Hamilton Lane Porter's Five Forces Analysis

From Overview to Strategy Blueprint

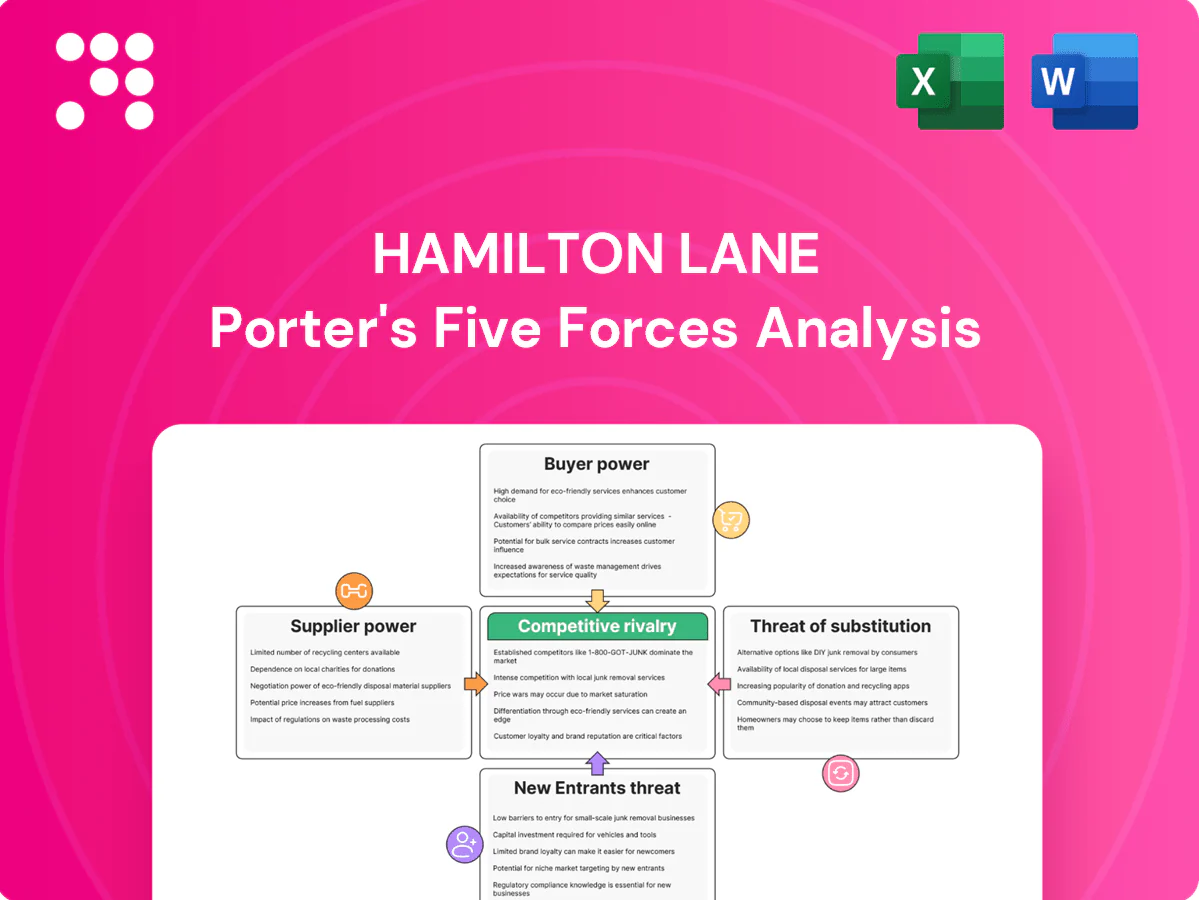

Hamilton Lane’s Porter’s Five Forces snapshot highlights buyer and supplier power, rival intensity, entry barriers, and substitute risks shaping its private markets advisory business. Our concise review pinpoints strategic strengths and pressure points for investors and managers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hamilton Lane’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated top-tier GPs

Hamilton Lane depends on a concentrated set of elite PE, credit and real asset GPs for allocations and co-invests; Preqin reported about $1.7 trillion of private equity dry powder in 2024, intensifying competition for top GP capacity. These top-tier managers are often oversubscribed, giving them pricing and allocation leverage and driving preferred access toward long-standing, large-scale relationships. Loss of GP access can materially hurt performance and product differentiation.

Scarce proprietary deal flow

Sponsor-sourced direct and co-invest deals are limited and fiercely contested; with Hamilton Lane reporting roughly $884 billion AUM in 2024 and global private equity dry powder near $1.6 trillion in 2024, sponsors can pick partners that underwrite faster or offer larger tickets. This scarcity boosts supplier power to dictate pricing, terms and timing. It forces Hamilton Lane to accelerate diligence cycles and deepen sector expertise to win allocations.

Data and analytics vendors

Third-party data vendors (e.g., Preqin, PitchBook) shape private-markets diligence and reporting; Preqin estimated about 2.5 trillion USD of private capital dry powder in 2024, underscoring dataset importance. Switching providers is costly given integrations and historical comparability, enabling vendors to raise prices or restrict usage. Hamilton Lane reduces exposure via in-house data and analytics platforms but still depends on external benchmarks for industry-wide comparability.

Specialized talent as a supplier

Experienced investment professionals and specialized engineers are scarce and mobile, giving them outsized bargaining power; typical private equity carried interest remains around 20% while standard management fees are near 2%, reinforcing negotiation leverage. Compensation cycles and carry structures amplify retention importance to preserve GP access and underwriting edge, and tight labor markets can pressure margins and execution capacity.

- Scarcity: experienced hires drive deal origination and execution

- Compensation: 20% carried interest, ~2% fees influence mobility

- Retention: critical for GP access and competitive edge

- Risk: tight labor markets compress margins, limit execution

Financial and operational infrastructure

Administrators, custodians and technology stacks (eg custodians like BNY Mellon, State Street, JPMorgan custody tens of trillions in assets) are foundational for SMAs and funds; vendor consolidation lowers negotiating leverage and raises concentration risk. Operational incidents in 2023–24 caused multi‑day reporting outages for some providers, disrupting client delivery. Multi‑vendor architectures and internal tooling mitigate risk, but vendor switching is costly and complex.

- Concentration: top custodians hold tens of trillions in assets

- Risk: vendor consolidation reduces bargaining power

- Impact: operational incidents cause multi‑day outages

- Mitigation: multi‑vendor + internal tooling, but switching is non‑trivial

Concentrated GPs, custodians and scarce carry talent squeeze PE fees and allocations

Hamilton Lane faces strong supplier power: concentrated top GPs control capacity (global PE dry powder ~$1.6T in 2024) and can demand premium allocations, risking product differentiation and returns. Data vendors and custodians are concentrated (top custodians hold tens of trillions), raising costs and switching barriers. Talent scarcity (carry ~20%, fees ~2%) amplifies retention pressure and margin risk.

| Supplier | Power | 2024 metric |

|---|---|---|

| Top GPs | High | PE dry powder ~$1.6T |

| Data vendors | Medium-High | Preqin/PitchBook market reliance |

| Custodians | High | Top custodians hold tens of trillions |

| Talent | High | Carry ~20%, fees ~2% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Hamilton Lane, uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and identifying disruptive risks and entry barriers to inform strategic positioning and valuation.

A concise, one-sheet Hamilton Lane Porter’s Five Forces summary—pinpoint competitive pressures and relieve analysis bottlenecks for faster, board-ready decisions.

Customers Bargaining Power

Institutional scale mandates

Clients—large pensions, sovereigns, endowments and insurers—tend to issue competitive RFPs and demand bespoke structures, driving aggressive fee negotiations and custom reporting. In 2024 the top 10 pension funds each oversaw more than $100 billion, enabling multi-manager comparisons and strict KPIs that amplify selection leverage. This concentration of mandates concentrates revenue and heightens buyer power over managers.

Fee compression pressure

Market-wide focus on net returns has compressed fees—industry management fees have fallen from the traditional 2% toward roughly 1.3–1.5% and carry expectations have trended toward 15% or below on negotiated deals. Clients increasingly demand low-cost SMAs, zero-to-0.5% co-invest fees and performance-based terms; transparent benchmarking tools bolster buyer leverage. Hamilton Lane must weigh lower pricing against demonstrable value-add and differentiated access.

Switching costs but not prohibitive

Illiquidity and typical private fund lives of about 10 years create meaningful switching frictions for Hamilton Lane clients, yet secondary markets exceeding $100 billion annually and the ability to allocate new capital elsewhere mean redirection is relatively easy. Buyers can dual-track relationships to transition gradually, and advisory mandates are far easier to reassign than closed‑end fund commitments, producing moderate, not absolute, buyer power.

In-sourcing alternatives

In 2024, many large institutions scaled in-house private markets teams, pressuring managers on fees, data access and co-invest volume; Hamilton Lane points to its breadth, scale and proprietary insights cited in its 2024 Global Private Markets Report to defend pricing. Still, credible in-sourcing materially amplifies buyer bargaining power and disciplines manager economics.

- In-sourcing: larger institutions building internal teams

- Pressure points: fees, data access, co-invest volume

- Hamilton Lane defense: breadth, scale, proprietary insights

- Net effect: stronger buyer bargaining power

Demand for data and transparency

Clients now demand granular performance, ESG, and look-through reporting, forcing Hamilton Lane to invest continuously in data systems and specialist staff. Buyers increasingly condition allocations on analytics access and bespoke dashboards, giving investors leverage in fee and service negotiations. Rising transparency expectations in 2024 amplify customer bargaining power across mandates.

- Granular performance reporting required

- ESG and look-through data standard

- Ongoing tech and talent costs

- Analytics access drives allocation

Large pensions' leverage cuts fees to ~1.3-1.5%; secondaries > $100B/year

Clients—large pensions, sovereigns, endowments and insurers—drive bespoke RFPs and aggressive fee negotiation; top 10 pensions in 2024 each oversaw >$100B, amplifying selection leverage. Industry fees moved from 2% toward ~1.3–1.5% and carry to ~15% as secondary markets >$100B/year and in-sourcing strengthen buyer power. Hamilton Lane leans on scale, proprietary data and co-invests but faces sustained buyer pressure.

| Metric | 2024 Value |

|---|---|

| Top 10 pensions AUM | >$100B each |

| Management fee | ~1.3–1.5% |

| Carry | ~15% |

| Secondary market volume | >$100B/year |

What You See Is What You Get

Hamilton Lane Porter's Five Forces Analysis

This preview shows the exact Hamilton Lane Porter's Five Forces analysis you'll receive after purchase. It is the full, professionally formatted document—no placeholders or mockups. Upon payment you’ll get instant access to this identical file, ready for download and use. No customization required.

From Overview to Strategy Blueprint

Hamilton Lane’s Porter’s Five Forces snapshot highlights buyer and supplier power, rival intensity, entry barriers, and substitute risks shaping its private markets advisory business. Our concise review pinpoints strategic strengths and pressure points for investors and managers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hamilton Lane’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated top-tier GPs

Hamilton Lane depends on a concentrated set of elite PE, credit and real asset GPs for allocations and co-invests; Preqin reported about $1.7 trillion of private equity dry powder in 2024, intensifying competition for top GP capacity. These top-tier managers are often oversubscribed, giving them pricing and allocation leverage and driving preferred access toward long-standing, large-scale relationships. Loss of GP access can materially hurt performance and product differentiation.

Scarce proprietary deal flow

Sponsor-sourced direct and co-invest deals are limited and fiercely contested; with Hamilton Lane reporting roughly $884 billion AUM in 2024 and global private equity dry powder near $1.6 trillion in 2024, sponsors can pick partners that underwrite faster or offer larger tickets. This scarcity boosts supplier power to dictate pricing, terms and timing. It forces Hamilton Lane to accelerate diligence cycles and deepen sector expertise to win allocations.

Data and analytics vendors

Third-party data vendors (e.g., Preqin, PitchBook) shape private-markets diligence and reporting; Preqin estimated about 2.5 trillion USD of private capital dry powder in 2024, underscoring dataset importance. Switching providers is costly given integrations and historical comparability, enabling vendors to raise prices or restrict usage. Hamilton Lane reduces exposure via in-house data and analytics platforms but still depends on external benchmarks for industry-wide comparability.

Specialized talent as a supplier

Experienced investment professionals and specialized engineers are scarce and mobile, giving them outsized bargaining power; typical private equity carried interest remains around 20% while standard management fees are near 2%, reinforcing negotiation leverage. Compensation cycles and carry structures amplify retention importance to preserve GP access and underwriting edge, and tight labor markets can pressure margins and execution capacity.

- Scarcity: experienced hires drive deal origination and execution

- Compensation: 20% carried interest, ~2% fees influence mobility

- Retention: critical for GP access and competitive edge

- Risk: tight labor markets compress margins, limit execution

Financial and operational infrastructure

Administrators, custodians and technology stacks (eg custodians like BNY Mellon, State Street, JPMorgan custody tens of trillions in assets) are foundational for SMAs and funds; vendor consolidation lowers negotiating leverage and raises concentration risk. Operational incidents in 2023–24 caused multi‑day reporting outages for some providers, disrupting client delivery. Multi‑vendor architectures and internal tooling mitigate risk, but vendor switching is costly and complex.

- Concentration: top custodians hold tens of trillions in assets

- Risk: vendor consolidation reduces bargaining power

- Impact: operational incidents cause multi‑day outages

- Mitigation: multi‑vendor + internal tooling, but switching is non‑trivial

Concentrated GPs, custodians and scarce carry talent squeeze PE fees and allocations

Hamilton Lane faces strong supplier power: concentrated top GPs control capacity (global PE dry powder ~$1.6T in 2024) and can demand premium allocations, risking product differentiation and returns. Data vendors and custodians are concentrated (top custodians hold tens of trillions), raising costs and switching barriers. Talent scarcity (carry ~20%, fees ~2%) amplifies retention pressure and margin risk.

| Supplier | Power | 2024 metric |

|---|---|---|

| Top GPs | High | PE dry powder ~$1.6T |

| Data vendors | Medium-High | Preqin/PitchBook market reliance |

| Custodians | High | Top custodians hold tens of trillions |

| Talent | High | Carry ~20%, fees ~2% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Hamilton Lane, uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and identifying disruptive risks and entry barriers to inform strategic positioning and valuation.

A concise, one-sheet Hamilton Lane Porter’s Five Forces summary—pinpoint competitive pressures and relieve analysis bottlenecks for faster, board-ready decisions.

Customers Bargaining Power

Institutional scale mandates

Clients—large pensions, sovereigns, endowments and insurers—tend to issue competitive RFPs and demand bespoke structures, driving aggressive fee negotiations and custom reporting. In 2024 the top 10 pension funds each oversaw more than $100 billion, enabling multi-manager comparisons and strict KPIs that amplify selection leverage. This concentration of mandates concentrates revenue and heightens buyer power over managers.

Fee compression pressure

Market-wide focus on net returns has compressed fees—industry management fees have fallen from the traditional 2% toward roughly 1.3–1.5% and carry expectations have trended toward 15% or below on negotiated deals. Clients increasingly demand low-cost SMAs, zero-to-0.5% co-invest fees and performance-based terms; transparent benchmarking tools bolster buyer leverage. Hamilton Lane must weigh lower pricing against demonstrable value-add and differentiated access.

Switching costs but not prohibitive

Illiquidity and typical private fund lives of about 10 years create meaningful switching frictions for Hamilton Lane clients, yet secondary markets exceeding $100 billion annually and the ability to allocate new capital elsewhere mean redirection is relatively easy. Buyers can dual-track relationships to transition gradually, and advisory mandates are far easier to reassign than closed‑end fund commitments, producing moderate, not absolute, buyer power.

In-sourcing alternatives

In 2024, many large institutions scaled in-house private markets teams, pressuring managers on fees, data access and co-invest volume; Hamilton Lane points to its breadth, scale and proprietary insights cited in its 2024 Global Private Markets Report to defend pricing. Still, credible in-sourcing materially amplifies buyer bargaining power and disciplines manager economics.

- In-sourcing: larger institutions building internal teams

- Pressure points: fees, data access, co-invest volume

- Hamilton Lane defense: breadth, scale, proprietary insights

- Net effect: stronger buyer bargaining power

Demand for data and transparency

Clients now demand granular performance, ESG, and look-through reporting, forcing Hamilton Lane to invest continuously in data systems and specialist staff. Buyers increasingly condition allocations on analytics access and bespoke dashboards, giving investors leverage in fee and service negotiations. Rising transparency expectations in 2024 amplify customer bargaining power across mandates.

- Granular performance reporting required

- ESG and look-through data standard

- Ongoing tech and talent costs

- Analytics access drives allocation

Large pensions' leverage cuts fees to ~1.3-1.5%; secondaries > $100B/year

Clients—large pensions, sovereigns, endowments and insurers—drive bespoke RFPs and aggressive fee negotiation; top 10 pensions in 2024 each oversaw >$100B, amplifying selection leverage. Industry fees moved from 2% toward ~1.3–1.5% and carry to ~15% as secondary markets >$100B/year and in-sourcing strengthen buyer power. Hamilton Lane leans on scale, proprietary data and co-invests but faces sustained buyer pressure.

| Metric | 2024 Value |

|---|---|

| Top 10 pensions AUM | >$100B each |

| Management fee | ~1.3–1.5% |

| Carry | ~15% |

| Secondary market volume | >$100B/year |

What You See Is What You Get

Hamilton Lane Porter's Five Forces Analysis

This preview shows the exact Hamilton Lane Porter's Five Forces analysis you'll receive after purchase. It is the full, professionally formatted document—no placeholders or mockups. Upon payment you’ll get instant access to this identical file, ready for download and use. No customization required.

Description

From Overview to Strategy Blueprint

Hamilton Lane’s Porter’s Five Forces snapshot highlights buyer and supplier power, rival intensity, entry barriers, and substitute risks shaping its private markets advisory business. Our concise review pinpoints strategic strengths and pressure points for investors and managers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hamilton Lane’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated top-tier GPs

Hamilton Lane depends on a concentrated set of elite PE, credit and real asset GPs for allocations and co-invests; Preqin reported about $1.7 trillion of private equity dry powder in 2024, intensifying competition for top GP capacity. These top-tier managers are often oversubscribed, giving them pricing and allocation leverage and driving preferred access toward long-standing, large-scale relationships. Loss of GP access can materially hurt performance and product differentiation.

Scarce proprietary deal flow

Sponsor-sourced direct and co-invest deals are limited and fiercely contested; with Hamilton Lane reporting roughly $884 billion AUM in 2024 and global private equity dry powder near $1.6 trillion in 2024, sponsors can pick partners that underwrite faster or offer larger tickets. This scarcity boosts supplier power to dictate pricing, terms and timing. It forces Hamilton Lane to accelerate diligence cycles and deepen sector expertise to win allocations.

Data and analytics vendors

Third-party data vendors (e.g., Preqin, PitchBook) shape private-markets diligence and reporting; Preqin estimated about 2.5 trillion USD of private capital dry powder in 2024, underscoring dataset importance. Switching providers is costly given integrations and historical comparability, enabling vendors to raise prices or restrict usage. Hamilton Lane reduces exposure via in-house data and analytics platforms but still depends on external benchmarks for industry-wide comparability.

Specialized talent as a supplier

Experienced investment professionals and specialized engineers are scarce and mobile, giving them outsized bargaining power; typical private equity carried interest remains around 20% while standard management fees are near 2%, reinforcing negotiation leverage. Compensation cycles and carry structures amplify retention importance to preserve GP access and underwriting edge, and tight labor markets can pressure margins and execution capacity.

- Scarcity: experienced hires drive deal origination and execution

- Compensation: 20% carried interest, ~2% fees influence mobility

- Retention: critical for GP access and competitive edge

- Risk: tight labor markets compress margins, limit execution

Financial and operational infrastructure

Administrators, custodians and technology stacks (eg custodians like BNY Mellon, State Street, JPMorgan custody tens of trillions in assets) are foundational for SMAs and funds; vendor consolidation lowers negotiating leverage and raises concentration risk. Operational incidents in 2023–24 caused multi‑day reporting outages for some providers, disrupting client delivery. Multi‑vendor architectures and internal tooling mitigate risk, but vendor switching is costly and complex.

- Concentration: top custodians hold tens of trillions in assets

- Risk: vendor consolidation reduces bargaining power

- Impact: operational incidents cause multi‑day outages

- Mitigation: multi‑vendor + internal tooling, but switching is non‑trivial

Concentrated GPs, custodians and scarce carry talent squeeze PE fees and allocations

Hamilton Lane faces strong supplier power: concentrated top GPs control capacity (global PE dry powder ~$1.6T in 2024) and can demand premium allocations, risking product differentiation and returns. Data vendors and custodians are concentrated (top custodians hold tens of trillions), raising costs and switching barriers. Talent scarcity (carry ~20%, fees ~2%) amplifies retention pressure and margin risk.

| Supplier | Power | 2024 metric |

|---|---|---|

| Top GPs | High | PE dry powder ~$1.6T |

| Data vendors | Medium-High | Preqin/PitchBook market reliance |

| Custodians | High | Top custodians hold tens of trillions |

| Talent | High | Carry ~20%, fees ~2% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Hamilton Lane, uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and identifying disruptive risks and entry barriers to inform strategic positioning and valuation.

A concise, one-sheet Hamilton Lane Porter’s Five Forces summary—pinpoint competitive pressures and relieve analysis bottlenecks for faster, board-ready decisions.

Customers Bargaining Power

Institutional scale mandates

Clients—large pensions, sovereigns, endowments and insurers—tend to issue competitive RFPs and demand bespoke structures, driving aggressive fee negotiations and custom reporting. In 2024 the top 10 pension funds each oversaw more than $100 billion, enabling multi-manager comparisons and strict KPIs that amplify selection leverage. This concentration of mandates concentrates revenue and heightens buyer power over managers.

Fee compression pressure

Market-wide focus on net returns has compressed fees—industry management fees have fallen from the traditional 2% toward roughly 1.3–1.5% and carry expectations have trended toward 15% or below on negotiated deals. Clients increasingly demand low-cost SMAs, zero-to-0.5% co-invest fees and performance-based terms; transparent benchmarking tools bolster buyer leverage. Hamilton Lane must weigh lower pricing against demonstrable value-add and differentiated access.

Switching costs but not prohibitive

Illiquidity and typical private fund lives of about 10 years create meaningful switching frictions for Hamilton Lane clients, yet secondary markets exceeding $100 billion annually and the ability to allocate new capital elsewhere mean redirection is relatively easy. Buyers can dual-track relationships to transition gradually, and advisory mandates are far easier to reassign than closed‑end fund commitments, producing moderate, not absolute, buyer power.

In-sourcing alternatives

In 2024, many large institutions scaled in-house private markets teams, pressuring managers on fees, data access and co-invest volume; Hamilton Lane points to its breadth, scale and proprietary insights cited in its 2024 Global Private Markets Report to defend pricing. Still, credible in-sourcing materially amplifies buyer bargaining power and disciplines manager economics.

- In-sourcing: larger institutions building internal teams

- Pressure points: fees, data access, co-invest volume

- Hamilton Lane defense: breadth, scale, proprietary insights

- Net effect: stronger buyer bargaining power

Demand for data and transparency

Clients now demand granular performance, ESG, and look-through reporting, forcing Hamilton Lane to invest continuously in data systems and specialist staff. Buyers increasingly condition allocations on analytics access and bespoke dashboards, giving investors leverage in fee and service negotiations. Rising transparency expectations in 2024 amplify customer bargaining power across mandates.

- Granular performance reporting required

- ESG and look-through data standard

- Ongoing tech and talent costs

- Analytics access drives allocation

Large pensions' leverage cuts fees to ~1.3-1.5%; secondaries > $100B/year

Clients—large pensions, sovereigns, endowments and insurers—drive bespoke RFPs and aggressive fee negotiation; top 10 pensions in 2024 each oversaw >$100B, amplifying selection leverage. Industry fees moved from 2% toward ~1.3–1.5% and carry to ~15% as secondary markets >$100B/year and in-sourcing strengthen buyer power. Hamilton Lane leans on scale, proprietary data and co-invests but faces sustained buyer pressure.

| Metric | 2024 Value |

|---|---|

| Top 10 pensions AUM | >$100B each |

| Management fee | ~1.3–1.5% |

| Carry | ~15% |

| Secondary market volume | >$100B/year |

What You See Is What You Get

Hamilton Lane Porter's Five Forces Analysis

This preview shows the exact Hamilton Lane Porter's Five Forces analysis you'll receive after purchase. It is the full, professionally formatted document—no placeholders or mockups. Upon payment you’ll get instant access to this identical file, ready for download and use. No customization required.