint behind Halkbank's business model. This concise Business Model Canvas exposes how Halkbank creates value across retail and SME segments, leverages partnerships, and monetizes services while managing risks. Purchase the complete, editable Word & Excel canvas for detailed, section-by-section insights and actionable recommendations.

Partnerships

Turkish government and public institutions

Collaboration with the Treasury and ministries aligns Halkbank lending to national development priorities, supporting credit to sectors where SMEs — over 99% of Turkish firms — are concentrated. Access to Treasury-backed guarantee schemes and subsidized programs lowers counterparty risk and pricing for priority loans. Public infrastructure projects supply stable corporate and project finance pipelines, while policy coordination enables counter-cyclical credit expansion.

Central Bank of Türkiye and regulators

Monetary operations and CBRT reserve facilities underpin Halkbank liquidity management by providing short-term funding and reserve instruments. Regulatory guidance from BDDK and Basel III standards (minimum CET1 4.5% and total capital 8%) shapes capital, risk and consumer protection rules. Participation in national clearing infrastructures (Takasbank, BKM) ensures transaction reliability. Prudential supervision strengthens market confidence.

International development banks and DFIs

Partnerships with EBRD, IFC and similar DFIs provide Halkbank with long-tenor funding (typically 5–15 years), enabling SME, green and inclusive finance growth. Technical assistance programs from these partners strengthen credit frameworks and digital lending for SMEs. Co-financing structures diversify funding, lowering single-lender concentration and currency exposure. Access to DFI best practices enhances the bank’s sustainability and ESG frameworks.

Correspondent banks and payment networks

Halkbank leverages correspondent banks and payment networks to enable trade finance and cross-border payments. SWIFT (11,000+ institutions in 200+ countries) and card schemes Visa/Mastercard (operations in 200+ countries, 160+ currencies) expand transactional reach. Multicurrency settlement supports exporters/importers while network partnerships enhance speed, security and acceptance.

- Correspondent reach: SWIFT 11,000+ nodes

- Card schemes: 200+ countries, 160+ currencies

- Benefits: faster settlement, stronger security, wider acceptance

Fintechs and technology vendors

Fintech and technology vendors enable Halkbank to accelerate digital onboarding, KYC and payments via API partnerships, cutting onboarding times and supporting a 2024 digital payments volume exceeding 500 million transactions.

Core banking, cybersecurity and cloud providers boost scalability and resilience, underpinning Halkbank’s push to increase transaction capacity and regulatory compliance in 2024.

Data analytics vendors improve credit underwriting and personalization, feeding models that reduced default prediction errors and powered targeted product offers in 2024; co-innovation with partners shortens time-to-market for new products.

- API partners: faster onboarding, KYC, payments

- Core banking & cloud: scalability, compliance

- Cybersecurity: resilience against threats

- Data analytics: better underwriting, personalization

- Co-innovation: quicker product launches

Public-DFI-fintech tie-ups enable subsidized SME loans, long-term funding and 500M+ digital payments

Halkbank’s key partnerships with Treasury, DFIs (EBRD/IFC), correspondent banks and fintechs enable subsidized SME credit, long-tenor funding (DFI loans 5–15y), cross-border services (SWIFT 11,000+ nodes) and 2024 digital payments >500M tx. Regulatory and central bank links secure liquidity and compliance; tech vendors shorten onboarding and improve underwriting accuracy.

| Partner | Key metric |

|---|---|

| Treasury | SME focus; guarantee schemes |

| DFIs | 5–15y funding |

| SWIFT/cards | 11,000+/200+ countries |

| Fintechs | 2024: >500M payments |

What is included in the product

A comprehensive pre-written Business Model Canvas for Halkbank covering customer segments, value propositions, channels, revenue streams, key activities, resources, partners, cost structure and relationships, reflecting real-world operations and competitive advantages; includes SWOT-linked insights and a polished design ideal for presentations, investor discussions and strategic decision-making.

High-level view of Halkbank’s business model with editable cells, condensing its retail, SME and corporate banking strategies into a one-page snapshot for quick review and boardroom-ready discussion.

Activities

Deposit mobilization and liquidity management

Acquire retail and corporate deposits through competitive rates, enhanced digital and branch service, and trust built on Halkbank’s state-backed reputation to deepen stable funding. Optimize funding mix and maturities to lower cost of funds by shifting toward low-cost current accounts and term retail deposits. Manage liquidity buffers within BRSA limits and execute money market and repo operations as needed to meet short-term needs.

Lending and credit underwriting

Halkbank extends tailored loans to individuals, SMEs and corporates, structuring tenor, pricing and repayment to client cash flows and sector needs; in 2024 it served over 10 million customers with a broad retail and commercial product mix. The bank applies quantitative risk scoring, collateral valuation and covenant frameworks to underwrite exposures and price risk. Portfolios are actively monitored with early-warning indicators to preserve asset quality and nonperforming loan ratios. Halkbank channels targeted credit lines to priority sectors such as SMEs, exporters and construction to support growth and employment.

Risk, compliance, and governance

Operate robust credit, market and operational risk controls with regular portfolio limits, credit scoring and loss forecasting; maintain Basel III capital standards including a common equity tier 1 minimum of 4.5% plus a 2.5% conservation buffer. Enforce AML/CFT, sanctions and KYC processes compliant with Turkish and international rules, monitor suspicious activity and report to authorities. Align provisioning and reporting with IFRS 9 and local BRSA requirements, and conduct periodic stress tests and forward-looking provisioning to safeguard capital.

Trade finance and international banking

Halkbank issues letters of credit, performance and bid guarantees and manages collections to support exporters and importers, while providing FX, hedging and cross-border settlement services. It structures supply chain and export finance with correspondent partner banks and facilitates state-backed trade support programs to de-risk transactions. Core focus is ensuring liquidity and payment certainty across Turkish foreign trade corridors.

- Issue LCs and guarantees

- FX, hedging, settlements

- Supply chain & export finance with partners

- Facilitate state-backed trade support

Digital delivery and customer service

Halkbank develops mobile, internet and API-based services to expand digital delivery, streamlines onboarding and payments for speed and convenience, operates contact centers alongside RM-led service for complex needs, and leverages customer data to personalize offers and reduce churn.

- mobile, internet, API services

- fast onboarding & payments

- contact centers + RM-led support

- data-driven personalization & churn reduction

Low-cost deposits drive lending to 10M customers

Acquire deposits via state-backed trust, optimize funding mix toward low-cost current accounts, manage liquidity per BRSA; extend tailored retail/SME/corporate loans (served over 10 million customers in 2024) with quantitative underwriting and active monitoring; enforce credit/market/operational risk, IFRS 9 provisioning and Basel III CET1 minimum 4.5% plus 2.5% buffer; operate trade finance, FX hedging and digital channels.

| Metric | 2024 |

|---|---|

| Customers | over 10 million |

| CET1 minimum | 4.5% + 2.5% buffer |

Delivered as Displayed

Business Model Canvas

The document previewed here is the actual Halkbank Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this identical file with all content included. Files are delivered ready-to-edit in Word and Excel formats for immediate use and presentation.

Original: $10.00

-65%$10.00

$3.50Description

Unlock a leading bank's Business Model Canvas for retail & SME value creation

Unlock the full strategic blueprint behind Halkbank's business model. This concise Business Model Canvas exposes how Halkbank creates value across retail and SME segments, leverages partnerships, and monetizes services while managing risks. Purchase the complete, editable Word & Excel canvas for detailed, section-by-section insights and actionable recommendations.

Partnerships

Turkish government and public institutions

Collaboration with the Treasury and ministries aligns Halkbank lending to national development priorities, supporting credit to sectors where SMEs — over 99% of Turkish firms — are concentrated. Access to Treasury-backed guarantee schemes and subsidized programs lowers counterparty risk and pricing for priority loans. Public infrastructure projects supply stable corporate and project finance pipelines, while policy coordination enables counter-cyclical credit expansion.

Central Bank of Türkiye and regulators

Monetary operations and CBRT reserve facilities underpin Halkbank liquidity management by providing short-term funding and reserve instruments. Regulatory guidance from BDDK and Basel III standards (minimum CET1 4.5% and total capital 8%) shapes capital, risk and consumer protection rules. Participation in national clearing infrastructures (Takasbank, BKM) ensures transaction reliability. Prudential supervision strengthens market confidence.

International development banks and DFIs

Partnerships with EBRD, IFC and similar DFIs provide Halkbank with long-tenor funding (typically 5–15 years), enabling SME, green and inclusive finance growth. Technical assistance programs from these partners strengthen credit frameworks and digital lending for SMEs. Co-financing structures diversify funding, lowering single-lender concentration and currency exposure. Access to DFI best practices enhances the bank’s sustainability and ESG frameworks.

Correspondent banks and payment networks

Halkbank leverages correspondent banks and payment networks to enable trade finance and cross-border payments. SWIFT (11,000+ institutions in 200+ countries) and card schemes Visa/Mastercard (operations in 200+ countries, 160+ currencies) expand transactional reach. Multicurrency settlement supports exporters/importers while network partnerships enhance speed, security and acceptance.

- Correspondent reach: SWIFT 11,000+ nodes

- Card schemes: 200+ countries, 160+ currencies

- Benefits: faster settlement, stronger security, wider acceptance

Fintechs and technology vendors

Fintech and technology vendors enable Halkbank to accelerate digital onboarding, KYC and payments via API partnerships, cutting onboarding times and supporting a 2024 digital payments volume exceeding 500 million transactions.

Core banking, cybersecurity and cloud providers boost scalability and resilience, underpinning Halkbank’s push to increase transaction capacity and regulatory compliance in 2024.

Data analytics vendors improve credit underwriting and personalization, feeding models that reduced default prediction errors and powered targeted product offers in 2024; co-innovation with partners shortens time-to-market for new products.

- API partners: faster onboarding, KYC, payments

- Core banking & cloud: scalability, compliance

- Cybersecurity: resilience against threats

- Data analytics: better underwriting, personalization

- Co-innovation: quicker product launches

Public-DFI-fintech tie-ups enable subsidized SME loans, long-term funding and 500M+ digital payments

Halkbank’s key partnerships with Treasury, DFIs (EBRD/IFC), correspondent banks and fintechs enable subsidized SME credit, long-tenor funding (DFI loans 5–15y), cross-border services (SWIFT 11,000+ nodes) and 2024 digital payments >500M tx. Regulatory and central bank links secure liquidity and compliance; tech vendors shorten onboarding and improve underwriting accuracy.

| Partner | Key metric |

|---|---|

| Treasury | SME focus; guarantee schemes |

| DFIs | 5–15y funding |

| SWIFT/cards | 11,000+/200+ countries |

| Fintechs | 2024: >500M payments |

What is included in the product

A comprehensive pre-written Business Model Canvas for Halkbank covering customer segments, value propositions, channels, revenue streams, key activities, resources, partners, cost structure and relationships, reflecting real-world operations and competitive advantages; includes SWOT-linked insights and a polished design ideal for presentations, investor discussions and strategic decision-making.

High-level view of Halkbank’s business model with editable cells, condensing its retail, SME and corporate banking strategies into a one-page snapshot for quick review and boardroom-ready discussion.

Activities

Deposit mobilization and liquidity management

Acquire retail and corporate deposits through competitive rates, enhanced digital and branch service, and trust built on Halkbank’s state-backed reputation to deepen stable funding. Optimize funding mix and maturities to lower cost of funds by shifting toward low-cost current accounts and term retail deposits. Manage liquidity buffers within BRSA limits and execute money market and repo operations as needed to meet short-term needs.

Lending and credit underwriting

Halkbank extends tailored loans to individuals, SMEs and corporates, structuring tenor, pricing and repayment to client cash flows and sector needs; in 2024 it served over 10 million customers with a broad retail and commercial product mix. The bank applies quantitative risk scoring, collateral valuation and covenant frameworks to underwrite exposures and price risk. Portfolios are actively monitored with early-warning indicators to preserve asset quality and nonperforming loan ratios. Halkbank channels targeted credit lines to priority sectors such as SMEs, exporters and construction to support growth and employment.

Risk, compliance, and governance

Operate robust credit, market and operational risk controls with regular portfolio limits, credit scoring and loss forecasting; maintain Basel III capital standards including a common equity tier 1 minimum of 4.5% plus a 2.5% conservation buffer. Enforce AML/CFT, sanctions and KYC processes compliant with Turkish and international rules, monitor suspicious activity and report to authorities. Align provisioning and reporting with IFRS 9 and local BRSA requirements, and conduct periodic stress tests and forward-looking provisioning to safeguard capital.

Trade finance and international banking

Halkbank issues letters of credit, performance and bid guarantees and manages collections to support exporters and importers, while providing FX, hedging and cross-border settlement services. It structures supply chain and export finance with correspondent partner banks and facilitates state-backed trade support programs to de-risk transactions. Core focus is ensuring liquidity and payment certainty across Turkish foreign trade corridors.

- Issue LCs and guarantees

- FX, hedging, settlements

- Supply chain & export finance with partners

- Facilitate state-backed trade support

Digital delivery and customer service

Halkbank develops mobile, internet and API-based services to expand digital delivery, streamlines onboarding and payments for speed and convenience, operates contact centers alongside RM-led service for complex needs, and leverages customer data to personalize offers and reduce churn.

- mobile, internet, API services

- fast onboarding & payments

- contact centers + RM-led support

- data-driven personalization & churn reduction

Low-cost deposits drive lending to 10M customers

Acquire deposits via state-backed trust, optimize funding mix toward low-cost current accounts, manage liquidity per BRSA; extend tailored retail/SME/corporate loans (served over 10 million customers in 2024) with quantitative underwriting and active monitoring; enforce credit/market/operational risk, IFRS 9 provisioning and Basel III CET1 minimum 4.5% plus 2.5% buffer; operate trade finance, FX hedging and digital channels.

| Metric | 2024 |

|---|---|

| Customers | over 10 million |

| CET1 minimum | 4.5% + 2.5% buffer |

Delivered as Displayed

Business Model Canvas

The document previewed here is the actual Halkbank Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this identical file with all content included. Files are delivered ready-to-edit in Word and Excel formats for immediate use and presentation.