HBT Financial Business Model Canvas

Financial Business Model Canvas: Benchmark value creation, revenue streams, and growth

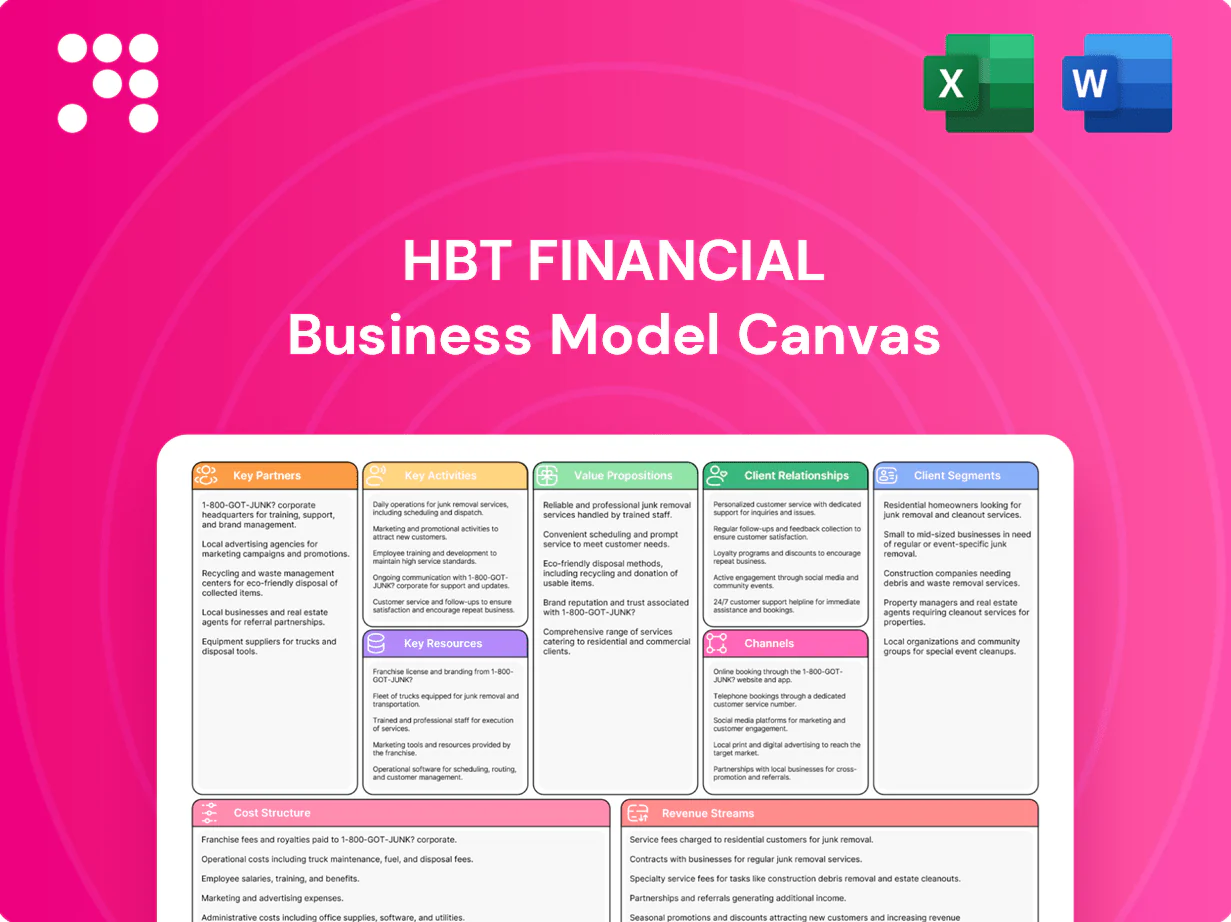

Explore the HBT Financial Business Model Canvas to see how the firm creates customer value, scales services, and monetizes relationships. This concise, actionable snapshot highlights key partners, channels, revenue streams and cost drivers. Ideal for investors, advisors and founders seeking proven strategy. Download the full Canvas to benchmark, adapt, and drive growth.

Partnerships

Core/Fintech vendors

Partnerships with core banking, digital banking and cybersecurity providers underpin reliable operations and a steady innovation cadence, delivering industry-standard 99.9% uptime SLAs. Vendors enable mobile features, payments and analytics without heavy in-house build, leveraging PCI-DSS and SOC 2 frameworks. Co-development roadmaps accelerate releases tied to customer needs, with quarterly roadmaps and annual audits ensuring resilience and regulatory compliance.

Payment networks

Ties with card networks and ACH/wire rails enable everyday spending, treasury and merchant services by connecting HBT to networks that process trillions of dollars annually. Interchange economics (typically ~1–2% of transaction value) add fee income while expanding acceptance and reducing friction. Network risk tools strengthen fraud prevention and dispute handling, and joint marketing lifts card adoption and usage.

Correspondent banks

Correspondent banks provide participation loans and liquidity lines typically sized $10–250m and access to specialized products beyond HBT’s local balance sheet, supporting foreign wires, cash management extensions and loan syndications across a network spanning 180+ countries.

Risk-sharing with correspondents drives capital efficiency—often yielding double-digit reductions in balance-sheet strain—and expands customer coverage while bilateral knowledge exchange improves HBT underwriting practices and credit selection.

Wealth custodians

HBT partners with wealth custodians, broker-dealers, and trust platforms to scale advisory, custody, and fiduciary operations, enabling consolidated reporting and secure asset servicing. Integrated APIs and middleware drive unified client statements and reduce reconciliation overhead. Open-architecture product shelves broaden client choice while compliance tooling enforces Reg BI (2020) best-interest standards.

- Consolidated reporting via integrated custody

- Open-architecture expands product access

- API-driven custody reduces ops risk

- Compliance tooling enforces Reg BI

Local groups & ag orgs

Local community associations, chambers, and agricultural cooperatives provide market access and credibility, linking HBT to entrepreneurs and producers. Co-hosted events and financial education deepen relationships with small businesses and farmers and surface local credit needs early. These partnerships reinforce HBT’s regional commitment and brand; 2024 SBA data show 99.9% of US firms are small businesses.

- Market access & credibility

- Events + education = deeper ties

- Early credit need discovery

- Reinforces regional brand

Payments ecosystem: 99.9% uptime, 1–2% interchange, $10–250M lines across 180+ countries

Core/digital/cyber vendors ensure 99.9% uptime, PCI‑DSS/SOC2 and quarterly roadmaps. Card networks/ACH yield interchange ~1–2% and fraud controls; correspondents provide $10–250m lines across 180+ countries. Wealth custodians and local associations scale custody/advisory and access to small businesses (2024 SBA: 99.9% firms).

| Partner | Role | KPI |

|---|---|---|

| Core/digital | Ops & innovation | 99.9% uptime |

| Card/rails | Payments | 1–2% interchange |

| Correspondents | Liquidity | $10–250m; 180+ countries |

What is included in the product

A concise, pre-built Business Model Canvas for HBT Financial mapping customer segments, channels, value propositions and revenue streams across the 9 BMC blocks, with integrated SWOT, competitive insights and investor-ready narratives.

High-level view of HBT Financial’s business model with editable cells, relieving the pain of fragmented strategy documents by consolidating core components into a single, shareable canvas that saves hours of formatting and alignment.

Activities

Deposit gathering

Designing competitive checking, savings and time deposits fuels low-cost funding by locking balances below market funding costs while the Fed funds target stood at 5.25–5.50% in mid‑2024. Targeted campaigns and relationship pricing grow stable household balances. Cash‑management solutions retain commercial deposits. Ongoing CX improvements increase customers naming HBT as their primary bank.

Underwriting & lending

Rigorous credit analysis for commercial, retail, and agricultural loans drives HBT Financials prudent growth, with underwriting standards updated through 2024 to reflect rising rate stress. Pricing, collateral requirements, and covenant structures are calibrated to the bank’s documented risk appetite and regulatory guidance. Ongoing portfolio monitoring and timely renewals manage lifecycle performance, while proactive problem loan resolution preserves capital and liquidity.

Risk & compliance

Executing BSA/AML, KYC, and fair lending programs ensures safety and soundness; 2024 AML-related fines globally exceeded $3 billion, underscoring enforcement risk. Regular stress testing and allowance modeling prepare for cycles. Cyber, fraud, and vendor risk frameworks protect customers and the bank. Timely regulatory reporting sustains trust and operating licenses.

Digital delivery

Enhancing online and mobile banking boosts convenience and engagement, with 2024 industry adoption exceeding 70% and session times up 15% year-over-year. Features include bill pay, RDC, P2P, and integrated treasury portals that expand wallet share. Data-driven UX testing reduces friction and supports sales while robust multi-factor authentication and real-time monitoring secure access.

- Digital adoption >70% (2024)

- Bill pay, RDC, P2P, treasury portals

- UX A/B testing → higher conversions

- MFA + real-time monitoring for security

Wealth & trust services

Competitive deposits and digital adoption >70% drive low‑cost funding and cross‑sell gains

Designing competitive deposits captures low‑cost funding while Fed funds target was 5.25–5.50% mid‑2024; digital adoption >70% boosts engagement. Updated 2024 credit underwriting and active portfolio monitoring preserve asset quality and liquidity. Wealth/trust + CX reduced errors 22% and raised cross‑sell revenue 18% (2024); BSA/AML, cyber, stress testing ensure compliance.

| Metric | 2024 |

|---|---|

| Fed funds target | 5.25–5.50% |

| Digital adoption | >70% |

| Error reduction (trust) | 22% |

| Cross‑sell lift | +18% |

Full Version Awaits

Business Model Canvas

The HBT Financial Business Model Canvas you’re previewing is the actual deliverable, not a mockup or sample. When you purchase, you’ll receive this exact document—complete, editable and ready to use. The full file mirrors this preview in structure and content, formatted for easy editing and presentation.

Financial Business Model Canvas: Benchmark value creation, revenue streams, and growth

Explore the HBT Financial Business Model Canvas to see how the firm creates customer value, scales services, and monetizes relationships. This concise, actionable snapshot highlights key partners, channels, revenue streams and cost drivers. Ideal for investors, advisors and founders seeking proven strategy. Download the full Canvas to benchmark, adapt, and drive growth.

Partnerships

Core/Fintech vendors

Partnerships with core banking, digital banking and cybersecurity providers underpin reliable operations and a steady innovation cadence, delivering industry-standard 99.9% uptime SLAs. Vendors enable mobile features, payments and analytics without heavy in-house build, leveraging PCI-DSS and SOC 2 frameworks. Co-development roadmaps accelerate releases tied to customer needs, with quarterly roadmaps and annual audits ensuring resilience and regulatory compliance.

Payment networks

Ties with card networks and ACH/wire rails enable everyday spending, treasury and merchant services by connecting HBT to networks that process trillions of dollars annually. Interchange economics (typically ~1–2% of transaction value) add fee income while expanding acceptance and reducing friction. Network risk tools strengthen fraud prevention and dispute handling, and joint marketing lifts card adoption and usage.

Correspondent banks

Correspondent banks provide participation loans and liquidity lines typically sized $10–250m and access to specialized products beyond HBT’s local balance sheet, supporting foreign wires, cash management extensions and loan syndications across a network spanning 180+ countries.

Risk-sharing with correspondents drives capital efficiency—often yielding double-digit reductions in balance-sheet strain—and expands customer coverage while bilateral knowledge exchange improves HBT underwriting practices and credit selection.

Wealth custodians

HBT partners with wealth custodians, broker-dealers, and trust platforms to scale advisory, custody, and fiduciary operations, enabling consolidated reporting and secure asset servicing. Integrated APIs and middleware drive unified client statements and reduce reconciliation overhead. Open-architecture product shelves broaden client choice while compliance tooling enforces Reg BI (2020) best-interest standards.

- Consolidated reporting via integrated custody

- Open-architecture expands product access

- API-driven custody reduces ops risk

- Compliance tooling enforces Reg BI

Local groups & ag orgs

Local community associations, chambers, and agricultural cooperatives provide market access and credibility, linking HBT to entrepreneurs and producers. Co-hosted events and financial education deepen relationships with small businesses and farmers and surface local credit needs early. These partnerships reinforce HBT’s regional commitment and brand; 2024 SBA data show 99.9% of US firms are small businesses.

- Market access & credibility

- Events + education = deeper ties

- Early credit need discovery

- Reinforces regional brand

Payments ecosystem: 99.9% uptime, 1–2% interchange, $10–250M lines across 180+ countries

Core/digital/cyber vendors ensure 99.9% uptime, PCI‑DSS/SOC2 and quarterly roadmaps. Card networks/ACH yield interchange ~1–2% and fraud controls; correspondents provide $10–250m lines across 180+ countries. Wealth custodians and local associations scale custody/advisory and access to small businesses (2024 SBA: 99.9% firms).

| Partner | Role | KPI |

|---|---|---|

| Core/digital | Ops & innovation | 99.9% uptime |

| Card/rails | Payments | 1–2% interchange |

| Correspondents | Liquidity | $10–250m; 180+ countries |

What is included in the product

A concise, pre-built Business Model Canvas for HBT Financial mapping customer segments, channels, value propositions and revenue streams across the 9 BMC blocks, with integrated SWOT, competitive insights and investor-ready narratives.

High-level view of HBT Financial’s business model with editable cells, relieving the pain of fragmented strategy documents by consolidating core components into a single, shareable canvas that saves hours of formatting and alignment.

Activities

Deposit gathering

Designing competitive checking, savings and time deposits fuels low-cost funding by locking balances below market funding costs while the Fed funds target stood at 5.25–5.50% in mid‑2024. Targeted campaigns and relationship pricing grow stable household balances. Cash‑management solutions retain commercial deposits. Ongoing CX improvements increase customers naming HBT as their primary bank.

Underwriting & lending

Rigorous credit analysis for commercial, retail, and agricultural loans drives HBT Financials prudent growth, with underwriting standards updated through 2024 to reflect rising rate stress. Pricing, collateral requirements, and covenant structures are calibrated to the bank’s documented risk appetite and regulatory guidance. Ongoing portfolio monitoring and timely renewals manage lifecycle performance, while proactive problem loan resolution preserves capital and liquidity.

Risk & compliance

Executing BSA/AML, KYC, and fair lending programs ensures safety and soundness; 2024 AML-related fines globally exceeded $3 billion, underscoring enforcement risk. Regular stress testing and allowance modeling prepare for cycles. Cyber, fraud, and vendor risk frameworks protect customers and the bank. Timely regulatory reporting sustains trust and operating licenses.

Digital delivery

Enhancing online and mobile banking boosts convenience and engagement, with 2024 industry adoption exceeding 70% and session times up 15% year-over-year. Features include bill pay, RDC, P2P, and integrated treasury portals that expand wallet share. Data-driven UX testing reduces friction and supports sales while robust multi-factor authentication and real-time monitoring secure access.

- Digital adoption >70% (2024)

- Bill pay, RDC, P2P, treasury portals

- UX A/B testing → higher conversions

- MFA + real-time monitoring for security

Wealth & trust services

Competitive deposits and digital adoption >70% drive low‑cost funding and cross‑sell gains

Designing competitive deposits captures low‑cost funding while Fed funds target was 5.25–5.50% mid‑2024; digital adoption >70% boosts engagement. Updated 2024 credit underwriting and active portfolio monitoring preserve asset quality and liquidity. Wealth/trust + CX reduced errors 22% and raised cross‑sell revenue 18% (2024); BSA/AML, cyber, stress testing ensure compliance.

| Metric | 2024 |

|---|---|

| Fed funds target | 5.25–5.50% |

| Digital adoption | >70% |

| Error reduction (trust) | 22% |

| Cross‑sell lift | +18% |

Full Version Awaits

Business Model Canvas

The HBT Financial Business Model Canvas you’re previewing is the actual deliverable, not a mockup or sample. When you purchase, you’ll receive this exact document—complete, editable and ready to use. The full file mirrors this preview in structure and content, formatted for easy editing and presentation.

Original: $10.00

-65%$10.00

$3.50Description

Financial Business Model Canvas: Benchmark value creation, revenue streams, and growth

Explore the HBT Financial Business Model Canvas to see how the firm creates customer value, scales services, and monetizes relationships. This concise, actionable snapshot highlights key partners, channels, revenue streams and cost drivers. Ideal for investors, advisors and founders seeking proven strategy. Download the full Canvas to benchmark, adapt, and drive growth.

Partnerships

Core/Fintech vendors

Partnerships with core banking, digital banking and cybersecurity providers underpin reliable operations and a steady innovation cadence, delivering industry-standard 99.9% uptime SLAs. Vendors enable mobile features, payments and analytics without heavy in-house build, leveraging PCI-DSS and SOC 2 frameworks. Co-development roadmaps accelerate releases tied to customer needs, with quarterly roadmaps and annual audits ensuring resilience and regulatory compliance.

Payment networks

Ties with card networks and ACH/wire rails enable everyday spending, treasury and merchant services by connecting HBT to networks that process trillions of dollars annually. Interchange economics (typically ~1–2% of transaction value) add fee income while expanding acceptance and reducing friction. Network risk tools strengthen fraud prevention and dispute handling, and joint marketing lifts card adoption and usage.

Correspondent banks

Correspondent banks provide participation loans and liquidity lines typically sized $10–250m and access to specialized products beyond HBT’s local balance sheet, supporting foreign wires, cash management extensions and loan syndications across a network spanning 180+ countries.

Risk-sharing with correspondents drives capital efficiency—often yielding double-digit reductions in balance-sheet strain—and expands customer coverage while bilateral knowledge exchange improves HBT underwriting practices and credit selection.

Wealth custodians

HBT partners with wealth custodians, broker-dealers, and trust platforms to scale advisory, custody, and fiduciary operations, enabling consolidated reporting and secure asset servicing. Integrated APIs and middleware drive unified client statements and reduce reconciliation overhead. Open-architecture product shelves broaden client choice while compliance tooling enforces Reg BI (2020) best-interest standards.

- Consolidated reporting via integrated custody

- Open-architecture expands product access

- API-driven custody reduces ops risk

- Compliance tooling enforces Reg BI

Local groups & ag orgs

Local community associations, chambers, and agricultural cooperatives provide market access and credibility, linking HBT to entrepreneurs and producers. Co-hosted events and financial education deepen relationships with small businesses and farmers and surface local credit needs early. These partnerships reinforce HBT’s regional commitment and brand; 2024 SBA data show 99.9% of US firms are small businesses.

- Market access & credibility

- Events + education = deeper ties

- Early credit need discovery

- Reinforces regional brand

Payments ecosystem: 99.9% uptime, 1–2% interchange, $10–250M lines across 180+ countries

Core/digital/cyber vendors ensure 99.9% uptime, PCI‑DSS/SOC2 and quarterly roadmaps. Card networks/ACH yield interchange ~1–2% and fraud controls; correspondents provide $10–250m lines across 180+ countries. Wealth custodians and local associations scale custody/advisory and access to small businesses (2024 SBA: 99.9% firms).

| Partner | Role | KPI |

|---|---|---|

| Core/digital | Ops & innovation | 99.9% uptime |

| Card/rails | Payments | 1–2% interchange |

| Correspondents | Liquidity | $10–250m; 180+ countries |

What is included in the product

A concise, pre-built Business Model Canvas for HBT Financial mapping customer segments, channels, value propositions and revenue streams across the 9 BMC blocks, with integrated SWOT, competitive insights and investor-ready narratives.

High-level view of HBT Financial’s business model with editable cells, relieving the pain of fragmented strategy documents by consolidating core components into a single, shareable canvas that saves hours of formatting and alignment.

Activities

Deposit gathering

Designing competitive checking, savings and time deposits fuels low-cost funding by locking balances below market funding costs while the Fed funds target stood at 5.25–5.50% in mid‑2024. Targeted campaigns and relationship pricing grow stable household balances. Cash‑management solutions retain commercial deposits. Ongoing CX improvements increase customers naming HBT as their primary bank.

Underwriting & lending

Rigorous credit analysis for commercial, retail, and agricultural loans drives HBT Financials prudent growth, with underwriting standards updated through 2024 to reflect rising rate stress. Pricing, collateral requirements, and covenant structures are calibrated to the bank’s documented risk appetite and regulatory guidance. Ongoing portfolio monitoring and timely renewals manage lifecycle performance, while proactive problem loan resolution preserves capital and liquidity.

Risk & compliance

Executing BSA/AML, KYC, and fair lending programs ensures safety and soundness; 2024 AML-related fines globally exceeded $3 billion, underscoring enforcement risk. Regular stress testing and allowance modeling prepare for cycles. Cyber, fraud, and vendor risk frameworks protect customers and the bank. Timely regulatory reporting sustains trust and operating licenses.

Digital delivery

Enhancing online and mobile banking boosts convenience and engagement, with 2024 industry adoption exceeding 70% and session times up 15% year-over-year. Features include bill pay, RDC, P2P, and integrated treasury portals that expand wallet share. Data-driven UX testing reduces friction and supports sales while robust multi-factor authentication and real-time monitoring secure access.

- Digital adoption >70% (2024)

- Bill pay, RDC, P2P, treasury portals

- UX A/B testing → higher conversions

- MFA + real-time monitoring for security

Wealth & trust services

Competitive deposits and digital adoption >70% drive low‑cost funding and cross‑sell gains

Designing competitive deposits captures low‑cost funding while Fed funds target was 5.25–5.50% mid‑2024; digital adoption >70% boosts engagement. Updated 2024 credit underwriting and active portfolio monitoring preserve asset quality and liquidity. Wealth/trust + CX reduced errors 22% and raised cross‑sell revenue 18% (2024); BSA/AML, cyber, stress testing ensure compliance.

| Metric | 2024 |

|---|---|

| Fed funds target | 5.25–5.50% |

| Digital adoption | >70% |

| Error reduction (trust) | 22% |

| Cross‑sell lift | +18% |

Full Version Awaits

Business Model Canvas

The HBT Financial Business Model Canvas you’re previewing is the actual deliverable, not a mockup or sample. When you purchase, you’ll receive this exact document—complete, editable and ready to use. The full file mirrors this preview in structure and content, formatted for easy editing and presentation.