Hansae Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

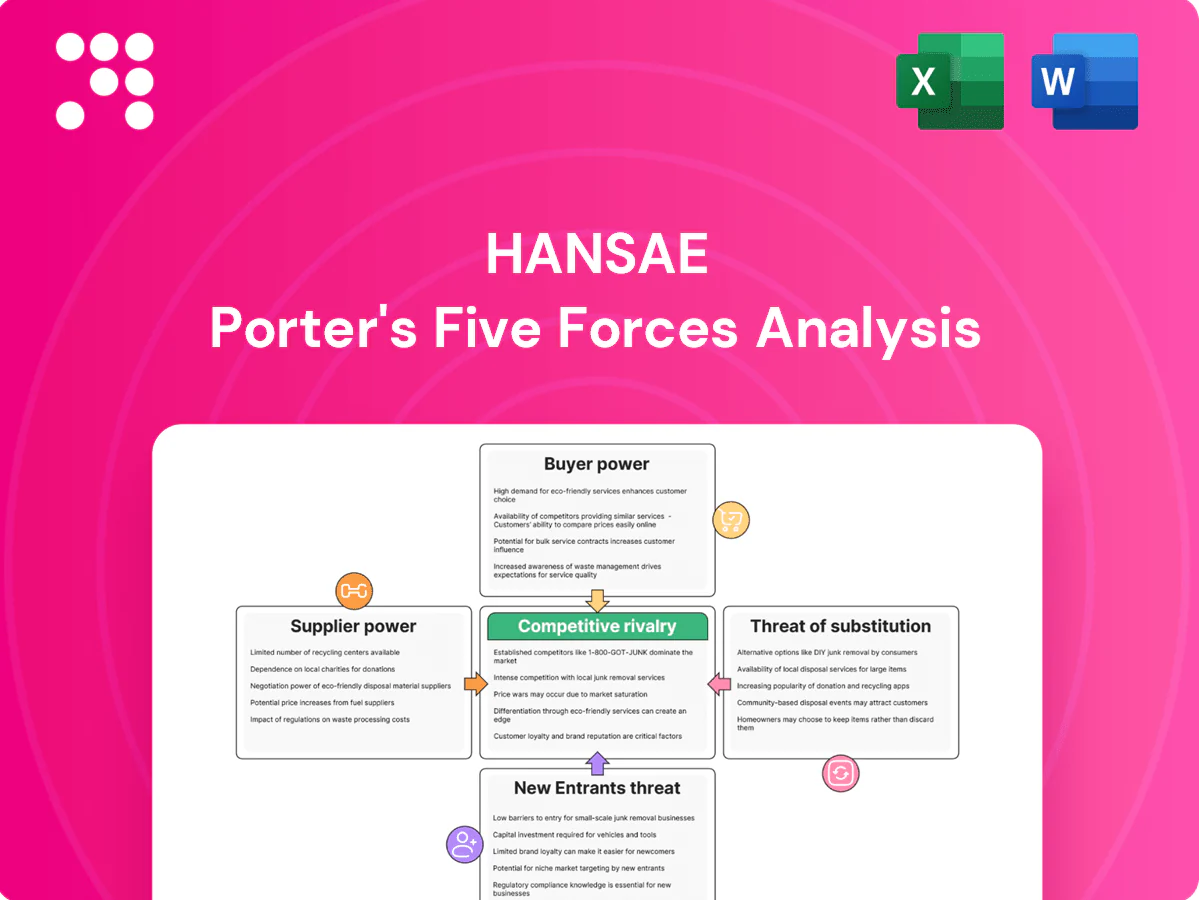

Hansae's Porter's Five Forces snapshot highlights intense buyer power, supplier dynamics, competitive rivalry, and threats from substitutes and new entrants shaping its apparel sourcing business. Understanding these forces reveals where margins and strategic vulnerabilities lie—and where opportunities for differentiation exist. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Hansae’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Multi-sourcing raw materials

Raw material suppliers for cotton, synthetics, trims and dyes can gain leverage when supply tightens, with ICE cotton futures climbing about 12% in 2024 and polyester feedstock volatility similarly elevated. Hansae’s diversified vendor base across Asia, Africa and the Americas reduces single-supplier dependence and supports continuity. Long-term contracts and volume bundling secure price concessions, though commodity swings can still transmit cost shocks to margins.

Specialized fabric dependence

Dependence on a small set of capable mills for moisture-wicking and recycled performance fabrics increases switching costs and supplier leverage, particularly where bluesign or GRS certifications are required.

Co-development deals can secure price and capacity advantages but deepen dependency and raise exit barriers.

Specialized yarn lead-times of 8–12 weeks constrain quick response and amplify supplier bargaining power.

Compliance and ESG constraints

Restricted Substances Lists and growing traceability demands shrink the eligible supplier base; the ECHA candidate list reached 233 SVHCs in 2024, raising compliance scope. Fewer compliant mills strengthen supplier bargaining power as brands compete for certified capacity. Hansae’s stringent audits and onboarding further narrow options. Price premiums for certified inputs commonly compress margins for garmentmakers.

Logistics and energy exposure

Freight carriers and energy providers materially affect delivered cost and timelines; fuel commonly represents roughly 20–30% of maritime transport costs, so 2024 fuel volatility increased landed-cost exposure and schedule risk.

Port congestion and fuel spikes in 2024 amplified supplier leverage, while Hansae’s multi-country network enables route and mode switching to mitigate disruptions, though systemic shocks remain only partially offset.

- Supplier cost influence: fuel ≈20–30% of transport cost

- 2024 impact: higher fuel volatility → increased landed costs

- Mitigation: multi-country routing and modal flexibility

- Limit: systemic shocks cannot be fully hedged

Machinery and technology vendors

Sewing, cutting, dyeing and digital-printing equipment are sourced from a concentrated set of OEMs (Kornit, Lectra, Juki, Karl Mayer among leaders), where proprietary parts and software create strong lock-in and raise switching costs. Preventive maintenance contracts reduce downtime risk but increase fixed operating costs, while capital-intensive upgrades for automation and sustainability further strengthen vendor bargaining power.

- Concentrated OEM supply

- Proprietary parts/software = lock-in

- Maintenance contracts = lower downtime, higher fixed costs

- Automation/sustainability upgrades raise vendor leverage

ICE cotton futures +12%, 8–12 week lead times tighten supplier power

Suppliers of cotton, synthetics and trims gain leverage when supply tightens — ICE cotton futures +12% in 2024 — transmitting cost shocks despite Hansae’s diversified vendor base. Certified performance mills are limited, with 8–12 week lead times and OEM lock-in raising switching costs. Fuel (~20–30% of maritime cost) and port congestion amplify supplier power; multi-country routing mitigates but not eliminates risk.

| Metric | 2024 |

|---|---|

| ICE cotton futures | +12% |

| Lead-times (specialized yarn) | 8–12 weeks |

| Fuel share of maritime cost | 20–30% |

What is included in the product

Tailored exclusively for Hansae, this Porter's Five Forces analysis evaluates competitive rivalry, supplier and buyer power, threats of substitutes and new entrants, and identifies disruptive forces and strategic barriers shaping Hansae's pricing, profitability, and market position.

Hansae Porter's Five Forces condenses competitive pressure into a single, customizable one-sheet—instantly revealing supplier, buyer, entrant, substitute and rivalry risks to relieve strategic analysis pain points.

Customers Bargaining Power

Concentrated global brands

In 2024 large retailers and global sportswear brands accounted for the bulk of order volume, exercising strong negotiating leverage through competitive vendor bidding and relentless year-over-year cost downs. Hansae must win on price, quality and delivery to retain allocations as buyers shift contracts rapidly. Buyer consolidation among top global brands further amplifies this power and compresses supplier margins.

High switching options

Buyers can dual-source across multiple Asian and nearshore manufacturers, with over 50% of tier-1 brands reporting multi-country sourcing strategies in 2024, increasing order portability. Standardized specs and modular tech mean orders move quickly between factories. Vendor scorecards enable rapid reallocation of POs, keeping pricing and service under constant pressure.

Stringent compliance demands

Audits on labor, environment and product safety are non-negotiable and in 2024 buyer audits intensified, making non-compliance — fines, chargebacks or order loss — a clear driver of buyer leverage; fulfilling evolving standards raises Hansae’s unit costs without assured price relief, yet Hansae’s 2024 sustainability and compliance disclosures showing no critical audit failures partially offset customer bargaining power.

Lead-time and flexibility expectations

- Cycle time: 2–6 weeks (2024 industry norm)

- OTIF target: ~95% (2024)

- Chargebacks: 1–3% of invoice value

- Quick-response lowers lead-times and stockouts

ODM co-development dynamics

ODM co-development adds design value and deepens Hansae-brand ties, lowering direct price comparability and switching; a 2024 industry survey found 62% of apparel brands cite ODM partnerships as a primary speed-to-market lever. Buyers still retain leverage by appropriating designs or forcing IP terms, so Hansae's unique tech, quality and lead times determine bargaining shifts.

- ODM strengthens lock-in

- IP risk preserves buyer power

- Speed-to-market is decisive

Buyers lift pressure via multi-sourcing (>50%) and OTIF (~95%)

Buyers exert strong leverage via consolidation and multi-sourcing (>50% of tier-1 brands in 2024), forcing Hansae to compete on price, quality and OTIF (~95%). Chargebacks (1–3% of invoice) and intensified audits raise supplier costs; ODM co-development (62% of brands cite as speed lever) partially reduces pure price competition but IP risk maintains buyer power.

| Metric | 2024 |

|---|---|

| Multi-country sourcing | >50% |

| OTIF target | ~95% |

| Chargebacks | 1–3% invoice |

| ODM cited | 62% |

Same Document Delivered

Hansae Porter's Five Forces Analysis

This preview shows the exact Hansae Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted and ready for download and use the moment you buy. You're viewing the final deliverable.

A Must-Have Tool for Decision-Makers

Hansae's Porter's Five Forces snapshot highlights intense buyer power, supplier dynamics, competitive rivalry, and threats from substitutes and new entrants shaping its apparel sourcing business. Understanding these forces reveals where margins and strategic vulnerabilities lie—and where opportunities for differentiation exist. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Hansae’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Multi-sourcing raw materials

Raw material suppliers for cotton, synthetics, trims and dyes can gain leverage when supply tightens, with ICE cotton futures climbing about 12% in 2024 and polyester feedstock volatility similarly elevated. Hansae’s diversified vendor base across Asia, Africa and the Americas reduces single-supplier dependence and supports continuity. Long-term contracts and volume bundling secure price concessions, though commodity swings can still transmit cost shocks to margins.

Specialized fabric dependence

Dependence on a small set of capable mills for moisture-wicking and recycled performance fabrics increases switching costs and supplier leverage, particularly where bluesign or GRS certifications are required.

Co-development deals can secure price and capacity advantages but deepen dependency and raise exit barriers.

Specialized yarn lead-times of 8–12 weeks constrain quick response and amplify supplier bargaining power.

Compliance and ESG constraints

Restricted Substances Lists and growing traceability demands shrink the eligible supplier base; the ECHA candidate list reached 233 SVHCs in 2024, raising compliance scope. Fewer compliant mills strengthen supplier bargaining power as brands compete for certified capacity. Hansae’s stringent audits and onboarding further narrow options. Price premiums for certified inputs commonly compress margins for garmentmakers.

Logistics and energy exposure

Freight carriers and energy providers materially affect delivered cost and timelines; fuel commonly represents roughly 20–30% of maritime transport costs, so 2024 fuel volatility increased landed-cost exposure and schedule risk.

Port congestion and fuel spikes in 2024 amplified supplier leverage, while Hansae’s multi-country network enables route and mode switching to mitigate disruptions, though systemic shocks remain only partially offset.

- Supplier cost influence: fuel ≈20–30% of transport cost

- 2024 impact: higher fuel volatility → increased landed costs

- Mitigation: multi-country routing and modal flexibility

- Limit: systemic shocks cannot be fully hedged

Machinery and technology vendors

Sewing, cutting, dyeing and digital-printing equipment are sourced from a concentrated set of OEMs (Kornit, Lectra, Juki, Karl Mayer among leaders), where proprietary parts and software create strong lock-in and raise switching costs. Preventive maintenance contracts reduce downtime risk but increase fixed operating costs, while capital-intensive upgrades for automation and sustainability further strengthen vendor bargaining power.

- Concentrated OEM supply

- Proprietary parts/software = lock-in

- Maintenance contracts = lower downtime, higher fixed costs

- Automation/sustainability upgrades raise vendor leverage

ICE cotton futures +12%, 8–12 week lead times tighten supplier power

Suppliers of cotton, synthetics and trims gain leverage when supply tightens — ICE cotton futures +12% in 2024 — transmitting cost shocks despite Hansae’s diversified vendor base. Certified performance mills are limited, with 8–12 week lead times and OEM lock-in raising switching costs. Fuel (~20–30% of maritime cost) and port congestion amplify supplier power; multi-country routing mitigates but not eliminates risk.

| Metric | 2024 |

|---|---|

| ICE cotton futures | +12% |

| Lead-times (specialized yarn) | 8–12 weeks |

| Fuel share of maritime cost | 20–30% |

What is included in the product

Tailored exclusively for Hansae, this Porter's Five Forces analysis evaluates competitive rivalry, supplier and buyer power, threats of substitutes and new entrants, and identifies disruptive forces and strategic barriers shaping Hansae's pricing, profitability, and market position.

Hansae Porter's Five Forces condenses competitive pressure into a single, customizable one-sheet—instantly revealing supplier, buyer, entrant, substitute and rivalry risks to relieve strategic analysis pain points.

Customers Bargaining Power

Concentrated global brands

In 2024 large retailers and global sportswear brands accounted for the bulk of order volume, exercising strong negotiating leverage through competitive vendor bidding and relentless year-over-year cost downs. Hansae must win on price, quality and delivery to retain allocations as buyers shift contracts rapidly. Buyer consolidation among top global brands further amplifies this power and compresses supplier margins.

High switching options

Buyers can dual-source across multiple Asian and nearshore manufacturers, with over 50% of tier-1 brands reporting multi-country sourcing strategies in 2024, increasing order portability. Standardized specs and modular tech mean orders move quickly between factories. Vendor scorecards enable rapid reallocation of POs, keeping pricing and service under constant pressure.

Stringent compliance demands

Audits on labor, environment and product safety are non-negotiable and in 2024 buyer audits intensified, making non-compliance — fines, chargebacks or order loss — a clear driver of buyer leverage; fulfilling evolving standards raises Hansae’s unit costs without assured price relief, yet Hansae’s 2024 sustainability and compliance disclosures showing no critical audit failures partially offset customer bargaining power.

Lead-time and flexibility expectations

- Cycle time: 2–6 weeks (2024 industry norm)

- OTIF target: ~95% (2024)

- Chargebacks: 1–3% of invoice value

- Quick-response lowers lead-times and stockouts

ODM co-development dynamics

ODM co-development adds design value and deepens Hansae-brand ties, lowering direct price comparability and switching; a 2024 industry survey found 62% of apparel brands cite ODM partnerships as a primary speed-to-market lever. Buyers still retain leverage by appropriating designs or forcing IP terms, so Hansae's unique tech, quality and lead times determine bargaining shifts.

- ODM strengthens lock-in

- IP risk preserves buyer power

- Speed-to-market is decisive

Buyers lift pressure via multi-sourcing (>50%) and OTIF (~95%)

Buyers exert strong leverage via consolidation and multi-sourcing (>50% of tier-1 brands in 2024), forcing Hansae to compete on price, quality and OTIF (~95%). Chargebacks (1–3% of invoice) and intensified audits raise supplier costs; ODM co-development (62% of brands cite as speed lever) partially reduces pure price competition but IP risk maintains buyer power.

| Metric | 2024 |

|---|---|

| Multi-country sourcing | >50% |

| OTIF target | ~95% |

| Chargebacks | 1–3% invoice |

| ODM cited | 62% |

Same Document Delivered

Hansae Porter's Five Forces Analysis

This preview shows the exact Hansae Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted and ready for download and use the moment you buy. You're viewing the final deliverable.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Hansae's Porter's Five Forces snapshot highlights intense buyer power, supplier dynamics, competitive rivalry, and threats from substitutes and new entrants shaping its apparel sourcing business. Understanding these forces reveals where margins and strategic vulnerabilities lie—and where opportunities for differentiation exist. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Hansae’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Multi-sourcing raw materials

Raw material suppliers for cotton, synthetics, trims and dyes can gain leverage when supply tightens, with ICE cotton futures climbing about 12% in 2024 and polyester feedstock volatility similarly elevated. Hansae’s diversified vendor base across Asia, Africa and the Americas reduces single-supplier dependence and supports continuity. Long-term contracts and volume bundling secure price concessions, though commodity swings can still transmit cost shocks to margins.

Specialized fabric dependence

Dependence on a small set of capable mills for moisture-wicking and recycled performance fabrics increases switching costs and supplier leverage, particularly where bluesign or GRS certifications are required.

Co-development deals can secure price and capacity advantages but deepen dependency and raise exit barriers.

Specialized yarn lead-times of 8–12 weeks constrain quick response and amplify supplier bargaining power.

Compliance and ESG constraints

Restricted Substances Lists and growing traceability demands shrink the eligible supplier base; the ECHA candidate list reached 233 SVHCs in 2024, raising compliance scope. Fewer compliant mills strengthen supplier bargaining power as brands compete for certified capacity. Hansae’s stringent audits and onboarding further narrow options. Price premiums for certified inputs commonly compress margins for garmentmakers.

Logistics and energy exposure

Freight carriers and energy providers materially affect delivered cost and timelines; fuel commonly represents roughly 20–30% of maritime transport costs, so 2024 fuel volatility increased landed-cost exposure and schedule risk.

Port congestion and fuel spikes in 2024 amplified supplier leverage, while Hansae’s multi-country network enables route and mode switching to mitigate disruptions, though systemic shocks remain only partially offset.

- Supplier cost influence: fuel ≈20–30% of transport cost

- 2024 impact: higher fuel volatility → increased landed costs

- Mitigation: multi-country routing and modal flexibility

- Limit: systemic shocks cannot be fully hedged

Machinery and technology vendors

Sewing, cutting, dyeing and digital-printing equipment are sourced from a concentrated set of OEMs (Kornit, Lectra, Juki, Karl Mayer among leaders), where proprietary parts and software create strong lock-in and raise switching costs. Preventive maintenance contracts reduce downtime risk but increase fixed operating costs, while capital-intensive upgrades for automation and sustainability further strengthen vendor bargaining power.

- Concentrated OEM supply

- Proprietary parts/software = lock-in

- Maintenance contracts = lower downtime, higher fixed costs

- Automation/sustainability upgrades raise vendor leverage

ICE cotton futures +12%, 8–12 week lead times tighten supplier power

Suppliers of cotton, synthetics and trims gain leverage when supply tightens — ICE cotton futures +12% in 2024 — transmitting cost shocks despite Hansae’s diversified vendor base. Certified performance mills are limited, with 8–12 week lead times and OEM lock-in raising switching costs. Fuel (~20–30% of maritime cost) and port congestion amplify supplier power; multi-country routing mitigates but not eliminates risk.

| Metric | 2024 |

|---|---|

| ICE cotton futures | +12% |

| Lead-times (specialized yarn) | 8–12 weeks |

| Fuel share of maritime cost | 20–30% |

What is included in the product

Tailored exclusively for Hansae, this Porter's Five Forces analysis evaluates competitive rivalry, supplier and buyer power, threats of substitutes and new entrants, and identifies disruptive forces and strategic barriers shaping Hansae's pricing, profitability, and market position.

Hansae Porter's Five Forces condenses competitive pressure into a single, customizable one-sheet—instantly revealing supplier, buyer, entrant, substitute and rivalry risks to relieve strategic analysis pain points.

Customers Bargaining Power

Concentrated global brands

In 2024 large retailers and global sportswear brands accounted for the bulk of order volume, exercising strong negotiating leverage through competitive vendor bidding and relentless year-over-year cost downs. Hansae must win on price, quality and delivery to retain allocations as buyers shift contracts rapidly. Buyer consolidation among top global brands further amplifies this power and compresses supplier margins.

High switching options

Buyers can dual-source across multiple Asian and nearshore manufacturers, with over 50% of tier-1 brands reporting multi-country sourcing strategies in 2024, increasing order portability. Standardized specs and modular tech mean orders move quickly between factories. Vendor scorecards enable rapid reallocation of POs, keeping pricing and service under constant pressure.

Stringent compliance demands

Audits on labor, environment and product safety are non-negotiable and in 2024 buyer audits intensified, making non-compliance — fines, chargebacks or order loss — a clear driver of buyer leverage; fulfilling evolving standards raises Hansae’s unit costs without assured price relief, yet Hansae’s 2024 sustainability and compliance disclosures showing no critical audit failures partially offset customer bargaining power.

Lead-time and flexibility expectations

- Cycle time: 2–6 weeks (2024 industry norm)

- OTIF target: ~95% (2024)

- Chargebacks: 1–3% of invoice value

- Quick-response lowers lead-times and stockouts

ODM co-development dynamics

ODM co-development adds design value and deepens Hansae-brand ties, lowering direct price comparability and switching; a 2024 industry survey found 62% of apparel brands cite ODM partnerships as a primary speed-to-market lever. Buyers still retain leverage by appropriating designs or forcing IP terms, so Hansae's unique tech, quality and lead times determine bargaining shifts.

- ODM strengthens lock-in

- IP risk preserves buyer power

- Speed-to-market is decisive

Buyers lift pressure via multi-sourcing (>50%) and OTIF (~95%)

Buyers exert strong leverage via consolidation and multi-sourcing (>50% of tier-1 brands in 2024), forcing Hansae to compete on price, quality and OTIF (~95%). Chargebacks (1–3% of invoice) and intensified audits raise supplier costs; ODM co-development (62% of brands cite as speed lever) partially reduces pure price competition but IP risk maintains buyer power.

| Metric | 2024 |

|---|---|

| Multi-country sourcing | >50% |

| OTIF target | ~95% |

| Chargebacks | 1–3% invoice |

| ODM cited | 62% |

Same Document Delivered

Hansae Porter's Five Forces Analysis

This preview shows the exact Hansae Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted and ready for download and use the moment you buy. You're viewing the final deliverable.