Hang Lung Group Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Hang Lung Group faces evolving retail and office dynamics, rising tenant bargaining power, and regional development risks that shape its competitive positioning; understanding these forces clarifies strategic levers and vulnerabilities. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated land supply via government and state entities

In Hong Kong (all land held on government lease) and mainland China (urban land is 100% state-owned), government auctions and state-backed entities control prime land release schedules, creating concentrated supplier power. This gives suppliers pricing power and timing leverage that can push up land costs. Hang Lung counters with multi-year land-bank planning and selective city/cluster strategies. Cyclical policy shifts, however, can still tighten access and elevate acquisition costs.

Large general contractors and specialist trades

Grade-A malls and office towers need Tier-1 general contractors and niche MEP/façade specialists, a shallow supplier pool that can command higher margins or reallocate capacity to other projects. Framework agreements and competitive tenders mitigate price risk, but execution risk—delays, workmanship or subcontractor shortages—still concentrates power with suppliers. Cost spikes or schedule slippages directly erode IRR and push back leasing timelines, increasing holding and financing costs.

Building materials and fit-out inputs

Steel, cement, glass, HVAC and interior finishes remain globally tradable but exposed to volatile commodity cycles, with premium-grade materials often 10-20% pricier; supplier fragmentation limits bargaining power. Logistics, technical specs and quality standards for trophy assets narrow choices despite many vendors. Hang Lung’s scale secures volume discounts and supply stability, while 2024 saw a c.15% rise in vetted green suppliers, raising switching costs.

Design, branding, and technology vendors

Signature architects, luxury retail planners and leading proptech firms remain concentrated at the top in 2024, raising Hang Lung Group’s dependence as reputational value and deep technical integration increase switching costs. Long-term, highly customized contracts and fit-outs amplify vendor lock-in and lifecycle costs. Rebalancing requires hard negotiation on IP ownership, interoperability clauses and phased upgrade schedules to preserve flexibility.

- Concentration: top-tier vendors limited

- Risk: high integration + long contracts

- Mitigation: IP negotiation

- Mitigation: enforce interoperability

- Mitigation: phase upgrades

Municipal utilities and regulatory approvals

Municipal utilities and fit-out permits function as quasi-monopoly inputs in Hong Kong—power is supplied by two firms (CLP, HK Electric), water by the Water Supplies Department and major transport links require MTR or government approvals; connection timelines and compliance routinely define project critical paths. Policy-driven ESG, safety and accessibility rules add measurable cost and time, and proactive stakeholder management reduces but does not remove supplier asymmetry.

- Power: 2 dominant suppliers (CLP, HK Electric)

- Water: government-controlled supply

- Transport: MTR/government approvals

- Permits: dictate critical path

- Mitigation: stakeholder engagement lowers but not removes risk

State land control, utility duopoly and +15% vetted green suppliers raise supplier leverage

Government-controlled land releases and state-backed developers give suppliers timing/pricing leverage; Hang Lung offsets with land-bank planning. Tier-1 contractors and niche MEP/façade firms concentrate execution risk; premium materials run c.10–20% higher. Utilities concentrated (CLP, HK Electric) and vetted green suppliers rose c.15% in 2024, increasing switching costs.

| Input | 2024 datapoint |

|---|---|

| Land control | Government/state auctions |

| Power suppliers | 2 dominant (CLP, HK Electric) |

| Green suppliers | +15% vetted (2024) |

| Premium materials | +10–20% |

What is included in the product

Tailored Porter’s Five Forces analysis for Hang Lung Group, uncovering competitive intensity, buyer and supplier power, threats from new entrants and substitutes, and disruptive market forces that shape pricing, profitability and strategic positioning.

A clear one-sheet summary of Hang Lung Group's five forces for quick strategic decisions, with customizable pressure levels and an instant spider chart to pinpoint pain points and guide real estate investment actions.

Customers Bargaining Power

Anchor luxury and fast-fashion tenants

Global luxury names and fast-fashion chains drive footfall and center positioning — the global personal luxury goods market reached about €330bn in 2023, giving such tenants leverage on rents, incentives and bespoke store formats. Co-tenancy clauses and marketing support are commonly negotiated, with operators trading incentives for guaranteed anchor presence. Hang Lung’s premium locations report above-market sales productivity, allowing portfolio-wide relationships to exchange concessions for multi-site rollouts (typically 3–10 malls).

Blue-chip office tenants

Blue-chip MNCs and financial institutions press Hang Lung for large contiguous floor plates, stringent sustainability specs and flexible lease terms; in soft cycles they commonly extract rent-free periods and fit-out contributions, driving incentives up—CBRE Asia 2024 found over 60% of occupiers rank sustainability as a key leasing criterion. High building quality and transit proximity remain potent counterweights, while green certifications and wellness features increasingly decide tenancy.

SME retailers and F&B operators

Fragmented SME retailers and F&B operators exert limited individual bargaining power, yet collectively they drive occupancy and tenant mix, making their aggregate behavior critical to revenue stability. Turnover rents and short-term leases spread landlord risk but raise churn and marketing costs as operators adjust to sales volatility. A curated tenant mix and experience-led offerings can increase willingness to pay and dwell time. Management must balance tenant diversity with operational stability to protect long-term cashflows.

Serviced apartment guests and corporates

Corporate housing contracts drive strong negotiating leverage—volume discounts and strict SLAs are common, while alternative lodging (OTA-listed apartments, hotels) caps Hang Lung Group’s pricing power; prime locations and consistent service still support rate premiums. IATA reported 2024 global business travel recovery near 90% of 2019, boosting corporate demand; dynamic pricing and ancillary services (F&B, housekeeping, meeting rooms) improve yield and reduce single-client dependency.

- Corporate discount pressure: frequent volume SLAs

- Market cap: OTA/hotel alternatives limit price hikes

- Yield levers: dynamic pricing + ancillary revenue

Digital-native and omnichannel expectations

Tenants increasingly demand data sharing, footfall analytics and omnichannel enablement, shifting bargaining from pure lease terms to tech and marketing support; centers offering experiential programming reported stronger rent resilience in 2024, with market-leading malls seeing occupancy around 95% and mid-single-digit rent growth.

- Tenants: data, analytics, omnichannel

- Landlord role: tech + marketing provider

- Advantage: experiential traffic → better economics

- Risk: underinvestment → higher vacancy, weaker rent growth

Luxury anchors (€330bn) boost malls as sustainability-driven occupiers rise

Anchor luxury tenants wield strong rent/leasing leverage (global personal luxury goods €330bn in 2023) while blue‑chip occupiers extract sustainability, contiguous space and incentives (CBRE Asia 2024: >60% cite sustainability). Fragmented SMEs hold limited individual power but collectively drive occupancy and churn; leading malls posted ~95% occupancy and mid‑single‑digit rent growth in 2024, with business travel ~90% of 2019 (IATA 2024).

| Metric | Value (year) |

|---|---|

| Global luxury market | €330bn (2023) |

| Leading mall occupancy | ~95% (2024) |

| Rent growth | Mid‑single‑digit (2024) |

| Sustainability priority | >60% occupiers (CBRE Asia 2024) |

| Business travel recovery | ~90% of 2019 (IATA 2024) |

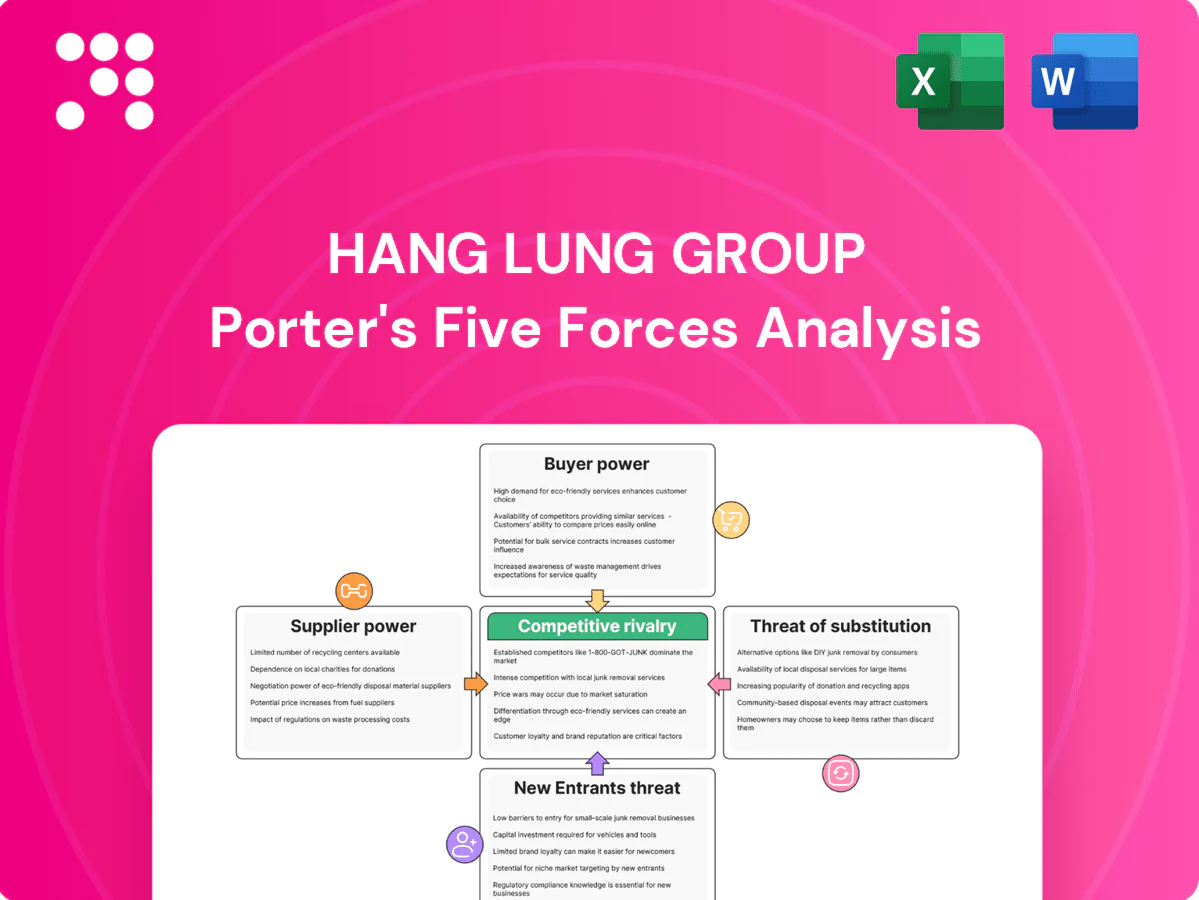

What You See Is What You Get

Hang Lung Group Porter's Five Forces Analysis

This preview shows the complete Hang Lung Group Porter's Five Forces analysis and is the exact document you'll receive upon purchase. It provides a detailed assessment of competitive rivalry, buyer and supplier power, and threats from new entrants and substitutes. No placeholders or samples—fully formatted and ready for immediate download.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Hang Lung Group faces evolving retail and office dynamics, rising tenant bargaining power, and regional development risks that shape its competitive positioning; understanding these forces clarifies strategic levers and vulnerabilities. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated land supply via government and state entities

In Hong Kong (all land held on government lease) and mainland China (urban land is 100% state-owned), government auctions and state-backed entities control prime land release schedules, creating concentrated supplier power. This gives suppliers pricing power and timing leverage that can push up land costs. Hang Lung counters with multi-year land-bank planning and selective city/cluster strategies. Cyclical policy shifts, however, can still tighten access and elevate acquisition costs.

Large general contractors and specialist trades

Grade-A malls and office towers need Tier-1 general contractors and niche MEP/façade specialists, a shallow supplier pool that can command higher margins or reallocate capacity to other projects. Framework agreements and competitive tenders mitigate price risk, but execution risk—delays, workmanship or subcontractor shortages—still concentrates power with suppliers. Cost spikes or schedule slippages directly erode IRR and push back leasing timelines, increasing holding and financing costs.

Building materials and fit-out inputs

Steel, cement, glass, HVAC and interior finishes remain globally tradable but exposed to volatile commodity cycles, with premium-grade materials often 10-20% pricier; supplier fragmentation limits bargaining power. Logistics, technical specs and quality standards for trophy assets narrow choices despite many vendors. Hang Lung’s scale secures volume discounts and supply stability, while 2024 saw a c.15% rise in vetted green suppliers, raising switching costs.

Design, branding, and technology vendors

Signature architects, luxury retail planners and leading proptech firms remain concentrated at the top in 2024, raising Hang Lung Group’s dependence as reputational value and deep technical integration increase switching costs. Long-term, highly customized contracts and fit-outs amplify vendor lock-in and lifecycle costs. Rebalancing requires hard negotiation on IP ownership, interoperability clauses and phased upgrade schedules to preserve flexibility.

- Concentration: top-tier vendors limited

- Risk: high integration + long contracts

- Mitigation: IP negotiation

- Mitigation: enforce interoperability

- Mitigation: phase upgrades

Municipal utilities and regulatory approvals

Municipal utilities and fit-out permits function as quasi-monopoly inputs in Hong Kong—power is supplied by two firms (CLP, HK Electric), water by the Water Supplies Department and major transport links require MTR or government approvals; connection timelines and compliance routinely define project critical paths. Policy-driven ESG, safety and accessibility rules add measurable cost and time, and proactive stakeholder management reduces but does not remove supplier asymmetry.

- Power: 2 dominant suppliers (CLP, HK Electric)

- Water: government-controlled supply

- Transport: MTR/government approvals

- Permits: dictate critical path

- Mitigation: stakeholder engagement lowers but not removes risk

State land control, utility duopoly and +15% vetted green suppliers raise supplier leverage

Government-controlled land releases and state-backed developers give suppliers timing/pricing leverage; Hang Lung offsets with land-bank planning. Tier-1 contractors and niche MEP/façade firms concentrate execution risk; premium materials run c.10–20% higher. Utilities concentrated (CLP, HK Electric) and vetted green suppliers rose c.15% in 2024, increasing switching costs.

| Input | 2024 datapoint |

|---|---|

| Land control | Government/state auctions |

| Power suppliers | 2 dominant (CLP, HK Electric) |

| Green suppliers | +15% vetted (2024) |

| Premium materials | +10–20% |

What is included in the product

Tailored Porter’s Five Forces analysis for Hang Lung Group, uncovering competitive intensity, buyer and supplier power, threats from new entrants and substitutes, and disruptive market forces that shape pricing, profitability and strategic positioning.

A clear one-sheet summary of Hang Lung Group's five forces for quick strategic decisions, with customizable pressure levels and an instant spider chart to pinpoint pain points and guide real estate investment actions.

Customers Bargaining Power

Anchor luxury and fast-fashion tenants

Global luxury names and fast-fashion chains drive footfall and center positioning — the global personal luxury goods market reached about €330bn in 2023, giving such tenants leverage on rents, incentives and bespoke store formats. Co-tenancy clauses and marketing support are commonly negotiated, with operators trading incentives for guaranteed anchor presence. Hang Lung’s premium locations report above-market sales productivity, allowing portfolio-wide relationships to exchange concessions for multi-site rollouts (typically 3–10 malls).

Blue-chip office tenants

Blue-chip MNCs and financial institutions press Hang Lung for large contiguous floor plates, stringent sustainability specs and flexible lease terms; in soft cycles they commonly extract rent-free periods and fit-out contributions, driving incentives up—CBRE Asia 2024 found over 60% of occupiers rank sustainability as a key leasing criterion. High building quality and transit proximity remain potent counterweights, while green certifications and wellness features increasingly decide tenancy.

SME retailers and F&B operators

Fragmented SME retailers and F&B operators exert limited individual bargaining power, yet collectively they drive occupancy and tenant mix, making their aggregate behavior critical to revenue stability. Turnover rents and short-term leases spread landlord risk but raise churn and marketing costs as operators adjust to sales volatility. A curated tenant mix and experience-led offerings can increase willingness to pay and dwell time. Management must balance tenant diversity with operational stability to protect long-term cashflows.

Serviced apartment guests and corporates

Corporate housing contracts drive strong negotiating leverage—volume discounts and strict SLAs are common, while alternative lodging (OTA-listed apartments, hotels) caps Hang Lung Group’s pricing power; prime locations and consistent service still support rate premiums. IATA reported 2024 global business travel recovery near 90% of 2019, boosting corporate demand; dynamic pricing and ancillary services (F&B, housekeeping, meeting rooms) improve yield and reduce single-client dependency.

- Corporate discount pressure: frequent volume SLAs

- Market cap: OTA/hotel alternatives limit price hikes

- Yield levers: dynamic pricing + ancillary revenue

Digital-native and omnichannel expectations

Tenants increasingly demand data sharing, footfall analytics and omnichannel enablement, shifting bargaining from pure lease terms to tech and marketing support; centers offering experiential programming reported stronger rent resilience in 2024, with market-leading malls seeing occupancy around 95% and mid-single-digit rent growth.

- Tenants: data, analytics, omnichannel

- Landlord role: tech + marketing provider

- Advantage: experiential traffic → better economics

- Risk: underinvestment → higher vacancy, weaker rent growth

Luxury anchors (€330bn) boost malls as sustainability-driven occupiers rise

Anchor luxury tenants wield strong rent/leasing leverage (global personal luxury goods €330bn in 2023) while blue‑chip occupiers extract sustainability, contiguous space and incentives (CBRE Asia 2024: >60% cite sustainability). Fragmented SMEs hold limited individual power but collectively drive occupancy and churn; leading malls posted ~95% occupancy and mid‑single‑digit rent growth in 2024, with business travel ~90% of 2019 (IATA 2024).

| Metric | Value (year) |

|---|---|

| Global luxury market | €330bn (2023) |

| Leading mall occupancy | ~95% (2024) |

| Rent growth | Mid‑single‑digit (2024) |

| Sustainability priority | >60% occupiers (CBRE Asia 2024) |

| Business travel recovery | ~90% of 2019 (IATA 2024) |

What You See Is What You Get

Hang Lung Group Porter's Five Forces Analysis

This preview shows the complete Hang Lung Group Porter's Five Forces analysis and is the exact document you'll receive upon purchase. It provides a detailed assessment of competitive rivalry, buyer and supplier power, and threats from new entrants and substitutes. No placeholders or samples—fully formatted and ready for immediate download.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Hang Lung Group faces evolving retail and office dynamics, rising tenant bargaining power, and regional development risks that shape its competitive positioning; understanding these forces clarifies strategic levers and vulnerabilities. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated land supply via government and state entities

In Hong Kong (all land held on government lease) and mainland China (urban land is 100% state-owned), government auctions and state-backed entities control prime land release schedules, creating concentrated supplier power. This gives suppliers pricing power and timing leverage that can push up land costs. Hang Lung counters with multi-year land-bank planning and selective city/cluster strategies. Cyclical policy shifts, however, can still tighten access and elevate acquisition costs.

Large general contractors and specialist trades

Grade-A malls and office towers need Tier-1 general contractors and niche MEP/façade specialists, a shallow supplier pool that can command higher margins or reallocate capacity to other projects. Framework agreements and competitive tenders mitigate price risk, but execution risk—delays, workmanship or subcontractor shortages—still concentrates power with suppliers. Cost spikes or schedule slippages directly erode IRR and push back leasing timelines, increasing holding and financing costs.

Building materials and fit-out inputs

Steel, cement, glass, HVAC and interior finishes remain globally tradable but exposed to volatile commodity cycles, with premium-grade materials often 10-20% pricier; supplier fragmentation limits bargaining power. Logistics, technical specs and quality standards for trophy assets narrow choices despite many vendors. Hang Lung’s scale secures volume discounts and supply stability, while 2024 saw a c.15% rise in vetted green suppliers, raising switching costs.

Design, branding, and technology vendors

Signature architects, luxury retail planners and leading proptech firms remain concentrated at the top in 2024, raising Hang Lung Group’s dependence as reputational value and deep technical integration increase switching costs. Long-term, highly customized contracts and fit-outs amplify vendor lock-in and lifecycle costs. Rebalancing requires hard negotiation on IP ownership, interoperability clauses and phased upgrade schedules to preserve flexibility.

- Concentration: top-tier vendors limited

- Risk: high integration + long contracts

- Mitigation: IP negotiation

- Mitigation: enforce interoperability

- Mitigation: phase upgrades

Municipal utilities and regulatory approvals

Municipal utilities and fit-out permits function as quasi-monopoly inputs in Hong Kong—power is supplied by two firms (CLP, HK Electric), water by the Water Supplies Department and major transport links require MTR or government approvals; connection timelines and compliance routinely define project critical paths. Policy-driven ESG, safety and accessibility rules add measurable cost and time, and proactive stakeholder management reduces but does not remove supplier asymmetry.

- Power: 2 dominant suppliers (CLP, HK Electric)

- Water: government-controlled supply

- Transport: MTR/government approvals

- Permits: dictate critical path

- Mitigation: stakeholder engagement lowers but not removes risk

State land control, utility duopoly and +15% vetted green suppliers raise supplier leverage

Government-controlled land releases and state-backed developers give suppliers timing/pricing leverage; Hang Lung offsets with land-bank planning. Tier-1 contractors and niche MEP/façade firms concentrate execution risk; premium materials run c.10–20% higher. Utilities concentrated (CLP, HK Electric) and vetted green suppliers rose c.15% in 2024, increasing switching costs.

| Input | 2024 datapoint |

|---|---|

| Land control | Government/state auctions |

| Power suppliers | 2 dominant (CLP, HK Electric) |

| Green suppliers | +15% vetted (2024) |

| Premium materials | +10–20% |

What is included in the product

Tailored Porter’s Five Forces analysis for Hang Lung Group, uncovering competitive intensity, buyer and supplier power, threats from new entrants and substitutes, and disruptive market forces that shape pricing, profitability and strategic positioning.

A clear one-sheet summary of Hang Lung Group's five forces for quick strategic decisions, with customizable pressure levels and an instant spider chart to pinpoint pain points and guide real estate investment actions.

Customers Bargaining Power

Anchor luxury and fast-fashion tenants

Global luxury names and fast-fashion chains drive footfall and center positioning — the global personal luxury goods market reached about €330bn in 2023, giving such tenants leverage on rents, incentives and bespoke store formats. Co-tenancy clauses and marketing support are commonly negotiated, with operators trading incentives for guaranteed anchor presence. Hang Lung’s premium locations report above-market sales productivity, allowing portfolio-wide relationships to exchange concessions for multi-site rollouts (typically 3–10 malls).

Blue-chip office tenants

Blue-chip MNCs and financial institutions press Hang Lung for large contiguous floor plates, stringent sustainability specs and flexible lease terms; in soft cycles they commonly extract rent-free periods and fit-out contributions, driving incentives up—CBRE Asia 2024 found over 60% of occupiers rank sustainability as a key leasing criterion. High building quality and transit proximity remain potent counterweights, while green certifications and wellness features increasingly decide tenancy.

SME retailers and F&B operators

Fragmented SME retailers and F&B operators exert limited individual bargaining power, yet collectively they drive occupancy and tenant mix, making their aggregate behavior critical to revenue stability. Turnover rents and short-term leases spread landlord risk but raise churn and marketing costs as operators adjust to sales volatility. A curated tenant mix and experience-led offerings can increase willingness to pay and dwell time. Management must balance tenant diversity with operational stability to protect long-term cashflows.

Serviced apartment guests and corporates

Corporate housing contracts drive strong negotiating leverage—volume discounts and strict SLAs are common, while alternative lodging (OTA-listed apartments, hotels) caps Hang Lung Group’s pricing power; prime locations and consistent service still support rate premiums. IATA reported 2024 global business travel recovery near 90% of 2019, boosting corporate demand; dynamic pricing and ancillary services (F&B, housekeeping, meeting rooms) improve yield and reduce single-client dependency.

- Corporate discount pressure: frequent volume SLAs

- Market cap: OTA/hotel alternatives limit price hikes

- Yield levers: dynamic pricing + ancillary revenue

Digital-native and omnichannel expectations

Tenants increasingly demand data sharing, footfall analytics and omnichannel enablement, shifting bargaining from pure lease terms to tech and marketing support; centers offering experiential programming reported stronger rent resilience in 2024, with market-leading malls seeing occupancy around 95% and mid-single-digit rent growth.

- Tenants: data, analytics, omnichannel

- Landlord role: tech + marketing provider

- Advantage: experiential traffic → better economics

- Risk: underinvestment → higher vacancy, weaker rent growth

Luxury anchors (€330bn) boost malls as sustainability-driven occupiers rise

Anchor luxury tenants wield strong rent/leasing leverage (global personal luxury goods €330bn in 2023) while blue‑chip occupiers extract sustainability, contiguous space and incentives (CBRE Asia 2024: >60% cite sustainability). Fragmented SMEs hold limited individual power but collectively drive occupancy and churn; leading malls posted ~95% occupancy and mid‑single‑digit rent growth in 2024, with business travel ~90% of 2019 (IATA 2024).

| Metric | Value (year) |

|---|---|

| Global luxury market | €330bn (2023) |

| Leading mall occupancy | ~95% (2024) |

| Rent growth | Mid‑single‑digit (2024) |

| Sustainability priority | >60% occupiers (CBRE Asia 2024) |

| Business travel recovery | ~90% of 2019 (IATA 2024) |

What You See Is What You Get

Hang Lung Group Porter's Five Forces Analysis

This preview shows the complete Hang Lung Group Porter's Five Forces analysis and is the exact document you'll receive upon purchase. It provides a detailed assessment of competitive rivalry, buyer and supplier power, and threats from new entrants and substitutes. No placeholders or samples—fully formatted and ready for immediate download.