Hansol Paper PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis of Hansol Paper—three to five sentence overview revealing how political, economic, social, technological, legal, and environmental forces shape its prospects. Perfect for investors, consultants, and managers seeking immediate market context. Buy the full, editable report to access deep-dive insights, risk scenarios, and actionable recommendations for confident decision-making.

Political factors

Korean industrial policy and subsidies

South Korea’s industrial policy — including the 2020 Green New Deal (≈KRW 73.4 trillion) and the national semiconductor push (≈KRW 510 trillion pledge) — can materially lower Hansol Paper’s capex for energy‑efficient mills via grants, tax breaks and concessional financing; shifts reallocating funds toward semiconductors may tighten eligibility for heavy‑industry subsidies, while alignment with decarbonization targets improves access to grants and low‑interest government loans, so monitoring ministry priorities and timing is crucial.

Trade policy, tariffs, and non-tariff barriers

Paper and pulp exporters like Hansol face antidumping suits and standards-based barriers in key markets, and past investigations have periodically disrupted shipments. South Korea’s FTAs, notably KORUS (effective 2012) and RCEP (effective 2022), can lower tariffs but add rules-of-origin complexity for qualifying inputs. Geopolitical frictions risk sudden quota or customs scrutiny. Diversifying markets and localizing converting capacity mitigate such shocks.

Geopolitical risk on the Korean peninsula

Geopolitical tension on the Korean peninsula—after about 90 North Korean missile tests in 2023—can disrupt Hansol Paper logistics, dent investor sentiment and lift insurance/transport costs; South Korea's defense budget rose to roughly KRW 61.7 trillion in 2024, underlining higher security premiums. Contingency plans for fuel, transport routes and workforce safety are necessary, while political stability elsewhere supports long-term capital deployment and supply chain redundancy reduces event risk.

Public procurement and sustainability mandates

Government procurement represents about 12% of GDP in OECD countries, prompting agencies to increasingly require eco-certified paper; FSC-certified forests covered ~224 million ha and PEFC ~338 million ha in 2023, expanding eligible supply. Meeting FSC/PEFC and recycled-content thresholds materially improves tender win rates, while EU CSRD phased-in from 2024 raises demand for transparent ESG reporting to qualify for public projects; non-compliance risks disqualification and reputational loss.

- Public procurement ~12% GDP (OECD)

- FSC ~224M ha, PEFC ~338M ha (2023)

- CSRD reporting phased from 2024 increases eligibility

- Non-compliance: disqualification and reputational damage

Energy and resource diplomacy

National strategies to secure LNG (South Korea imported about 43 million tonnes in 2023) and electricity generation policies directly affect Hansol Paper’s input availability and costs; cross-border renewable power cooperation can enable green PPAs and lower carbon electricity premiums. Diplomatic ties with pulp exporters such as Canada and Brazil influence supply reliability, while long-term offtake contracts (typically 10–20 years) hedge price volatility.

- LNG import scale: 43 Mt (2023)

- Pulp suppliers: Canada, Brazil — supply risk exposure

- Green PPA opportunity: cross-border renewables

- Hedge tool: 10–20 year offtake agreements

Green and chip policies cut green capex but heighten trade, energy and procurement risks

South Korea’s industrial pushes (Green New Deal ≈KRW 73.4T; semiconductor pledge ≈KRW 510T) can lower Hansol’s green-capex costs via subsidies but reallocation risks tighter heavy‑industry aid. Trade remedies and FTAs (KORUS, RCEP) create tariff relief yet rules‑of‑origin complexity and antidumping exposure. Rising defense spend (KRW 61.7T in 2024) and 43 Mt LNG imports (2023) raise logistics and energy costs; public procurement (~12% GDP) favors FSC/PEFC compliance.

| Factor | Metric | Impact |

|---|---|---|

| Industrial policy | KRW 73.4T / 510T | Capex relief vs eligibility risk |

| Trade & tariffs | KORUS/RCEP | Tariff cuts, origin complexity |

| Defense & energy | KRW 61.7T; 43Mt LNG | Higher premiums, input cost |

What is included in the product

Explores how macro-environmental factors uniquely affect Hansol Paper across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and industry-specific examples; designed for executives and investors, it offers forward-looking insights, scenario guidance, and ready-to-use formatting for reports and pitches.

A concise PESTLE summary of Hansol Paper for quick reference in meetings, visually segmented by category and written in simple language so teams can align on external risks and market positioning.

Economic factors

Global pulp price volatility

Pulp accounts for the largest single input cost for Hansol Paper, often representing over 40% of raw material costs; cyclical NBSK swings (about USD 700–1,200/ton in 2024) compress margins during spikes. Active hedging and supplier diversification reduce spot exposure. Passing costs depends on contract indexation and customer elasticity. Inventory timing materially affects quarterly earnings.

KRW exchange rate fluctuations

Imported pulp and energy make Hansol Paper highly FX-sensitive: USD/KRW averaged about 1,320 in 2024 and was near 1,350 mid-2025, so a weaker KRW raises input costs while export revenue in USD gains competitiveness. Financial hedges and natural offsets (USD sales vs USD inputs) have flattened cash-flow volatility historically. Contracts should include pricing clauses tied to FX indices such as USD/KRW or Bloomberg FX rates.

Demand shifts: print decline vs packaging growth

Digital media continues to erode printing and writing volumes, pressuring legacy grades as global demand for graphic paper falls; Hansol Paper offsets this by leaning into packaging where e-commerce — $5.7 trillion in global retail sales in 2022 — and food delivery boost demand for corrugates and barrier papers. Portfolio mix optimization sustains mill utilization and margins, while capex should prioritize high-growth substrates like coated kraft and barrier liners to capture rising packaging share.

Energy prices and power intensity

Paper production is energy-intensive, with energy often accounting for 20-30% of mill running costs; electricity and steam prices therefore drive Hansol Paper unit economics. Efficiency upgrades and cogeneration lower specific energy use and improve margins. Volatile LNG and coal markets (JKM swings 2023–24) complicate budgeting, while renewable PPAs lock predictable costs.

- Energy share: 20-30% of costs

- JKM volatility 2023–24: wide swings

- Cogeneration and PPAs reduce cost risk

Macroeconomic cycles and customer industries

- Macro linkage: orders ~GDP-correlated

- Destocking: intensified recent downturns

- Flexibility: cushions demand volatility

- Contracts: stabilize base volumes

Green and chip policies cut green capex but heighten trade, energy and procurement risks

Pulp is the largest input (>40% of raw-material costs) with NBSK ~USD 700–1,200/ton in 2024, compressing margins on spikes. FX sensitivity is high: USD/KRW ~1,320 average in 2024, ~1,350 mid-2025; hedges and USD revenues partially offset. Energy is 20–30% of running costs; cogeneration/PPAs lower volatility. Packaging demand offsets print decline as global GDP ~3.1% in 2024.

| Metric | Value |

|---|---|

| Pulp share | >40% |

| NBSK 2024 | USD 700–1,200/ton |

| USD/KRW | ~1,320 (2024 avg), ~1,350 (mid-2025) |

| Energy share | 20–30% |

| Global GDP 2024 | ~3.1% |

What You See Is What You Get

Hansol Paper PESTLE Analysis

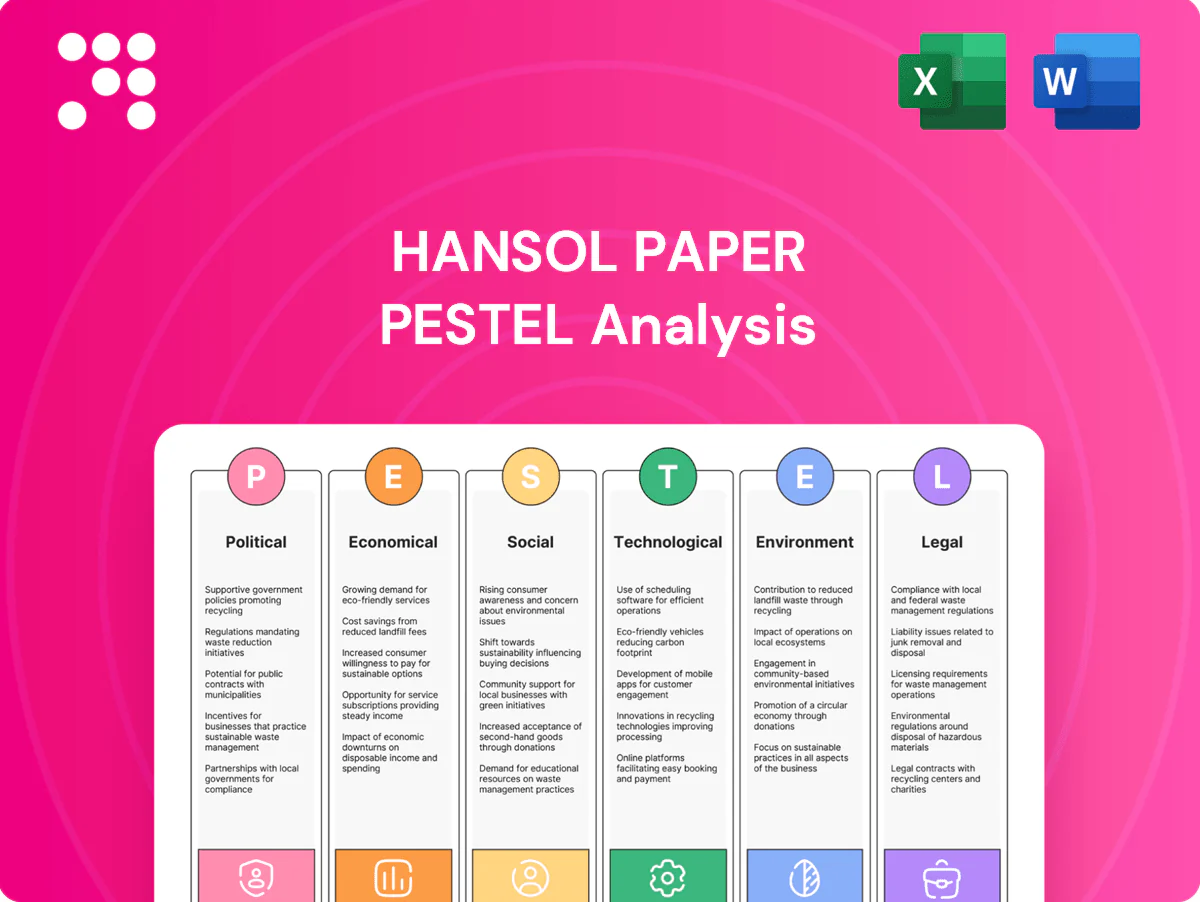

The Hansol Paper PESTLE Analysis provides a concise review of Political, Economic, Social, Technological, Legal and Environmental factors affecting the company and includes actionable insights for investors and strategists. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders, no surprises.

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis of Hansol Paper—three to five sentence overview revealing how political, economic, social, technological, legal, and environmental forces shape its prospects. Perfect for investors, consultants, and managers seeking immediate market context. Buy the full, editable report to access deep-dive insights, risk scenarios, and actionable recommendations for confident decision-making.

Political factors

Korean industrial policy and subsidies

South Korea’s industrial policy — including the 2020 Green New Deal (≈KRW 73.4 trillion) and the national semiconductor push (≈KRW 510 trillion pledge) — can materially lower Hansol Paper’s capex for energy‑efficient mills via grants, tax breaks and concessional financing; shifts reallocating funds toward semiconductors may tighten eligibility for heavy‑industry subsidies, while alignment with decarbonization targets improves access to grants and low‑interest government loans, so monitoring ministry priorities and timing is crucial.

Trade policy, tariffs, and non-tariff barriers

Paper and pulp exporters like Hansol face antidumping suits and standards-based barriers in key markets, and past investigations have periodically disrupted shipments. South Korea’s FTAs, notably KORUS (effective 2012) and RCEP (effective 2022), can lower tariffs but add rules-of-origin complexity for qualifying inputs. Geopolitical frictions risk sudden quota or customs scrutiny. Diversifying markets and localizing converting capacity mitigate such shocks.

Geopolitical risk on the Korean peninsula

Geopolitical tension on the Korean peninsula—after about 90 North Korean missile tests in 2023—can disrupt Hansol Paper logistics, dent investor sentiment and lift insurance/transport costs; South Korea's defense budget rose to roughly KRW 61.7 trillion in 2024, underlining higher security premiums. Contingency plans for fuel, transport routes and workforce safety are necessary, while political stability elsewhere supports long-term capital deployment and supply chain redundancy reduces event risk.

Public procurement and sustainability mandates

Government procurement represents about 12% of GDP in OECD countries, prompting agencies to increasingly require eco-certified paper; FSC-certified forests covered ~224 million ha and PEFC ~338 million ha in 2023, expanding eligible supply. Meeting FSC/PEFC and recycled-content thresholds materially improves tender win rates, while EU CSRD phased-in from 2024 raises demand for transparent ESG reporting to qualify for public projects; non-compliance risks disqualification and reputational loss.

- Public procurement ~12% GDP (OECD)

- FSC ~224M ha, PEFC ~338M ha (2023)

- CSRD reporting phased from 2024 increases eligibility

- Non-compliance: disqualification and reputational damage

Energy and resource diplomacy

National strategies to secure LNG (South Korea imported about 43 million tonnes in 2023) and electricity generation policies directly affect Hansol Paper’s input availability and costs; cross-border renewable power cooperation can enable green PPAs and lower carbon electricity premiums. Diplomatic ties with pulp exporters such as Canada and Brazil influence supply reliability, while long-term offtake contracts (typically 10–20 years) hedge price volatility.

- LNG import scale: 43 Mt (2023)

- Pulp suppliers: Canada, Brazil — supply risk exposure

- Green PPA opportunity: cross-border renewables

- Hedge tool: 10–20 year offtake agreements

Green and chip policies cut green capex but heighten trade, energy and procurement risks

South Korea’s industrial pushes (Green New Deal ≈KRW 73.4T; semiconductor pledge ≈KRW 510T) can lower Hansol’s green-capex costs via subsidies but reallocation risks tighter heavy‑industry aid. Trade remedies and FTAs (KORUS, RCEP) create tariff relief yet rules‑of‑origin complexity and antidumping exposure. Rising defense spend (KRW 61.7T in 2024) and 43 Mt LNG imports (2023) raise logistics and energy costs; public procurement (~12% GDP) favors FSC/PEFC compliance.

| Factor | Metric | Impact |

|---|---|---|

| Industrial policy | KRW 73.4T / 510T | Capex relief vs eligibility risk |

| Trade & tariffs | KORUS/RCEP | Tariff cuts, origin complexity |

| Defense & energy | KRW 61.7T; 43Mt LNG | Higher premiums, input cost |

What is included in the product

Explores how macro-environmental factors uniquely affect Hansol Paper across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and industry-specific examples; designed for executives and investors, it offers forward-looking insights, scenario guidance, and ready-to-use formatting for reports and pitches.

A concise PESTLE summary of Hansol Paper for quick reference in meetings, visually segmented by category and written in simple language so teams can align on external risks and market positioning.

Economic factors

Global pulp price volatility

Pulp accounts for the largest single input cost for Hansol Paper, often representing over 40% of raw material costs; cyclical NBSK swings (about USD 700–1,200/ton in 2024) compress margins during spikes. Active hedging and supplier diversification reduce spot exposure. Passing costs depends on contract indexation and customer elasticity. Inventory timing materially affects quarterly earnings.

KRW exchange rate fluctuations

Imported pulp and energy make Hansol Paper highly FX-sensitive: USD/KRW averaged about 1,320 in 2024 and was near 1,350 mid-2025, so a weaker KRW raises input costs while export revenue in USD gains competitiveness. Financial hedges and natural offsets (USD sales vs USD inputs) have flattened cash-flow volatility historically. Contracts should include pricing clauses tied to FX indices such as USD/KRW or Bloomberg FX rates.

Demand shifts: print decline vs packaging growth

Digital media continues to erode printing and writing volumes, pressuring legacy grades as global demand for graphic paper falls; Hansol Paper offsets this by leaning into packaging where e-commerce — $5.7 trillion in global retail sales in 2022 — and food delivery boost demand for corrugates and barrier papers. Portfolio mix optimization sustains mill utilization and margins, while capex should prioritize high-growth substrates like coated kraft and barrier liners to capture rising packaging share.

Energy prices and power intensity

Paper production is energy-intensive, with energy often accounting for 20-30% of mill running costs; electricity and steam prices therefore drive Hansol Paper unit economics. Efficiency upgrades and cogeneration lower specific energy use and improve margins. Volatile LNG and coal markets (JKM swings 2023–24) complicate budgeting, while renewable PPAs lock predictable costs.

- Energy share: 20-30% of costs

- JKM volatility 2023–24: wide swings

- Cogeneration and PPAs reduce cost risk

Macroeconomic cycles and customer industries

- Macro linkage: orders ~GDP-correlated

- Destocking: intensified recent downturns

- Flexibility: cushions demand volatility

- Contracts: stabilize base volumes

Green and chip policies cut green capex but heighten trade, energy and procurement risks

Pulp is the largest input (>40% of raw-material costs) with NBSK ~USD 700–1,200/ton in 2024, compressing margins on spikes. FX sensitivity is high: USD/KRW ~1,320 average in 2024, ~1,350 mid-2025; hedges and USD revenues partially offset. Energy is 20–30% of running costs; cogeneration/PPAs lower volatility. Packaging demand offsets print decline as global GDP ~3.1% in 2024.

| Metric | Value |

|---|---|

| Pulp share | >40% |

| NBSK 2024 | USD 700–1,200/ton |

| USD/KRW | ~1,320 (2024 avg), ~1,350 (mid-2025) |

| Energy share | 20–30% |

| Global GDP 2024 | ~3.1% |

What You See Is What You Get

Hansol Paper PESTLE Analysis

The Hansol Paper PESTLE Analysis provides a concise review of Political, Economic, Social, Technological, Legal and Environmental factors affecting the company and includes actionable insights for investors and strategists. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders, no surprises.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis of Hansol Paper—three to five sentence overview revealing how political, economic, social, technological, legal, and environmental forces shape its prospects. Perfect for investors, consultants, and managers seeking immediate market context. Buy the full, editable report to access deep-dive insights, risk scenarios, and actionable recommendations for confident decision-making.

Political factors

Korean industrial policy and subsidies

South Korea’s industrial policy — including the 2020 Green New Deal (≈KRW 73.4 trillion) and the national semiconductor push (≈KRW 510 trillion pledge) — can materially lower Hansol Paper’s capex for energy‑efficient mills via grants, tax breaks and concessional financing; shifts reallocating funds toward semiconductors may tighten eligibility for heavy‑industry subsidies, while alignment with decarbonization targets improves access to grants and low‑interest government loans, so monitoring ministry priorities and timing is crucial.

Trade policy, tariffs, and non-tariff barriers

Paper and pulp exporters like Hansol face antidumping suits and standards-based barriers in key markets, and past investigations have periodically disrupted shipments. South Korea’s FTAs, notably KORUS (effective 2012) and RCEP (effective 2022), can lower tariffs but add rules-of-origin complexity for qualifying inputs. Geopolitical frictions risk sudden quota or customs scrutiny. Diversifying markets and localizing converting capacity mitigate such shocks.

Geopolitical risk on the Korean peninsula

Geopolitical tension on the Korean peninsula—after about 90 North Korean missile tests in 2023—can disrupt Hansol Paper logistics, dent investor sentiment and lift insurance/transport costs; South Korea's defense budget rose to roughly KRW 61.7 trillion in 2024, underlining higher security premiums. Contingency plans for fuel, transport routes and workforce safety are necessary, while political stability elsewhere supports long-term capital deployment and supply chain redundancy reduces event risk.

Public procurement and sustainability mandates

Government procurement represents about 12% of GDP in OECD countries, prompting agencies to increasingly require eco-certified paper; FSC-certified forests covered ~224 million ha and PEFC ~338 million ha in 2023, expanding eligible supply. Meeting FSC/PEFC and recycled-content thresholds materially improves tender win rates, while EU CSRD phased-in from 2024 raises demand for transparent ESG reporting to qualify for public projects; non-compliance risks disqualification and reputational loss.

- Public procurement ~12% GDP (OECD)

- FSC ~224M ha, PEFC ~338M ha (2023)

- CSRD reporting phased from 2024 increases eligibility

- Non-compliance: disqualification and reputational damage

Energy and resource diplomacy

National strategies to secure LNG (South Korea imported about 43 million tonnes in 2023) and electricity generation policies directly affect Hansol Paper’s input availability and costs; cross-border renewable power cooperation can enable green PPAs and lower carbon electricity premiums. Diplomatic ties with pulp exporters such as Canada and Brazil influence supply reliability, while long-term offtake contracts (typically 10–20 years) hedge price volatility.

- LNG import scale: 43 Mt (2023)

- Pulp suppliers: Canada, Brazil — supply risk exposure

- Green PPA opportunity: cross-border renewables

- Hedge tool: 10–20 year offtake agreements

Green and chip policies cut green capex but heighten trade, energy and procurement risks

South Korea’s industrial pushes (Green New Deal ≈KRW 73.4T; semiconductor pledge ≈KRW 510T) can lower Hansol’s green-capex costs via subsidies but reallocation risks tighter heavy‑industry aid. Trade remedies and FTAs (KORUS, RCEP) create tariff relief yet rules‑of‑origin complexity and antidumping exposure. Rising defense spend (KRW 61.7T in 2024) and 43 Mt LNG imports (2023) raise logistics and energy costs; public procurement (~12% GDP) favors FSC/PEFC compliance.

| Factor | Metric | Impact |

|---|---|---|

| Industrial policy | KRW 73.4T / 510T | Capex relief vs eligibility risk |

| Trade & tariffs | KORUS/RCEP | Tariff cuts, origin complexity |

| Defense & energy | KRW 61.7T; 43Mt LNG | Higher premiums, input cost |

What is included in the product

Explores how macro-environmental factors uniquely affect Hansol Paper across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and industry-specific examples; designed for executives and investors, it offers forward-looking insights, scenario guidance, and ready-to-use formatting for reports and pitches.

A concise PESTLE summary of Hansol Paper for quick reference in meetings, visually segmented by category and written in simple language so teams can align on external risks and market positioning.

Economic factors

Global pulp price volatility

Pulp accounts for the largest single input cost for Hansol Paper, often representing over 40% of raw material costs; cyclical NBSK swings (about USD 700–1,200/ton in 2024) compress margins during spikes. Active hedging and supplier diversification reduce spot exposure. Passing costs depends on contract indexation and customer elasticity. Inventory timing materially affects quarterly earnings.

KRW exchange rate fluctuations

Imported pulp and energy make Hansol Paper highly FX-sensitive: USD/KRW averaged about 1,320 in 2024 and was near 1,350 mid-2025, so a weaker KRW raises input costs while export revenue in USD gains competitiveness. Financial hedges and natural offsets (USD sales vs USD inputs) have flattened cash-flow volatility historically. Contracts should include pricing clauses tied to FX indices such as USD/KRW or Bloomberg FX rates.

Demand shifts: print decline vs packaging growth

Digital media continues to erode printing and writing volumes, pressuring legacy grades as global demand for graphic paper falls; Hansol Paper offsets this by leaning into packaging where e-commerce — $5.7 trillion in global retail sales in 2022 — and food delivery boost demand for corrugates and barrier papers. Portfolio mix optimization sustains mill utilization and margins, while capex should prioritize high-growth substrates like coated kraft and barrier liners to capture rising packaging share.

Energy prices and power intensity

Paper production is energy-intensive, with energy often accounting for 20-30% of mill running costs; electricity and steam prices therefore drive Hansol Paper unit economics. Efficiency upgrades and cogeneration lower specific energy use and improve margins. Volatile LNG and coal markets (JKM swings 2023–24) complicate budgeting, while renewable PPAs lock predictable costs.

- Energy share: 20-30% of costs

- JKM volatility 2023–24: wide swings

- Cogeneration and PPAs reduce cost risk

Macroeconomic cycles and customer industries

- Macro linkage: orders ~GDP-correlated

- Destocking: intensified recent downturns

- Flexibility: cushions demand volatility

- Contracts: stabilize base volumes

Green and chip policies cut green capex but heighten trade, energy and procurement risks

Pulp is the largest input (>40% of raw-material costs) with NBSK ~USD 700–1,200/ton in 2024, compressing margins on spikes. FX sensitivity is high: USD/KRW ~1,320 average in 2024, ~1,350 mid-2025; hedges and USD revenues partially offset. Energy is 20–30% of running costs; cogeneration/PPAs lower volatility. Packaging demand offsets print decline as global GDP ~3.1% in 2024.

| Metric | Value |

|---|---|

| Pulp share | >40% |

| NBSK 2024 | USD 700–1,200/ton |

| USD/KRW | ~1,320 (2024 avg), ~1,350 (mid-2025) |

| Energy share | 20–30% |

| Global GDP 2024 | ~3.1% |

What You See Is What You Get

Hansol Paper PESTLE Analysis

The Hansol Paper PESTLE Analysis provides a concise review of Political, Economic, Social, Technological, Legal and Environmental factors affecting the company and includes actionable insights for investors and strategists. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders, no surprises.