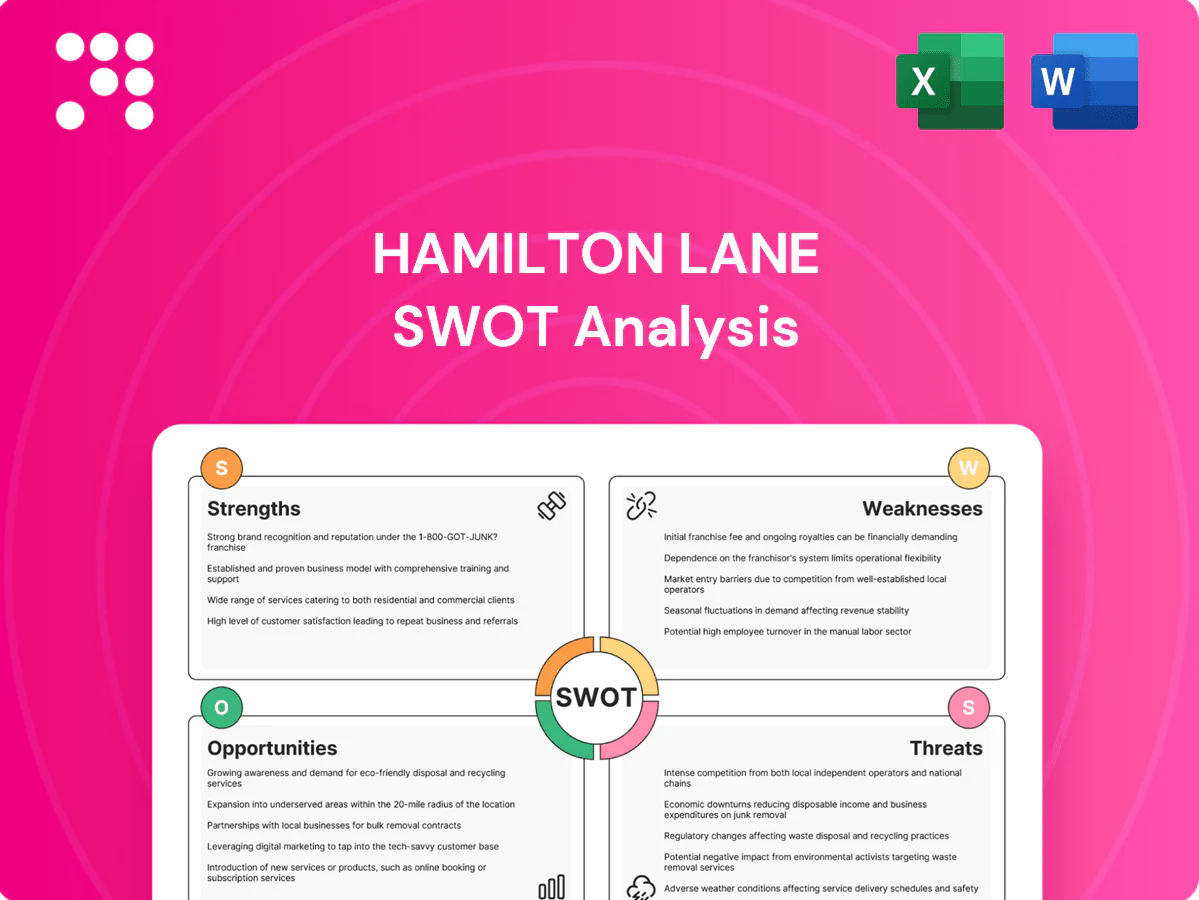

Hamilton Lane SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Hamilton Lane's SWOT highlights its strong private markets leadership, diversified fee streams, and global network, balanced against valuation sensitivity and regulatory risks; unlock the full analysis to access actionable strategies, financial context, and editable deliverables—purchase the complete SWOT for investor-ready insights and planning tools.

Strengths

Global private-markets scale

Hamilton Lane operates at global private-markets scale, overseeing over $900 billion in assets as of mid‑2024, which delivers broad deal flow and benchmarking insights across regions. That scale provides negotiating leverage with GPs and counterparties, improving terms and access. It enables diversified portfolio construction across cycles and sectors, and its reach strengthens client confidence and retention.

Diversified strategies and solutions

Founded in 1991 and with over 34 years of experience, Hamilton Lane spans private equity, private credit and real assets through fund investments, directs, co-invests and secondaries. This diversified product set smooths returns and deployment pacing across market cycles and lets the firm tailor solutions to client risk/return and liquidity needs. The breadth supports cross-selling and wallet-share growth with institutional clients globally.

Data and advisory capabilities

Hamilton Lane leverages proprietary datasets and analytical tools—built over 34 years since its 1991 founding—to strengthen underwriting, risk management and market insight, enabling more precise manager selection and portfolio diagnostics.

Its advisory services expand client engagement beyond capital deployment, converting data-driven perspectives into tailored governance and co-investment opportunities that deepen relationships.

These integrated data and advisory capabilities form a differentiated moat versus peers by translating proprietary analytics into measurable portfolio outcomes and client retention.

Customized separate accounts

Customized separate accounts position Hamilton Lane as an outsourced private markets department, building bespoke portfolios that align with institutional mandates, constraints, and reporting standards; this customization increases client stickiness and provides multi-year fee visibility. Tailored solutions enable the firm to command premium pricing and deepen long-term relationships.

- Outsourced CIO: bespoke portfolio construction

- Mandate alignment: compliance and reporting fidelity

- Revenue resilience: multi-year fee visibility

- Pricing power: ability to charge premiums

Strong LP and GP relationships

Longstanding ties with institutional LPs and top-tier GPs give Hamilton Lane preferred deal flow and informational advantages, supporting co-investments and often enabling fee concessions; the firm reported over $850 billion in assets under management and advisement in 2024, amplifying its sourcing power. These relationships speed due diligence, improve deal selection quality, and create network effects that compound as the platform grows.

- 900+ institutional clients (2024)

- 2,000+ GP relationships

- Preferential co-investment access

- Fee negotiation leverage

Scale, preferred deal flow and multi-year fee visibility; ~900bn AUM, 34+ yrs

Hamilton Lane manages ~900bn AUM/AUA (mid‑2024), delivering scale, sourcing and negotiation leverage.

34+ years and diversified products across PE, credit and real assets enable bespoke separate accounts and multi-year fee visibility.

Proprietary data plus 900+ institutional clients and 2,000+ GP relationships drive preferred deal flow and client retention.

| Metric | 2024 |

|---|---|

| AUM/AUA | ~900bn |

| Institutional clients | 900+ |

| GP relationships | 2,000+ |

| Years operating | 34+ |

What is included in the product

Delivers a strategic overview of Hamilton Lane’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and growth prospects.

Provides a concise Hamilton Lane SWOT matrix for fast, visual strategy alignment and investor-focused decision-making. Editable format lets teams quickly update assumptions, integrate insights into reports and presentations, and respond to changing market priorities.

Weaknesses

Illiquidity and valuation lag

Private assets’ inherent illiquidity limits rapid rebalancing and makes raising cash in stress difficult, as positions cannot be sold quickly without price concessions. Valuation marks are typically updated quarterly, creating a lag behind public markets and obscuring real-time risk profiles. This lag complicates client communication during volatility and can cause liquidity constraints that cap exposure for some investors.

Fee pressure and competition

Clients increasingly push for lower management fees and greater fee transparency, eroding traditional revenue pools. Large multi-asset managers and growing in-house private markets teams intensify pricing pressure, forcing Hamilton Lane to defend margins. Without scale efficiencies margin compression is likely, so clear product differentiation is required to offset commoditization in some segments.

Market-cycle sensitivity

Market-cycle sensitivity ties Hamilton Lane fundraising, exits and performance to economic and rate cycles; with the fed funds target at 5.25–5.50% (mid‑2025) slow M&A and IPO markets delay realizations and DPI, making deployment pacing uneven and squeezing IRRs. Prolonged downturns can weaken track records and reduce incentive fee accruals, pressuring revenue volatility.

Operational complexity

Managing multiple strategies, geographies, and vehicles increases legal, tax, and reporting complexity for Hamilton Lane, which reported approximately $827 billion in AUM and advisory as of June 30, 2024, heightening demands on compliance and documentation; this forces heavy middle/back-office and technology investment to avoid errors or delays that can erode client trust.

- Operational complexity

- High compliance & tax burden

- Tech & middle/back-office capex

- Risk of trust damage from errors

- Overhead can outpace revenue in expansion

Concentration in private markets

Concentration in private markets limits Hamilton Lane’s exposure to liquid beta, narrowing revenue diversification; the firm reported roughly $1.0 trillion AUM in mid‑2024 with over 80% of fee revenue tied to private strategies, and public-market hedges remain noncore. Heavy reliance on private capital flows raises sensitivity to client allocation cuts and makes strategic pivots harder given deep specialization.

- High AUM: ~$1.0T (mid‑2024)

- Private-derived fees >80%

- Low liquid beta exposure

- Vulnerable to allocation cuts

Private markets: illiquidity, fee compression and rising compliance costs hamper returns

Private illiquidity and quarterly marks limit rapid rebalancing and obscure real-time risk; fee pressure from clients and competitors compresses margins; market-cycle sensitivity (fed funds 5.25–5.50% mid‑2025) delays realizations and squeezes IRRs; complex global operations raise compliance and tech costs for Hamilton Lane (~$1.0T AUM mid‑2024; >80% fee revenue from private strategies).

| Metric | Value |

|---|---|

| AUM (mid‑2024) | ~$1.0T |

| Private-fee share | >80% |

| Fed funds (mid‑2025) | 5.25–5.50% |

Preview Before You Purchase

Hamilton Lane SWOT Analysis

This is the actual SWOT analysis document you'll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report, and the complete, editable version becomes available immediately after checkout. You're viewing a live excerpt of the same file included in your download; buy now to unlock the full, detailed Hamilton Lane SWOT analysis.

Elevate Your Analysis with the Complete SWOT Report

Hamilton Lane's SWOT highlights its strong private markets leadership, diversified fee streams, and global network, balanced against valuation sensitivity and regulatory risks; unlock the full analysis to access actionable strategies, financial context, and editable deliverables—purchase the complete SWOT for investor-ready insights and planning tools.

Strengths

Global private-markets scale

Hamilton Lane operates at global private-markets scale, overseeing over $900 billion in assets as of mid‑2024, which delivers broad deal flow and benchmarking insights across regions. That scale provides negotiating leverage with GPs and counterparties, improving terms and access. It enables diversified portfolio construction across cycles and sectors, and its reach strengthens client confidence and retention.

Diversified strategies and solutions

Founded in 1991 and with over 34 years of experience, Hamilton Lane spans private equity, private credit and real assets through fund investments, directs, co-invests and secondaries. This diversified product set smooths returns and deployment pacing across market cycles and lets the firm tailor solutions to client risk/return and liquidity needs. The breadth supports cross-selling and wallet-share growth with institutional clients globally.

Data and advisory capabilities

Hamilton Lane leverages proprietary datasets and analytical tools—built over 34 years since its 1991 founding—to strengthen underwriting, risk management and market insight, enabling more precise manager selection and portfolio diagnostics.

Its advisory services expand client engagement beyond capital deployment, converting data-driven perspectives into tailored governance and co-investment opportunities that deepen relationships.

These integrated data and advisory capabilities form a differentiated moat versus peers by translating proprietary analytics into measurable portfolio outcomes and client retention.

Customized separate accounts

Customized separate accounts position Hamilton Lane as an outsourced private markets department, building bespoke portfolios that align with institutional mandates, constraints, and reporting standards; this customization increases client stickiness and provides multi-year fee visibility. Tailored solutions enable the firm to command premium pricing and deepen long-term relationships.

- Outsourced CIO: bespoke portfolio construction

- Mandate alignment: compliance and reporting fidelity

- Revenue resilience: multi-year fee visibility

- Pricing power: ability to charge premiums

Strong LP and GP relationships

Longstanding ties with institutional LPs and top-tier GPs give Hamilton Lane preferred deal flow and informational advantages, supporting co-investments and often enabling fee concessions; the firm reported over $850 billion in assets under management and advisement in 2024, amplifying its sourcing power. These relationships speed due diligence, improve deal selection quality, and create network effects that compound as the platform grows.

- 900+ institutional clients (2024)

- 2,000+ GP relationships

- Preferential co-investment access

- Fee negotiation leverage

Scale, preferred deal flow and multi-year fee visibility; ~900bn AUM, 34+ yrs

Hamilton Lane manages ~900bn AUM/AUA (mid‑2024), delivering scale, sourcing and negotiation leverage.

34+ years and diversified products across PE, credit and real assets enable bespoke separate accounts and multi-year fee visibility.

Proprietary data plus 900+ institutional clients and 2,000+ GP relationships drive preferred deal flow and client retention.

| Metric | 2024 |

|---|---|

| AUM/AUA | ~900bn |

| Institutional clients | 900+ |

| GP relationships | 2,000+ |

| Years operating | 34+ |

What is included in the product

Delivers a strategic overview of Hamilton Lane’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and growth prospects.

Provides a concise Hamilton Lane SWOT matrix for fast, visual strategy alignment and investor-focused decision-making. Editable format lets teams quickly update assumptions, integrate insights into reports and presentations, and respond to changing market priorities.

Weaknesses

Illiquidity and valuation lag

Private assets’ inherent illiquidity limits rapid rebalancing and makes raising cash in stress difficult, as positions cannot be sold quickly without price concessions. Valuation marks are typically updated quarterly, creating a lag behind public markets and obscuring real-time risk profiles. This lag complicates client communication during volatility and can cause liquidity constraints that cap exposure for some investors.

Fee pressure and competition

Clients increasingly push for lower management fees and greater fee transparency, eroding traditional revenue pools. Large multi-asset managers and growing in-house private markets teams intensify pricing pressure, forcing Hamilton Lane to defend margins. Without scale efficiencies margin compression is likely, so clear product differentiation is required to offset commoditization in some segments.

Market-cycle sensitivity

Market-cycle sensitivity ties Hamilton Lane fundraising, exits and performance to economic and rate cycles; with the fed funds target at 5.25–5.50% (mid‑2025) slow M&A and IPO markets delay realizations and DPI, making deployment pacing uneven and squeezing IRRs. Prolonged downturns can weaken track records and reduce incentive fee accruals, pressuring revenue volatility.

Operational complexity

Managing multiple strategies, geographies, and vehicles increases legal, tax, and reporting complexity for Hamilton Lane, which reported approximately $827 billion in AUM and advisory as of June 30, 2024, heightening demands on compliance and documentation; this forces heavy middle/back-office and technology investment to avoid errors or delays that can erode client trust.

- Operational complexity

- High compliance & tax burden

- Tech & middle/back-office capex

- Risk of trust damage from errors

- Overhead can outpace revenue in expansion

Concentration in private markets

Concentration in private markets limits Hamilton Lane’s exposure to liquid beta, narrowing revenue diversification; the firm reported roughly $1.0 trillion AUM in mid‑2024 with over 80% of fee revenue tied to private strategies, and public-market hedges remain noncore. Heavy reliance on private capital flows raises sensitivity to client allocation cuts and makes strategic pivots harder given deep specialization.

- High AUM: ~$1.0T (mid‑2024)

- Private-derived fees >80%

- Low liquid beta exposure

- Vulnerable to allocation cuts

Private markets: illiquidity, fee compression and rising compliance costs hamper returns

Private illiquidity and quarterly marks limit rapid rebalancing and obscure real-time risk; fee pressure from clients and competitors compresses margins; market-cycle sensitivity (fed funds 5.25–5.50% mid‑2025) delays realizations and squeezes IRRs; complex global operations raise compliance and tech costs for Hamilton Lane (~$1.0T AUM mid‑2024; >80% fee revenue from private strategies).

| Metric | Value |

|---|---|

| AUM (mid‑2024) | ~$1.0T |

| Private-fee share | >80% |

| Fed funds (mid‑2025) | 5.25–5.50% |

Preview Before You Purchase

Hamilton Lane SWOT Analysis

This is the actual SWOT analysis document you'll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report, and the complete, editable version becomes available immediately after checkout. You're viewing a live excerpt of the same file included in your download; buy now to unlock the full, detailed Hamilton Lane SWOT analysis.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

Hamilton Lane's SWOT highlights its strong private markets leadership, diversified fee streams, and global network, balanced against valuation sensitivity and regulatory risks; unlock the full analysis to access actionable strategies, financial context, and editable deliverables—purchase the complete SWOT for investor-ready insights and planning tools.

Strengths

Global private-markets scale

Hamilton Lane operates at global private-markets scale, overseeing over $900 billion in assets as of mid‑2024, which delivers broad deal flow and benchmarking insights across regions. That scale provides negotiating leverage with GPs and counterparties, improving terms and access. It enables diversified portfolio construction across cycles and sectors, and its reach strengthens client confidence and retention.

Diversified strategies and solutions

Founded in 1991 and with over 34 years of experience, Hamilton Lane spans private equity, private credit and real assets through fund investments, directs, co-invests and secondaries. This diversified product set smooths returns and deployment pacing across market cycles and lets the firm tailor solutions to client risk/return and liquidity needs. The breadth supports cross-selling and wallet-share growth with institutional clients globally.

Data and advisory capabilities

Hamilton Lane leverages proprietary datasets and analytical tools—built over 34 years since its 1991 founding—to strengthen underwriting, risk management and market insight, enabling more precise manager selection and portfolio diagnostics.

Its advisory services expand client engagement beyond capital deployment, converting data-driven perspectives into tailored governance and co-investment opportunities that deepen relationships.

These integrated data and advisory capabilities form a differentiated moat versus peers by translating proprietary analytics into measurable portfolio outcomes and client retention.

Customized separate accounts

Customized separate accounts position Hamilton Lane as an outsourced private markets department, building bespoke portfolios that align with institutional mandates, constraints, and reporting standards; this customization increases client stickiness and provides multi-year fee visibility. Tailored solutions enable the firm to command premium pricing and deepen long-term relationships.

- Outsourced CIO: bespoke portfolio construction

- Mandate alignment: compliance and reporting fidelity

- Revenue resilience: multi-year fee visibility

- Pricing power: ability to charge premiums

Strong LP and GP relationships

Longstanding ties with institutional LPs and top-tier GPs give Hamilton Lane preferred deal flow and informational advantages, supporting co-investments and often enabling fee concessions; the firm reported over $850 billion in assets under management and advisement in 2024, amplifying its sourcing power. These relationships speed due diligence, improve deal selection quality, and create network effects that compound as the platform grows.

- 900+ institutional clients (2024)

- 2,000+ GP relationships

- Preferential co-investment access

- Fee negotiation leverage

Scale, preferred deal flow and multi-year fee visibility; ~900bn AUM, 34+ yrs

Hamilton Lane manages ~900bn AUM/AUA (mid‑2024), delivering scale, sourcing and negotiation leverage.

34+ years and diversified products across PE, credit and real assets enable bespoke separate accounts and multi-year fee visibility.

Proprietary data plus 900+ institutional clients and 2,000+ GP relationships drive preferred deal flow and client retention.

| Metric | 2024 |

|---|---|

| AUM/AUA | ~900bn |

| Institutional clients | 900+ |

| GP relationships | 2,000+ |

| Years operating | 34+ |

What is included in the product

Delivers a strategic overview of Hamilton Lane’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and growth prospects.

Provides a concise Hamilton Lane SWOT matrix for fast, visual strategy alignment and investor-focused decision-making. Editable format lets teams quickly update assumptions, integrate insights into reports and presentations, and respond to changing market priorities.

Weaknesses

Illiquidity and valuation lag

Private assets’ inherent illiquidity limits rapid rebalancing and makes raising cash in stress difficult, as positions cannot be sold quickly without price concessions. Valuation marks are typically updated quarterly, creating a lag behind public markets and obscuring real-time risk profiles. This lag complicates client communication during volatility and can cause liquidity constraints that cap exposure for some investors.

Fee pressure and competition

Clients increasingly push for lower management fees and greater fee transparency, eroding traditional revenue pools. Large multi-asset managers and growing in-house private markets teams intensify pricing pressure, forcing Hamilton Lane to defend margins. Without scale efficiencies margin compression is likely, so clear product differentiation is required to offset commoditization in some segments.

Market-cycle sensitivity

Market-cycle sensitivity ties Hamilton Lane fundraising, exits and performance to economic and rate cycles; with the fed funds target at 5.25–5.50% (mid‑2025) slow M&A and IPO markets delay realizations and DPI, making deployment pacing uneven and squeezing IRRs. Prolonged downturns can weaken track records and reduce incentive fee accruals, pressuring revenue volatility.

Operational complexity

Managing multiple strategies, geographies, and vehicles increases legal, tax, and reporting complexity for Hamilton Lane, which reported approximately $827 billion in AUM and advisory as of June 30, 2024, heightening demands on compliance and documentation; this forces heavy middle/back-office and technology investment to avoid errors or delays that can erode client trust.

- Operational complexity

- High compliance & tax burden

- Tech & middle/back-office capex

- Risk of trust damage from errors

- Overhead can outpace revenue in expansion

Concentration in private markets

Concentration in private markets limits Hamilton Lane’s exposure to liquid beta, narrowing revenue diversification; the firm reported roughly $1.0 trillion AUM in mid‑2024 with over 80% of fee revenue tied to private strategies, and public-market hedges remain noncore. Heavy reliance on private capital flows raises sensitivity to client allocation cuts and makes strategic pivots harder given deep specialization.

- High AUM: ~$1.0T (mid‑2024)

- Private-derived fees >80%

- Low liquid beta exposure

- Vulnerable to allocation cuts

Private markets: illiquidity, fee compression and rising compliance costs hamper returns

Private illiquidity and quarterly marks limit rapid rebalancing and obscure real-time risk; fee pressure from clients and competitors compresses margins; market-cycle sensitivity (fed funds 5.25–5.50% mid‑2025) delays realizations and squeezes IRRs; complex global operations raise compliance and tech costs for Hamilton Lane (~$1.0T AUM mid‑2024; >80% fee revenue from private strategies).

| Metric | Value |

|---|---|

| AUM (mid‑2024) | ~$1.0T |

| Private-fee share | >80% |

| Fed funds (mid‑2025) | 5.25–5.50% |

Preview Before You Purchase

Hamilton Lane SWOT Analysis

This is the actual SWOT analysis document you'll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report, and the complete, editable version becomes available immediately after checkout. You're viewing a live excerpt of the same file included in your download; buy now to unlock the full, detailed Hamilton Lane SWOT analysis.