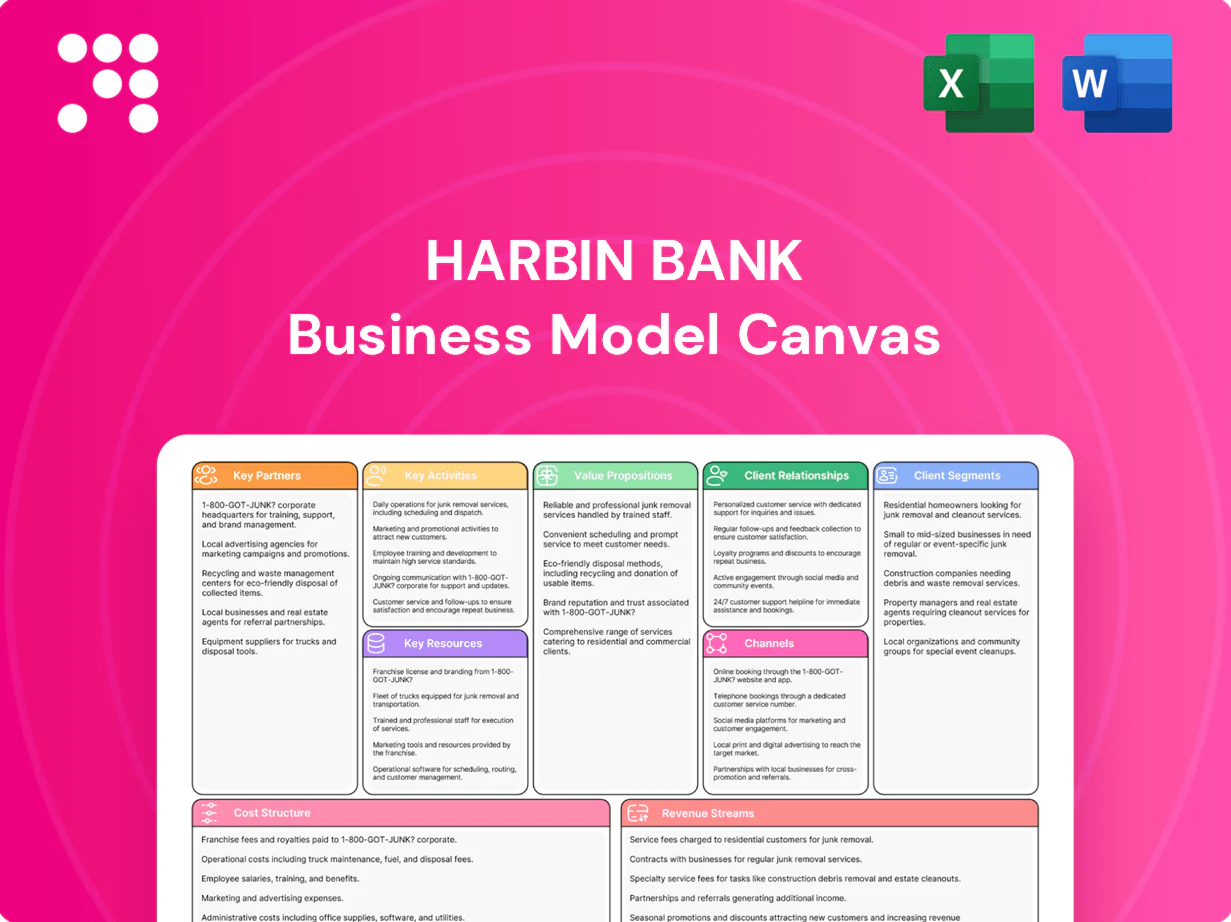

Harbin Bank Business Model Canvas

Business Model Canvas for a regional bank: customers, value, revenue & partners

Unlock Harbin Bank’s strategic playbook with a concise Business Model Canvas that maps customer segments, core value propositions, revenue streams and partnerships. This snapshot shows how the bank scales, manages risk and competes regionally. Purchase the full, editable Canvas (Word & Excel) for a complete, actionable breakdown you can use for benchmarking or investor-ready presentations.

Partnerships

Regulatory bodies

Partnerships with the People’s Bank of China and the China Banking and Insurance Regulatory Commission ensure Harbin Bank compliance and access to CNAPS payment and clearing systems, coordination on prudential rules for risk management and capital adequacy, and participation in interbank markets and policy programs such as targeted relending; China’s foreign exchange reserves stood near 3.2 trillion USD in 2024, underpinning macro stability.

Interbank counterparts

Treasury, repo, and FX partnerships provide Harbin Bank's Financial Market Business with essential liquidity and pricing depth. Counterparties facilitate syndications, risk transfers, and market-making to support market access and execution. Collaborative arrangements help manage interest rate and funding risks, and in 2024 China’s FX reserves remained near 3.2 trillion USD, underpinning interbank FX liquidity.

Fintech and payment firms

Alliances with fintechs enhance Harbin Bank's digital onboarding, payments, and credit analytics, leveraging partners that drive faster KYC and risk scoring; in China Alipay and WeChat Pay together exceed 90% of mobile payment market share (2024). API integrations expand service reach and improve customer experience across channels. Co-developed products accelerate innovation and lower time-to-market. Such partnerships bolster retail and SME propositions.

Corporate and SME ecosystems

Tie-ups with industrial parks, supply chains and chambers of commerce create steady corporate lending pipelines; ecosystem data from partners improves underwriting precision and product fit. Embedded finance arrangements deepen client stickiness, enabling cross-sell into deposits, cash management and trade finance. In 2024 Chinese SMEs account for roughly 60% of GDP and about 80% of urban employment.

- Pipeline sourcing via parks and chambers

- Ecosystem data → better underwriting

- Embedded finance increases retention

- Drives cross-sell: deposits, cash mgmt, trade finance

Technology and data vendors

Technology and data vendors supply Harbin Bank with core banking, cybersecurity, cloud platforms and risk models, enabling omnichannel scalability with typical uptime SLAs of 99.95% and vendor-driven modernization that can cut build costs by up to 40% and speed time-to-market by ~30% (2024 industry benchmarks). Data providers strengthen KYC/AML screening and credit scoring, improving detection and PD model accuracy by double-digit percentages in 2024 pilots.

- core: core banking, cloud, cybersecurity, risk models

- impact: 99.95% uptime, −40% build costs, −30% time-to-market

- data: stronger KYC/AML, double-digit PD accuracy gains (2024)

Partners power compliance, liquidity & digital; FX 3.2T, mobile >90%

Harbin Bank's partners—regulators, interbank counterparties, fintechs, industrial parks and tech vendors—deliver compliance, liquidity, digital distribution, underwriting data and infrastructure. 2024 metrics: PBOC/CIBRC access, ~3.2 trillion USD FX reserves, Alipay+WeChat >90% mobile share, SMEs ~60% GDP. Vendor partnerships cut build costs ~40% and improved PD accuracy by double digits in pilots.

| Partner | Role | 2024 metric |

|---|---|---|

| Regulators | Clearing, prudential | CNAPS; FX reserves ~3.2T USD |

| Fintechs | Digital onboarding | Alipay+WeChat >90% mobile |

| Parks/SMEs | Loan pipeline | SMEs ~60% GDP |

| Vendors | Core tech, risk | -40% costs; +DD PD accuracy |

What is included in the product

Comprehensive Business Model Canvas for Harbin Bank outlining nine blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, activities, partners, and cost structure—reflecting real-world operations, competitive advantages, and linked SWOT insights; ideal for presentations, investor pitches, and strategic decision-making by entrepreneurs and analysts.

High-level view of Harbin Bank’s business model with editable cells that relieves strategic uncertainty and operational pain points. Clean, shareable one-page snapshot saves hours of formatting and enables fast team alignment and comparison across scenarios.

Activities

Deposit mobilization

Deposit mobilization at Harbin Bank focuses on attracting and retaining low-cost deposits to underpin balance sheet funding, with campaigns tailored to retail, SME and corporate treasury segments. Product design covers current, time and structured deposits, while dynamic pricing and proactive relationship management optimize the bank’s cost of funds and liquidity profile.

Credit underwriting

Originating and assessing loans to corporates, SMEs and consumers is central to Harbin Bank’s credit underwriting, with 2024 policies emphasizing sectoral limits and documented credit-scoring models. Risk models, collateral assessment and policy rules guide approvals and downgrade triggers. Portfolio monitoring tracks sector concentrations and early-warning indicators to contain losses. Pricing is set to meet risk-adjusted return targets and internal hurdle rates.

Treasury operations

Treasury operations manage liquidity, ALM and investments to stabilize earnings, with Harbin Bank's treasury overseeing interbank lending, a bond portfolio and hedging positions; in 2024 the bank reported total assets of RMB 1.02 trillion and a treasury-held bond portfolio exceeding RMB 120 billion. Interest rate and FX risks are matched within Board-set ALM limits and regulatory caps. Treasury also informs product pricing and optimizes capital efficiency to support ROE targets.

Transaction banking

- 2024 fee income +7% YoY

- Focus: cash mgmt, collections, payroll, trade finance

- ERP integration for straight-through processing

- Operational controls to cut errors and losses

Digital delivery

Developing and maintaining mobile, online, and API channels expands Harbin Bank’s reach and supports digital account growth as China’s mobile payment ecosystem exceeded 1.06 billion users in 2024; UX optimization boosts adoption and self-service, cutting branch traffic and operating costs. Data analytics enable personalized offers to reduce churn and increase cross-sell; robust cybersecurity investments preserve trust and regulatory compliance.

- Channels: mobile, online, API

- UX: higher adoption, lower costs

- Data: personalization, churn reduction

- Security: trust, compliance

Low-cost deposits, sector-limited loans, treasury RMB 1.02T, fees +7% YoY

Deposit mobilization targeting low-cost retail/SME/corporate; loans origination with sector limits and credit scoring; treasury ALM and bond portfolio (assets RMB 1.02 trillion; bonds >RMB 120bn); transaction banking and digital channels driving fee income +7% YoY and leveraging China’s 1.06bn mobile payment users (2024).

| Metric | 2024 |

|---|---|

| Total assets | RMB 1.02 trillion |

| Treasury bonds | >RMB 120 billion |

| Fee income growth | +7% YoY |

| Mobile payment users (China) | 1.06 billion |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Harbin Bank Business Model Canvas, not a mockup or sample. When you purchase, you'll receive this exact file—complete, fully editable and formatted—ready for presentation and analysis. No placeholders or surprises: the preview matches the deliverable you'll download.

Business Model Canvas for a regional bank: customers, value, revenue & partners

Unlock Harbin Bank’s strategic playbook with a concise Business Model Canvas that maps customer segments, core value propositions, revenue streams and partnerships. This snapshot shows how the bank scales, manages risk and competes regionally. Purchase the full, editable Canvas (Word & Excel) for a complete, actionable breakdown you can use for benchmarking or investor-ready presentations.

Partnerships

Regulatory bodies

Partnerships with the People’s Bank of China and the China Banking and Insurance Regulatory Commission ensure Harbin Bank compliance and access to CNAPS payment and clearing systems, coordination on prudential rules for risk management and capital adequacy, and participation in interbank markets and policy programs such as targeted relending; China’s foreign exchange reserves stood near 3.2 trillion USD in 2024, underpinning macro stability.

Interbank counterparts

Treasury, repo, and FX partnerships provide Harbin Bank's Financial Market Business with essential liquidity and pricing depth. Counterparties facilitate syndications, risk transfers, and market-making to support market access and execution. Collaborative arrangements help manage interest rate and funding risks, and in 2024 China’s FX reserves remained near 3.2 trillion USD, underpinning interbank FX liquidity.

Fintech and payment firms

Alliances with fintechs enhance Harbin Bank's digital onboarding, payments, and credit analytics, leveraging partners that drive faster KYC and risk scoring; in China Alipay and WeChat Pay together exceed 90% of mobile payment market share (2024). API integrations expand service reach and improve customer experience across channels. Co-developed products accelerate innovation and lower time-to-market. Such partnerships bolster retail and SME propositions.

Corporate and SME ecosystems

Tie-ups with industrial parks, supply chains and chambers of commerce create steady corporate lending pipelines; ecosystem data from partners improves underwriting precision and product fit. Embedded finance arrangements deepen client stickiness, enabling cross-sell into deposits, cash management and trade finance. In 2024 Chinese SMEs account for roughly 60% of GDP and about 80% of urban employment.

- Pipeline sourcing via parks and chambers

- Ecosystem data → better underwriting

- Embedded finance increases retention

- Drives cross-sell: deposits, cash mgmt, trade finance

Technology and data vendors

Technology and data vendors supply Harbin Bank with core banking, cybersecurity, cloud platforms and risk models, enabling omnichannel scalability with typical uptime SLAs of 99.95% and vendor-driven modernization that can cut build costs by up to 40% and speed time-to-market by ~30% (2024 industry benchmarks). Data providers strengthen KYC/AML screening and credit scoring, improving detection and PD model accuracy by double-digit percentages in 2024 pilots.

- core: core banking, cloud, cybersecurity, risk models

- impact: 99.95% uptime, −40% build costs, −30% time-to-market

- data: stronger KYC/AML, double-digit PD accuracy gains (2024)

Partners power compliance, liquidity & digital; FX 3.2T, mobile >90%

Harbin Bank's partners—regulators, interbank counterparties, fintechs, industrial parks and tech vendors—deliver compliance, liquidity, digital distribution, underwriting data and infrastructure. 2024 metrics: PBOC/CIBRC access, ~3.2 trillion USD FX reserves, Alipay+WeChat >90% mobile share, SMEs ~60% GDP. Vendor partnerships cut build costs ~40% and improved PD accuracy by double digits in pilots.

| Partner | Role | 2024 metric |

|---|---|---|

| Regulators | Clearing, prudential | CNAPS; FX reserves ~3.2T USD |

| Fintechs | Digital onboarding | Alipay+WeChat >90% mobile |

| Parks/SMEs | Loan pipeline | SMEs ~60% GDP |

| Vendors | Core tech, risk | -40% costs; +DD PD accuracy |

What is included in the product

Comprehensive Business Model Canvas for Harbin Bank outlining nine blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, activities, partners, and cost structure—reflecting real-world operations, competitive advantages, and linked SWOT insights; ideal for presentations, investor pitches, and strategic decision-making by entrepreneurs and analysts.

High-level view of Harbin Bank’s business model with editable cells that relieves strategic uncertainty and operational pain points. Clean, shareable one-page snapshot saves hours of formatting and enables fast team alignment and comparison across scenarios.

Activities

Deposit mobilization

Deposit mobilization at Harbin Bank focuses on attracting and retaining low-cost deposits to underpin balance sheet funding, with campaigns tailored to retail, SME and corporate treasury segments. Product design covers current, time and structured deposits, while dynamic pricing and proactive relationship management optimize the bank’s cost of funds and liquidity profile.

Credit underwriting

Originating and assessing loans to corporates, SMEs and consumers is central to Harbin Bank’s credit underwriting, with 2024 policies emphasizing sectoral limits and documented credit-scoring models. Risk models, collateral assessment and policy rules guide approvals and downgrade triggers. Portfolio monitoring tracks sector concentrations and early-warning indicators to contain losses. Pricing is set to meet risk-adjusted return targets and internal hurdle rates.

Treasury operations

Treasury operations manage liquidity, ALM and investments to stabilize earnings, with Harbin Bank's treasury overseeing interbank lending, a bond portfolio and hedging positions; in 2024 the bank reported total assets of RMB 1.02 trillion and a treasury-held bond portfolio exceeding RMB 120 billion. Interest rate and FX risks are matched within Board-set ALM limits and regulatory caps. Treasury also informs product pricing and optimizes capital efficiency to support ROE targets.

Transaction banking

- 2024 fee income +7% YoY

- Focus: cash mgmt, collections, payroll, trade finance

- ERP integration for straight-through processing

- Operational controls to cut errors and losses

Digital delivery

Developing and maintaining mobile, online, and API channels expands Harbin Bank’s reach and supports digital account growth as China’s mobile payment ecosystem exceeded 1.06 billion users in 2024; UX optimization boosts adoption and self-service, cutting branch traffic and operating costs. Data analytics enable personalized offers to reduce churn and increase cross-sell; robust cybersecurity investments preserve trust and regulatory compliance.

- Channels: mobile, online, API

- UX: higher adoption, lower costs

- Data: personalization, churn reduction

- Security: trust, compliance

Low-cost deposits, sector-limited loans, treasury RMB 1.02T, fees +7% YoY

Deposit mobilization targeting low-cost retail/SME/corporate; loans origination with sector limits and credit scoring; treasury ALM and bond portfolio (assets RMB 1.02 trillion; bonds >RMB 120bn); transaction banking and digital channels driving fee income +7% YoY and leveraging China’s 1.06bn mobile payment users (2024).

| Metric | 2024 |

|---|---|

| Total assets | RMB 1.02 trillion |

| Treasury bonds | >RMB 120 billion |

| Fee income growth | +7% YoY |

| Mobile payment users (China) | 1.06 billion |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Harbin Bank Business Model Canvas, not a mockup or sample. When you purchase, you'll receive this exact file—complete, fully editable and formatted—ready for presentation and analysis. No placeholders or surprises: the preview matches the deliverable you'll download.

Original: $10.00

-65%$10.00

$3.50Description

Business Model Canvas for a regional bank: customers, value, revenue & partners

Unlock Harbin Bank’s strategic playbook with a concise Business Model Canvas that maps customer segments, core value propositions, revenue streams and partnerships. This snapshot shows how the bank scales, manages risk and competes regionally. Purchase the full, editable Canvas (Word & Excel) for a complete, actionable breakdown you can use for benchmarking or investor-ready presentations.

Partnerships

Regulatory bodies

Partnerships with the People’s Bank of China and the China Banking and Insurance Regulatory Commission ensure Harbin Bank compliance and access to CNAPS payment and clearing systems, coordination on prudential rules for risk management and capital adequacy, and participation in interbank markets and policy programs such as targeted relending; China’s foreign exchange reserves stood near 3.2 trillion USD in 2024, underpinning macro stability.

Interbank counterparts

Treasury, repo, and FX partnerships provide Harbin Bank's Financial Market Business with essential liquidity and pricing depth. Counterparties facilitate syndications, risk transfers, and market-making to support market access and execution. Collaborative arrangements help manage interest rate and funding risks, and in 2024 China’s FX reserves remained near 3.2 trillion USD, underpinning interbank FX liquidity.

Fintech and payment firms

Alliances with fintechs enhance Harbin Bank's digital onboarding, payments, and credit analytics, leveraging partners that drive faster KYC and risk scoring; in China Alipay and WeChat Pay together exceed 90% of mobile payment market share (2024). API integrations expand service reach and improve customer experience across channels. Co-developed products accelerate innovation and lower time-to-market. Such partnerships bolster retail and SME propositions.

Corporate and SME ecosystems

Tie-ups with industrial parks, supply chains and chambers of commerce create steady corporate lending pipelines; ecosystem data from partners improves underwriting precision and product fit. Embedded finance arrangements deepen client stickiness, enabling cross-sell into deposits, cash management and trade finance. In 2024 Chinese SMEs account for roughly 60% of GDP and about 80% of urban employment.

- Pipeline sourcing via parks and chambers

- Ecosystem data → better underwriting

- Embedded finance increases retention

- Drives cross-sell: deposits, cash mgmt, trade finance

Technology and data vendors

Technology and data vendors supply Harbin Bank with core banking, cybersecurity, cloud platforms and risk models, enabling omnichannel scalability with typical uptime SLAs of 99.95% and vendor-driven modernization that can cut build costs by up to 40% and speed time-to-market by ~30% (2024 industry benchmarks). Data providers strengthen KYC/AML screening and credit scoring, improving detection and PD model accuracy by double-digit percentages in 2024 pilots.

- core: core banking, cloud, cybersecurity, risk models

- impact: 99.95% uptime, −40% build costs, −30% time-to-market

- data: stronger KYC/AML, double-digit PD accuracy gains (2024)

Partners power compliance, liquidity & digital; FX 3.2T, mobile >90%

Harbin Bank's partners—regulators, interbank counterparties, fintechs, industrial parks and tech vendors—deliver compliance, liquidity, digital distribution, underwriting data and infrastructure. 2024 metrics: PBOC/CIBRC access, ~3.2 trillion USD FX reserves, Alipay+WeChat >90% mobile share, SMEs ~60% GDP. Vendor partnerships cut build costs ~40% and improved PD accuracy by double digits in pilots.

| Partner | Role | 2024 metric |

|---|---|---|

| Regulators | Clearing, prudential | CNAPS; FX reserves ~3.2T USD |

| Fintechs | Digital onboarding | Alipay+WeChat >90% mobile |

| Parks/SMEs | Loan pipeline | SMEs ~60% GDP |

| Vendors | Core tech, risk | -40% costs; +DD PD accuracy |

What is included in the product

Comprehensive Business Model Canvas for Harbin Bank outlining nine blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, activities, partners, and cost structure—reflecting real-world operations, competitive advantages, and linked SWOT insights; ideal for presentations, investor pitches, and strategic decision-making by entrepreneurs and analysts.

High-level view of Harbin Bank’s business model with editable cells that relieves strategic uncertainty and operational pain points. Clean, shareable one-page snapshot saves hours of formatting and enables fast team alignment and comparison across scenarios.

Activities

Deposit mobilization

Deposit mobilization at Harbin Bank focuses on attracting and retaining low-cost deposits to underpin balance sheet funding, with campaigns tailored to retail, SME and corporate treasury segments. Product design covers current, time and structured deposits, while dynamic pricing and proactive relationship management optimize the bank’s cost of funds and liquidity profile.

Credit underwriting

Originating and assessing loans to corporates, SMEs and consumers is central to Harbin Bank’s credit underwriting, with 2024 policies emphasizing sectoral limits and documented credit-scoring models. Risk models, collateral assessment and policy rules guide approvals and downgrade triggers. Portfolio monitoring tracks sector concentrations and early-warning indicators to contain losses. Pricing is set to meet risk-adjusted return targets and internal hurdle rates.

Treasury operations

Treasury operations manage liquidity, ALM and investments to stabilize earnings, with Harbin Bank's treasury overseeing interbank lending, a bond portfolio and hedging positions; in 2024 the bank reported total assets of RMB 1.02 trillion and a treasury-held bond portfolio exceeding RMB 120 billion. Interest rate and FX risks are matched within Board-set ALM limits and regulatory caps. Treasury also informs product pricing and optimizes capital efficiency to support ROE targets.

Transaction banking

- 2024 fee income +7% YoY

- Focus: cash mgmt, collections, payroll, trade finance

- ERP integration for straight-through processing

- Operational controls to cut errors and losses

Digital delivery

Developing and maintaining mobile, online, and API channels expands Harbin Bank’s reach and supports digital account growth as China’s mobile payment ecosystem exceeded 1.06 billion users in 2024; UX optimization boosts adoption and self-service, cutting branch traffic and operating costs. Data analytics enable personalized offers to reduce churn and increase cross-sell; robust cybersecurity investments preserve trust and regulatory compliance.

- Channels: mobile, online, API

- UX: higher adoption, lower costs

- Data: personalization, churn reduction

- Security: trust, compliance

Low-cost deposits, sector-limited loans, treasury RMB 1.02T, fees +7% YoY

Deposit mobilization targeting low-cost retail/SME/corporate; loans origination with sector limits and credit scoring; treasury ALM and bond portfolio (assets RMB 1.02 trillion; bonds >RMB 120bn); transaction banking and digital channels driving fee income +7% YoY and leveraging China’s 1.06bn mobile payment users (2024).

| Metric | 2024 |

|---|---|

| Total assets | RMB 1.02 trillion |

| Treasury bonds | >RMB 120 billion |

| Fee income growth | +7% YoY |

| Mobile payment users (China) | 1.06 billion |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Harbin Bank Business Model Canvas, not a mockup or sample. When you purchase, you'll receive this exact file—complete, fully editable and formatted—ready for presentation and analysis. No placeholders or surprises: the preview matches the deliverable you'll download.