Hannover Ruck Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Hannover Rück faces moderate buyer power, concentrated reinsurer competition, and evolving regulatory and catastrophe risks that shape its margin profile and strategic choices. Our snapshot highlights these forces but stops short of force-by-force ratings, visual maps, and tailored implications. The complete Porter's Five Forces Analysis uncovers actionable insights on supplier influence, entry barriers, and substitute threats. Unlock the full report to inform investment or strategic decisions.

Suppliers Bargaining Power

Capital providers influence pricing

Shareholders and debt markets supply the risk-bearing capital Hannover Re needs to underwrite; in 2024 capital availability and cost remained key constraints on deal flow. After large-loss years pricing hardened and required returns rose, with 2024 property-cat renewal rates up to about 20% higher in some segments per industry reports. When capital is abundant rates soften and margins compress, so the cost and availability of capital directly shape underwriting appetite and terms.

Retrocession capacity is cyclical

Hannover Re relies on retrocessionaires to manage peak exposures and volatility, and retro pricing/capacity are cyclical — influenced by catastrophe activity such as the ~113bn USD insured losses in 2023 (Swiss Re). Tight retro markets push up Hannover Re’s net retained risk and cost base, raising ceded-to-net volatility. This dependence gives retro suppliers meaningful leverage in stressed periods, driving higher premium and collateral demands.

Critical data and models are concentrated

RMS, AIR Worldwide and CoreLogic are among the few dominant catastrophe-modeling vendors, making critical data and models highly concentrated. Model updates have historically produced double-digit swings in industry modeled losses, materially shifting insurers’ view of risk and capital needs. Multi-million-dollar licensing fees and platform dependency give these suppliers clear bargaining power. Using multiple models reduces but does not remove that leverage.

Specialist talent is scarce

Experienced actuaries, catastrophe modelers and senior underwriters remain scarce and mobile; 2024 industry surveys find about 70% of insurers reporting recruitment difficulties, driving higher compensation and retention costs and concentrating critical knowledge among few employees.

- Knowledge concentration increases supplier power of labor

- Competition raises pay/turnover costs

- Training/culture lower but do not remove scarcity

Brokers control key distribution

Global reinsurance brokers intermediate the majority of placements and, in 2024, continued to dominate market access; top brokers shape panel selection and terms through superior market intelligence. Their fee structures and broker-favored clauses compress reinsurer economics, making Hannover Re reliant on strong broker relationships to secure flow and marquee deals; Hannover Re reported ~€24.3bn GWP in 2024, underscoring scale sensitivity to broker channels.

- Majority of placements via brokers

- Broker intelligence drives panel & terms

- Fees/structures affect underwriting economics

- Hannover Re 2024 GWP ~€24.3bn

Suppliers tighten reins: capital cost, +20% retro and €24.3bn GWP squeeze margins

Suppliers—capital markets, retrocessionaires, modeling firms, brokers and scarce talent—wield material leverage over Hannover Re’s economics in 2024. Capital cost/availability and tightened retro pricing (up ~20% in segments) raised required returns; brokers controlled placement flow (Hannover Re GWP ~€24.3bn) while 70% of insurers reported recruitment difficulties. Concentrated model vendors and 2023’s ~113bn USD insured losses amplified supplier bargaining power.

| Supplier | Power driver | 2024 metric |

|---|---|---|

| Capital markets | Cost/availability | GWP €24.3bn |

| Retrocessionaires | Capacity/pricing | Renewals +~20% |

| Model vendors | Concentrated data | Impacted by 2023 ~$113bn |

| Labor | Scarcity | 70% recruitment issues |

| Brokers | Market access | Major placement control |

What is included in the product

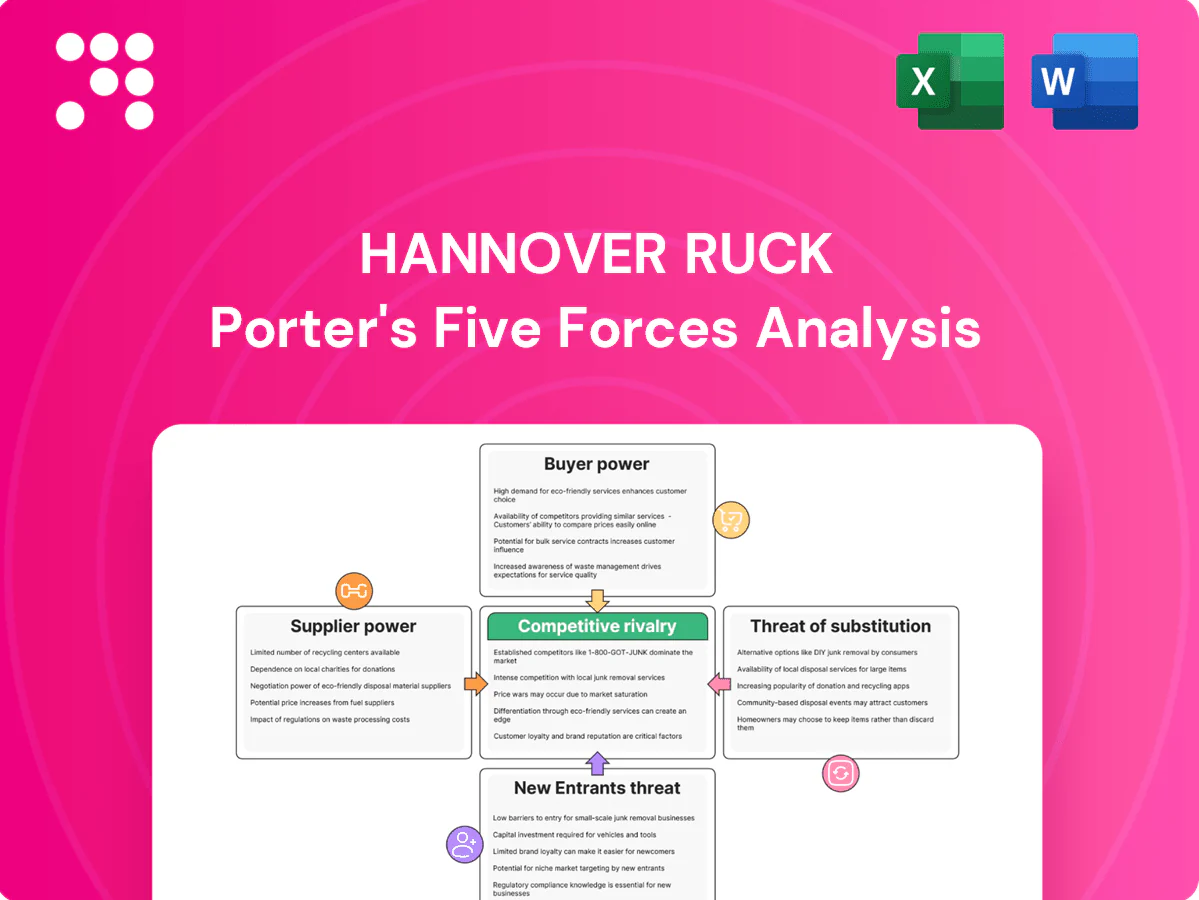

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Hannover Ruck, detailing supplier and buyer power, substitutes, rivalry, and barriers to entry while highlighting disruptive threats and strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces for Hannover Rück that quantifies reinsurance-specific pressures with adjustable inputs and a radar chart for instant strategic clarity—copy-ready for decks, integrates into Excel dashboards and easy for non-finance users to update.

Customers Bargaining Power

Large cedents are highly concentrated

Large cedents—global primary insurers and composites—purchase substantial reinsurance capacity, and in 2024 Hannover Re wrote roughly EUR 30bn gross premiums, highlighting exposure to a concentrated client base. Their scale and alternative markets increase negotiating leverage on price and contract terms. Multi-year partnerships soften but do not eliminate this bargaining power. Retaining these portfolios is strategically vital given their revenue concentration.

Brokered placements intensify negotiation

Brokers aggregate demand and run competitive tenders, delivering side-by-side quotes that increase price transparency and compress margins for reinsurers. Layered placement structures and digital platforms let buyers switch capacity rapidly, intensifying short-term bargaining power. As a top-three global reinsurer, Hannover Re must differentiate on service, analytics and portfolio capacity—not just price—to defend market share.

Alternative capital offers options

Cat bonds and collateralized retro buyers provide uncorrelated, often lower-cost capacity, with global ILS outstanding estimated at about 120bn in 2024 and new cat bond issuance near 11bn that year, expanding capacity in peak-peril zones and reducing buyers dependence on traditional reinsurers.

This optionality strengthens buyers bargaining power by creating outside alternatives and pricing pressure on reinsurers, especially for peak-peril layers where ILS supply grew materially in 2024.

Hannover Re responds by partnering with ILS managers and offering tailored ILS solutions and quota-share structures to retain clients and match alternative capacity pricing.

Data-rich buyers demand customization

- Data-driven cedents: large accounts demand customization

- Pricing risk: bespoke terms can erode returns if mispriced

- Service expectation: real-time quoting + analytics

- Competitive edge: Hannover Re technical analytics preserves profitability

Cyclical price sensitivity

In soft markets buyers press for broader wordings and lower rates-on-line, with industry reports in 2024 noting rate softening of up to 15% in non-cat lines; post-loss hardening tightens terms but buyers resist higher renewals. Budget constraints and regulatory capital needs (Solvency II/NAIC) shape purchasing timing. Hannover Re must actively manage cycle exposure across lines and regions.

- Buyers push broader wordings, lower ROL

- 2024 softening up to 15% in some lines

- Post-loss hardening improves terms but meets resistance

- Budget/regulatory capital drive timing

- Hannover Re must hedge cycle exposure

Major reinsurer faces pricing pressure as ILS growth and cat bonds soften rates up to 15%

Large cedents and brokers exert strong leverage: Hannover Re reported EUR 33.8bn GWP and a 96.3% combined ratio in 2024, while buyers used ILS and cat bonds (EUR 120bn outstanding; ~EUR 11bn issuance) to pressure rates (softening up to 15% in some lines). Hannover Re counters with analytics, ILS partnerships and tailored quota-share deals to defend margins and retain key accounts.

| Metric | 2024 |

|---|---|

| Hannover Re GWP | EUR 33.8bn |

| Combined ratio | 96.3% |

| Global ILS outstanding | EUR 120bn |

| Cat bond issuance | ~EUR 11bn |

| Rate softening | Up to 15% |

Preview the Actual Deliverable

Hannover Ruck Porter's Five Forces Analysis

This Hannover Ruck Porter's Five Forces Analysis presents a concise, professional assessment of competitive dynamics for the company. This preview is the exact document you’ll receive upon purchase—fully formatted and ready to download. No placeholders or samples; what you see is what you get.

Don't Miss the Bigger Picture

Hannover Rück faces moderate buyer power, concentrated reinsurer competition, and evolving regulatory and catastrophe risks that shape its margin profile and strategic choices. Our snapshot highlights these forces but stops short of force-by-force ratings, visual maps, and tailored implications. The complete Porter's Five Forces Analysis uncovers actionable insights on supplier influence, entry barriers, and substitute threats. Unlock the full report to inform investment or strategic decisions.

Suppliers Bargaining Power

Capital providers influence pricing

Shareholders and debt markets supply the risk-bearing capital Hannover Re needs to underwrite; in 2024 capital availability and cost remained key constraints on deal flow. After large-loss years pricing hardened and required returns rose, with 2024 property-cat renewal rates up to about 20% higher in some segments per industry reports. When capital is abundant rates soften and margins compress, so the cost and availability of capital directly shape underwriting appetite and terms.

Retrocession capacity is cyclical

Hannover Re relies on retrocessionaires to manage peak exposures and volatility, and retro pricing/capacity are cyclical — influenced by catastrophe activity such as the ~113bn USD insured losses in 2023 (Swiss Re). Tight retro markets push up Hannover Re’s net retained risk and cost base, raising ceded-to-net volatility. This dependence gives retro suppliers meaningful leverage in stressed periods, driving higher premium and collateral demands.

Critical data and models are concentrated

RMS, AIR Worldwide and CoreLogic are among the few dominant catastrophe-modeling vendors, making critical data and models highly concentrated. Model updates have historically produced double-digit swings in industry modeled losses, materially shifting insurers’ view of risk and capital needs. Multi-million-dollar licensing fees and platform dependency give these suppliers clear bargaining power. Using multiple models reduces but does not remove that leverage.

Specialist talent is scarce

Experienced actuaries, catastrophe modelers and senior underwriters remain scarce and mobile; 2024 industry surveys find about 70% of insurers reporting recruitment difficulties, driving higher compensation and retention costs and concentrating critical knowledge among few employees.

- Knowledge concentration increases supplier power of labor

- Competition raises pay/turnover costs

- Training/culture lower but do not remove scarcity

Brokers control key distribution

Global reinsurance brokers intermediate the majority of placements and, in 2024, continued to dominate market access; top brokers shape panel selection and terms through superior market intelligence. Their fee structures and broker-favored clauses compress reinsurer economics, making Hannover Re reliant on strong broker relationships to secure flow and marquee deals; Hannover Re reported ~€24.3bn GWP in 2024, underscoring scale sensitivity to broker channels.

- Majority of placements via brokers

- Broker intelligence drives panel & terms

- Fees/structures affect underwriting economics

- Hannover Re 2024 GWP ~€24.3bn

Suppliers tighten reins: capital cost, +20% retro and €24.3bn GWP squeeze margins

Suppliers—capital markets, retrocessionaires, modeling firms, brokers and scarce talent—wield material leverage over Hannover Re’s economics in 2024. Capital cost/availability and tightened retro pricing (up ~20% in segments) raised required returns; brokers controlled placement flow (Hannover Re GWP ~€24.3bn) while 70% of insurers reported recruitment difficulties. Concentrated model vendors and 2023’s ~113bn USD insured losses amplified supplier bargaining power.

| Supplier | Power driver | 2024 metric |

|---|---|---|

| Capital markets | Cost/availability | GWP €24.3bn |

| Retrocessionaires | Capacity/pricing | Renewals +~20% |

| Model vendors | Concentrated data | Impacted by 2023 ~$113bn |

| Labor | Scarcity | 70% recruitment issues |

| Brokers | Market access | Major placement control |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Hannover Ruck, detailing supplier and buyer power, substitutes, rivalry, and barriers to entry while highlighting disruptive threats and strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces for Hannover Rück that quantifies reinsurance-specific pressures with adjustable inputs and a radar chart for instant strategic clarity—copy-ready for decks, integrates into Excel dashboards and easy for non-finance users to update.

Customers Bargaining Power

Large cedents are highly concentrated

Large cedents—global primary insurers and composites—purchase substantial reinsurance capacity, and in 2024 Hannover Re wrote roughly EUR 30bn gross premiums, highlighting exposure to a concentrated client base. Their scale and alternative markets increase negotiating leverage on price and contract terms. Multi-year partnerships soften but do not eliminate this bargaining power. Retaining these portfolios is strategically vital given their revenue concentration.

Brokered placements intensify negotiation

Brokers aggregate demand and run competitive tenders, delivering side-by-side quotes that increase price transparency and compress margins for reinsurers. Layered placement structures and digital platforms let buyers switch capacity rapidly, intensifying short-term bargaining power. As a top-three global reinsurer, Hannover Re must differentiate on service, analytics and portfolio capacity—not just price—to defend market share.

Alternative capital offers options

Cat bonds and collateralized retro buyers provide uncorrelated, often lower-cost capacity, with global ILS outstanding estimated at about 120bn in 2024 and new cat bond issuance near 11bn that year, expanding capacity in peak-peril zones and reducing buyers dependence on traditional reinsurers.

This optionality strengthens buyers bargaining power by creating outside alternatives and pricing pressure on reinsurers, especially for peak-peril layers where ILS supply grew materially in 2024.

Hannover Re responds by partnering with ILS managers and offering tailored ILS solutions and quota-share structures to retain clients and match alternative capacity pricing.

Data-rich buyers demand customization

- Data-driven cedents: large accounts demand customization

- Pricing risk: bespoke terms can erode returns if mispriced

- Service expectation: real-time quoting + analytics

- Competitive edge: Hannover Re technical analytics preserves profitability

Cyclical price sensitivity

In soft markets buyers press for broader wordings and lower rates-on-line, with industry reports in 2024 noting rate softening of up to 15% in non-cat lines; post-loss hardening tightens terms but buyers resist higher renewals. Budget constraints and regulatory capital needs (Solvency II/NAIC) shape purchasing timing. Hannover Re must actively manage cycle exposure across lines and regions.

- Buyers push broader wordings, lower ROL

- 2024 softening up to 15% in some lines

- Post-loss hardening improves terms but meets resistance

- Budget/regulatory capital drive timing

- Hannover Re must hedge cycle exposure

Major reinsurer faces pricing pressure as ILS growth and cat bonds soften rates up to 15%

Large cedents and brokers exert strong leverage: Hannover Re reported EUR 33.8bn GWP and a 96.3% combined ratio in 2024, while buyers used ILS and cat bonds (EUR 120bn outstanding; ~EUR 11bn issuance) to pressure rates (softening up to 15% in some lines). Hannover Re counters with analytics, ILS partnerships and tailored quota-share deals to defend margins and retain key accounts.

| Metric | 2024 |

|---|---|

| Hannover Re GWP | EUR 33.8bn |

| Combined ratio | 96.3% |

| Global ILS outstanding | EUR 120bn |

| Cat bond issuance | ~EUR 11bn |

| Rate softening | Up to 15% |

Preview the Actual Deliverable

Hannover Ruck Porter's Five Forces Analysis

This Hannover Ruck Porter's Five Forces Analysis presents a concise, professional assessment of competitive dynamics for the company. This preview is the exact document you’ll receive upon purchase—fully formatted and ready to download. No placeholders or samples; what you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Hannover Rück faces moderate buyer power, concentrated reinsurer competition, and evolving regulatory and catastrophe risks that shape its margin profile and strategic choices. Our snapshot highlights these forces but stops short of force-by-force ratings, visual maps, and tailored implications. The complete Porter's Five Forces Analysis uncovers actionable insights on supplier influence, entry barriers, and substitute threats. Unlock the full report to inform investment or strategic decisions.

Suppliers Bargaining Power

Capital providers influence pricing

Shareholders and debt markets supply the risk-bearing capital Hannover Re needs to underwrite; in 2024 capital availability and cost remained key constraints on deal flow. After large-loss years pricing hardened and required returns rose, with 2024 property-cat renewal rates up to about 20% higher in some segments per industry reports. When capital is abundant rates soften and margins compress, so the cost and availability of capital directly shape underwriting appetite and terms.

Retrocession capacity is cyclical

Hannover Re relies on retrocessionaires to manage peak exposures and volatility, and retro pricing/capacity are cyclical — influenced by catastrophe activity such as the ~113bn USD insured losses in 2023 (Swiss Re). Tight retro markets push up Hannover Re’s net retained risk and cost base, raising ceded-to-net volatility. This dependence gives retro suppliers meaningful leverage in stressed periods, driving higher premium and collateral demands.

Critical data and models are concentrated

RMS, AIR Worldwide and CoreLogic are among the few dominant catastrophe-modeling vendors, making critical data and models highly concentrated. Model updates have historically produced double-digit swings in industry modeled losses, materially shifting insurers’ view of risk and capital needs. Multi-million-dollar licensing fees and platform dependency give these suppliers clear bargaining power. Using multiple models reduces but does not remove that leverage.

Specialist talent is scarce

Experienced actuaries, catastrophe modelers and senior underwriters remain scarce and mobile; 2024 industry surveys find about 70% of insurers reporting recruitment difficulties, driving higher compensation and retention costs and concentrating critical knowledge among few employees.

- Knowledge concentration increases supplier power of labor

- Competition raises pay/turnover costs

- Training/culture lower but do not remove scarcity

Brokers control key distribution

Global reinsurance brokers intermediate the majority of placements and, in 2024, continued to dominate market access; top brokers shape panel selection and terms through superior market intelligence. Their fee structures and broker-favored clauses compress reinsurer economics, making Hannover Re reliant on strong broker relationships to secure flow and marquee deals; Hannover Re reported ~€24.3bn GWP in 2024, underscoring scale sensitivity to broker channels.

- Majority of placements via brokers

- Broker intelligence drives panel & terms

- Fees/structures affect underwriting economics

- Hannover Re 2024 GWP ~€24.3bn

Suppliers tighten reins: capital cost, +20% retro and €24.3bn GWP squeeze margins

Suppliers—capital markets, retrocessionaires, modeling firms, brokers and scarce talent—wield material leverage over Hannover Re’s economics in 2024. Capital cost/availability and tightened retro pricing (up ~20% in segments) raised required returns; brokers controlled placement flow (Hannover Re GWP ~€24.3bn) while 70% of insurers reported recruitment difficulties. Concentrated model vendors and 2023’s ~113bn USD insured losses amplified supplier bargaining power.

| Supplier | Power driver | 2024 metric |

|---|---|---|

| Capital markets | Cost/availability | GWP €24.3bn |

| Retrocessionaires | Capacity/pricing | Renewals +~20% |

| Model vendors | Concentrated data | Impacted by 2023 ~$113bn |

| Labor | Scarcity | 70% recruitment issues |

| Brokers | Market access | Major placement control |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Hannover Ruck, detailing supplier and buyer power, substitutes, rivalry, and barriers to entry while highlighting disruptive threats and strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces for Hannover Rück that quantifies reinsurance-specific pressures with adjustable inputs and a radar chart for instant strategic clarity—copy-ready for decks, integrates into Excel dashboards and easy for non-finance users to update.

Customers Bargaining Power

Large cedents are highly concentrated

Large cedents—global primary insurers and composites—purchase substantial reinsurance capacity, and in 2024 Hannover Re wrote roughly EUR 30bn gross premiums, highlighting exposure to a concentrated client base. Their scale and alternative markets increase negotiating leverage on price and contract terms. Multi-year partnerships soften but do not eliminate this bargaining power. Retaining these portfolios is strategically vital given their revenue concentration.

Brokered placements intensify negotiation

Brokers aggregate demand and run competitive tenders, delivering side-by-side quotes that increase price transparency and compress margins for reinsurers. Layered placement structures and digital platforms let buyers switch capacity rapidly, intensifying short-term bargaining power. As a top-three global reinsurer, Hannover Re must differentiate on service, analytics and portfolio capacity—not just price—to defend market share.

Alternative capital offers options

Cat bonds and collateralized retro buyers provide uncorrelated, often lower-cost capacity, with global ILS outstanding estimated at about 120bn in 2024 and new cat bond issuance near 11bn that year, expanding capacity in peak-peril zones and reducing buyers dependence on traditional reinsurers.

This optionality strengthens buyers bargaining power by creating outside alternatives and pricing pressure on reinsurers, especially for peak-peril layers where ILS supply grew materially in 2024.

Hannover Re responds by partnering with ILS managers and offering tailored ILS solutions and quota-share structures to retain clients and match alternative capacity pricing.

Data-rich buyers demand customization

- Data-driven cedents: large accounts demand customization

- Pricing risk: bespoke terms can erode returns if mispriced

- Service expectation: real-time quoting + analytics

- Competitive edge: Hannover Re technical analytics preserves profitability

Cyclical price sensitivity

In soft markets buyers press for broader wordings and lower rates-on-line, with industry reports in 2024 noting rate softening of up to 15% in non-cat lines; post-loss hardening tightens terms but buyers resist higher renewals. Budget constraints and regulatory capital needs (Solvency II/NAIC) shape purchasing timing. Hannover Re must actively manage cycle exposure across lines and regions.

- Buyers push broader wordings, lower ROL

- 2024 softening up to 15% in some lines

- Post-loss hardening improves terms but meets resistance

- Budget/regulatory capital drive timing

- Hannover Re must hedge cycle exposure

Major reinsurer faces pricing pressure as ILS growth and cat bonds soften rates up to 15%

Large cedents and brokers exert strong leverage: Hannover Re reported EUR 33.8bn GWP and a 96.3% combined ratio in 2024, while buyers used ILS and cat bonds (EUR 120bn outstanding; ~EUR 11bn issuance) to pressure rates (softening up to 15% in some lines). Hannover Re counters with analytics, ILS partnerships and tailored quota-share deals to defend margins and retain key accounts.

| Metric | 2024 |

|---|---|

| Hannover Re GWP | EUR 33.8bn |

| Combined ratio | 96.3% |

| Global ILS outstanding | EUR 120bn |

| Cat bond issuance | ~EUR 11bn |

| Rate softening | Up to 15% |

Preview the Actual Deliverable

Hannover Ruck Porter's Five Forces Analysis

This Hannover Ruck Porter's Five Forces Analysis presents a concise, professional assessment of competitive dynamics for the company. This preview is the exact document you’ll receive upon purchase—fully formatted and ready to download. No placeholders or samples; what you see is what you get.