Hang Seng Bank Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

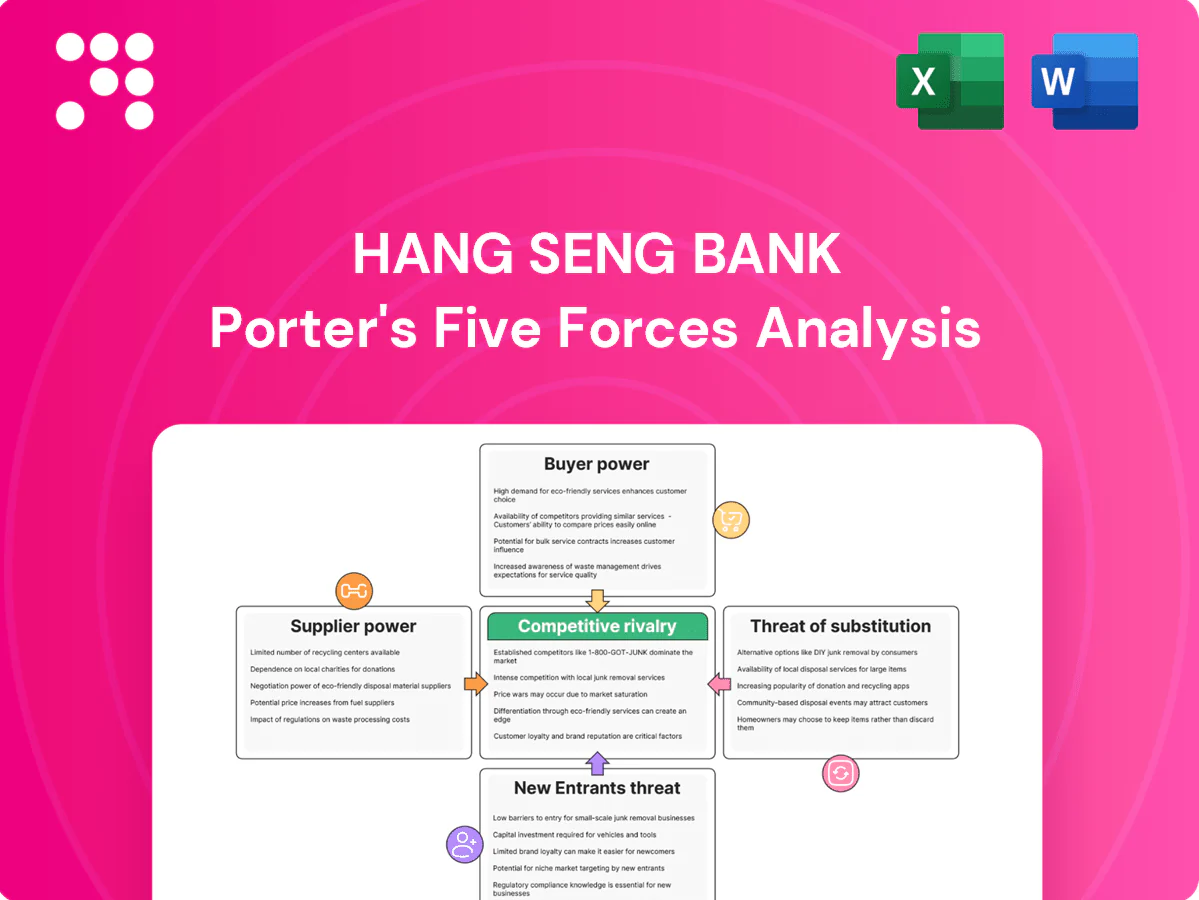

Hang Seng Bank faces intense competitive rivalry from big Hong Kong banks and fintech challengers, while regulatory scrutiny and strong depositor bargaining shape margins; supplier power is moderate and threat of new entrants is constrained by scale and trust. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hang Seng Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Funding and Liquidity Providers

Wholesale funding, interbank markets and central bank liquidity are critical inputs for Hang Seng; diversified retail and corporate deposits limit reliance on volatile wholesale lines. In stress, wholesale suppliers can reprice or ration funds, forcing higher funding costs and tighter liquidity. Hang Seng’s strong credit profile and HSBC backing mitigate but do not eliminate rollover and repricing risks.

Technology and Core Banking Vendors

Core systems, cloud, cybersecurity and payment rails for Hang Seng are concentrated among vendors such as Temenos, FIS, Fiserv, Finastra and hyperscalers (AWS, Microsoft), giving suppliers leverage through high switching costs and integration risk. Long multi‑year contracts commonly embed pricing power and service dependencies. Hang Seng’s scale improves negotiation but HKMA continuity and uptime obligations materially limit suppliers’ ability to extract excessive concessions.

Talent and Specialist Expertise

Front-office bankers, risk, compliance and data scientists remain scarce, increasing suppliers' leverage over Hang Seng Bank. Tight Hong Kong labor markets (unemployment ~3.1% in 2024) elevate wage pressure and hiring costs. Retention, licensing and niche skills deepen dependence despite a strong employer brand. Rivals and fintechs continue active poaching, sustaining turnover risk.

Data, Analytics, and Credit Bureaus

Access to high-quality bureau and analytics data materially improves Hang Seng’s underwriting and personalization; Hong Kong’s population ~7.4 million (2024) concentrates credit activity, while vendors command premium pricing for advanced datasets and models, and API/model lock-in raises switching costs; alternative data expands signals but regulatory and privacy compliance narrows usable sources.

- Premium fees: advanced datasets and models — high subscription/usage costs

- Vendor lock-in: proprietary APIs/models increase switching friction

- Alternative data: diversifies inputs but compliance limits providers

Payment Networks and Custodians

Card schemes are highly concentrated—Visa and Mastercard together processed over 80% of global card transactions in 2024—so network rules and standardized fee schedules sharply limit Hang Seng Bank’s negotiation room; volume discounts offset some costs but scheme fee changes are passed through rapidly. Global custody is likewise concentrated among BNY Mellon, State Street, JPMorgan, Citi and HSBC, creating structural dependency for clearing and cross-border services.

- Concentration: Visa + Mastercard >80% (2024)

- Custodial dominance: BNY Mellon, State Street, JPMorgan, Citi, HSBC

- Negotiation limits: network rules, standardized fees

- Mitigants: volume discounts; quick pass-through of scheme changes

High supplier power: card schemes > 80% vol; HK 7.4m pop

Wholesale funding, core tech vendors (Temenos, FIS, hyperscalers) and talent wield significant supplier power; Hang Seng’s HSBC backing and retail deposits (HK pop 7.4m) mitigate but do not remove rollover, pricing and switching risks. Card schemes (Visa+Mastercard >80% global volume 2024) and custodians concentrate fees; advanced data and niche hires raise costs amid 3.1% HK unemployment (2024).

| Supplier | 2024 metric |

|---|---|

| Card schemes | Visa+MC >80% global vol |

| Labor | HK unemployment 3.1% |

| Population | HK 7.4m |

What is included in the product

Tailored Porter's Five Forces analysis for Hang Seng Bank that uncovers competitive intensity, buyer and supplier leverage, threat of new entrants and substitutes, plus regulatory and digital disruptions shaping profitability and strategic positioning.

Clear, one-sheet Porter's Five Forces for Hang Seng Bank that pinpoints competitive pain points, enables rapid strategic decisions, and exports cleanly into decks or reports.

Customers Bargaining Power

Retail Depositors and Borrowers

Retail depositors and borrowers can compare Hang Seng rates and fees instantly via digital channels, driving price sensitivity—especially for mortgages and time deposits where a few basis points matter; FPS, which had over 5 million registrations in Hong Kong by 2024, and eKYC notably reduce switching friction. Loyalty programs and ecosystem tie-ins improve stickiness but only partially offset high price-driven churn among rate-sensitive segments.

Affluent and Wealth Clients

Affluent and wealth clients at Hang Seng wield strong bargaining power as high balances and transparent fee structures drive demands for bespoke pricing, preferential rates and premium service. In 2024 these clients commonly multi-bank to extract better offers, forcing rival pricing. Deep relationships can defend margins but require higher service costs and tailored coverage.

SMEs and Corporate Treasuries

SMEs and corporate treasuries hold moderate bargaining power as contestable products—credit lines, trade finance and cash management face intense competition; SMEs constitute over 98% of Hong Kong firms (HK Gov 2024). RFP-driven procurement tightens price and covenant demands, while bundling increases share but compresses yields. Switching costs exist but are falling due to standardized API/ISO 20022 connectivity and platform integration.

Digital-Native Users

User experience and fee transparency drive rapid churn to virtual banks and wallets; in 2024 global digital wallet users exceeded 4 billion, raising benchmarks for zero-fee basic services. Transparent pricing has normalized expectations for no-fee accounts, making cross-sell success hinge on app quality and seamless onboarding. Online reviews and social proof amplify customer bargaining power, accelerating switching.

- UX-driven churn

- Zero-fee expectation

- App quality = cross-sell

- Reviews amplify voice

Institutional Investors

Institutional investors extract tight spreads and strict execution terms from Hang Seng, leveraging scale while economics per trade remain thin; many are global asset managers with mandate-driven best-ex and transparency requirements that raise transaction scrutiny. Large-volume clients secure fee breaks and rebates—Hang Seng remains under HSBC group control (62.14% stake) which shapes institutional relationships and product access.

- Negotiate tight spreads and execution

- Fee breaks and rebates for large volumes

- Best-ex/transparency increases scrutiny

- Broad relationships but thin economics

Digital price pressure: FPS >5m, wallets >4bn, SMEs 98%, rebates 62.14%

Customers exert high price sensitivity via digital channels (FPS >5m HK registrations in 2024) and expect zero-fee accounts (global digital wallet users >4bn in 2024), while affluent clients demand bespoke pricing and SMEs (98% of HK firms 2024) press for competitive cash/credit terms; institutional volumes secure rebates (HSBC stake 62.14%).

| Segment | Power | 2024 metric |

|---|---|---|

| Retail | High | FPS >5m |

| Affluent | Strong | Multi-bank trend |

| SME | Moderate | 98% of firms |

| Inst. | High | HSBC 62.14% |

Same Document Delivered

Hang Seng Bank Porter's Five Forces Analysis

This preview shows the exact Hang Seng Bank Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. It is the full, professionally formatted document, ready for download and use the moment you buy. The analysis covers competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications for investors and managers.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Hang Seng Bank faces intense competitive rivalry from big Hong Kong banks and fintech challengers, while regulatory scrutiny and strong depositor bargaining shape margins; supplier power is moderate and threat of new entrants is constrained by scale and trust. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hang Seng Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Funding and Liquidity Providers

Wholesale funding, interbank markets and central bank liquidity are critical inputs for Hang Seng; diversified retail and corporate deposits limit reliance on volatile wholesale lines. In stress, wholesale suppliers can reprice or ration funds, forcing higher funding costs and tighter liquidity. Hang Seng’s strong credit profile and HSBC backing mitigate but do not eliminate rollover and repricing risks.

Technology and Core Banking Vendors

Core systems, cloud, cybersecurity and payment rails for Hang Seng are concentrated among vendors such as Temenos, FIS, Fiserv, Finastra and hyperscalers (AWS, Microsoft), giving suppliers leverage through high switching costs and integration risk. Long multi‑year contracts commonly embed pricing power and service dependencies. Hang Seng’s scale improves negotiation but HKMA continuity and uptime obligations materially limit suppliers’ ability to extract excessive concessions.

Talent and Specialist Expertise

Front-office bankers, risk, compliance and data scientists remain scarce, increasing suppliers' leverage over Hang Seng Bank. Tight Hong Kong labor markets (unemployment ~3.1% in 2024) elevate wage pressure and hiring costs. Retention, licensing and niche skills deepen dependence despite a strong employer brand. Rivals and fintechs continue active poaching, sustaining turnover risk.

Data, Analytics, and Credit Bureaus

Access to high-quality bureau and analytics data materially improves Hang Seng’s underwriting and personalization; Hong Kong’s population ~7.4 million (2024) concentrates credit activity, while vendors command premium pricing for advanced datasets and models, and API/model lock-in raises switching costs; alternative data expands signals but regulatory and privacy compliance narrows usable sources.

- Premium fees: advanced datasets and models — high subscription/usage costs

- Vendor lock-in: proprietary APIs/models increase switching friction

- Alternative data: diversifies inputs but compliance limits providers

Payment Networks and Custodians

Card schemes are highly concentrated—Visa and Mastercard together processed over 80% of global card transactions in 2024—so network rules and standardized fee schedules sharply limit Hang Seng Bank’s negotiation room; volume discounts offset some costs but scheme fee changes are passed through rapidly. Global custody is likewise concentrated among BNY Mellon, State Street, JPMorgan, Citi and HSBC, creating structural dependency for clearing and cross-border services.

- Concentration: Visa + Mastercard >80% (2024)

- Custodial dominance: BNY Mellon, State Street, JPMorgan, Citi, HSBC

- Negotiation limits: network rules, standardized fees

- Mitigants: volume discounts; quick pass-through of scheme changes

High supplier power: card schemes > 80% vol; HK 7.4m pop

Wholesale funding, core tech vendors (Temenos, FIS, hyperscalers) and talent wield significant supplier power; Hang Seng’s HSBC backing and retail deposits (HK pop 7.4m) mitigate but do not remove rollover, pricing and switching risks. Card schemes (Visa+Mastercard >80% global volume 2024) and custodians concentrate fees; advanced data and niche hires raise costs amid 3.1% HK unemployment (2024).

| Supplier | 2024 metric |

|---|---|

| Card schemes | Visa+MC >80% global vol |

| Labor | HK unemployment 3.1% |

| Population | HK 7.4m |

What is included in the product

Tailored Porter's Five Forces analysis for Hang Seng Bank that uncovers competitive intensity, buyer and supplier leverage, threat of new entrants and substitutes, plus regulatory and digital disruptions shaping profitability and strategic positioning.

Clear, one-sheet Porter's Five Forces for Hang Seng Bank that pinpoints competitive pain points, enables rapid strategic decisions, and exports cleanly into decks or reports.

Customers Bargaining Power

Retail Depositors and Borrowers

Retail depositors and borrowers can compare Hang Seng rates and fees instantly via digital channels, driving price sensitivity—especially for mortgages and time deposits where a few basis points matter; FPS, which had over 5 million registrations in Hong Kong by 2024, and eKYC notably reduce switching friction. Loyalty programs and ecosystem tie-ins improve stickiness but only partially offset high price-driven churn among rate-sensitive segments.

Affluent and Wealth Clients

Affluent and wealth clients at Hang Seng wield strong bargaining power as high balances and transparent fee structures drive demands for bespoke pricing, preferential rates and premium service. In 2024 these clients commonly multi-bank to extract better offers, forcing rival pricing. Deep relationships can defend margins but require higher service costs and tailored coverage.

SMEs and Corporate Treasuries

SMEs and corporate treasuries hold moderate bargaining power as contestable products—credit lines, trade finance and cash management face intense competition; SMEs constitute over 98% of Hong Kong firms (HK Gov 2024). RFP-driven procurement tightens price and covenant demands, while bundling increases share but compresses yields. Switching costs exist but are falling due to standardized API/ISO 20022 connectivity and platform integration.

Digital-Native Users

User experience and fee transparency drive rapid churn to virtual banks and wallets; in 2024 global digital wallet users exceeded 4 billion, raising benchmarks for zero-fee basic services. Transparent pricing has normalized expectations for no-fee accounts, making cross-sell success hinge on app quality and seamless onboarding. Online reviews and social proof amplify customer bargaining power, accelerating switching.

- UX-driven churn

- Zero-fee expectation

- App quality = cross-sell

- Reviews amplify voice

Institutional Investors

Institutional investors extract tight spreads and strict execution terms from Hang Seng, leveraging scale while economics per trade remain thin; many are global asset managers with mandate-driven best-ex and transparency requirements that raise transaction scrutiny. Large-volume clients secure fee breaks and rebates—Hang Seng remains under HSBC group control (62.14% stake) which shapes institutional relationships and product access.

- Negotiate tight spreads and execution

- Fee breaks and rebates for large volumes

- Best-ex/transparency increases scrutiny

- Broad relationships but thin economics

Digital price pressure: FPS >5m, wallets >4bn, SMEs 98%, rebates 62.14%

Customers exert high price sensitivity via digital channels (FPS >5m HK registrations in 2024) and expect zero-fee accounts (global digital wallet users >4bn in 2024), while affluent clients demand bespoke pricing and SMEs (98% of HK firms 2024) press for competitive cash/credit terms; institutional volumes secure rebates (HSBC stake 62.14%).

| Segment | Power | 2024 metric |

|---|---|---|

| Retail | High | FPS >5m |

| Affluent | Strong | Multi-bank trend |

| SME | Moderate | 98% of firms |

| Inst. | High | HSBC 62.14% |

Same Document Delivered

Hang Seng Bank Porter's Five Forces Analysis

This preview shows the exact Hang Seng Bank Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. It is the full, professionally formatted document, ready for download and use the moment you buy. The analysis covers competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications for investors and managers.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Hang Seng Bank faces intense competitive rivalry from big Hong Kong banks and fintech challengers, while regulatory scrutiny and strong depositor bargaining shape margins; supplier power is moderate and threat of new entrants is constrained by scale and trust. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hang Seng Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Funding and Liquidity Providers

Wholesale funding, interbank markets and central bank liquidity are critical inputs for Hang Seng; diversified retail and corporate deposits limit reliance on volatile wholesale lines. In stress, wholesale suppliers can reprice or ration funds, forcing higher funding costs and tighter liquidity. Hang Seng’s strong credit profile and HSBC backing mitigate but do not eliminate rollover and repricing risks.

Technology and Core Banking Vendors

Core systems, cloud, cybersecurity and payment rails for Hang Seng are concentrated among vendors such as Temenos, FIS, Fiserv, Finastra and hyperscalers (AWS, Microsoft), giving suppliers leverage through high switching costs and integration risk. Long multi‑year contracts commonly embed pricing power and service dependencies. Hang Seng’s scale improves negotiation but HKMA continuity and uptime obligations materially limit suppliers’ ability to extract excessive concessions.

Talent and Specialist Expertise

Front-office bankers, risk, compliance and data scientists remain scarce, increasing suppliers' leverage over Hang Seng Bank. Tight Hong Kong labor markets (unemployment ~3.1% in 2024) elevate wage pressure and hiring costs. Retention, licensing and niche skills deepen dependence despite a strong employer brand. Rivals and fintechs continue active poaching, sustaining turnover risk.

Data, Analytics, and Credit Bureaus

Access to high-quality bureau and analytics data materially improves Hang Seng’s underwriting and personalization; Hong Kong’s population ~7.4 million (2024) concentrates credit activity, while vendors command premium pricing for advanced datasets and models, and API/model lock-in raises switching costs; alternative data expands signals but regulatory and privacy compliance narrows usable sources.

- Premium fees: advanced datasets and models — high subscription/usage costs

- Vendor lock-in: proprietary APIs/models increase switching friction

- Alternative data: diversifies inputs but compliance limits providers

Payment Networks and Custodians

Card schemes are highly concentrated—Visa and Mastercard together processed over 80% of global card transactions in 2024—so network rules and standardized fee schedules sharply limit Hang Seng Bank’s negotiation room; volume discounts offset some costs but scheme fee changes are passed through rapidly. Global custody is likewise concentrated among BNY Mellon, State Street, JPMorgan, Citi and HSBC, creating structural dependency for clearing and cross-border services.

- Concentration: Visa + Mastercard >80% (2024)

- Custodial dominance: BNY Mellon, State Street, JPMorgan, Citi, HSBC

- Negotiation limits: network rules, standardized fees

- Mitigants: volume discounts; quick pass-through of scheme changes

High supplier power: card schemes > 80% vol; HK 7.4m pop

Wholesale funding, core tech vendors (Temenos, FIS, hyperscalers) and talent wield significant supplier power; Hang Seng’s HSBC backing and retail deposits (HK pop 7.4m) mitigate but do not remove rollover, pricing and switching risks. Card schemes (Visa+Mastercard >80% global volume 2024) and custodians concentrate fees; advanced data and niche hires raise costs amid 3.1% HK unemployment (2024).

| Supplier | 2024 metric |

|---|---|

| Card schemes | Visa+MC >80% global vol |

| Labor | HK unemployment 3.1% |

| Population | HK 7.4m |

What is included in the product

Tailored Porter's Five Forces analysis for Hang Seng Bank that uncovers competitive intensity, buyer and supplier leverage, threat of new entrants and substitutes, plus regulatory and digital disruptions shaping profitability and strategic positioning.

Clear, one-sheet Porter's Five Forces for Hang Seng Bank that pinpoints competitive pain points, enables rapid strategic decisions, and exports cleanly into decks or reports.

Customers Bargaining Power

Retail Depositors and Borrowers

Retail depositors and borrowers can compare Hang Seng rates and fees instantly via digital channels, driving price sensitivity—especially for mortgages and time deposits where a few basis points matter; FPS, which had over 5 million registrations in Hong Kong by 2024, and eKYC notably reduce switching friction. Loyalty programs and ecosystem tie-ins improve stickiness but only partially offset high price-driven churn among rate-sensitive segments.

Affluent and Wealth Clients

Affluent and wealth clients at Hang Seng wield strong bargaining power as high balances and transparent fee structures drive demands for bespoke pricing, preferential rates and premium service. In 2024 these clients commonly multi-bank to extract better offers, forcing rival pricing. Deep relationships can defend margins but require higher service costs and tailored coverage.

SMEs and Corporate Treasuries

SMEs and corporate treasuries hold moderate bargaining power as contestable products—credit lines, trade finance and cash management face intense competition; SMEs constitute over 98% of Hong Kong firms (HK Gov 2024). RFP-driven procurement tightens price and covenant demands, while bundling increases share but compresses yields. Switching costs exist but are falling due to standardized API/ISO 20022 connectivity and platform integration.

Digital-Native Users

User experience and fee transparency drive rapid churn to virtual banks and wallets; in 2024 global digital wallet users exceeded 4 billion, raising benchmarks for zero-fee basic services. Transparent pricing has normalized expectations for no-fee accounts, making cross-sell success hinge on app quality and seamless onboarding. Online reviews and social proof amplify customer bargaining power, accelerating switching.

- UX-driven churn

- Zero-fee expectation

- App quality = cross-sell

- Reviews amplify voice

Institutional Investors

Institutional investors extract tight spreads and strict execution terms from Hang Seng, leveraging scale while economics per trade remain thin; many are global asset managers with mandate-driven best-ex and transparency requirements that raise transaction scrutiny. Large-volume clients secure fee breaks and rebates—Hang Seng remains under HSBC group control (62.14% stake) which shapes institutional relationships and product access.

- Negotiate tight spreads and execution

- Fee breaks and rebates for large volumes

- Best-ex/transparency increases scrutiny

- Broad relationships but thin economics

Digital price pressure: FPS >5m, wallets >4bn, SMEs 98%, rebates 62.14%

Customers exert high price sensitivity via digital channels (FPS >5m HK registrations in 2024) and expect zero-fee accounts (global digital wallet users >4bn in 2024), while affluent clients demand bespoke pricing and SMEs (98% of HK firms 2024) press for competitive cash/credit terms; institutional volumes secure rebates (HSBC stake 62.14%).

| Segment | Power | 2024 metric |

|---|---|---|

| Retail | High | FPS >5m |

| Affluent | Strong | Multi-bank trend |

| SME | Moderate | 98% of firms |

| Inst. | High | HSBC 62.14% |

Same Document Delivered

Hang Seng Bank Porter's Five Forces Analysis

This preview shows the exact Hang Seng Bank Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. It is the full, professionally formatted document, ready for download and use the moment you buy. The analysis covers competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications for investors and managers.