HCL Technologies Porter's Five Forces Analysis

From Overview to Strategy Blueprint

HCL Technologies faces moderate buyer power, intense rivalry, rising substitute threats from digital platforms, significant supplier leverage in niche tech, and barriers that moderate new entrants—this snapshot highlights strategic pressure points. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Hyperscaler and platform dependency

Cloud providers and platforms concentrate supplier power for HCLTech, with AWS (32%), Microsoft Azure (23%) and Google Cloud (11%) controlling most market share in 2024, shaping pricing and roadmap influence. Preferred partner tiers and long-term volume deals secure discounts but can lock HCLTech to vendor timelines; multicloud certifications and reusable accelerators improve switching and deployment speed. HCLTech’s FY24 revenue near $12.2B amplifies both leverage and dependence.

Specialized talent as a critical input

Scarce skills in AI, cybersecurity and product engineering push wage inflation and premium hiring; HCLTech reported roughly 224,000 employees in FY2024 and cited attrition near 20% in 2024, amplifying cost pressure. HCLTech’s global delivery model and internal academies expand supply and lower unit costs by leveraging offshore scale. Rapid technology shifts shorten upskilling cycles and raise training spend, while attrition spikes can disrupt delivery and margin mix.

Third‑party software licensing costs

Third-party licensing is a material input for HCL, with the company reporting FY2024 revenue of about $12.2B while clients face rising software costs; bundled enterprise agreements and HCL’s reseller partnerships often cut list prices, but usage-based models introduce billing volatility that can swing project margins. Increased use of open-source and proprietary IP reduces supplier dependency and can shave licensing spend across engagements.

Hardware and network vendors

Hardware and network vendors are concentrated: Dell, HPE, Cisco, Lenovo and Arista account for roughly 70% of server and network appliance shipments (IDC 2024), giving suppliers notable bargaining power; HCL mitigates this through scale purchasing, multi-vendor panels and regional logistics hubs which lower costs and supplier risk.

Supply-chain shocks have lengthened lead times by about 6–12 weeks and tightened SLAs; continued cloud migration (public cloud revenue up ~18% in 2024) reduces on-prem hardware exposure but increases dependency on platform providers.

- Concentration: top 5 OEMs ~70% (IDC 2024)

- Mitigation: scale buying, multi-vendor panels, logistics hubs

- Risk: 6–12 week lead-time elongation; SLA pressure

- Trend: cloud spend +~18% (2024) → less hardware, more platform dependency

Regulatory and compliance service inputs

Regulatory and compliance service inputs for HCL demand rigorous background checks, facility security and certified compliance tools in regulated deals, tightening supplier selection even as vendor diversity exists; HCL Technologies reported roughly $13.1 billion revenue in FY2024, amplifying exposure to credentialed supplier risk. Standardized control frameworks and reuse cut switching costs, but shifts in data sovereignty can force rapid vendor changes and operational disruption.

- Background checks narrow suppliers in sensitive geographies

- Facility security and certified tools are mandatory for regulated deals

- Framework reuse lowers switching costs

- Data sovereignty shifts can cause abrupt vendor swaps

Supplier power high - AWS 32% Azure 23% GCP 11%; talent strain, margins pressured

Supplier power is high: cloud platforms concentrate influence (AWS 32%, Azure 23%, Google 11% in 2024), tying pricing and roadmaps to vendors. Talent scarcity (224,000 employees; ~20% attrition FY2024) and third-party licensing raise costs and margin volatility. Hardware OEMs are concentrated (~70% top‑5), but HCLTech scale, multivendor buying and reuse reduce switching risk.

| Metric | 2024 |

|---|---|

| Cloud share (AWS/Azure/GCP) | 32% / 23% / 11% |

| Revenue (FY2024) | $12.2B |

| Employees | 224,000 |

| Attrition | ~20% |

| Top‑5 OEMs | ~70% |

| Cloud spend growth | +18% |

What is included in the product

Tailored Porter's Five Forces analysis of HCL Technologies that uncovers key drivers of competition, evaluates buyer and supplier power, assesses entry barriers and substitutes, and highlights disruptive threats and strategic levers shaping pricing, profitability, and market positioning.

A clear one-sheet Porter's Five Forces snapshot for HCL Technologies—customize pressure levels, swap in your own data, and instantly visualize strategic pressure with a spider chart; clean layout ready to copy into pitch decks or dashboards, no macros required.

Customers Bargaining Power

Large enterprises with strong procurement

Fortune 500 buyers run competitive RFPs and enforce strict rate cards, while multi-year, multi-tower contracts give them strong leverage on price and terms. HCLTech counters with outcome-based pricing and differentiated domain IP to protect margins. Its FY2024 revenue of $12.4B and documented transformation wins enhance referenceability and soften a pure cost focus.

High switching and multi-sourcing

Clients often split work across several vendors to manage risk and price, keeping switching barriers moderate—especially for commoditized IT services—while HCL Technologies reported full-year FY2024 revenue of about $12.5 billion, reflecting broad client diversification. Sticky areas such as managed operations and product engineering sustain higher retention. Strong governance and automation in large accounts raise exit frictions and increase lifetime value.

Demand for measurable outcomes

Buyers increasingly insist on business KPIs rather than effort-based hours, shifting leverage toward outcome contracts; HCL Technologies, with FY2024 revenue around $12.1 billion, markets accelerators and GenAI productivity uplifts to justify premium pricing. Missed outcomes lead to penalties and margin dilution, while co-innovation models lock longer tenures and deepen customer stickiness.

Vertical expertise expectations

Vertical expertise expectations heighten bargaining power where industry depth in BFSI, healthcare and manufacturing dictates procurement choices; HCLTech's regulatory fluency and product lineage in these sectors shifts negotiating leverage toward the vendor. In nascent verticals buyers retain leverage via pilots and PoCs, while published case studies and domain solutions reduce bake-off risk and accelerate deal closure in 2024.

- Seller strength: regulatory fluency

- Buyer leverage: pilots in nascent verticals

- Risk reduction: case studies/domain solutions

Security and compliance scrutiny

CISOs and regulators impose stringent controls that lengthen procurement and delivery cycles, raising pre-sales effort and audit timelines. Meeting high security and compliance bars narrows the competitor field and can materially lift win rates; assured compliance supports premium contracted margins. Remediation and audit requirements increase delivery cost and overhead—IBM 2024 reports average breach cost $4.45 million, underscoring buyer caution.

- lengthened cycles: higher pre-sales & audit time

- narrowed competition: improved win rates & pricing power

- higher delivery cost: remediation, audits, compliance teams

- market signal: IBM 2024 breach cost $4.45M

Outcome pricing and IP drive stickiness vs RFP pressure; $12.4B scale

Large enterprise buyers run competitive RFPs and enforce rate cards, giving them strong price leverage; HCLTech offsets this via outcome-based pricing, domain IP and FY2024 revenue of $12.4B, which improves references and softens pure cost focus. Multi-vendor sourcing keeps switching moderate for commoditized work, while managed services and co-innovation raise stickiness and lifetime value.

| Metric | Value | Impact |

|---|---|---|

| HCLTech FY2024 revenue | $12.4B | Referenceability, pricing leverage |

| Avg breach cost (2024, IBM) | $4.45M | Higher compliance demands |

What You See Is What You Get

HCL Technologies Porter's Five Forces Analysis

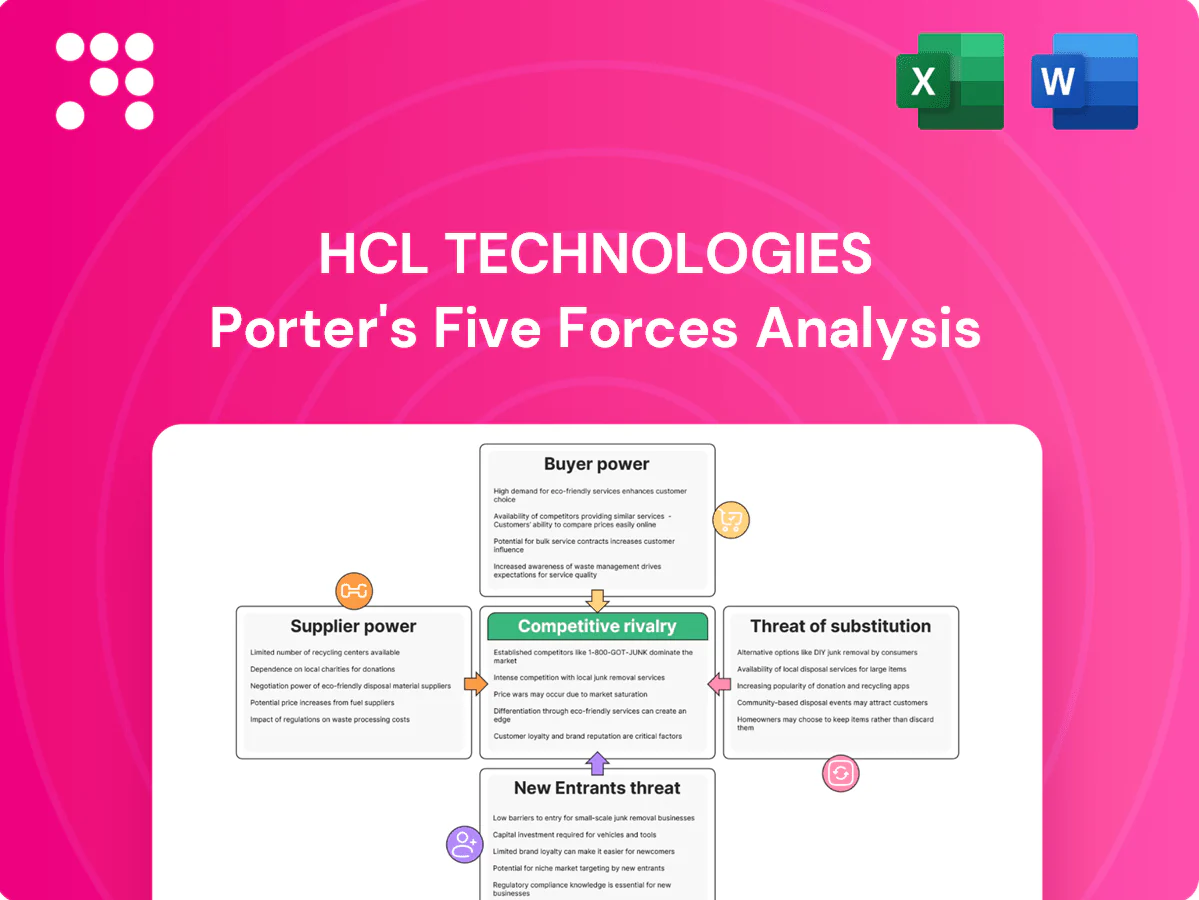

This preview shows the exact HCL Technologies Porter's Five Forces Analysis you'll receive—no placeholders or mockups. It is the fully formatted, final document covering competitive rivalry, threat of entrants, buyer and supplier power, and substitutes. Once you purchase, you'll get immediate access to this same ready-to-use file for download and use.

From Overview to Strategy Blueprint

HCL Technologies faces moderate buyer power, intense rivalry, rising substitute threats from digital platforms, significant supplier leverage in niche tech, and barriers that moderate new entrants—this snapshot highlights strategic pressure points. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Hyperscaler and platform dependency

Cloud providers and platforms concentrate supplier power for HCLTech, with AWS (32%), Microsoft Azure (23%) and Google Cloud (11%) controlling most market share in 2024, shaping pricing and roadmap influence. Preferred partner tiers and long-term volume deals secure discounts but can lock HCLTech to vendor timelines; multicloud certifications and reusable accelerators improve switching and deployment speed. HCLTech’s FY24 revenue near $12.2B amplifies both leverage and dependence.

Specialized talent as a critical input

Scarce skills in AI, cybersecurity and product engineering push wage inflation and premium hiring; HCLTech reported roughly 224,000 employees in FY2024 and cited attrition near 20% in 2024, amplifying cost pressure. HCLTech’s global delivery model and internal academies expand supply and lower unit costs by leveraging offshore scale. Rapid technology shifts shorten upskilling cycles and raise training spend, while attrition spikes can disrupt delivery and margin mix.

Third‑party software licensing costs

Third-party licensing is a material input for HCL, with the company reporting FY2024 revenue of about $12.2B while clients face rising software costs; bundled enterprise agreements and HCL’s reseller partnerships often cut list prices, but usage-based models introduce billing volatility that can swing project margins. Increased use of open-source and proprietary IP reduces supplier dependency and can shave licensing spend across engagements.

Hardware and network vendors

Hardware and network vendors are concentrated: Dell, HPE, Cisco, Lenovo and Arista account for roughly 70% of server and network appliance shipments (IDC 2024), giving suppliers notable bargaining power; HCL mitigates this through scale purchasing, multi-vendor panels and regional logistics hubs which lower costs and supplier risk.

Supply-chain shocks have lengthened lead times by about 6–12 weeks and tightened SLAs; continued cloud migration (public cloud revenue up ~18% in 2024) reduces on-prem hardware exposure but increases dependency on platform providers.

- Concentration: top 5 OEMs ~70% (IDC 2024)

- Mitigation: scale buying, multi-vendor panels, logistics hubs

- Risk: 6–12 week lead-time elongation; SLA pressure

- Trend: cloud spend +~18% (2024) → less hardware, more platform dependency

Regulatory and compliance service inputs

Regulatory and compliance service inputs for HCL demand rigorous background checks, facility security and certified compliance tools in regulated deals, tightening supplier selection even as vendor diversity exists; HCL Technologies reported roughly $13.1 billion revenue in FY2024, amplifying exposure to credentialed supplier risk. Standardized control frameworks and reuse cut switching costs, but shifts in data sovereignty can force rapid vendor changes and operational disruption.

- Background checks narrow suppliers in sensitive geographies

- Facility security and certified tools are mandatory for regulated deals

- Framework reuse lowers switching costs

- Data sovereignty shifts can cause abrupt vendor swaps

Supplier power high - AWS 32% Azure 23% GCP 11%; talent strain, margins pressured

Supplier power is high: cloud platforms concentrate influence (AWS 32%, Azure 23%, Google 11% in 2024), tying pricing and roadmaps to vendors. Talent scarcity (224,000 employees; ~20% attrition FY2024) and third-party licensing raise costs and margin volatility. Hardware OEMs are concentrated (~70% top‑5), but HCLTech scale, multivendor buying and reuse reduce switching risk.

| Metric | 2024 |

|---|---|

| Cloud share (AWS/Azure/GCP) | 32% / 23% / 11% |

| Revenue (FY2024) | $12.2B |

| Employees | 224,000 |

| Attrition | ~20% |

| Top‑5 OEMs | ~70% |

| Cloud spend growth | +18% |

What is included in the product

Tailored Porter's Five Forces analysis of HCL Technologies that uncovers key drivers of competition, evaluates buyer and supplier power, assesses entry barriers and substitutes, and highlights disruptive threats and strategic levers shaping pricing, profitability, and market positioning.

A clear one-sheet Porter's Five Forces snapshot for HCL Technologies—customize pressure levels, swap in your own data, and instantly visualize strategic pressure with a spider chart; clean layout ready to copy into pitch decks or dashboards, no macros required.

Customers Bargaining Power

Large enterprises with strong procurement

Fortune 500 buyers run competitive RFPs and enforce strict rate cards, while multi-year, multi-tower contracts give them strong leverage on price and terms. HCLTech counters with outcome-based pricing and differentiated domain IP to protect margins. Its FY2024 revenue of $12.4B and documented transformation wins enhance referenceability and soften a pure cost focus.

High switching and multi-sourcing

Clients often split work across several vendors to manage risk and price, keeping switching barriers moderate—especially for commoditized IT services—while HCL Technologies reported full-year FY2024 revenue of about $12.5 billion, reflecting broad client diversification. Sticky areas such as managed operations and product engineering sustain higher retention. Strong governance and automation in large accounts raise exit frictions and increase lifetime value.

Demand for measurable outcomes

Buyers increasingly insist on business KPIs rather than effort-based hours, shifting leverage toward outcome contracts; HCL Technologies, with FY2024 revenue around $12.1 billion, markets accelerators and GenAI productivity uplifts to justify premium pricing. Missed outcomes lead to penalties and margin dilution, while co-innovation models lock longer tenures and deepen customer stickiness.

Vertical expertise expectations

Vertical expertise expectations heighten bargaining power where industry depth in BFSI, healthcare and manufacturing dictates procurement choices; HCLTech's regulatory fluency and product lineage in these sectors shifts negotiating leverage toward the vendor. In nascent verticals buyers retain leverage via pilots and PoCs, while published case studies and domain solutions reduce bake-off risk and accelerate deal closure in 2024.

- Seller strength: regulatory fluency

- Buyer leverage: pilots in nascent verticals

- Risk reduction: case studies/domain solutions

Security and compliance scrutiny

CISOs and regulators impose stringent controls that lengthen procurement and delivery cycles, raising pre-sales effort and audit timelines. Meeting high security and compliance bars narrows the competitor field and can materially lift win rates; assured compliance supports premium contracted margins. Remediation and audit requirements increase delivery cost and overhead—IBM 2024 reports average breach cost $4.45 million, underscoring buyer caution.

- lengthened cycles: higher pre-sales & audit time

- narrowed competition: improved win rates & pricing power

- higher delivery cost: remediation, audits, compliance teams

- market signal: IBM 2024 breach cost $4.45M

Outcome pricing and IP drive stickiness vs RFP pressure; $12.4B scale

Large enterprise buyers run competitive RFPs and enforce rate cards, giving them strong price leverage; HCLTech offsets this via outcome-based pricing, domain IP and FY2024 revenue of $12.4B, which improves references and softens pure cost focus. Multi-vendor sourcing keeps switching moderate for commoditized work, while managed services and co-innovation raise stickiness and lifetime value.

| Metric | Value | Impact |

|---|---|---|

| HCLTech FY2024 revenue | $12.4B | Referenceability, pricing leverage |

| Avg breach cost (2024, IBM) | $4.45M | Higher compliance demands |

What You See Is What You Get

HCL Technologies Porter's Five Forces Analysis

This preview shows the exact HCL Technologies Porter's Five Forces Analysis you'll receive—no placeholders or mockups. It is the fully formatted, final document covering competitive rivalry, threat of entrants, buyer and supplier power, and substitutes. Once you purchase, you'll get immediate access to this same ready-to-use file for download and use.

Description

From Overview to Strategy Blueprint

HCL Technologies faces moderate buyer power, intense rivalry, rising substitute threats from digital platforms, significant supplier leverage in niche tech, and barriers that moderate new entrants—this snapshot highlights strategic pressure points. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Hyperscaler and platform dependency

Cloud providers and platforms concentrate supplier power for HCLTech, with AWS (32%), Microsoft Azure (23%) and Google Cloud (11%) controlling most market share in 2024, shaping pricing and roadmap influence. Preferred partner tiers and long-term volume deals secure discounts but can lock HCLTech to vendor timelines; multicloud certifications and reusable accelerators improve switching and deployment speed. HCLTech’s FY24 revenue near $12.2B amplifies both leverage and dependence.

Specialized talent as a critical input

Scarce skills in AI, cybersecurity and product engineering push wage inflation and premium hiring; HCLTech reported roughly 224,000 employees in FY2024 and cited attrition near 20% in 2024, amplifying cost pressure. HCLTech’s global delivery model and internal academies expand supply and lower unit costs by leveraging offshore scale. Rapid technology shifts shorten upskilling cycles and raise training spend, while attrition spikes can disrupt delivery and margin mix.

Third‑party software licensing costs

Third-party licensing is a material input for HCL, with the company reporting FY2024 revenue of about $12.2B while clients face rising software costs; bundled enterprise agreements and HCL’s reseller partnerships often cut list prices, but usage-based models introduce billing volatility that can swing project margins. Increased use of open-source and proprietary IP reduces supplier dependency and can shave licensing spend across engagements.

Hardware and network vendors

Hardware and network vendors are concentrated: Dell, HPE, Cisco, Lenovo and Arista account for roughly 70% of server and network appliance shipments (IDC 2024), giving suppliers notable bargaining power; HCL mitigates this through scale purchasing, multi-vendor panels and regional logistics hubs which lower costs and supplier risk.

Supply-chain shocks have lengthened lead times by about 6–12 weeks and tightened SLAs; continued cloud migration (public cloud revenue up ~18% in 2024) reduces on-prem hardware exposure but increases dependency on platform providers.

- Concentration: top 5 OEMs ~70% (IDC 2024)

- Mitigation: scale buying, multi-vendor panels, logistics hubs

- Risk: 6–12 week lead-time elongation; SLA pressure

- Trend: cloud spend +~18% (2024) → less hardware, more platform dependency

Regulatory and compliance service inputs

Regulatory and compliance service inputs for HCL demand rigorous background checks, facility security and certified compliance tools in regulated deals, tightening supplier selection even as vendor diversity exists; HCL Technologies reported roughly $13.1 billion revenue in FY2024, amplifying exposure to credentialed supplier risk. Standardized control frameworks and reuse cut switching costs, but shifts in data sovereignty can force rapid vendor changes and operational disruption.

- Background checks narrow suppliers in sensitive geographies

- Facility security and certified tools are mandatory for regulated deals

- Framework reuse lowers switching costs

- Data sovereignty shifts can cause abrupt vendor swaps

Supplier power high - AWS 32% Azure 23% GCP 11%; talent strain, margins pressured

Supplier power is high: cloud platforms concentrate influence (AWS 32%, Azure 23%, Google 11% in 2024), tying pricing and roadmaps to vendors. Talent scarcity (224,000 employees; ~20% attrition FY2024) and third-party licensing raise costs and margin volatility. Hardware OEMs are concentrated (~70% top‑5), but HCLTech scale, multivendor buying and reuse reduce switching risk.

| Metric | 2024 |

|---|---|

| Cloud share (AWS/Azure/GCP) | 32% / 23% / 11% |

| Revenue (FY2024) | $12.2B |

| Employees | 224,000 |

| Attrition | ~20% |

| Top‑5 OEMs | ~70% |

| Cloud spend growth | +18% |

What is included in the product

Tailored Porter's Five Forces analysis of HCL Technologies that uncovers key drivers of competition, evaluates buyer and supplier power, assesses entry barriers and substitutes, and highlights disruptive threats and strategic levers shaping pricing, profitability, and market positioning.

A clear one-sheet Porter's Five Forces snapshot for HCL Technologies—customize pressure levels, swap in your own data, and instantly visualize strategic pressure with a spider chart; clean layout ready to copy into pitch decks or dashboards, no macros required.

Customers Bargaining Power

Large enterprises with strong procurement

Fortune 500 buyers run competitive RFPs and enforce strict rate cards, while multi-year, multi-tower contracts give them strong leverage on price and terms. HCLTech counters with outcome-based pricing and differentiated domain IP to protect margins. Its FY2024 revenue of $12.4B and documented transformation wins enhance referenceability and soften a pure cost focus.

High switching and multi-sourcing

Clients often split work across several vendors to manage risk and price, keeping switching barriers moderate—especially for commoditized IT services—while HCL Technologies reported full-year FY2024 revenue of about $12.5 billion, reflecting broad client diversification. Sticky areas such as managed operations and product engineering sustain higher retention. Strong governance and automation in large accounts raise exit frictions and increase lifetime value.

Demand for measurable outcomes

Buyers increasingly insist on business KPIs rather than effort-based hours, shifting leverage toward outcome contracts; HCL Technologies, with FY2024 revenue around $12.1 billion, markets accelerators and GenAI productivity uplifts to justify premium pricing. Missed outcomes lead to penalties and margin dilution, while co-innovation models lock longer tenures and deepen customer stickiness.

Vertical expertise expectations

Vertical expertise expectations heighten bargaining power where industry depth in BFSI, healthcare and manufacturing dictates procurement choices; HCLTech's regulatory fluency and product lineage in these sectors shifts negotiating leverage toward the vendor. In nascent verticals buyers retain leverage via pilots and PoCs, while published case studies and domain solutions reduce bake-off risk and accelerate deal closure in 2024.

- Seller strength: regulatory fluency

- Buyer leverage: pilots in nascent verticals

- Risk reduction: case studies/domain solutions

Security and compliance scrutiny

CISOs and regulators impose stringent controls that lengthen procurement and delivery cycles, raising pre-sales effort and audit timelines. Meeting high security and compliance bars narrows the competitor field and can materially lift win rates; assured compliance supports premium contracted margins. Remediation and audit requirements increase delivery cost and overhead—IBM 2024 reports average breach cost $4.45 million, underscoring buyer caution.

- lengthened cycles: higher pre-sales & audit time

- narrowed competition: improved win rates & pricing power

- higher delivery cost: remediation, audits, compliance teams

- market signal: IBM 2024 breach cost $4.45M

Outcome pricing and IP drive stickiness vs RFP pressure; $12.4B scale

Large enterprise buyers run competitive RFPs and enforce rate cards, giving them strong price leverage; HCLTech offsets this via outcome-based pricing, domain IP and FY2024 revenue of $12.4B, which improves references and softens pure cost focus. Multi-vendor sourcing keeps switching moderate for commoditized work, while managed services and co-innovation raise stickiness and lifetime value.

| Metric | Value | Impact |

|---|---|---|

| HCLTech FY2024 revenue | $12.4B | Referenceability, pricing leverage |

| Avg breach cost (2024, IBM) | $4.45M | Higher compliance demands |

What You See Is What You Get

HCL Technologies Porter's Five Forces Analysis

This preview shows the exact HCL Technologies Porter's Five Forces Analysis you'll receive—no placeholders or mockups. It is the fully formatted, final document covering competitive rivalry, threat of entrants, buyer and supplier power, and substitutes. Once you purchase, you'll get immediate access to this same ready-to-use file for download and use.