Halma Porter's Five Forces Analysis

Don't Miss the Bigger Picture

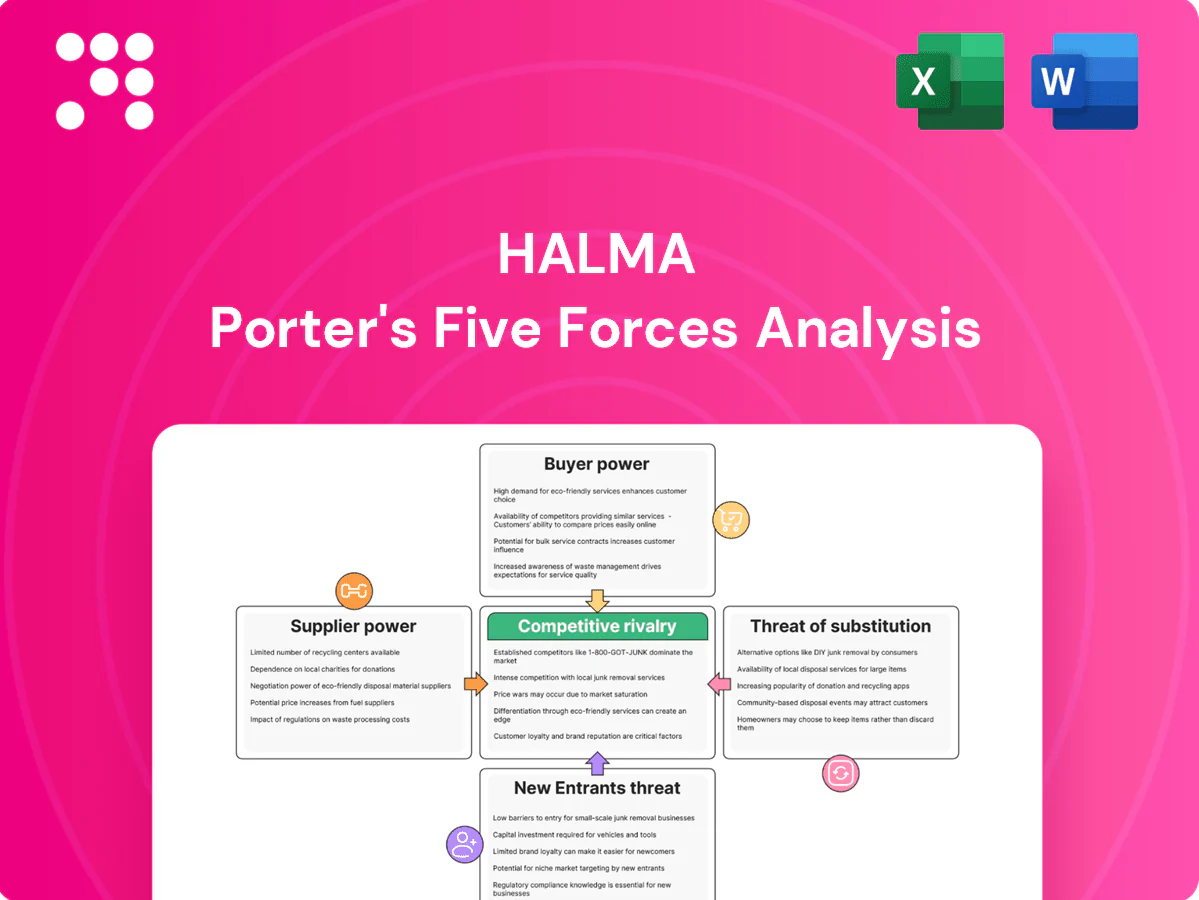

Halma's Porter's Five Forces snapshot highlights moderate supplier power, high buyer expectations, limited new entrant threat, evolving competitive rivalry and manageable substitute risk. This brief view surfaces strategic pressures shaping margins, growth and M&A rationale. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals and actionable implications for Halma.

Suppliers Bargaining Power

Specialized components dependence

Halma’s devices depend on niche sensors, optics, semiconductors and certified materials, concentrating supplier leverage and exposing ~£1.15bn FY2024 group revenues to component risk. Qualification cycles and regulatory documentation prolong switching costs, with supplier lead times commonly 12+ weeks. Multi-sourcing and modular designs dilute individual supplier power, while strategic inventory and multi-year agreements buffer price and availability volatility.

Regulatory-grade inputs

Medical and safety certifications demand traceable, validated inputs, which by 2024 industry surveys show typically cut the eligible supplier pool by about 50%, limiting substitution. Vendors with compliant processes command premiums, often pricing 5–15% higher for validated batches. Halma’s quality systems and supplier audits standardize expectations and help curb opportunistic pricing. Approved vendor lists keep supplier power at a moderate level.

Global footprint, diversified sourcing

Halma’s network of over 100 operating companies across 20+ countries spreads sourcing and reduces single-point supplier dependency, balancing currency, logistics and geopolitical exposure. Global shocks—seen in the 2020–22 chip cycle and logistics constraints—can synchronously raise supplier power across regions. Increased regionalization and near-shoring lower but do not remove this systemic risk.

Scale and relationship leverage

Aggregated group spend strengthens Halma’s supplier negotiation leverage, lowering unit costs across divisions and securing better payment and delivery terms. Long-standing partnerships enable priority allocation during component shortages, while co-development with key suppliers creates mutual dependency that reduces supplier-driven price pressure. The trade-off is increased lock-in to specific technologies and platforms.

- Aggregated spend: stronger terms

- Partnerships: priority allocation

- Co-development: mutual dependency

- Risk: technology lock-in

ESG and scarce materials exposure

Stringent ESG sourcing and the EU Conflict Minerals Regulation (in force since 2021) have narrowed qualified supplier pools; the global rare earths market was about $7 billion in 2023 and China supplied roughly 60% of rare earth output, creating upstream concentration risk. Rare earths and specialty alloys therefore raise episodic supplier leverage. Supplier audits and circularity programmes reduce volatility but add compliance cost, leaving overall moderate supplier power with occasional spikes.

- ESG regulation: EU Conflict Minerals Reg. in force 2021

- Market scale: rare earths ~ $7bn (2023)

- Concentration: China ~60% of supply (2023)

- Impact: moderate supplier power; episodic price/availability spikes

Industrial-safety group: £1.15bn at risk from 12+ week lead times and rare-earth squeeze

Halma faces moderate supplier power: ~£1.15bn FY2024 revenue exposed to niche sensors/semiconductors with 12+ week lead times and validated suppliers charging 5–15% premiums; qualification cuts eligible suppliers by ~50%. Group scale (100+ ops, 20+ countries) and multi-sourcing reduce risk, while rare-earth concentration (global market ~$7bn; China ~60% in 2023) creates episodic spikes.

| Metric | Value |

|---|---|

| Revenue exposed (FY2024) | £1.15bn |

| Lead times | 12+ weeks |

| Supplier pool reduction | ~50% |

| Premium for validated inputs | 5–15% |

| Rare earths market (2023) | $7bn; China ~60% |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored to Halma, uncovering competitive drivers, supplier/buyer power, barriers to entry, substitutes and emerging threats, with strategic commentary for decision-makers.

Halma Porter's Five Forces condenses competitive pressures into a single, editable snapshot so teams quickly spot vulnerabilities and prioritize defensive moves. Use the clear scores, notes and radar view to relieve analysis bottlenecks and make faster, board-ready decisions.

Customers Bargaining Power

Diverse, knowledgeable buyers

Customers span hospitals, labs, industrials, utilities and municipalities with professional procurement teams that benchmark technical specs and lifecycle cost; OECD data show public procurement represents about 12% of GDP, reinforcing formal tender discipline. Public tenders and group purchasing impose transparent price pressure, while Halma’s spread across end-markets limits any single buyer’s leverage.

High switching and validation costs

Safety and medical use-cases require validation, training, and regulatory filings that often drive requalification cycles of 3–12 months, elevating switching costs and reducing buyer leverage. Installed-base integration and operator familiarity create stickiness, with many hospitals planning equipment replacement over multi-year timelines. Downtime and requalification risks—where single-day outages can cost six-figure sums in critical units—deter change and lower buyer power for mission-critical products.

Outcome and compliance differentiation

Performance, reliability and compliance often trump headline price in Halma markets; buyers demand uptime targets of 99.9% (≈8.8 hours downtime/year) and recognised credentials such as ISO 9001 and CE/UL certification. Strong Halma brands and service networks (FY2024 revenue ≈£1.74bn) reduce pure price bargaining by guaranteeing accuracy and rapid field support. Documented ROI and quantifiable risk reduction (common payback horizons under 18 months) further curb buyer leverage.

Aftermarket and service dependency

Aftermarket consumables, calibration and multiyear service contracts create recurring ties that shift bargaining power toward suppliers by locking customers into ongoing spend; proprietary parts and software ecosystems reinforce this lock-in and limit switching. Multiyear SLAs reduce renegotiation frequency, so buyers exert most leverage at initial platform selection rather than during aftermarket support.

- Consumables drive repeat revenue

- Proprietary parts/software create lock-in

- Multiyear SLAs limit renegotiation

- Buyer leverage concentrated at purchase

Budget cycles and tender pressure

Public-sector and clinical budget cycles create periodic price tension, with IMF forecasting 2024 world GDP growth of 3.1% tightening fiscal space. Large tenders extract volume discounts and extended warranties, and procurement in 2024 increasingly evaluates total cost of ownership. Halma counters via value-based selling and modular offer tiers.

- IMF 2024 world GDP 3.1%

- Tenders push volume discounts, extended warranties

- Halma: value-based selling, modular tiers

High switching costs and uptime needs give suppliers leverage despite tender-driven price pressure

Customers (hospitals, labs, utilities) push price via tenders but professional procurement and public procurement (~12% GDP OECD) limit informal bargaining; Halma FY2024 revenue £1.74bn and strong brands reduce price pressure. High switching costs (requalification 3–12 months), uptime requirements 99.9% and consumables/service contracts shift power to suppliers. Buyers strongest at initial purchase; tenders and budget cycles (IMF 2024 GDP growth 3.1%) create periodic leverage.

| Metric | Value |

|---|---|

| FY2024 revenue | £1.74bn |

| Public procurement | ~12% GDP (OECD) |

| Uptime target | 99.9% |

| Requalification | 3–12 months |

| IMF 2024 GDP | 3.1% |

Full Version Awaits

Halma Porter's Five Forces Analysis

This preview shows the exact Halma Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, ready for download and use the moment you buy, covering supplier power, buyer power, competitive rivalry, threats of new entrants, and substitutes with tailored insights. Instant access to the same professional file is granted upon payment.

Don't Miss the Bigger Picture

Halma's Porter's Five Forces snapshot highlights moderate supplier power, high buyer expectations, limited new entrant threat, evolving competitive rivalry and manageable substitute risk. This brief view surfaces strategic pressures shaping margins, growth and M&A rationale. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals and actionable implications for Halma.

Suppliers Bargaining Power

Specialized components dependence

Halma’s devices depend on niche sensors, optics, semiconductors and certified materials, concentrating supplier leverage and exposing ~£1.15bn FY2024 group revenues to component risk. Qualification cycles and regulatory documentation prolong switching costs, with supplier lead times commonly 12+ weeks. Multi-sourcing and modular designs dilute individual supplier power, while strategic inventory and multi-year agreements buffer price and availability volatility.

Regulatory-grade inputs

Medical and safety certifications demand traceable, validated inputs, which by 2024 industry surveys show typically cut the eligible supplier pool by about 50%, limiting substitution. Vendors with compliant processes command premiums, often pricing 5–15% higher for validated batches. Halma’s quality systems and supplier audits standardize expectations and help curb opportunistic pricing. Approved vendor lists keep supplier power at a moderate level.

Global footprint, diversified sourcing

Halma’s network of over 100 operating companies across 20+ countries spreads sourcing and reduces single-point supplier dependency, balancing currency, logistics and geopolitical exposure. Global shocks—seen in the 2020–22 chip cycle and logistics constraints—can synchronously raise supplier power across regions. Increased regionalization and near-shoring lower but do not remove this systemic risk.

Scale and relationship leverage

Aggregated group spend strengthens Halma’s supplier negotiation leverage, lowering unit costs across divisions and securing better payment and delivery terms. Long-standing partnerships enable priority allocation during component shortages, while co-development with key suppliers creates mutual dependency that reduces supplier-driven price pressure. The trade-off is increased lock-in to specific technologies and platforms.

- Aggregated spend: stronger terms

- Partnerships: priority allocation

- Co-development: mutual dependency

- Risk: technology lock-in

ESG and scarce materials exposure

Stringent ESG sourcing and the EU Conflict Minerals Regulation (in force since 2021) have narrowed qualified supplier pools; the global rare earths market was about $7 billion in 2023 and China supplied roughly 60% of rare earth output, creating upstream concentration risk. Rare earths and specialty alloys therefore raise episodic supplier leverage. Supplier audits and circularity programmes reduce volatility but add compliance cost, leaving overall moderate supplier power with occasional spikes.

- ESG regulation: EU Conflict Minerals Reg. in force 2021

- Market scale: rare earths ~ $7bn (2023)

- Concentration: China ~60% of supply (2023)

- Impact: moderate supplier power; episodic price/availability spikes

Industrial-safety group: £1.15bn at risk from 12+ week lead times and rare-earth squeeze

Halma faces moderate supplier power: ~£1.15bn FY2024 revenue exposed to niche sensors/semiconductors with 12+ week lead times and validated suppliers charging 5–15% premiums; qualification cuts eligible suppliers by ~50%. Group scale (100+ ops, 20+ countries) and multi-sourcing reduce risk, while rare-earth concentration (global market ~$7bn; China ~60% in 2023) creates episodic spikes.

| Metric | Value |

|---|---|

| Revenue exposed (FY2024) | £1.15bn |

| Lead times | 12+ weeks |

| Supplier pool reduction | ~50% |

| Premium for validated inputs | 5–15% |

| Rare earths market (2023) | $7bn; China ~60% |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored to Halma, uncovering competitive drivers, supplier/buyer power, barriers to entry, substitutes and emerging threats, with strategic commentary for decision-makers.

Halma Porter's Five Forces condenses competitive pressures into a single, editable snapshot so teams quickly spot vulnerabilities and prioritize defensive moves. Use the clear scores, notes and radar view to relieve analysis bottlenecks and make faster, board-ready decisions.

Customers Bargaining Power

Diverse, knowledgeable buyers

Customers span hospitals, labs, industrials, utilities and municipalities with professional procurement teams that benchmark technical specs and lifecycle cost; OECD data show public procurement represents about 12% of GDP, reinforcing formal tender discipline. Public tenders and group purchasing impose transparent price pressure, while Halma’s spread across end-markets limits any single buyer’s leverage.

High switching and validation costs

Safety and medical use-cases require validation, training, and regulatory filings that often drive requalification cycles of 3–12 months, elevating switching costs and reducing buyer leverage. Installed-base integration and operator familiarity create stickiness, with many hospitals planning equipment replacement over multi-year timelines. Downtime and requalification risks—where single-day outages can cost six-figure sums in critical units—deter change and lower buyer power for mission-critical products.

Outcome and compliance differentiation

Performance, reliability and compliance often trump headline price in Halma markets; buyers demand uptime targets of 99.9% (≈8.8 hours downtime/year) and recognised credentials such as ISO 9001 and CE/UL certification. Strong Halma brands and service networks (FY2024 revenue ≈£1.74bn) reduce pure price bargaining by guaranteeing accuracy and rapid field support. Documented ROI and quantifiable risk reduction (common payback horizons under 18 months) further curb buyer leverage.

Aftermarket and service dependency

Aftermarket consumables, calibration and multiyear service contracts create recurring ties that shift bargaining power toward suppliers by locking customers into ongoing spend; proprietary parts and software ecosystems reinforce this lock-in and limit switching. Multiyear SLAs reduce renegotiation frequency, so buyers exert most leverage at initial platform selection rather than during aftermarket support.

- Consumables drive repeat revenue

- Proprietary parts/software create lock-in

- Multiyear SLAs limit renegotiation

- Buyer leverage concentrated at purchase

Budget cycles and tender pressure

Public-sector and clinical budget cycles create periodic price tension, with IMF forecasting 2024 world GDP growth of 3.1% tightening fiscal space. Large tenders extract volume discounts and extended warranties, and procurement in 2024 increasingly evaluates total cost of ownership. Halma counters via value-based selling and modular offer tiers.

- IMF 2024 world GDP 3.1%

- Tenders push volume discounts, extended warranties

- Halma: value-based selling, modular tiers

High switching costs and uptime needs give suppliers leverage despite tender-driven price pressure

Customers (hospitals, labs, utilities) push price via tenders but professional procurement and public procurement (~12% GDP OECD) limit informal bargaining; Halma FY2024 revenue £1.74bn and strong brands reduce price pressure. High switching costs (requalification 3–12 months), uptime requirements 99.9% and consumables/service contracts shift power to suppliers. Buyers strongest at initial purchase; tenders and budget cycles (IMF 2024 GDP growth 3.1%) create periodic leverage.

| Metric | Value |

|---|---|

| FY2024 revenue | £1.74bn |

| Public procurement | ~12% GDP (OECD) |

| Uptime target | 99.9% |

| Requalification | 3–12 months |

| IMF 2024 GDP | 3.1% |

Full Version Awaits

Halma Porter's Five Forces Analysis

This preview shows the exact Halma Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, ready for download and use the moment you buy, covering supplier power, buyer power, competitive rivalry, threats of new entrants, and substitutes with tailored insights. Instant access to the same professional file is granted upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Halma's Porter's Five Forces snapshot highlights moderate supplier power, high buyer expectations, limited new entrant threat, evolving competitive rivalry and manageable substitute risk. This brief view surfaces strategic pressures shaping margins, growth and M&A rationale. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals and actionable implications for Halma.

Suppliers Bargaining Power

Specialized components dependence

Halma’s devices depend on niche sensors, optics, semiconductors and certified materials, concentrating supplier leverage and exposing ~£1.15bn FY2024 group revenues to component risk. Qualification cycles and regulatory documentation prolong switching costs, with supplier lead times commonly 12+ weeks. Multi-sourcing and modular designs dilute individual supplier power, while strategic inventory and multi-year agreements buffer price and availability volatility.

Regulatory-grade inputs

Medical and safety certifications demand traceable, validated inputs, which by 2024 industry surveys show typically cut the eligible supplier pool by about 50%, limiting substitution. Vendors with compliant processes command premiums, often pricing 5–15% higher for validated batches. Halma’s quality systems and supplier audits standardize expectations and help curb opportunistic pricing. Approved vendor lists keep supplier power at a moderate level.

Global footprint, diversified sourcing

Halma’s network of over 100 operating companies across 20+ countries spreads sourcing and reduces single-point supplier dependency, balancing currency, logistics and geopolitical exposure. Global shocks—seen in the 2020–22 chip cycle and logistics constraints—can synchronously raise supplier power across regions. Increased regionalization and near-shoring lower but do not remove this systemic risk.

Scale and relationship leverage

Aggregated group spend strengthens Halma’s supplier negotiation leverage, lowering unit costs across divisions and securing better payment and delivery terms. Long-standing partnerships enable priority allocation during component shortages, while co-development with key suppliers creates mutual dependency that reduces supplier-driven price pressure. The trade-off is increased lock-in to specific technologies and platforms.

- Aggregated spend: stronger terms

- Partnerships: priority allocation

- Co-development: mutual dependency

- Risk: technology lock-in

ESG and scarce materials exposure

Stringent ESG sourcing and the EU Conflict Minerals Regulation (in force since 2021) have narrowed qualified supplier pools; the global rare earths market was about $7 billion in 2023 and China supplied roughly 60% of rare earth output, creating upstream concentration risk. Rare earths and specialty alloys therefore raise episodic supplier leverage. Supplier audits and circularity programmes reduce volatility but add compliance cost, leaving overall moderate supplier power with occasional spikes.

- ESG regulation: EU Conflict Minerals Reg. in force 2021

- Market scale: rare earths ~ $7bn (2023)

- Concentration: China ~60% of supply (2023)

- Impact: moderate supplier power; episodic price/availability spikes

Industrial-safety group: £1.15bn at risk from 12+ week lead times and rare-earth squeeze

Halma faces moderate supplier power: ~£1.15bn FY2024 revenue exposed to niche sensors/semiconductors with 12+ week lead times and validated suppliers charging 5–15% premiums; qualification cuts eligible suppliers by ~50%. Group scale (100+ ops, 20+ countries) and multi-sourcing reduce risk, while rare-earth concentration (global market ~$7bn; China ~60% in 2023) creates episodic spikes.

| Metric | Value |

|---|---|

| Revenue exposed (FY2024) | £1.15bn |

| Lead times | 12+ weeks |

| Supplier pool reduction | ~50% |

| Premium for validated inputs | 5–15% |

| Rare earths market (2023) | $7bn; China ~60% |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored to Halma, uncovering competitive drivers, supplier/buyer power, barriers to entry, substitutes and emerging threats, with strategic commentary for decision-makers.

Halma Porter's Five Forces condenses competitive pressures into a single, editable snapshot so teams quickly spot vulnerabilities and prioritize defensive moves. Use the clear scores, notes and radar view to relieve analysis bottlenecks and make faster, board-ready decisions.

Customers Bargaining Power

Diverse, knowledgeable buyers

Customers span hospitals, labs, industrials, utilities and municipalities with professional procurement teams that benchmark technical specs and lifecycle cost; OECD data show public procurement represents about 12% of GDP, reinforcing formal tender discipline. Public tenders and group purchasing impose transparent price pressure, while Halma’s spread across end-markets limits any single buyer’s leverage.

High switching and validation costs

Safety and medical use-cases require validation, training, and regulatory filings that often drive requalification cycles of 3–12 months, elevating switching costs and reducing buyer leverage. Installed-base integration and operator familiarity create stickiness, with many hospitals planning equipment replacement over multi-year timelines. Downtime and requalification risks—where single-day outages can cost six-figure sums in critical units—deter change and lower buyer power for mission-critical products.

Outcome and compliance differentiation

Performance, reliability and compliance often trump headline price in Halma markets; buyers demand uptime targets of 99.9% (≈8.8 hours downtime/year) and recognised credentials such as ISO 9001 and CE/UL certification. Strong Halma brands and service networks (FY2024 revenue ≈£1.74bn) reduce pure price bargaining by guaranteeing accuracy and rapid field support. Documented ROI and quantifiable risk reduction (common payback horizons under 18 months) further curb buyer leverage.

Aftermarket and service dependency

Aftermarket consumables, calibration and multiyear service contracts create recurring ties that shift bargaining power toward suppliers by locking customers into ongoing spend; proprietary parts and software ecosystems reinforce this lock-in and limit switching. Multiyear SLAs reduce renegotiation frequency, so buyers exert most leverage at initial platform selection rather than during aftermarket support.

- Consumables drive repeat revenue

- Proprietary parts/software create lock-in

- Multiyear SLAs limit renegotiation

- Buyer leverage concentrated at purchase

Budget cycles and tender pressure

Public-sector and clinical budget cycles create periodic price tension, with IMF forecasting 2024 world GDP growth of 3.1% tightening fiscal space. Large tenders extract volume discounts and extended warranties, and procurement in 2024 increasingly evaluates total cost of ownership. Halma counters via value-based selling and modular offer tiers.

- IMF 2024 world GDP 3.1%

- Tenders push volume discounts, extended warranties

- Halma: value-based selling, modular tiers

High switching costs and uptime needs give suppliers leverage despite tender-driven price pressure

Customers (hospitals, labs, utilities) push price via tenders but professional procurement and public procurement (~12% GDP OECD) limit informal bargaining; Halma FY2024 revenue £1.74bn and strong brands reduce price pressure. High switching costs (requalification 3–12 months), uptime requirements 99.9% and consumables/service contracts shift power to suppliers. Buyers strongest at initial purchase; tenders and budget cycles (IMF 2024 GDP growth 3.1%) create periodic leverage.

| Metric | Value |

|---|---|

| FY2024 revenue | £1.74bn |

| Public procurement | ~12% GDP (OECD) |

| Uptime target | 99.9% |

| Requalification | 3–12 months |

| IMF 2024 GDP | 3.1% |

Full Version Awaits

Halma Porter's Five Forces Analysis

This preview shows the exact Halma Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, ready for download and use the moment you buy, covering supplier power, buyer power, competitive rivalry, threats of new entrants, and substitutes with tailored insights. Instant access to the same professional file is granted upon payment.