Haulotte Group PESTLE Analysis

Skip the Research. Get the Strategy.

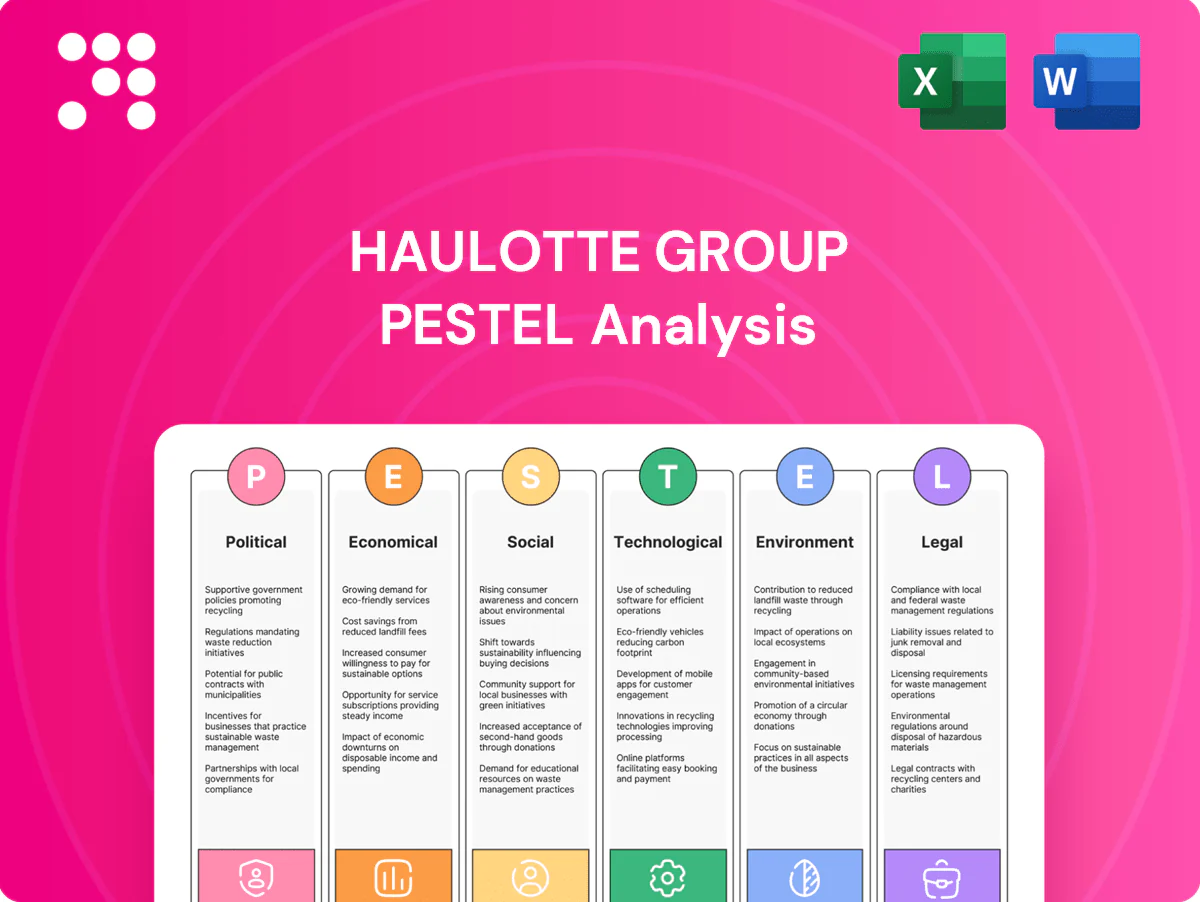

Get strategic clarity with our focused PESTLE Analysis of Haulotte Group—three to five expert-level insights reveal how political, economic, and technological forces are reshaping its market position. Ideal for investors and strategists, this concise report highlights risks and growth levers. Download the full, editable analysis now to act with confidence.

Political factors

Trade policy and tariffs

AWPs and components cross borders, exposing Haulotte to tariff swings and non-tariff barriers; US Section 232 steel tariffs (25%) and periodic EU safeguard measures can raise input costs and squeeze margins. Shifts in EU–US–China trade relations since 2022 altered sourcing costs and price competitiveness, prompting localization and supplier diversification strategies to mitigate disruption. Monitoring anti-dumping actions on steel and electronics remains critical.

Public infrastructure spending

Government-funded infrastructure and energy projects, supported by NextGenerationEU (€723.8bn) and the EU 2021–2027 multiannual budget (€1.074tn), materially boost demand for lift equipment. Fiscal stimulus or cohesion fund disbursements accelerate orders, while austerity dampens cycles. Renewables and grid-upgrade priorities favor telehandlers and boom lifts, and staggered regional budget timing obscures backlog visibility.

Geopolitical stability and sanctions

Conflict zones and sanctions (notably measures since 2022 against Russia) constrain Haulotte’s sales channels, service access and parts logistics across its presence in over 140 countries. Currency inconvertibility and export restrictions complicate deliveries and receivables, increasing DSO and collection risk. Relocating inventory and adjusting dealer networks preserves continuity, while political risk insurance is used to protect large contracts abroad.

Industrial policy and reshoring

Industrial policy and reshoring drive Haulotte plant siting and local-content rules; France Relance mobilized €100 billion and France 2030 €54 billion to boost onshore industry, while the EU Recovery and Resilience Facility totals €672.5 billion. Subsidies and public procurement favor electric/hybrid AWPs, with CAPEX support commonly covering 20–40% and local-content thresholds often around 30%, boosting tender eligibility and lowering deployment cost.

- Policies: France Relance €100bn; France 2030 €54bn; RRF €672.5bn

- Local content: commonly ~30%

- Subsidy impact: CAPEX support often 20–40%

- Innovation: national programs increase tech funding and grant access

Workplace safety regulation support

Governments promoting safety at height favor aerial work platforms over scaffolding, boosting AWP adoption through regulations and public procurement that commonly require CE-marked and certified machines under EU Directive 2014/24/EU.

Active engagement with regulators and IPAF-led industry associations helps Haulotte influence standards timelines and align policy with practical safety outcomes, aiding market access and tender success.

Tariff shocks and sanctions reshape AWP supply chains; EU funds drive electric AWP demand

Haulotte faces tariff volatility (US steel Section 232 25%) and trade shifts since 2022 that drive supplier diversification; anti-dumping and sanctions (post‑2022 Russia) increase delivery and receivable risk across 140+ countries. EU fiscal programs (NextGenerationEU €723.8bn; RRF €672.5bn; France Relance €100bn; France 2030 €54bn) boost AWP demand and favor electric AWPs via CAPEX support (20–40%) and ~30% local‑content rules.

| Metric | Value |

|---|---|

| Tariff | US steel 25% |

| Fiscal programs | €723.8bn / €672.5bn |

| Local content | ~30% |

What is included in the product

Examines how Political, Economic, Social, Technological, Environmental and Legal forces shape Haulotte Group’s operating landscape, with data-driven insights and forward-looking scenarios tailored to its markets and industry; formatted for executives, investors and consultants to identify risks, opportunities and strategic actions.

Provides a clean, categorized Haulotte Group PESTLE summary for quick reference in meetings or presentations, with editable notes to tailor insights by region or business line.

Economic factors

Construction cycle sensitivity

AWP demand closely follows non-residential construction, logistics hubs and maintenance cycles, so construction slowdowns curb fleet expansion and new unit purchases, shifting OEM revenue mix toward parts and after-sales services.

Backlog levels and rental fleet utilization are key leading indicators for Haulotte’s order intake and production planning.

Diversification across end-markets such as infrastructure, retail and utilities helps smooth cyclical volatility and stabilise service revenues.

Interest rates and financing costs

Higher benchmark rates (Fed funds 5.25–5.50% peak in 2023–24; ECB deposit ~4.00% in 2024) raise leasing and rental fleet financing costs, constraining rental operators and dampening capex for Haulotte’s equipment. OEM captive finance or bank partnerships can sustain sales by offering subsidized terms. Rate cuts typically unlock deferred purchases; hedging reduces exposure on variable-rate debt and stabilizes margins.

FX volatility and global footprint

Haulotte’s revenues and costs span EUR, USD, CNY and several emerging-market currencies, so FX swings materially affect margins and competitive price positioning versus US and Asian peers. Natural hedging from localized production, indexed pricing clauses and export price adjustments help stabilize profitability. A transparent FX policy and regular disclosure to investors and distributors reduce uncertainty and support order-book visibility.

Input costs and supply chain

Steel, batteries, hydraulics and semiconductors are the main BOM drivers for Haulotte; battery pack costs were about 132 USD/kWh in 2023 (BloombergNEF), directly lifting unit costs. Inflation and lingering logistics/port bottlenecks have pressured lead times and delivery reliability into 2024. Dual-sourcing and design-to-cost efforts help protect gross margins, while multi-year contracts with key suppliers improve cost visibility.

- steel — price volatility raises input cost risk

- batteries — 132 USD/kWh (BNEF 2023)

- semiconductors/hydraulics — lead-time exposure

- mitigation — dual-sourcing, design-to-cost, long-term supplier contracts

Rental market dynamics

Rental companies are Haulotte's primary buyers; their fleet age, utilization and ROIC tightly govern order cycles, with rental penetration in mature markets often above 60%, pushing cyclicality into 12–36 month refresh windows. Consolidation among giants (United Rentals, Ashtead/Sunbelt, Herc) boosts customer pricing power and order concentration. Shifts to electrified and rough-terrain units raise ASPs, while service contracts and telematics create resilient recurring revenue streams.

- Primary buyers: rental firms

- Fleet metrics drive orders

- Consolidation increases buyer power

- Electrified/RT ups ASPs

- Aftermarket & telematics = recurring revenue

Tariff shocks and sanctions reshape AWP supply chains; EU funds drive electric AWP demand

AWP demand tracks non-residential construction and rental fleet cycles, so slowdowns shift Haulotte mix toward parts and services. Higher rates (Fed 5.25–5.50% peak 2023–24; ECB ~4.0% 2024) raise leasing costs and delay purchases. FX across EUR/USD/CNY and BOM (batteries 132 USD/kWh BNEF 2023) materially affect margins.

| Indicator | Value |

|---|---|

| Fed peak | 5.25–5.50% (2023–24) |

| ECB | ~4.0% (2024) |

| Battery cost | 132 USD/kWh (2023) |

| Rental penetration | >60% (mature markets) |

Same Document Delivered

Haulotte Group PESTLE Analysis

The Haulotte Group PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment. No placeholders or teasers. After checkout you’ll instantly download this same finished file.

Skip the Research. Get the Strategy.

Get strategic clarity with our focused PESTLE Analysis of Haulotte Group—three to five expert-level insights reveal how political, economic, and technological forces are reshaping its market position. Ideal for investors and strategists, this concise report highlights risks and growth levers. Download the full, editable analysis now to act with confidence.

Political factors

Trade policy and tariffs

AWPs and components cross borders, exposing Haulotte to tariff swings and non-tariff barriers; US Section 232 steel tariffs (25%) and periodic EU safeguard measures can raise input costs and squeeze margins. Shifts in EU–US–China trade relations since 2022 altered sourcing costs and price competitiveness, prompting localization and supplier diversification strategies to mitigate disruption. Monitoring anti-dumping actions on steel and electronics remains critical.

Public infrastructure spending

Government-funded infrastructure and energy projects, supported by NextGenerationEU (€723.8bn) and the EU 2021–2027 multiannual budget (€1.074tn), materially boost demand for lift equipment. Fiscal stimulus or cohesion fund disbursements accelerate orders, while austerity dampens cycles. Renewables and grid-upgrade priorities favor telehandlers and boom lifts, and staggered regional budget timing obscures backlog visibility.

Geopolitical stability and sanctions

Conflict zones and sanctions (notably measures since 2022 against Russia) constrain Haulotte’s sales channels, service access and parts logistics across its presence in over 140 countries. Currency inconvertibility and export restrictions complicate deliveries and receivables, increasing DSO and collection risk. Relocating inventory and adjusting dealer networks preserves continuity, while political risk insurance is used to protect large contracts abroad.

Industrial policy and reshoring

Industrial policy and reshoring drive Haulotte plant siting and local-content rules; France Relance mobilized €100 billion and France 2030 €54 billion to boost onshore industry, while the EU Recovery and Resilience Facility totals €672.5 billion. Subsidies and public procurement favor electric/hybrid AWPs, with CAPEX support commonly covering 20–40% and local-content thresholds often around 30%, boosting tender eligibility and lowering deployment cost.

- Policies: France Relance €100bn; France 2030 €54bn; RRF €672.5bn

- Local content: commonly ~30%

- Subsidy impact: CAPEX support often 20–40%

- Innovation: national programs increase tech funding and grant access

Workplace safety regulation support

Governments promoting safety at height favor aerial work platforms over scaffolding, boosting AWP adoption through regulations and public procurement that commonly require CE-marked and certified machines under EU Directive 2014/24/EU.

Active engagement with regulators and IPAF-led industry associations helps Haulotte influence standards timelines and align policy with practical safety outcomes, aiding market access and tender success.

Tariff shocks and sanctions reshape AWP supply chains; EU funds drive electric AWP demand

Haulotte faces tariff volatility (US steel Section 232 25%) and trade shifts since 2022 that drive supplier diversification; anti-dumping and sanctions (post‑2022 Russia) increase delivery and receivable risk across 140+ countries. EU fiscal programs (NextGenerationEU €723.8bn; RRF €672.5bn; France Relance €100bn; France 2030 €54bn) boost AWP demand and favor electric AWPs via CAPEX support (20–40%) and ~30% local‑content rules.

| Metric | Value |

|---|---|

| Tariff | US steel 25% |

| Fiscal programs | €723.8bn / €672.5bn |

| Local content | ~30% |

What is included in the product

Examines how Political, Economic, Social, Technological, Environmental and Legal forces shape Haulotte Group’s operating landscape, with data-driven insights and forward-looking scenarios tailored to its markets and industry; formatted for executives, investors and consultants to identify risks, opportunities and strategic actions.

Provides a clean, categorized Haulotte Group PESTLE summary for quick reference in meetings or presentations, with editable notes to tailor insights by region or business line.

Economic factors

Construction cycle sensitivity

AWP demand closely follows non-residential construction, logistics hubs and maintenance cycles, so construction slowdowns curb fleet expansion and new unit purchases, shifting OEM revenue mix toward parts and after-sales services.

Backlog levels and rental fleet utilization are key leading indicators for Haulotte’s order intake and production planning.

Diversification across end-markets such as infrastructure, retail and utilities helps smooth cyclical volatility and stabilise service revenues.

Interest rates and financing costs

Higher benchmark rates (Fed funds 5.25–5.50% peak in 2023–24; ECB deposit ~4.00% in 2024) raise leasing and rental fleet financing costs, constraining rental operators and dampening capex for Haulotte’s equipment. OEM captive finance or bank partnerships can sustain sales by offering subsidized terms. Rate cuts typically unlock deferred purchases; hedging reduces exposure on variable-rate debt and stabilizes margins.

FX volatility and global footprint

Haulotte’s revenues and costs span EUR, USD, CNY and several emerging-market currencies, so FX swings materially affect margins and competitive price positioning versus US and Asian peers. Natural hedging from localized production, indexed pricing clauses and export price adjustments help stabilize profitability. A transparent FX policy and regular disclosure to investors and distributors reduce uncertainty and support order-book visibility.

Input costs and supply chain

Steel, batteries, hydraulics and semiconductors are the main BOM drivers for Haulotte; battery pack costs were about 132 USD/kWh in 2023 (BloombergNEF), directly lifting unit costs. Inflation and lingering logistics/port bottlenecks have pressured lead times and delivery reliability into 2024. Dual-sourcing and design-to-cost efforts help protect gross margins, while multi-year contracts with key suppliers improve cost visibility.

- steel — price volatility raises input cost risk

- batteries — 132 USD/kWh (BNEF 2023)

- semiconductors/hydraulics — lead-time exposure

- mitigation — dual-sourcing, design-to-cost, long-term supplier contracts

Rental market dynamics

Rental companies are Haulotte's primary buyers; their fleet age, utilization and ROIC tightly govern order cycles, with rental penetration in mature markets often above 60%, pushing cyclicality into 12–36 month refresh windows. Consolidation among giants (United Rentals, Ashtead/Sunbelt, Herc) boosts customer pricing power and order concentration. Shifts to electrified and rough-terrain units raise ASPs, while service contracts and telematics create resilient recurring revenue streams.

- Primary buyers: rental firms

- Fleet metrics drive orders

- Consolidation increases buyer power

- Electrified/RT ups ASPs

- Aftermarket & telematics = recurring revenue

Tariff shocks and sanctions reshape AWP supply chains; EU funds drive electric AWP demand

AWP demand tracks non-residential construction and rental fleet cycles, so slowdowns shift Haulotte mix toward parts and services. Higher rates (Fed 5.25–5.50% peak 2023–24; ECB ~4.0% 2024) raise leasing costs and delay purchases. FX across EUR/USD/CNY and BOM (batteries 132 USD/kWh BNEF 2023) materially affect margins.

| Indicator | Value |

|---|---|

| Fed peak | 5.25–5.50% (2023–24) |

| ECB | ~4.0% (2024) |

| Battery cost | 132 USD/kWh (2023) |

| Rental penetration | >60% (mature markets) |

Same Document Delivered

Haulotte Group PESTLE Analysis

The Haulotte Group PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment. No placeholders or teasers. After checkout you’ll instantly download this same finished file.

Description

Skip the Research. Get the Strategy.

Get strategic clarity with our focused PESTLE Analysis of Haulotte Group—three to five expert-level insights reveal how political, economic, and technological forces are reshaping its market position. Ideal for investors and strategists, this concise report highlights risks and growth levers. Download the full, editable analysis now to act with confidence.

Political factors

Trade policy and tariffs

AWPs and components cross borders, exposing Haulotte to tariff swings and non-tariff barriers; US Section 232 steel tariffs (25%) and periodic EU safeguard measures can raise input costs and squeeze margins. Shifts in EU–US–China trade relations since 2022 altered sourcing costs and price competitiveness, prompting localization and supplier diversification strategies to mitigate disruption. Monitoring anti-dumping actions on steel and electronics remains critical.

Public infrastructure spending

Government-funded infrastructure and energy projects, supported by NextGenerationEU (€723.8bn) and the EU 2021–2027 multiannual budget (€1.074tn), materially boost demand for lift equipment. Fiscal stimulus or cohesion fund disbursements accelerate orders, while austerity dampens cycles. Renewables and grid-upgrade priorities favor telehandlers and boom lifts, and staggered regional budget timing obscures backlog visibility.

Geopolitical stability and sanctions

Conflict zones and sanctions (notably measures since 2022 against Russia) constrain Haulotte’s sales channels, service access and parts logistics across its presence in over 140 countries. Currency inconvertibility and export restrictions complicate deliveries and receivables, increasing DSO and collection risk. Relocating inventory and adjusting dealer networks preserves continuity, while political risk insurance is used to protect large contracts abroad.

Industrial policy and reshoring

Industrial policy and reshoring drive Haulotte plant siting and local-content rules; France Relance mobilized €100 billion and France 2030 €54 billion to boost onshore industry, while the EU Recovery and Resilience Facility totals €672.5 billion. Subsidies and public procurement favor electric/hybrid AWPs, with CAPEX support commonly covering 20–40% and local-content thresholds often around 30%, boosting tender eligibility and lowering deployment cost.

- Policies: France Relance €100bn; France 2030 €54bn; RRF €672.5bn

- Local content: commonly ~30%

- Subsidy impact: CAPEX support often 20–40%

- Innovation: national programs increase tech funding and grant access

Workplace safety regulation support

Governments promoting safety at height favor aerial work platforms over scaffolding, boosting AWP adoption through regulations and public procurement that commonly require CE-marked and certified machines under EU Directive 2014/24/EU.

Active engagement with regulators and IPAF-led industry associations helps Haulotte influence standards timelines and align policy with practical safety outcomes, aiding market access and tender success.

Tariff shocks and sanctions reshape AWP supply chains; EU funds drive electric AWP demand

Haulotte faces tariff volatility (US steel Section 232 25%) and trade shifts since 2022 that drive supplier diversification; anti-dumping and sanctions (post‑2022 Russia) increase delivery and receivable risk across 140+ countries. EU fiscal programs (NextGenerationEU €723.8bn; RRF €672.5bn; France Relance €100bn; France 2030 €54bn) boost AWP demand and favor electric AWPs via CAPEX support (20–40%) and ~30% local‑content rules.

| Metric | Value |

|---|---|

| Tariff | US steel 25% |

| Fiscal programs | €723.8bn / €672.5bn |

| Local content | ~30% |

What is included in the product

Examines how Political, Economic, Social, Technological, Environmental and Legal forces shape Haulotte Group’s operating landscape, with data-driven insights and forward-looking scenarios tailored to its markets and industry; formatted for executives, investors and consultants to identify risks, opportunities and strategic actions.

Provides a clean, categorized Haulotte Group PESTLE summary for quick reference in meetings or presentations, with editable notes to tailor insights by region or business line.

Economic factors

Construction cycle sensitivity

AWP demand closely follows non-residential construction, logistics hubs and maintenance cycles, so construction slowdowns curb fleet expansion and new unit purchases, shifting OEM revenue mix toward parts and after-sales services.

Backlog levels and rental fleet utilization are key leading indicators for Haulotte’s order intake and production planning.

Diversification across end-markets such as infrastructure, retail and utilities helps smooth cyclical volatility and stabilise service revenues.

Interest rates and financing costs

Higher benchmark rates (Fed funds 5.25–5.50% peak in 2023–24; ECB deposit ~4.00% in 2024) raise leasing and rental fleet financing costs, constraining rental operators and dampening capex for Haulotte’s equipment. OEM captive finance or bank partnerships can sustain sales by offering subsidized terms. Rate cuts typically unlock deferred purchases; hedging reduces exposure on variable-rate debt and stabilizes margins.

FX volatility and global footprint

Haulotte’s revenues and costs span EUR, USD, CNY and several emerging-market currencies, so FX swings materially affect margins and competitive price positioning versus US and Asian peers. Natural hedging from localized production, indexed pricing clauses and export price adjustments help stabilize profitability. A transparent FX policy and regular disclosure to investors and distributors reduce uncertainty and support order-book visibility.

Input costs and supply chain

Steel, batteries, hydraulics and semiconductors are the main BOM drivers for Haulotte; battery pack costs were about 132 USD/kWh in 2023 (BloombergNEF), directly lifting unit costs. Inflation and lingering logistics/port bottlenecks have pressured lead times and delivery reliability into 2024. Dual-sourcing and design-to-cost efforts help protect gross margins, while multi-year contracts with key suppliers improve cost visibility.

- steel — price volatility raises input cost risk

- batteries — 132 USD/kWh (BNEF 2023)

- semiconductors/hydraulics — lead-time exposure

- mitigation — dual-sourcing, design-to-cost, long-term supplier contracts

Rental market dynamics

Rental companies are Haulotte's primary buyers; their fleet age, utilization and ROIC tightly govern order cycles, with rental penetration in mature markets often above 60%, pushing cyclicality into 12–36 month refresh windows. Consolidation among giants (United Rentals, Ashtead/Sunbelt, Herc) boosts customer pricing power and order concentration. Shifts to electrified and rough-terrain units raise ASPs, while service contracts and telematics create resilient recurring revenue streams.

- Primary buyers: rental firms

- Fleet metrics drive orders

- Consolidation increases buyer power

- Electrified/RT ups ASPs

- Aftermarket & telematics = recurring revenue

Tariff shocks and sanctions reshape AWP supply chains; EU funds drive electric AWP demand

AWP demand tracks non-residential construction and rental fleet cycles, so slowdowns shift Haulotte mix toward parts and services. Higher rates (Fed 5.25–5.50% peak 2023–24; ECB ~4.0% 2024) raise leasing costs and delay purchases. FX across EUR/USD/CNY and BOM (batteries 132 USD/kWh BNEF 2023) materially affect margins.

| Indicator | Value |

|---|---|

| Fed peak | 5.25–5.50% (2023–24) |

| ECB | ~4.0% (2024) |

| Battery cost | 132 USD/kWh (2023) |

| Rental penetration | >60% (mature markets) |

Same Document Delivered

Haulotte Group PESTLE Analysis

The Haulotte Group PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment. No placeholders or teasers. After checkout you’ll instantly download this same finished file.